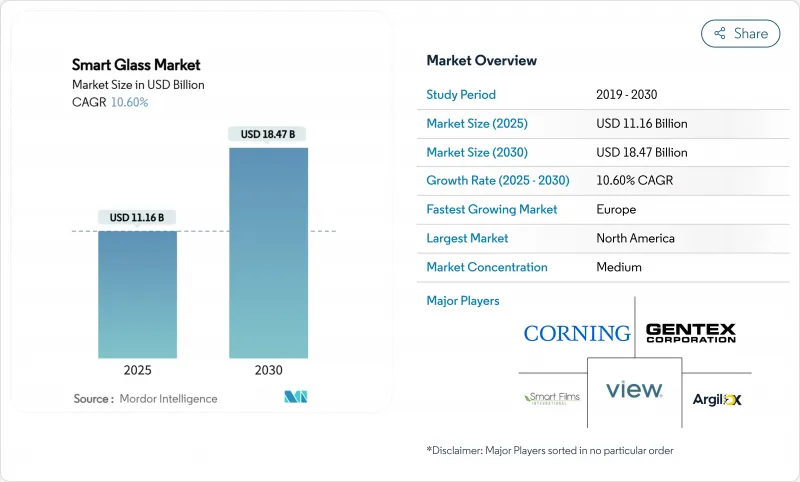

세계의 스마트 글래스 시장은 2025년 111억 6,000만 달러, 2030년 184억 7,000만 달러에 이르고, CAGR 10.60%로 확대될 것으로 예측됩니다.

이 궤도를 뒷받침하고 있는 것은 에너지 성능 규정의 의무화, 일렉트로크로믹의 효율 향상, 기술의 투자 회수 사이클을 단축하는 자동차의 프리미엄화입니다. 상업시설의 주택은 HVAC 비용 억제를 선호하며, 자동차 OEM은 동적 선루프를 이익률이 높은 트림에 번들링하고 재료 과학자는 제조 비용을 낮추는 무전극 장치에 집중하고 있습니다. 동시에 첨단 제조업과 5G 대응 외관에 대한 정부 인센티브가 스마트 글래스 시장 기회를 확대하고 있습니다.

캘리포니아의 2025년 건축물 에너지 효율 기준과 같은 외벽 성능 기준치의 의무화는 U-팩터와 일사획득계수의 기준으로 기존의 글레이징을 뛰어넘는 일렉트로크로믹 파사드에 대한 비재량적인 수요를 창출하고 있습니다. 2024년 국제 에너지 보존 규약의 개정은 트레이드 오프의 허점을 없애고 유리 성능의 기준선을 끌어올려 이전 사이클에 비해 9.8%의 절약을 실현합니다. 네덜란드의 하이브리드 퍼니스 이니셔티브를 포함한 유럽의 유사한 조치는 리노베이션 활동을 활성화시키는 컴플라이언스 주도의 조달주기를 강화하고 있습니다. 주인이 피크시 냉방부하 감소, 녹색금융 적격성, 자산가치 향상 등을 목격하면서 스마트 글래스 시장은 지속적인 규제 추풍을 얻게 됩니다.

자동차 제조업체는 캐빈을 차별화하고 공조 부하를 줄이기 위해 다이나믹 라이트 컨트롤 루프를 도입했습니다. Renault의 Solarbay PDLC 선루프는 50% 가까운 재활용 원료를 사용하면서 부문 불투명화를 실현합니다. AGC의 SPD 기반 원더라이트 루프는 Mercedes S-클래스 쿠페에 장착되어 에어컨 수요를 줄이고 꼬리 파이프의 CO2를 줄입니다. 현대의 나노 쿨링 필름은 시험 차량에서 차내 온도를 12.33 ℃로 낮추어 주류로의 전환을 보였습니다. 자동차 설계 사이클은 3-5년이며 비용 절감은 건축 분야에도 파급되어 스마트 글래스 시장의 대응 가능 베이스가 확대됩니다.

일렉트로크로믹 윈도우의 가격은 표준 유닛이 20-30㎡인 반면 180-250㎡입니다. 애널리스트는 215m2(20ft2)를 대량 대체 크로스오버 포인트로 삼아 기술 혁신 경쟁을 촉진하고 있습니다. 무전극 일렉트로크로믹 프로토타입은 인듐주석 산화물층을 박리함으로써 비용을 80m2 USD로 줄였습니다. 플라즈마 증강 화학 기상 증착법은 연간 140만 m2 규모로 5.26m2 달러에 가까운 비용을 약속합니다. 시공업체의 숙련도가 높아짐에 따라 설치의 복잡성은 후퇴하고 있지만, 가격에 대한 저항이 비용에 민감한 스마트 글래스 시장의 가장 큰 제한 요인임에 변함이 없습니다.

2024년 스마트 글래스 시장 점유율은 일렉트로크로믹 솔루션이 43.00%를 차지했습니다. 저전력 동작, 완만한 착색, 50,000 사이클 수명이 입증되었기 때문에 대규모 외관과 기업 캠퍼스에서는 기본 옵션이 되었습니다. 일렉트로크로믹 제품의 스마트 글래스 시장 규모는 CAGR 9.8%로 2025년 48억 달러에서 2030년에는 77억 달러로 확대될 것으로 예측됩니다. 인라인 스퍼터링에서 전체 고체 화학에 이르는 비용 절감 로드맵은 설비 투자 예산을 예측 가능한 수준으로 유지합니다. 한편 하이브리드 태양전지 유리는 덴마크의 CitySolar 프로젝트에서 이미 셀 효율 12.3%를 달성한 투명 유기 태양전지를 활용해 CAGR 18.50%로 확대되고 있습니다. NEXT Energy Technologies는 이러한 패널이 건축적인 투명성을 유지하면서 일반적인 사무실 수요의 25%를 상쇄할 수 있을 것으로 추정하고 있으며, 하이브리드 유리를 일렉트로크로믹이라는 기존 기술에 과제하는 파괴자로 자리매김하고 있습니다.

부유 입자 소자 제품은 조종석, 철도 객실, 고급 세단 등 초 이하의 전환이 중요한 틈새를 유지하고 있습니다. 고분자 분산형 LCD 창은 저전압 프라이버시 파티션으로 의료실과 회의실에 침투합니다. 열 변색과 광 변색의 변화는 수동적인 기후로 제한되지만, 배선이 필요없는 설치는 복고풍 예산에 호소합니다. 따라서 기술 스택은 이분화됩니다. 에너지 의무화에는 일렉트로크로믹, 넷 제로 파사드에는 하이브리드 PV, 스피드와 프라이버시의 이용 사례에는 SPD와 PDLC가 대응합니다.

상업용 부동산 용도는 사무실 및 소매점에서 광범위한 사용으로 2024년 매출의 38.20%를 차지했습니다. 이 부문에서는 에너지 절약, 일광 최적화, ESG 인증이 프리미엄 비용의 정당성을 입증합니다. 상업용 부동산 스마트 글래스 시장 규모는 CAGR 9.6%로 성장해 2025년 42억 7,000만 달러에서 2030년에는 67억 5,000만 달러에 달할 것으로 예측됩니다. 그러나 헬스케어는 감염 제어 프로토콜이 터치 프리 프라이버시를 우선시하기 때문에 CAGR 17.50%의 급성장을 확보하고 있습니다. 집중 치료 병동에서는 커튼의 세탁을 줄이기 위해 순간적으로 불투명해지는 PDLC 패널이 채용되고, 정신과 병동에서는 환자의 감시와 존엄의 균형을 잡기 위해 깨지기 어려운 동적 유리가 채용되고 있습니다.

자동차용 글레이징은 세 번째 수익의 기둥이며, 특히 럭셔리 자동차 및 전기자동차에서는 동적 채광창이 배터리를 소모하는 에어컨을 보완하고 있습니다. 주택으로의 도입은 늦었지만 세제 우대조치와 모듈 가격 하락으로 고성능 주택의 ROI가 변화하고 있습니다. 항공우주, 철도, 해양은 소규모이면서 꾸준히 진전하고 있으며, 가전은 소형화된 일렉트로크로믹 스크린이나 AR 헤드셋을 시험하고 있습니다.

스마트 글래스 시장 보고서는 기술 유형(일렉트로크로믹, 써모크로믹, 포토크로믹, 기타), 최종 사용자(자동차, 아비오닉스, 해양, 소매, 기타), 제어 모드(유선 스위치, 월 패널, 리모트, RF 컨트롤러, 디밍 패널, 슬라이더, 기타), 용도(파사드, 커튼월, 인테리어 파티션, 프라이버시), 지역으로 구분됩니다.

북미는 캘리포니아의 건축 기준법이 글레이징 기준치를 인상하고 연방 정부의 CHIPS법이 고순도 유리 공장에 인센티브를 주었기 때문에 2024년 매출의 34.70%를 차지했습니다. Corning의 뉴욕에서 3억 1,500만 달러 용융 실리카의 확장은 리드 타임을 단축하고 5년간의 서비스 보증을 맡는 지역 공급망의 성숙을 보여줍니다. 이 지역의 스마트 글래스 시장은 파노라마 루프의 OEM 수요와 연방 정부 시설을 대상으로 한 관민 개보수 프로그램에도 지원됩니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 14.60%를 기록했으며, 중국의 BOE에 의한 88억 달러의 OLED 캠퍼스, 일본의 5G 파사드 파일럿, 한국의 EV 유리 업그레이드에 추진되고 있습니다. Fuyao와 같은 중국 제조업체는 58억 위안 오토그레이드 생산 능력을 추가하고 판매 가격을 압축하는 규모의 경제를 증폭하고 있습니다. 산화텅스텐의 전구체 규제가 공급 위험이 되는 반면, 지방정부는 전략적 자치를 강화하기 위해 현지 채굴과 재활용을 가속화하고 있습니다.

유럽은 EPC 등급의 엄격화와 보수 보조금에 의해 지원되고 안정적인 속도로 전진하고 있습니다. 산고방의 저탄소 ORAE 유리와 AGC 인터페인의 다중 거점 전개는 재활용 소재와 넷 제로 제조에 대한 지역적 주력을 입증하고 있습니다. 그러나 전기 요금이 상승하고 중복되는 허가의 틀은 대중 주택의 수익성을 낮추어 상업용 타워와 프리미엄 리노베이션에 수요를 유도하고 있습니다. 이러한 역학이 결합되어 지리적으로 다양화된 시장 역학이 유지되고 있습니다.

The smart glass market stands at USD 11.16 billion in 2025 and is forecast to post USD 18.47 billion by 2030, expanding at a 10.60% CAGR.

This trajectory is propelled by mandatory energy-performance codes, electrochromic efficiency gains, and premium automotive adoption that shortens technology payback cycles. Commercial landlords are prioritizing HVAC cost control, automotive OEMs are bundling dynamic sunroofs into high-margin trims, and materials scientists are converging on electrode-free devices that lower production costs. Simultaneously, government incentives for advanced manufacturing and 5G-ready facades are enlarging the smart glass market opportunity set.

Mandatory envelope performance thresholds such as California's 2025 Building Energy Efficiency Standards are creating non-discretionary demand for electrochromic facades that outperform conventional glazing on U-factor and Solar Heat Gain Coefficient criteria. The 2024 International Energy Conservation Code revision delivers 9.8% incremental savings versus the prior cycle, eliminating trade-off loopholes and elevating glass performance baselines. Similar measures in Europe, including the Netherlands' hybrid-furnace initiative, reinforce a compliance-driven procurement cycle that lifts retrofit activity. As owners witness lower peak cooling loads, green-finance eligibility, and enhanced asset values, the smart glass market gains a durable regulatory tailwind.

Automakers are deploying dynamic light-control roofs to differentiate cabins and trim HVAC loads. Renault's Solarbay PDLC sunroof supplies segmental opacification while using nearly 50% recycled content. AGC's SPD-based Wonderlite roof on the Mercedes S-Class Coupe cuts air-conditioning demand and lowers tailpipe CO2. Hyundai's Nano Cooling Film shows mainstream migration by shaving interior temperatures by 12.33 °C in pilot fleets. Automotive design cycles of 3-5 years accelerate cost degression that cascades into the building sector, expanding the smart glass market addressable base.

Electrochromic windows still price at USD 180-250 m2 against USD 20-30 m2 for standard units. Analysts peg USD 215 m2 (USD 20 ft2) as the crossover point for mass substitution, prompting an innovation race. Electrode-free electrochromic prototypes have sliced costs toward USD 80 m2 by stripping indium-tin-oxide layers. Plasma-enhanced chemical vapor deposition promises costs near USD 5.26 m2 at 1.4 million m2 annual scale. Installation complexity is receding as contractor familiarity grows, but price resistance remains the foremost limiting factor in cost-sensitive slices of the smart glass market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Electrochromic solutions dominated 2024 with 43.00% smart glass market share. Their low-power operation, gradual tinting, and proven 50,000 cycle life make them the default choice for large facades and corporate campuses. The smart glass market size for electrochromic products is projected to expand from USD 4.80 billion in 2025 to USD 7.70 billion by 2030 at a 9.8% CAGR. Cost-out roadmaps ranging from in-line sputtering to all-solid-state chemistries keep capex budgets predictable. Meanwhile, hybrid photovoltaic glass is scaling at an 18.50% CAGR, leveraging transparent organic photovoltaics that already hit 12.3% cell efficiency in Denmark's CitySolar project. NEXT Energy Technologies estimates these panels could offset 25% of typical office demand while retaining architectural clarity, positioning hybrids as the disruptor that challenges electrochromic incumbency.

Suspended Particle Device products maintain a niche where sub-second switching is critical-cockpits, rail cabins, and luxury sedans. Polymer-Dispersed Liquid Crystal windows are penetrating healthcare suites and conference rooms as low-voltage privacy partitions. Thermochromic and photochromic variants stay limited to passive climates, yet their wiring-free installation appeals to retrofit budgets. The technology stack is therefore bifurcating: electrochromic for energy mandates and hybrid PV for net-zero facades, with SPD and PDLC covering speed and privacy use cases.

Commercial real-estate applications captured 38.20% of 2024 revenue through broad office and retail uptake. The segment relied on energy savings, daylight optimization, and ESG credentialing to justify premium costs. Smart glass market size for commercial real estate is forecast to grow at 9.6% CAGR, moving from USD 4.27 billion in 2025 to USD 6.75 billion in 2030. Healthcare, however, secures the steepest 17.50% CAGR as infection-control protocols privilege touch-free privacy. Intensive-care wards deploy instant-opaque PDLC panels to reduce curtain laundering, while psychiatric units harness break-resistant dynamic glass to balance patient oversight with dignity.

Automotive glazing remains the third revenue pillar, particularly within luxury and electric vehicles, where dynamic skylights offset battery-draining HVAC. Residential uptake is slower, but tax incentives and lower module prices are shifting the ROI narrative for high-performance homes. Aerospace, rail, and marine progress steadily, albeit off smaller bases, and consumer electronics experiment with miniaturized electrochromic screens and AR headsets.

Smart Glass Market Report is Segmented by Technology Type (Electrochromic, Thermochromic, Photochromic, and More), End User (Automotive, Avionics, Marine, Retail, and More), Control Mode (Wired Switch / Wall Panel, Remote / RF Controller, Dimming Panel / Slider, and More), Application (Facades and Curtain Walls, Interior Partitions and Privacy Panels, and More), and Geography.

North America anchored 34.70% of 2024 revenue as California's building code raised glazing baselines and the federal CHIPS Act funnelled incentives to high-purity glass fabs. Corning's USD 315 million fused-silica expansion in New York exemplifies local supply-chain maturation that lowers lead times and underwrites five-year service warranties. The regional smart glass market is also buoyed by OEM demand for panoramic roofs and public-private retrofit programmes targeting federal properties.

Asia Pacific charts the fastest 14.60% CAGR through 2030, propelled by China's BOE USD 8.8 billion OLED campus, Japan's 5G facade pilots, and South Korea's EV-glass upgrades. Chinese producers such as Fuyao are adding CNY 5.8 billion of auto-grade capacity, amplifying economies of scale that compress selling prices. While tungsten-oxide precursor restrictions pose supply risk, regional governments are accelerating localised mining and recycling to fortify strategic autonomy.

Europe advances at a stable pace underpinned by stricter EPC ratings and renovation-wave subsidies. Saint-Gobain's low-carbon ORAE glass and AGC Interpane's multi-site expansion validate a regional focus on recycled content and net-zero manufacturing. However, elevated electricity prices and overlapping permitting frameworks dampen return profiles in mass-market housing, steering demand toward commercial towers and premium retrofits. Together, these dynamics sustain a geographically diversified smart glass market footprint.