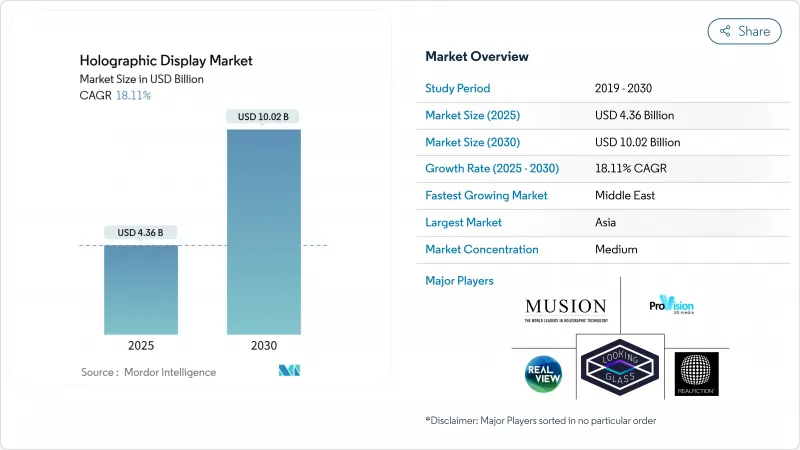

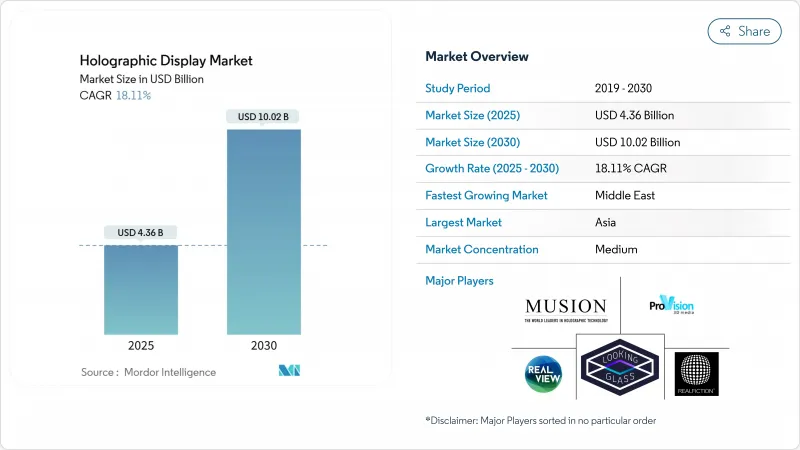

홀로그래픽 디스플레이 시장 규모는 2025년에 43억 6,000만 달러로 추정되고, 2030년에는 100억 2,000만 달러에 이를 전망이며, CAGR 18.11%로 성장할 것으로 예측됩니다.

왕성한 수요는 자동차의 프리미엄 브랜드가 증강현실 헤드업 디스플레이를 전개하고, 미국의 일류 병원이 용적 측정 수술실을 설치하거나, 고급 소매점이 360도 사이니지를 채용하는 것에 기인하고 있습니다. 이러한 이용 사례는 마이크로 LED 도파관의 수율이 향상되고 AI 주도 컨텐츠 엔진이 제작 비용을 절감함에 따라 연구 파일럿에서 생산 전개로의 결정적인 전환을 시사합니다. 독일과 중국의 자동차 제조업체들이 앞유리 도입의 대부분을 차지하는 반면, 미국 의료 기관은 수술실의 계획 주기를 단축하는 3D 이미지 구매를 가속화하고 있습니다. 아시아는 계속해서 생산 규모와 컨텐츠 혁신을 주도하고 있으며, 중동의 소매 부문은 가장 빠른 지역 확대를 실현하고 있습니다. 광학, 경쟁 및 컨텐츠 제작의 융합은 기업이 몰입형 경험을 수익화하고 지속적인 경쟁 우위를 창출할 수 있는 생태계를 지원합니다.

독일의 고급 자동차 제조업체와 중국의 전기자동차 브랜드는 프리미엄 트림을 차별화하고 운전자의 상황 인식을 높이기 위해 전면 유리 전면에 홀로그램 헤드업 디스플레이를 탑재하고 있습니다. 2025년 CES에서 전시된 현대모비스의 컨셉은 3가지 표시 영역에 내비게이션 신호, 경보, 엔터테인먼트 컨텐츠를 투영하는 것으로, 자이스와의 공동 개발로 2027년까지 양산을 목표로 하고 있습니다. 시장 예측에 따르면 2030년까지 700만대의 자동차가 출하되어 대시보드 영역이 몰입형 AR 캔버스로 변환된다고 합니다.

병원은 종양학, 심장병학 및 정형외과를 위해 진정한 깊이의 홀로그램에 눈을 돌리고 있습니다. RealView Imaging의 HOLOSCOPE-i는 외과의사가 실시간으로 3D 해부학적 구조를 조작할 수 있게 하고, 계획에 소요되는 시간을 단축하며, 수술실에서 실수를 줄여줍니다. 임상 연구에서는 특히 비코플라나 방사선 치료 빔에 대해 2D법보다 홀로그래픽 플랜이 61% 선호된다는 결과가 나왔습니다.

효율적인 도파로에 필요한 나노스케일의 공차를 달성할 수 있는 팹은 거의 없기 때문에 가격은 LCD나 OLED의 대체품보다 40-60% 높게 유지되고 있습니다. 소니의 0.44인치 Full HDOLED 마이크로디스플레이의 샘플 가격은 260달러(4만 엔)를 넘어 소비자용 디바이스의 경제성을 제한하고 있습니다.

하드웨어는 2024년 매출의 75.6%를 차지했으며, 홀로그래픽 디스플레이 시장을 지원하는 공간 광 변조기, 레이저 엔진, 정밀 광학 부품의 자본 집약도를 부각하고 있습니다. 프로젝터, 광도파로 및 마이크로디스플레이 엔진은 여전히 비용 드라이버이지만 부품 가격 하락으로 인해 홀로그래픽 디스플레이 시장 규모의 하드웨어 점유율은 10년 후까지 소폭 감소할 전망입니다. 기업이 턴키 도입, 캘리브레이션, 라이프사이클 지원 계약을 요구하고 있기 때문에 서비스는 이미 가장 빠른 CAGR 22.7%로 성장을 지속하고 있습니다. 통합 전문가는 온프레미스에서 설치, 클라우드 렌더링 및 교육을 번들로 제공하여 단발 장비 판매를 다년간 계약으로 바꾸고 있습니다. 헬스케어 네트워크는 수술 계획실의 가동 시간을 보장하는 서비스 수준 계약을 지정하며, 자동차 제조업체는 광학 시스템의 정렬을 Tier 1 공급업체에 위임합니다. 따라서 홀로그래픽 디스플레이 시장은 하드웨어 마진 의존에서 부속 서비스 연금으로 이동하고 있습니다.

병행하여 소프트웨어 스택은 실시간 렌더링, AI에 의한 컨텐츠 작성, 애널리틱스를 추가하고 물리적 기기 위에 구독 수입을 거듭합니다. 이 추세는 컨텐츠 관리 플랫폼이 필수적인 프로젝션 및 사이니지 업계에서 이전의 전환을 모방합니다. 볼류메트릭 스트리밍이 보급됨에 따라 대역폭 최적화 및 보안 패치가 서비스 기회를 더욱 확대할 것으로 보입니다. 하드웨어 벤더는 현재 내부에 전문 서비스 그룹을 설립하거나 시스템 통합사업자와 제휴하여 광학, 펌웨어 및 관리 컨텐츠 간의 긴밀한 협력을 보장합니다.

일렉트로 홀로그래픽 아키텍처는 성숙한 액정 온실리콘과 반사형 공간 광 변조기 공급망으로 2024년 40.8%의 매출을 획득했습니다. 안정적인 수율과 확립된 설계 도구 세트를 통해 이 형식은 차량용 HUD 및 의료용 스캐너에 안전한 옵션이 되었으며 홀로그래픽 디스플레이 시장에서의 리드를 유지하고 있습니다. 한편, 햅틱 공중 시스템은 CAGR 24.6%로 성장을 지속하고 있습니다. 개발자가 위상 배열 초음파와 부피 비주얼을 결합하여 사용자는 부동 인터페이스를 '만질' 수 있습니다. 제스처 기반의 상품 회전을 가능하게 하는 소매점의 연단이나 무균의 인터랙션을 가능하게 하는 병원의 디스플레이는 상업적인 견인력의 일례입니다.

레이저 및 플라즈마 투영 솔루션은 야외 스테이지 쇼 및 대시보드 태양광 조건과 같은 극단적인 밝기 시나리오를 목표로 하며 반투명 도파관은 AR 스마트 글라스에 유용합니다. POSTECH이 발표한 메타서피스 광학 부품은 색수차를 보정하고, 컬러 매니지먼트를 간소화하며, 디바이스 프로파일을 슬림화합니다. 음향 및 광자 트랩의 연구 라인은 효율성을 재정의할 수 있지만, 상업화는 현재 예측에서 어렵습니다. 전반적으로 기존의 일렉트로홀로그래픽 공급업체는 홀로그래픽 디스플레이 시장에서 급속히 상승하는 촉각 과제를 퇴치하기 위해 전력, 해상도 및 상호작용을 혁신해야 합니다.

아시아태평양은 중국 전기자동차 붐, 일본 엔터테인먼트 기술, 한국 반도체 에코시스템을 활용해 2024년 매출의 36.9%를 창출했습니다. 민간 프로그램은 마이크로 LED 백플레인과 메타 서피스 광학에 인센티브를 부어 지역 공급의 우위를 강화하고 있습니다. 아시아태평양의 홀로그래픽 디스플레이 시장 규모는 도쿄, 서울, 상하이의 고밀도 소매 전개에서도 혜택을 누리고 있습니다. 유럽은 차이스와 현대와 같은 협업이 혁신의 파이프라인을 유지하고 있는 반면, 자동차 설계의 승리가 성장을 억제하는 밝기의 한계에 직면하고 있습니다.

북미는 외과 수술용 비주얼리제이션 스위트를 업그레이드하는 미국의 일류 병원과 용적형 미션플래닝 테이블을 조달하는 방위 기관을 중심으로 꾸준한 기세를 보이고 있습니다. 캐나다의 라이브 이벤트 프로모터는 홀로그램 페스티벌을 시도해 시장 범위를 확대합니다. 중동에서는 2030년까지 CAGR 21.5%로 가장 높은 성장이 전망되며, 두바이, 리야드, 도하의 고급 몰이 브랜드의 스토리성을 높이는 360도 홀로그래픽 쇼케이스에 다액의 투자를 실시했습니다. 아부다비와 네옴의 정부 스마트 시티 이니셔티브는 추가 실험을 촉진합니다.

라틴아메리카 및 아프리카는 수입 관세와 대역폭 제한에 제약을 받았으며 아직 초기 단계에 머물렀지만 상파울루 소매업과 남아프리카 광업 시각화의 조종사 프로젝트는 강하로의 확대를 시사합니다. 그러나 세계 공급망은 일본과 한국을 통해 중요한 도파관 제조를 통해 모든 지역을 잠재적인 병목에 노출시킵니다.

The holographic display market size is estimated posted a current value of USD 4.36 billion in 2025, and it is on track to reach USD 10.02 billion by 2030, supported by an 18.11% CAGR.

Robust demand stems from automotive premium brands rolling out augmented-reality head-up displays, tier-1 U.S. hospitals installing volumetric surgical suites, and luxury retailers adopting 360-degree signage. These use-cases signal a decisive move from research pilots to production roll-outs as micro-LED waveguide yields improve and AI-driven content engines cut creation costs. German and Chinese automakers account for the bulk of windshield deployments, while U.S. health providers accelerate 3D imaging purchases that shorten operating-room planning cycles. Asia continues to lead production scale and content innovation, whereas the Middle East's retail sector delivers the fastest regional expansion. The convergence of optics, computing, and content creation underpins an ecosystem where enterprises can monetize immersive experiences and create durable competitive advantage.

German luxury marques and Chinese electric-vehicle brands are integrating full-windshield holographic head-up displays to differentiate premium trims and enhance driver situational awareness. Hyundai Mobis' concept shown at CES 2025 projects navigation cues, alerts, and entertainment content across three viewing zones, and joint development with Zeiss targets mass production by 2027. Market forecasts suggest 7 million automotive units will ship by 2030, converting dashboard real estate into immersive AR canvases.

Hospitals are turning to true-depth holograms for oncology, cardiology, and orthopedics. RealView Imaging's HOLOSCOPE-i enables surgeons to manipulate 3D anatomy in real time, trimming planning hours and reducing operating-room errors. Clinical studies show 61% preference for holographic plans over 2D methods, especially for non-coplanar radiotherapy beams.

Few fabs can achieve the nanoscale tolerances required for efficient waveguides, keeping prices 40-60% above LCD or OLED alternatives. Sample quotes for Sony's 0.44-type Full HD OLED microdisplay exceed USD 260 (JPY 40,000), restricting consumer-device economics.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware accounted for 75.6% of 2024 revenue, underscoring the capital intensity of spatial-light modulators, laser engines, and precision optics that underpin the holographic display market. Projectors, optical waveguides, and microdisplay engines remain cost drivers, yet falling component prices will push the hardware share of the holographic display market size down modestly by the decade's close. Services already command the fastest 22.7% CAGR as enterprises look for turnkey deployment, calibration, and lifecycle support agreements. Integration specialists bundle on-premises installation, cloud rendering, and training, converting one-off device sales into multi-year contracts. Healthcare networks specify service-level agreements that guarantee uptime for surgical planning suites, while automakers outsource optical system alignment to tier-1 suppliers. The holographic display market is therefore shifting from hardware margin dependency to attached-service annuities.

In parallel, software stacks add real-time rendering, AI-assisted content creation, and analytics, layering subscription revenue atop physical equipment. The trend mimics earlier transitions in the projection and signage industries, where content-management platforms became indispensable. As volumetric streaming proliferates, bandwidth optimization and security patches will further enlarge the services opportunity. Hardware vendors now incubate internal professional-services groups or ally with systems integrators, ensuring tight coupling between optics, firmware, and managed content-an approach that strengthens ecosystem lock-in across the holographic display industry.

Electro-holographic architectures captured 40.8% revenue in 2024 thanks to mature liquid-crystal-on-silicon and reflective spatial-light-modulator supply chains. Stable yields and established design toolsets make the format the safe choice for automotive HUDs and medical scanners, sustaining its lead in the holographic display market. Meanwhile, haptic mid-air systems clock a 24.6% CAGR as developers combine phased-array ultrasounds with volumetric visuals to let users "touch" floating interfaces. Retail podiums that permit gesture-based product rotation and hospital displays allowing sterile interaction exemplify commercial traction.

Laser/plasma projection solutions target extreme-brightness scenarios such as open-air stage shows and dashboard sunlit conditions, while semi-transparent waveguides serve AR smart-glasses. Metasurface optics unveiled by POSTECH help correct chromatic aberration, simplifying color management and slimming device profiles. Acoustic and photon-trap research lines could redefine efficiency, yet commercialization sits beyond the current forecast horizon. Overall, incumbent electro-holographic vendors must innovate on power, resolution, and interaction to fend off fast-rising haptic challengers in the holographic display market.

The Holographic Display Market Report is Segmented by Component (Hardware, Software, Services), Technology (Electro-Holographic, Touchable/Mid-Air Haptic, and More), Product Type (Digital Signage and Kiosks, Smart TVs and Monitors, and More), End-User (Consumer Electronics, Retail and Exhibition, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific generated 36.9% of 2024 revenue, leveraging China's electric-vehicle boom, Japan's entertainment tech, and South Korea's semiconductor ecosystem. Public-private programs funnel incentives into micro-LED backplanes and metasurface optics, fortifying regional supply dominance. The holographic display market size attributed to Asia Pacific also benefits from dense retail deployments in Tokyo, Seoul, and Shanghai. Europe follows with automotive design wins but faces brightness restrictions that temper growth, although collaborations such as Zeiss-Hyundai sustain innovation pipelines.

North America exhibits steady momentum anchored by U.S. tier-1 hospitals that upgrade surgical visualization suites and defense agencies procuring volumetric mission-planning tables. Canada's live-event promoters experiment with hologram festivals, extending market reach. The Middle East posts the highest 21.5% CAGR through 2030 as luxury malls in Dubai, Riyadh, and Doha invest heavily in 360-degree holographic showcases that elevate brand storytelling. Government smart-city initiatives in Abu Dhabi and Neom foster further experimentation.

Latin America and Africa remain early-stage, constrained by import duties and bandwidth limitations, yet pilot projects in Sao Paulo retail and South African mining visualization hint at downstream expansion. Global supply chains nonetheless route critical waveguide fabrication through Japan and South Korea, exposing all regions to potential bottlenecks, a factor that stakeholders across the holographic display market monitor closely for risk mitigation.