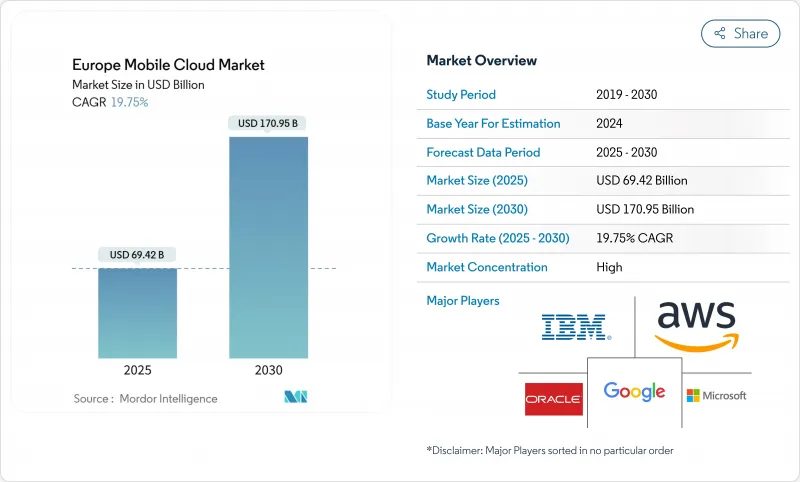

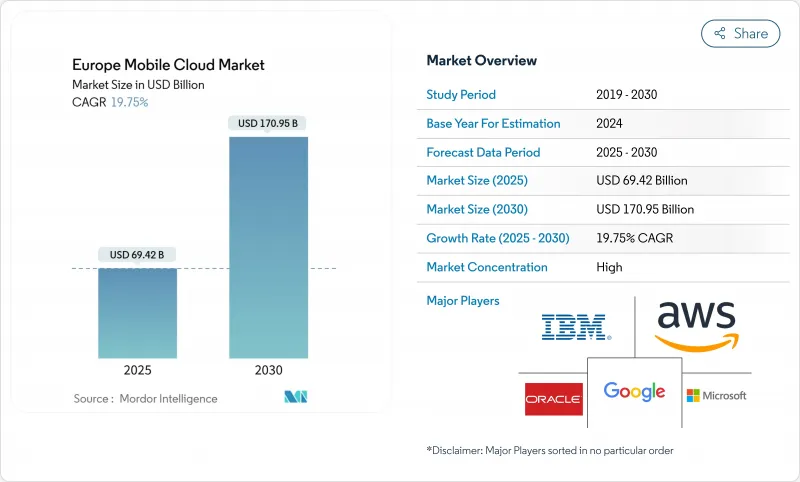

유럽의 모바일 클라우드 시장 규모는 2025년 694억 2,000만 달러로, 2030년에는 CAGR 19.75%를 기록해 1,709억 5,000만 달러로 확대될 것으로 예측됩니다.

소버린 클라우드 프레임워크 채용 증가, 5G 독립형(SA) 커버리지 확대, 저지연 모바일 워크로드에 대한 기업의 주목의 고조가 이 궤도를 뒷받침하고 있습니다. 또한 5G SA 네트워크는 이미 10밀리초 이하의 왕복 레이턴시를 실현하고 있으며, 실시간 산업, 게임, 핀테크 이용 사례에 새로운 수요가 탄생하고 있습니다. Deutsche Telekom의 NVIDIA가 지원하는 탑재한 산업용 AI 클라우드 등 통신 사업자와 클라우드의 제휴는 통신 사업자가 AI 워크로드의 인프라 공급업체로 변모하고 있음을 나타냅니다. 동시에 하이퍼스케일러 시장 파워에 대한 규제 당국의 감시는 이그레스 비용의 철폐를 포함한 가격 재구성을 촉구하고, 이로 인해 스위칭 장벽이 저하되고 멀티클라우드 전략이 촉진되고 있습니다.

유럽 위원회의 EuroStack 프로그램은 2030년까지 10,000개의 분산 에지 클라우드 노드를 목표로 하고 있으며, 엄격한 데이터 거주 규정을 충족하는 로컬 처리 지점을 구축하고 있습니다. Orange와 Capgemini의 Bleu 플랫폼은 2024년에 SecNumCloud 규칙을 기반으로 Microsoft 기술을 제공하기 위해 시작되었으며 규정 준수 우선 서비스가 기밀성 있는 워크로드를 유치할 수 있음을 입증했습니다. 곧 시작되는 EU 클라우드 서비스 체계는 주권과 보안의 기준에 비추어 공급자를 인증하고, 지금까지 역외에 호스팅되었던 중요한 부문의 데이터의 본국 송환을 가속시킵니다. 동시에 EU 데이터법은 벤더에게 2027년 1월까지 전환 수수료를 폐지할 것을 의무화하고 있으며, 락인 경제를 약체화시키고 경쟁 생태계에 인센티브를 부여합니다. 공공기관이 조달 규칙을 적응함에 따라 유럽 기업들은 규제 산업과 관련된 클라우드 수요가 크게 증가할 것으로 예측됩니다.

독일, 영국, 이탈리아, 스페인 등 세계에서 60개 이상의 사업자가 상용 5G SA 네트워크를 시작하고 있습니다. 네트워크 슬라이싱은 모바일 클라우드 용도 요구사항에 맞는 지연 및 대역폭 클래스를 미리 정의하고 프리미엄 서비스 계층을 통해 직접 수익을 창출합니다. Deutsche Telekom의 5G+ Gaming 파일럿은 클라우드 게임 트래픽의 엔드 투 엔드 지연이 10ms 이하임을 이미 입증했습니다. GSMA는 2030년까지 5G가 가져온 유럽의 경제 가치를 1,640억 유로로 예측하고 있지만, 대부분은 SA의 전개에 의존하고 있습니다. O2 Telefonica의 클라우드 네이티브 듀얼 모드 코어와 같은 핵심 네트워크 업그레이드는 유지 보수 가동 중지 시간을 더욱 줄이고 지속적인 기능 릴리스를 가능하게 합니다.

영국 경쟁 시장 당국은 AWS와 Microsoft가 각각 국내 클라우드 비용의 30-40%를 지배하고 있음을 밝히고 상호 운용성과 가격 시정을 강제할 수 있는 전략적 시장 지위 의무를 제안했습니다. 경쟁 개혁으로 영국 기업은 연간 4억 3천만 파운드를 절약할 수 있습니다. 브뤼셀에서 디지털 시장법 시행과 병행하여 '게이트키퍼' 플랫폼은 소프트웨어 라이선스와 클라우드 사용을 연결하는 한계를 포함한 추가 컴플라이언스 계층을 추가합니다. AWS와 Microsoft 양사는 최종 재정에 앞서 공급자를 변경하는 고객의 이그레스 비용을 먼저 철폐하고 행동 조정을 실시했습니다. 이러한 양보는 고객을 돕는 반면 공급자 마진을 압축하고 단기 투자 페이스를 줄일 수 있습니다.

기업이 성능 보증과 주권 준수를 우선시했기 때문에 엔터프라이즈 워크로드는 2024년 유럽 모바일 클라우드 시장 매출의 67%를 차지했습니다. BBVA와 같은 금융 기관은 클라우드 네이티브 데이터 플랫폼으로 전환하여 분석 시간이 94% 단축되었음을 강조합니다. 이러한 측정 가능한 성과는 할인된 계약 금액을 정당화하고 지속적인 인프라 투자에 박차를 가하고 있습니다. 소비자의 도입은 소규모이지만 클라우드 게임의 구독이나 모바일 엔터테인먼트 번들에 의해 CAGR 19.90%로 급속히 확대하고 있습니다. Telefonica Germany는 100만 명의 5G 사용자를 AWS 핵심 클라우드로 전환하고 기업과 소비자의 밸류체인을 융합시켜 차별화된 네트워크 서비스가 두 부문 모두에서 수익을 창출할 수 있음을 입증했습니다. 기업이 유럽의 모바일 클라우드 시장의 기반이 되는 것은 아니지만, 소비자의 성장은 수익을 다양화하고 기업의 예산주기에 대한 쿠션이 됩니다.

소비자 중심의 성장은 인구 집중 지역 근처에 위치한 엣지 컴퓨팅 노드와의 연관성을 강화하여 그래픽을 많이 사용하는 타이틀과 비디오 스트리밍 지터를 줄입니다. 네트워크 사업자는 홀세일 트래픽 증가로부터 혜택을 받고, 하이퍼스케일러는 대도시권의 포인트 오브 프레즌스에 컨텐츠 캐쉬를 분산시킵니다. 한편, 기업 구매자들은 록인을 완화하기 위해 멀티클라우드 실적를 넓히고, Vodafone은 3대의 대규모 공급업체들 사이에 '상업적 긴장'을 유지함으로써 비용 절감을 실현하고 있습니다. 고급 FinOps 대시보드는 비즈니스 단위별 사용량을 추적하여 모든 워크로드가 최적의 비용 성능 영역에서 실행되도록 합니다. 이러한 이중 진화는 유럽 모바일 클라우드 업계의 탄력성을 유지하고 있습니다.

게이밍은 2024년 매출의 32%를 차지하며 CAGR 22.60%로 확대될 것으로 예측됩니다. Deutsche Telekom의 5G+ Gaming은 네트워크 슬라이싱이 모바일 광대역 속도에서 프레임 속도의 일관성을 보장한다는 것을 입증합니다. 금융 및 비즈니스 용도는 안전하고 낮은 지연된 파이프를 통해 전달되는 실시간 위험 분석에 의해 구동되며 그 가치는 2위를 차지합니다. 자본 시장의 중심지에 있는 기업은 알고리즘 트레이딩에 확정적인 지연 시간을 요구하고 에지에 최적화된 존에 수요를 유도하고 있습니다.

원격 학습 플랫폼과 진단 AI 워크로드가 클라우드로 이동함에 따라 교육 및 건강 관리 용도의 점유율이 계속 확대되고 있습니다. 규제 당국은 기밀성이 높은 의료 데이터를 소블린 클라우드 존에 둘 수 있도록 허락하고 있으며, 공급자는 프라이버시법을 저촉하지 않고 AI를 활용한 이미지 처리를 전개할 수 있습니다. 엔터테인먼트 플랫폼은 게임과 동일한 엣지 실적를 활용하여 버퍼링 없이 적응형 비트레이트 비디오를 스트리밍합니다. 이러한 다양한 이용 사례는 유럽의 모바일 클라우드 시장 전체의 성장을 강화하고 증가하는 용량이 구매자를 확실히 찾을 수 있도록 합니다.

유럽의 모바일 클라우드 시장 보고서는 사용자별(기업 및 소비자), 용도별(게임, 엔터테인먼트, 교육 등), 서비스 모델별(SaaS, PaaS 등), 배포 모델별(퍼블릭 클라우드, 프라이빗 클라우드 등), 국가별로 분류됩니다.

Europe mobile cloud market value reached USD 69.42 billion in 2025 and is forecast to rise to USD 170.95 billion by 2030, registering a 19.75% CAGR.

Rising adoption of sovereign-cloud frameworks, expanding 5G standalone (SA) coverage, and intensifying enterprise focus on low-latency mobile workloads underpin this trajectory. National data-sovereignty mandates are forcing workload repatriation from extra-regional hyperscale zones to EU-hosted platforms, while 5G SA networks already deliver sub-10 millisecond round-trip latency, opening fresh demand for real-time industrial, gaming and fintech use cases. Telco-cloud alliances-such as Deutsche Telekom's NVIDIA-powered industrial AI cloud-illustrate how telecom operators are transforming into infrastructure suppliers for AI workloads. At the same time, regulatory scrutiny of hyperscaler market power is prompting price realignments, including the removal of egress fees, which lowers switching barriers and encourages multi-cloud strategies.

The European Commission's EuroStack programme targets 10,000 distributed edge-cloud nodes by 2030, creating local processing points that satisfy strict data-residency statutes. Orange and Capgemini's Bleu platform was launched in 2024 to offer Microsoft technology under SecNumCloud rules, proving that compliance-first offerings can attract sensitive workloads. The forthcoming EU Cloud Services Scheme will certify providers against sovereignty and security standards, accelerating repatriation of critical-sector data previously hosted outside the bloc. Simultaneously, the EU Data Act obliges vendors to abolish switching fees by January 2027, undermining lock-in economics and incentivizing a competitive ecosystem. As public agencies adapt procurement rules, European operators expect a sizeable uplift in cloud demand tied to regulated industries.

More than 60 operators worldwide have launched commercial 5G SA networks, including installations across Germany, the UK, Italy, and Spain. Network slicing allows predefined latency and bandwidth classes that match mobile-cloud application requirements, directly monetised through premium service tiers. Deutsche Telekom's 5G+ Gaming pilot has already proven sub-10 millisecond end-to-end latency for cloud gaming traffic. The GSMA projects EUR 164 billion in European economic value from 5G by 2030, most of which depends on SA deployment. Core-network upgrades, such as O2 Telefonica's cloud-native dual-mode core, further cut maintenance downtime and enable continuous feature releases.

The UK Competition and Markets Authority found AWS and Microsoft each control 30-40 % of domestic cloud spend, proposing Strategic Market Status obligations that could force interoperability and pricing remedies. The watchdog estimates competitive reforms might save UK businesses GBP 430 million annually. Parallel Digital Markets Act enforcement in Brussels adds further compliance layers for "gatekeeper" platforms, including limits on tying software licences to cloud consumption. Both AWS and Microsoft have pre-emptively eliminated egress fees for customers switching providers, demonstrating behavioural adjustments ahead of final rulings. While such concessions help clients, they compress provider margins and may reduce near-term investment pace.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Enterprise workloads produced 67% of 2024 Europe mobile cloud market revenue as corporates prioritised performance guarantees and sovereignty compliance. Financial institutions such as BBVA highlighted time-to-insight gains-94% faster analytics-after pivoting to cloud-native data platforms. These measurable outcomes justify premium contract values and spur continued infrastructure investment. Consumer adoption, while smaller, is expanding briskly at a 19.90% CAGR due to cloud gaming subscriptions and mobile entertainment bundles. Telefonica Germany moved 1 million 5G users onto AWS core cloud, blending enterprise and consumer value chains, proving that differentiated network services can monetise both segments. Although enterprises remain the bedrock of the Europe mobile cloud market, consumer growth diversifies revenue and cushions against corporate budget cycles.

The consumer-driven upswing is increasingly tied to edge-compute nodes situated near population centres, reducing jitter for graphics-intensive titles and video streaming. Network operators benefit from incremental wholesale traffic, while hyperscalers distribute content caches across metropolitan points of presence. Meanwhile, enterprise buyers widen multi-cloud footprints to mitigate lock-in, with Vodafone registering cost savings by maintaining "commercial tension" across three large providers. Advanced FinOps dashboards track usage by business unit, ensuring every workload runs in the optimal cost-performance zone. This dual-track evolution keeps the Europe mobile cloud industry resilient

Gaming secured a 32% slice of 2024 revenue and is projected to expand at 22.60% CAGR, propelled by pay-as-you-go cloud gaming services that remove local hardware constraints. Deutsche Telekom's 5G+ Gaming offer demonstrates how network slicing guarantees frame-rate consistency at mobile broadband speeds. Finance and business applications rank second in value, powered by real-time risk analytics delivered over secure, low-latency pipes. Enterprises in capital-markets hubs depend on deterministic latency for algorithmic trading, steering demand toward edge-optimised zones.

Education and healthcare applications continue gaining share as remote-learning platforms and diagnostic AI workloads migrate to cloud. Regulators permit sensitive health data to reside in sovereign cloud zones, enabling providers to roll out AI-powered imaging without contravening privacy law. Entertainment platforms capitalise on the same edge footprints that gaming uses, streaming adaptive-bitrate video without buffering. Collectively, these diverse use cases reinforce growth across the Europe mobile cloud market, ensuring that incremental capacity finds ready buyers.

The Europe Mobile Cloud Market Report is Segmented by User (Enterprise and Consumer), Application (Gaming, Entertainment, Education, and More), Service Model (Software-As-A-Service (SaaS), Platform-As-A-Service (PaaS), and More), Deployment Model (Public Cloud, Private Cloud, and More), and Country.