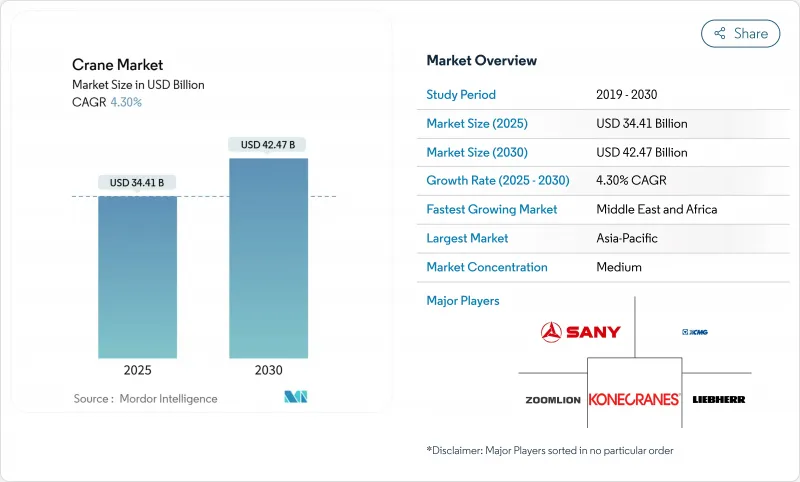

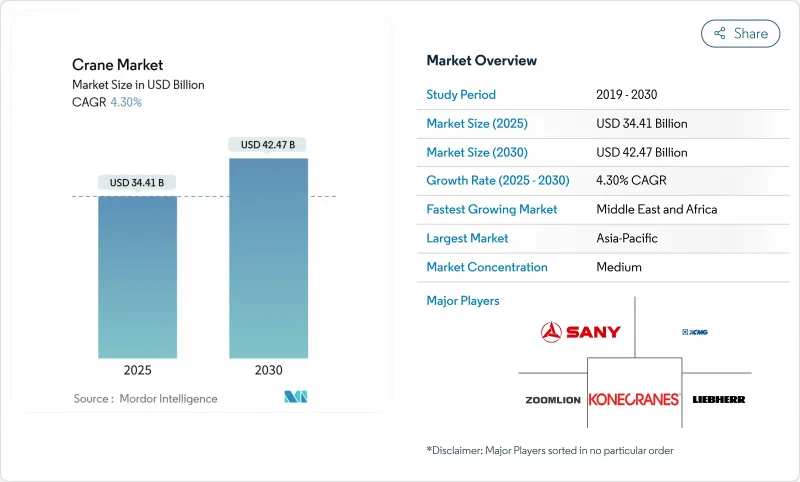

크레인 시장은 2025년에 344억 1,000만 달러에 이르고, 2030년에는 424억 7,000만 달러로 확대될 것으로 예측되며, CAGR은 4.30%를 나타낼 전망입니다.

안정적인 공공 지출, 대규모 민간 메가 프로젝트, 신재생에너지로의 세계 이동은 크레인 시장의 핵심 수요 엔진을 형성하고 있습니다. 미국 인프라 투자·고용촉진법으로 대표되는 정부의 인프라 계획은 계약자를 단기적인 경기변동으로부터 보호하기 위해 수년간 수주 잔여를 창출하고 있습니다. 해상 풍력 발전, 태양광 공원 및 송전망 업그레이드는 특히 특수 중량물 및 선박용 장비의 경우 이 밝은 전망을 강화합니다. 동시에, 전기 의무화는 하이브리드 크레인과 완전 전동 크레인에 대한 투자에 박차를 가하고, 텔레매틱스의 채용은 플릿의 가동률을 높여 다운타임을 억제합니다. 기존 기업이 제로 방출 플랫폼의 연구 개발을 가속화하고 틈새 혁신자를 인수하여 포트폴리오를 확대하기 때문에 경쟁이 격화됩니다.

인프라의 현대화는 크레인 수요의 주요 촉매제로 부상하고 있으며, 인프라 투자 및 고용 촉진법(Infrastructure Investment and Jobs Act)만으로도 교통, 에너지, 디지털 인프라 전체에서 1조 2,000억 달러를 넘는 투자가 계획되고 있습니다. 이 인프라 추진의 규모는 기존의 도로와 다리 프로젝트에 그치지 않고, 특수한 중량물 운반 능력을 필요로 하는 데이터센터, 반도체 공장, 클린 에너지 시설에까지 확장하고 있습니다. 건설 지출은 연간 2조 1,300억 달러에 달할 것으로 예상되며, 공공 인프라는 전년 대비 8% 가까운 성장을 차지합니다. 이 인프라 르네상스는 2027년까지 프로젝트의 백로그를 연장하는 크레인 사업자들에게 여러 해에 걸친 전망을 제공합니다. 인프라 프로젝트에서 모듈식 건설 기술로의 전환은 수백 톤의 조립식 부품을 처리 할 수있는 정밀 리프팅 장비에 대한 수요를 촉진하고 있습니다. 연방 정부의 인프라 자금 지원을 통해 각 주는 노동력 개발 프로그램에 투자할 수 있으며, 그렇지 않으면 시장 성장을 억제할 수 있는 크레인 인증 운영자의 심각한 부족을 해결하고 있습니다.

신재생에너지의 전환은 크레인 시장 역학을 근본적으로 바꾸고 있으며, 해상풍력발전설비는 2,500톤 이상의 터빈부품을 현수할 수 있는 특수한 해상크레인 수요를 견인하고 있습니다. Cadeler사의 Wind Peak를 비롯해 풍력 터빈 설치용 선박은 15MW의 터빈 세트를 7대 적재할 수 있는 등 점점 세련된 크레인 시스템을 탑재하게 되어 왔습니다. 신재생에너지의 도입 규모는 전례가 없는 것으로, Huisman사와 같은 기업은 150미터를 넘는 높이로 컴퍼넌트를 취급하기 위한, 특수한 해상 풍력 설치 크레인이나 모션 보정 플랫폼을 개발하고 있습니다. 태양광 발전의 설치는 특히 패널과 설치 시스템이 광대한 지역에서 정확한 위치 결정을 필요로 하는 유틸리티 스케일 프로젝트에서 이동식 크레인 수요를 촉진하고 있습니다. 신재생에너지 섹터의 성장은 부유식 해상풍력 플랫폼에서부터 특수 리프팅 솔루션을 필요로 하는 집광형 태양광 발전 설비에 이르기까지 새로운 크레인 용도 카테고리를 만들어 냈습니다. 신재생에너지 인프라는 지속적인 유지보수와 부품교환을 필요로 하므로, 이 에너지 전환은 기존의 건설사이클을 넘어 크레인 수요성장을 유지할 것으로 예측됩니다.

Manitowoc의 Model 31000과 같은 신형 중량물 크레인의 가격은 3,000만 달러에 달하는 반면, 엄청난 지속적인 유지보수 투자가 필요합니다. 재료비 인플레이션으로 건축자재 가격은 주요 시장에서 평균 15% 상승하여 크레인 제조 비용과 대여료에 직접 영향을 미치고 있습니다. 고금리는 이러한 과제를 더욱 심각화시켜 설비 자금 조달 비용이 크게 상승하여 크레인의 구입과 렌탈 수요에 영향을 미치고 있습니다. 중소 크레인 운영자는 가격 상승을 흡수하는 규모가 없기 때문에 이러한 비용 압력에 특히 약하며 시장에서 철수하거나 선수와의 통합을 강요 할 수 있습니다. 최신 크레인 시스템은 복잡하기 때문에 전문 기술자와 고가의 교체 부품이 필요하며 운영자 예산을 압박할 수 있습니다. 공인 운영자의 교육 비용이 증가하고 있으며, 시뮬레이션 기반 프로그램은 교육 시간 단축과 안전성 향상의 장기적인 이점이 있음에도 불구하고 상당한 선행 투자가 필요합니다.

이동식 크레인은 2024년 건설, 인프라, 산업용도의 다목적성을 반영하여 45.25%의 최대 시장 점유율을 유지했습니다. 이동식 크레인 부문은 다양한 현장에 대한 적응성과 여러 프로젝트에 신속하게 전개할 수 있는 능력으로부터 이익을 얻고 있으며, 다양한 작업량을 관리하는 계약자에게 선호되는 옵션이 되었습니다. 해상 및 해양 크레인은 2025-2030년의 CAGR이 7.45%로 가장 강한 성장 궤도를 따르고 있습니다. 이는 해양 풍력 발전 설비의 전례 없는 확장과 선박에 장착된 특수 리프팅 솔루션의 필요성 때문입니다.

타워 크레인과 천장 크레인을 포함한 고정 크레인은 고층 건축 및 산업 시설에서 중요한 역할을 수행하며 특히 중동 및 아시아태평양 도시 메가 프로젝트에서 수요가 증가하고 있습니다. 해양·해양 부문의 급성장은 해상 풍력 터빈의 설치라는 특수한 성질을 반영하고 있으며, 크레인은 수천 톤의 부품을 취급하면서 엄격한 해양 환경에서 가동해야 합니다. Cadeler와 같은 기업은 성장하는 해상 풍력 발전 시장을 수용하기 위해 2,200t급 크레인을 갖춘 풍력 터빈 설치 선박에 많은 투자를 하고 있습니다. 해상 풍력 터빈의 대형화가 진행됨에 따라 엄격한 기상 조건 하에서도 정밀한 리프팅이 가능한 점점 정교한 선박 크레인 시스템에 대한 수요가 높아지고 있습니다.

51-150톤의 부문은 2024년에 33.90%로 최대 시장 점유율을 차지하며 일반 건설 및 산업용 제품의 스위트 스팟이 되었습니다. 용량 300톤 이상의 부문은 CAGR 8.25% 2025-2030에서 가장 빠른 성장을 경험하고 있으며, 전례없는 리프팅 능력이 필요한 메가 프로젝트로의 산업 변화를 반영합니다. 이 미드레인지 용량 부문은 리프팅 능력과 작동 유연성의 균형을 통해 혜택을 받으며 상업용 건물에서 인프라 개발까지 다양한 건설 프로젝트에 적합합니다.

중량물 리프팅 용도는 원자로 부품, 프로세스 모듈 및 터빈 어셈블리를 리프팅할 수 있는 크레인이 필요한 원자력 발전소 건설, 석유화학 시설, 해양 에너지 프로젝트에 의해 추진되고 있습니다. Mammoet가 개발한 용량 6,000톤의 SK6000 크레인은 초중량 리프팅 능력에 대한 업계의 뒷받침을 보여줍니다. 50톤까지의 부문은 소규모 건설 프로젝트 및 유지보수 용도에 대응하고, 151-300톤 범위는 중규모 산업 및 인프라 요구에 대응합니다. Zoomlion의 3,600톤 크롤러 크레인은 단일 리프팅 중량의 세계 기록을 세우고 중량물 리프팅 능력의 기술적 진보를 입증합니다. 모듈식 건축 동향은 조립식 부품이 정확한 리프팅과 위치 결정 능력을 필요로 하기 때문에 모든 능력 범위에 걸쳐 수요를 견인하고 있습니다.

아시아태평양은 2024년 크레인 시장 수익의 42.10%를 차지했으며, 이는 중국이 높은 유틸리티 지출을 유지했고 인도가 공장 건설을 가속화했기 때문입니다. 중국의 항만 자동화 성공 사례는 1시간에 평균 60.9개의 컨테이너를 이동하는 1대의 교량 크레인으로 처리량 성능의 지역 리더십을 이야기하고 있습니다. 인도의 2025년 연방예산은 선거기간 중 경계에도 불구하고 크롤러와 타워크레인에 대한 지속적인 수요를 지지하고 높은 수준의 인프라 배분을 유지했습니다. 일본과 한국은 시설의 유지보수와 근대화로 1자리대 전반의 성장을 기록합니다.

중동 및 아프리카은 2025-2030년 CAGR이 가장 빠른 6.65%를 나타낼 것으로 예측됩니다. 사우디아라비아만으로도 NEOM과 관련된 기가 프로젝트를 위해 약 2만대의 타워크레인을 배치할 예정입니다. Wolffkran과 Zamil Group의 새로운 공장과 같은 현지 합작 투자는 수입 리드 타임을 단축하고 현지화 된 공급망을 구축합니다. 원유 가격 상승은 중량물 크롤러 크레인에 의존하는 하류의 석유화학 콤비나트에 수익을 가져다가 용도의 다양성을 넓혀줍니다.

북미는 1조 2,000억 달러의 인프라 투자·고용 촉진법의 혜택을 받고, 6만 이상의 프로젝트에 자금을 공급하고, 다년간의 일량을 유지합니다. 미국 설비 렌탈 부문은 2025년 773억 달러에 달할 것으로 예상되며 크레인이 큰 점유율을 차지합니다. 유럽은 해상 풍력 발전이 설비 수요를 가속화하면서 금리 상승이 상업용 부동산 착공을 억제한다는 복잡한 신호에 직면하고 있습니다. 라틴아메리카의 회복은 상품 가격에 달려 있지만 브라질의 에너지 입찰이 재개됨에 따라이 지역의 대형 리프트 수주가 증가했습니다.

The crane market reached USD 34.41 billion in 2025 and is projected to advance to USD 42.47 billion by 2030, translating into a 4.30% CAGR.

Stable public spending, large-scale private megaprojects, and the global shift to renewable energy form the core demand engine for the crane market. Government infrastructure programs, led by the U.S. Infrastructure Investment and Jobs Act, have created multi-year backlogs that shield contractors from short-term economic swings. Offshore wind, solar parks, and grid upgrades reinforce this positive outlook, especially for specialized heavy-lift and marine equipment. Concurrently, electrification mandates spur investment in hybrid and fully electric cranes, while telematics adoption raises fleet utilization and curbs downtime. Competition intensifies as incumbents accelerate R&D on zero-emission platforms and acquire niche innovators to broaden portfolios.

Infrastructure modernization has emerged as the primary catalyst for crane demand, with the Infrastructure Investment and Jobs Act alone generating over USD 1.2 trillion in planned investments across transportation, energy, and digital infrastructure. The scale of this infrastructure push extends beyond traditional road and bridge projects to encompass data centers, semiconductor fabs, and clean energy facilities that require specialized heavy-lifting capabilities. Construction spending is projected to reach USD 2.13 trillion annually, with public infrastructure accounting for nearly 8% year-over-year growth. This infrastructure renaissance creates multi-year visibility for crane operators, extending project backlogs well into 2027. The shift toward modular construction techniques in infrastructure projects also drives demand for precision lifting equipment capable of handling prefabricated components weighing hundreds of tons. Federal infrastructure funding has enabled states to invest in workforce development programs, addressing the critical shortage of certified crane operators that could otherwise constrain market growth.

The renewable energy transition fundamentally reshapes crane market dynamics, with offshore wind installations driving demand for specialized marine cranes capable of lifting turbine components exceeding 2,500 tons. Wind turbine installation vessels are being delivered with increasingly sophisticated crane systems, including Cadeler's Wind Peak vessel, capable of transporting seven complete 15 MW turbine sets per load. The scale of renewable energy deployment is unprecedented, with companies like Huisman developing specialized offshore wind installation cranes and motion-compensated platforms to handle components at heights exceeding 150 meters. Solar installations drive demand for mobile cranes, particularly in utility-scale projects where panels and mounting systems require precise positioning across vast areas. The growth of the renewable energy sector is creating new crane application categories, from floating offshore wind platforms to concentrated solar power installations requiring specialized lifting solutions. This energy transition is expected to sustain crane demand growth well beyond traditional construction cycles, as renewable energy infrastructure requires ongoing maintenance and component replacement.

The crane industry faces mounting cost pressures constraining market expansion, with new heavy-lift cranes like Manitowoc's Model 31000 commanding prices of USD 30 million while requiring substantial ongoing maintenance investments. Material cost inflation has increased construction input prices by an average of 15% across major markets, directly impacting crane manufacturing costs and rental rates. High interest rates compound these challenges, with equipment financing costs rising significantly and affecting crane purchases and rental demand. Smaller crane operators are particularly vulnerable to these cost pressures, as they lack the scale to absorb price increases and may be forced to exit the market or consolidate with larger players. The complexity of modern crane systems is also driving up maintenance costs, requiring specialized technicians and expensive replacement parts that can strain operator budgets. Training costs for certified operators are increasing, with simulation-based programs requiring substantial upfront investments despite their long-term benefits in reducing training time and improving safety outcomes.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Mobile cranes maintain the largest market share at 45.25% in 2024, reflecting their versatility across construction, infrastructure, and industrial applications. The mobile crane segment benefits from its adaptability to diverse job sites and the ability to be rapidly deployed across multiple projects, making it the preferred choice for contractors managing varied workloads. Marine and offshore cranes are experiencing the strongest growth trajectory at 7.45% CAGR 2025-2030, driven by the unprecedented expansion of offshore wind installations and the need for specialized vessel-mounted lifting solutions.

Fixed cranes, encompassing tower cranes and overhead systems, serve critical roles in high-rise construction and industrial facilities, with the demand particularly strong in urban megaprojects across the Middle East and Asia Pacific. The marine and offshore segment's rapid growth reflects the specialized nature of offshore wind turbine installation, where cranes must operate in challenging maritime environments while handling components weighing thousands of tons. Companies like Cadeler invest heavily in wind turbine installation vessels equipped with 2,200-ton capacity cranes to serve the growing offshore wind market. The evolution toward larger offshore wind turbines drives demand for increasingly sophisticated marine crane systems capable of lifting precision in harsh weather conditions.

The 51-150 ton segment commands the largest market share at 33.90% in 2024, representing the sweet spot for general construction and industrial applications. The above 300-ton capacity segment is experiencing the fastest growth at 8.25% CAGR 2025-2030, reflecting the industry's shift toward megaprojects requiring unprecedented lifting capabilities. This mid-range capacity segment benefits from its balance of lifting capability and operational flexibility, making it suitable for various construction projects from commercial buildings to infrastructure development.

Heavy-lift applications are being driven by nuclear power plant construction, petrochemical facilities, and offshore energy projects that require cranes capable of lifting reactor components, process modules, and turbine assemblies weighing hundreds of tons. Mammoet's 6,000-ton capacity SK6000 crane development exemplifies the industry's push toward ultra-heavy lifting capabilities. The up to 50-ton segment serves smaller construction projects and maintenance applications, while the 151-300 ton range addresses mid-scale industrial and infrastructure needs. Zoomlion's 3,600-ton crawler crane, setting world records for single lifting weight, demonstrates the technological advancement in heavy-lift capabilities. Modular construction trends drive demand across all capacity ranges, as prefabricated components require precise lifting and positioning capabilities.

The Crane Market Report is Segmented by Type (Mobile Crane, Fixed Crane, and Marine and Offshore Crane), Capacity (Up To 50 T, 51 To 150 T, 151 To 300 T, and Above 300 T), Power Source (Diesel, Hybrid, and Fully Electric), Boom Type (Lattice Boom and Telescopic Boom), Application (Construction and Mining and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Asia-Pacific accounted for 42.10% of crane market revenue in 2024 as China sustained high public works spending and India accelerated factory construction. Chinese port automation success stories, with single bridge cranes averaging 60.9 container moves an hour, illustrate regional leadership in throughput performance. India's Union Budget 2025 maintained elevated infrastructure allocations, underpinning continued demand for crawlers and tower cranes despite election-year caution. Japan and South Korea post low-single-digit growth, driven by facility maintenance and modernization.

The Middle East and Africa region is projected to post the fastest 6.65% CAGR between 2025-2030. Saudi Arabia alone intends to deploy about 20,000 tower cranes for NEOM and associated giga-projects. Local joint ventures, such as Wolffkran and Zamil Group's new factory, reduce import lead times and create a localized supply chain. High oil prices funnel revenue into downstream petrochemical complexes that rely on heavy-lift crawler cranes, broadening application diversity.

North America benefits from the USD 1.2 trillion Infrastructure Investment and Jobs Act, which funds over 60,000 projects and sustains multi-year workloads. The U.S. equipment rental sector is forecast to reach USD 77.3 billion in 2025, with cranes forming a sizable share. Europe faces mixed signals: offshore wind accelerates equipment demand, yet elevated interest rates suppress commercial real estate starts. Latin America's recovery hinges on commodity pricing, while renewed Brazilian energy auctions boost regional heavy-lift orders.