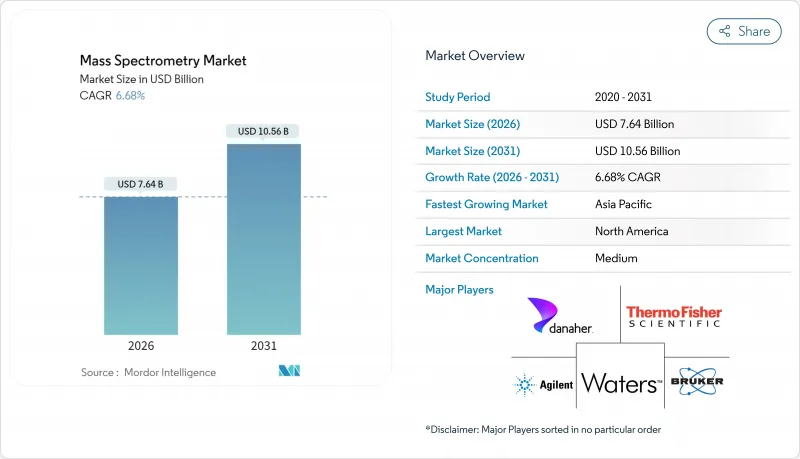

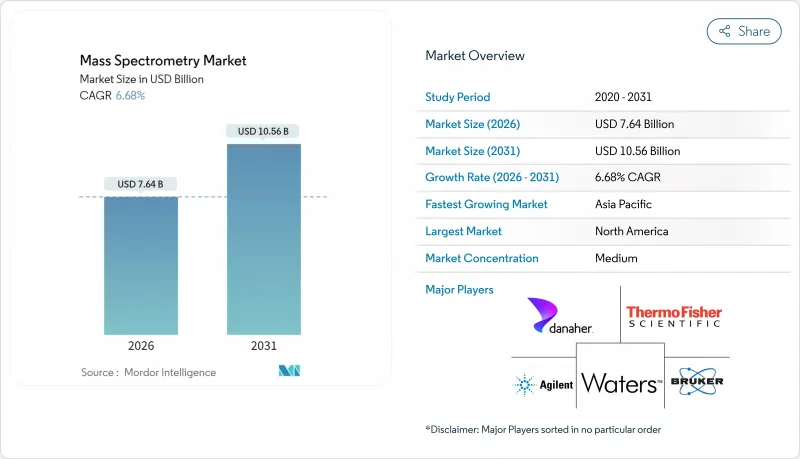

질량분석법 시장은 2025년 71억 6,000만 달러로 평가되었고, 2026년에는 76억 4,000만 달러로 성장할 전망이며, 2026-2031년 CAGR 6.68%로 추이하여, 2031년에는 105억 6,000만 달러에 달할 것으로 예측됩니다.

이 성장세는 바이오 의약품 특성 평가 증가, 식품 안전 모니터링 강화, 소형화된 포인트 오브 케어 시스템, 인공지능(AI) 데이터 분석, 멀티오믹스 연구에 대한 자금 투입에 기인하고 있습니다. 북미의 성숙한 연구 생태계 및 엄격한 규제 프레임워크가 이 지역을 최첨단에 두고 있지만, 아시아태평양의 두 자릿수 성장은 지리적 세력도의 변화를 시사합니다. 경쟁 차별화는 소프트웨어 및 하드웨어의 통합으로 전환하고 있습니다. 이는 실시간으로 높은 처리량 지식에 대한 사용자 수요가 순수한 장비 사양을 초과하기 때문입니다. 한편, 개발도상국의 학술 시설에 있어서 자금 제약 및 지속적인 인재 부족이 도입을 억제하고 있어, 창조적인 자금 조달 및 연수 프로그램의 필요성이 부각되고 있습니다.

의약품 개발이 단일클론항체 및 세포 기반 요법으로 이행하는 가운데, 초고분해능 장치에 대한 수요가 급증하고 있습니다. 번역후 수식의 매핑이나 고차 구조의 검증에는 단편화 시의 취약한 결합을 유지하기 위해, 전자 포획 해리를 짜넣은 하이브리드 플랫폼이 불가결이 되고 있습니다. 복잡한 단백질 워크플로우를 효율화할 수 있는 제조업체는 향후 수익을 얻는 데 있어 이점이 있습니다.

미국 환경보호청(EPA)이 2024년 PFOA 및 PFOS를 유해물질로 지정함으로써 환경 및 식품 검사 기관에서 액체 크로마토그래피 탠덤 질량분석 장치의 업그레이드가 잇따랐습니다. 유럽 화학물질청(ECHA)에 의한 유럽에서의 유사한 정책 동향은 검출 한계의 계약을 계속하고 있으며, 장치의 도입과 분석법 개발 서비스를 추진하고 있습니다. 식품 산업의 대응으로는 추출액 샘플링 전자 이온화 질량분석법(E-LEI-MS)과 같은 새로운 방법의 채용이 포함됩니다. 이 방법은 시료 준비 없이 과피 농약을 실시간으로 확인할 수 있으며, 분석 시간을 몇 시간에서 몇 분으로 크게 단축합니다.

하이엔드 시스템은 50만 달러에서 150만 달러의 범위이며, 보조금 부족으로 인해 공유 리소스 센터는 업그레이드를 연기해야 하며, 지역 연구자들의 장비에 대한 액세스가 제한됩니다. 이 재정적 장벽은 유지보수 계약 및 소모품을 포함한 지속적인 운영 비용으로 더욱 심각해지고 있으며, 연간 초기 투자액의 15-20%에 해당할 수 있습니다. 여러 연구 그룹에 서비스를 제공하는 핵심 시설의 경우 구매 비용과 현지 연구자에게 저렴한 요금과 균형을 맞추어야 하며 상황은 특히 어려움입니다.

2025년에도 하이브리드 구조가 질량분석법 시장의 46.15%를 차지하는 주요 지위를 유지하고 있지만, MALDI-TOF 플랫폼은 가장 급격한 성장 궤도를 나타내며 2031년까지 연평균 복합 성장률(CAGR) 10.88% 전망을 보이고 있습니다. MALDI-TOF에 의한 신속한 미생물 동정은 진단까지의 시간을 몇 분으로 단축해, 입원 비용의 삭감에 공헌하고 있습니다. 미생물 분야를 넘어, MALDI HiPLEX-IHC는 현재, 5 마이크로미터의 공간 분해능으로 다중화 완전 단백질 이미징을 실현해, 종양 조직 절편에 있어서 공간 단백질체학를 가능하게 하고 있습니다.

2세대 MALDI 장치는 90% 가까운 정밀도로 미생물총의 신속 분류에도 대응하여 장내 미생물총 연구에서의 이용 범위를 확대하고 있습니다. 머신러닝 알고리즘과의 통합에 의해 스펙트럼 핑거프린트 라이브러리의 자동화를 실현해, 병원 검사실이 처리 능력 수요 증가에 대응하는데 있어서 중요한 차별화 요인이 되고 있습니다.

북미는 2025년 시점에서 질량분석법 시장에 34.65%를 차지했습니다. 이는 미국 국립위생연구소(NIH)의 강력한 자금 제공, 활발한 생명공학 개발 파이프라인, 엄격한 환경 규제 때문입니다. 미국 환경보호청(EPA)의 PFAS 규제에서는 검출 한계의 저하가 요구되고 있어 장치의 갱신 사이클이나 전용 소모품 수요를 촉진하고 있습니다. 캐나다에서는 식수 품질 가이드라인의 개정이 진행되어 주정부에 의한 조달 안건이 증가하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 9.92%로 확대해 미래 수량 성장의 핵심이 될 전망입니다. 중국의 제조업체는 소형화 직접 이온화 장치의 상업화를 위한 벤처 자금을 확보하고, 국내 수요 및 수출 기회에 대한 대응을 목표로 하고 있습니다. 인도와 한국의 수탁개발제조기관(CDMO)의 병행 확대는 규제 대응 플랫폼에 대한 지속적인 수요를 창출하고 있습니다.

유럽은 유럽 식품안전기관(EFSA) 및 유럽의약청(EMA)의 엄격한 규제에 힘입어 안정된 고부가가치 시장으로 계속되고 있습니다. 유럽 화학물질청(ECHA)의 끊임없이 진화하는 화학물질 안전 틀은 빈번한 방법 검증의 갱신을 필요로 하고 서비스 수익의 흐름을 지속시키고 있습니다. 중동 및 아프리카, 남미는 총 잠재 수익 규모가 작은 반면, 각각 GCC(만안 협력 이사회)의 공중 위생 투자 및 브라질 농약 잔류 감시 프로그램을 통해 기세를 보이고 있습니다.

The Mass Spectrometry market is expected to grow from USD 7.16 billion in 2025 to USD 7.64 billion in 2026 and is forecast to reach USD 10.56 billion by 2031 at 6.68% CAGR over 2026-2031.

Momentum stems from rising biologics characterization, tighter food-safety oversight, miniaturized point-of-care systems, artificial-intelligence (AI) data analytics, and multi-omics funding. North America's mature research ecosystem and stringent regulatory framework keep the region at the forefront, yet Asia-Pacific's double-digit trajectory signals a geographical power shift. Competitive differentiation is gravitating toward software-hardware integration, as user demand for real-time, high-throughput insights eclipses pure instrument specifications. Meanwhile, capital constraints in developing-country academic facilities and persistent talent gaps temper adoption, underscoring the need for creative financing and training programs.

Demand for ultra-high-resolution instruments is soaring as drug developers pivot toward monoclonal antibodies and cell-based therapies. Post-translational modification mapping and higher-order structure verification now require hybrid platforms incorporating electron capture dissociation to preserve fragile bonds during fragmentation. Manufacturers that can streamline complex protein workflows are well-positioned to capture future revenue.

The US EPA's 2024 designation of PFOA and PFOS as hazardous substances drove a wave of liquid chromatography-tandem mass spectrometry upgrades across environmental and food laboratories. Comparable policy moves in Europe under ECHA continue to tighten detection limits, propelling instrument placements and method-development services. The food industry's response includes adopting novel approaches like Extractive-liquid sampling electron ionization-mass spectrometry (E-LEI-MS), which enables real-time identification of pesticides on fruit peels without sample preparation, significantly reducing analysis time from hours to minutes.

High-end systems range from USD 500,000 to USD 1.5 million, with grant scarcity forces shared-resource centers to postpone upgrades, reducing instrument access for regional researchers. This financial barrier is compounded by ongoing operational costs, including maintenance contracts and consumables, which can represent 15-20% of the initial investment annually. The situation is particularly challenging for core facilities that serve multiple research groups, as they must balance acquisition costs against user fees that remain affordable for local researchers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hybrid architectures continued to dominate 46.15% of the mass spectrometry market share in 2025, yet MALDI-TOF platforms exhibit the steepest trajectory, posting an 10.88% CAGR outlook to 2031. MALDI-TOF's rapid microbial identification slashed diagnostic turnaround to minutes, lowering hospitalization costs. Beyond microorganisms, MALDI HiPLEX-IHC now delivers multiplexed intact-protein imaging at 5 µm spatial resolution, enabling spatial proteomics in oncology tissue sections.

Second-generation MALDI units also tackle rapid microbiota classification with near-90% accuracy, broadening usage in gut-microbiome studies. Integration with machine-learning algorithms automates spectral-fingerprint libraries, a key differentiator as hospital laboratories scale throughput demands.

The Mass Spectrometry Market Report is Segmented by Technology (Hybrid Mass Spectrometry, Single Mass Spectrometry, MALDI-TOF Mass Spectrometry, and More), Component (Instruments, Ionization Sources, and More), Application (Pharmaceutical & Biotechnology, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 34.65% to the mass spectrometry market in 2025, owing to strong National Institutes of Health funding, a vibrant biotech pipeline, and stringent environmental regulations. The United States Environmental Protection Agency's PFAS mandates require lower detection limits, driving instrument refresh cycles, and specialized consumables. Canada is following up with updated drinking-water quality guidelines, spurring provincial tenders.

Asia-Pacific is forecast to expand at a 9.92% CAGR to 2031 and is central to future volume growth. China's manufacturers secured venture funding to commercialize miniaturized direct-ionization devices, aiming to address domestic demand and export opportunities. Parallel expansion of contract development and manufacturing organizations (CDMOs) in India and South Korea creates recurring demand for compliance-ready platforms.

Europe remains a stable, high-value market, anchored by stringent EFSA and EMA regulations. The ECHA's continuously evolving chemical-safety framework necessitates frequent method-validation updates, sustaining service revenue streams. Middle East & Africa and South America, though smaller in total addressable revenue, exhibit momentum through GCC public-health investments and Brazil's agrochemical-residue monitoring programs, respectively.