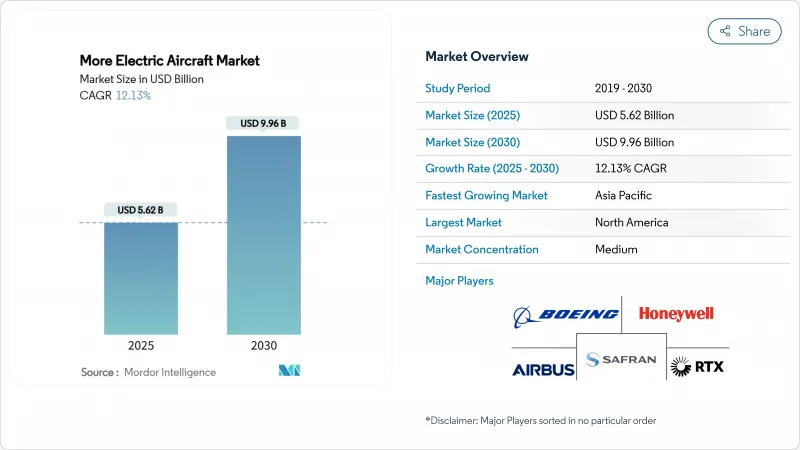

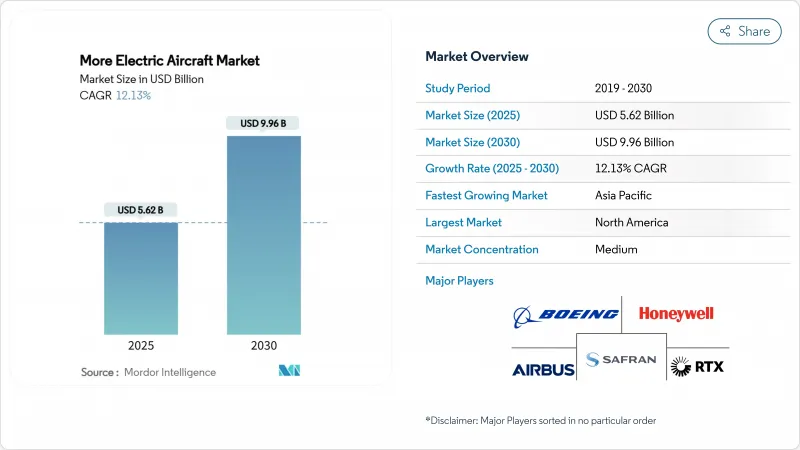

항공기 전기화(MEA) 시장 규모는 2025년에 56억 2,000만 달러로 추정되고, 2030년에는 99억 6,000만 달러에 이를 전망이며, CAGR 12.13%로 성장할 것으로 예측됩니다.

연료 가격 상승, 이산화탄소 감축 의무, 고출력 전자 제품의 성숙으로 항공사와 항공기는 유압 및 공압 서브 시스템을 전기 아키텍처로 전환하는 경향이 있습니다. 항공사는 엔진이 환경 제어를 위해 공기를 배출하지 않게 되면서 연료 소비를 최대 20% 절감할 수 있었다고 보고하고 있으며, 전력 밀도가 높은 발전기 및 반도체 배터리가 보다 긴 전기적 내구성을 지원하고 있습니다. B787과 같은 고정 날개 프로그램은 블리드리스 운영을 실제 운영으로 증명하고 있으며, eVTOL 개발자는 도시의 임무에 동일한 논리를 적용합니다. 그 결과 기존 기업과 신흥 기업은 와이드 밴드갭 반도체, 열 제어 재료, 고전압 인증 프레임을 확보하고 수요를 따라 잡으려고 경쟁하고 있습니다.

연료는 항공사 운항 경비의 20-30%를 차지하기 때문에 킬로와트 클래스의 전동 파워트레인은 배출 가스 삭감 효과에 더해 경제적으로도 매력적입니다. GE 에어로 스페이스의 CLEEN III 시연은 블리드 에어 배관을 제거하고 터보 팬 코어를 최적의 추력 설정에 가깝게 운전할 수 있도록 하는 90kW 스타터 제너레이터를 제공합니다. 콜린스 에어로스페이스사가 787형기에 탑재한 블리드리스 환경 제어 팩은 전기 서브 시스템이 유지보수 계획을 용이하게 하는 동시에, 이산화탄소 배출량을 줄이는 방법을 보여줍니다. 따라서 항공사는 예측 가능한 점검 간격과 유체 누출을 줄이고 예정되지 않은 지상 대기 시간을 줄일 수 있습니다. 이러한 금전적, 컴플라이언스적인 이중 보상은 항공기의 유형에 관계없이 전동화된 LINE-FIT 및 레트로 피트 프로그램에 대한 지속적인 투자를 강화하는 것입니다.

현재 자발적인 서약을 대신하여 구속력있는 규칙이 도입되었습니다. 미국 연방 항공국(FAA)은 2024년 4월에 발효되는 연비 기준을 채택하여 신형 제트기의 시트 킬로미터당 최대 연료를 설정했습니다. 유럽의 'ReFuelEU' 지령은 2030년까지 6%, 2050년까지 70%의 지속 가능한 항공 연료를 증가시킬 것을 항공사에 의무화하고 있으며, 드롭 인 연료와 전기 부스트를 혼합한 하이브리드 전기 아키텍처를 촉구하고 있습니다. ICAO의 세계 오프셋 방식은 검증 가능한 배출 감소를 요구하기 때문에 OEM은 전기적 통합을 가속화할 수밖에 없습니다. 예를 들어 에어버스는 2035년까지 제로 방출의 상용 모델을 규제 가드 레일의 범위 내에 머물기 위해 공공의 목표로 삼고 있습니다.

전기 추진은 일상적으로 DC 1,000V를 초과하지만, 과거의 규제에서는 270V 아키텍처가 중심이었습니다. FAA는 BETA Technologies의 H500A에 새로운 아크 폴트 모드와 절연 파괴 모드에 대처하기 위한 특별 조건을 발행했습니다. FAA와 EASA간에 다른 규칙을 만드는 것은 세계 검증을 복잡하게 하고 개발자는 여러 최악의 경우 시나리오를 가정한 설계를 강요합니다. 보잉의 B777-9형기는 기존의 전력을 사용하지 않는 운항에 대한 추가적인 조사에 직면하고 있으며, 레거시 프로그램이 전압 엔벨로프가 확대되었을 때 어떻게 인증의 지연에 휩쓸리는지 부조하고 있습니다. 이러한 불확실성은 개발 사이클을 장기화하고 예산을 팽창시켜 항공기 전기화 시장의 주요 성장률을 억제합니다.

2024년 항공기 전기화 시장의 39.56%는 민간기체였습니다. 이는 항공사가 유지보수 비용을 억제하기 위해 유압 시스템을 분산형 전기 서브시스템으로 대체했기 때문입니다. 항공사는 라인 교환 가능한 유닛이 유체 구동이 아닌 솔리드 스테이트이기 때문에 예측 가능한 수명주기 비용을 강조합니다. 한편, eVTOL 카테고리는 2030년까지 15.65%의 연평균 복합 성장률(CAGR)을 기록했으며, 도시 간 에어택시 사업에 대한 투자자의 신뢰가 높아지고 있음을 보여줍니다. Joby와 Archer의 인증 획득 마일스톤은 개념에서 가까운 미래의 서비스로 인식을 전환하여 지역 운영자로부터 플릿 주문을 이끌어 냈습니다. 군사 프로그램은 주로 레이더 신호 감소를 위해 전동 액추에이터를 채택하고, 비즈니스 항공은 객실 소음과 공항 배출을 줄이기 위해 전동 액추에이터를 채택합니다.

이 부문의 차이는 항공기 전기화 시장이 기존 수요 지표를 검토할 가능성을 시사합니다. 2028년 이후 300대 이상의 하이브리드 전기식 지역 항공기를 수락한다는 JSX의 계획은 지역 항공사가 가능하다면 오래된 항공기를 뛰어넘는 방법을 보여줍니다. 주문이 가속화되면 개발 리드 타임이 단축되므로 공급망은 반도체를 eVTOL 파운더에 먼저 할당해야 합니다. 하이 사이클 배터리의 셀 생산은 제한되어 있기 때문에 레거시 내로우 바디의 레트로핏 입구가 됩니다. 그럼에도 불구하고, 항공기의 완전 갱신이 경제적으로 어려운 경우에는 구형의 민간기용의 후부 부착 키트가 보급되어, 항공기 클래스 간에 균형 잡힌 주문 구성이 확보됩니다.

2024년 항공기 전기화 시장 규모의 63.55%는 고정익형이 차지했는데, 이것은 B787이나 A350과 같은 인증된 레퍼런스 프로그램이 수익운항에 있어서의 전기 환경 제어를 실증하고 있는 덕분입니다. 이러한 예는 내로우 바디 기체로의 고전압 개수를 승인할 때 규제 당국과 대주를 안심시킵니다. 동시에 회전 날개 및 전동 리프트의 개념은 직접 구동 전기 모터가 가져오는 호버링 효율의 단계적 변화에 힘입어 CAGR12.4%로 확대됩니다.

DARPA의 XRQ-73 하이브리드 전기 드론은 로터 리프트와 고정 날개 순항을 융합시켜 파워 일렉트로닉스가 수직 비행 자산에 스텔스와 내구성을 제공한다는 것을 보여줍니다. Electra의 단거리 이륙 지역 실증기는 이 홈을 더욱 붕괴시켜 미래의 분류학이 날개 계획보다 미션 프로파일에 초점을 맞추는 것을 시사합니다. 로터리 프로그램도 기어박스의 윤활 라인이 없는 것을 이용하여 경량화 및 유지보수의 경감을 도모하고 있습니다. 이와 같이 범주가 모호해지면, 통일된 인증의 틀이 촉진되고, 종래와는 다른 레이아웃의 진입이 원활해져, 항공기 전기화 시장 내에 플랫폼의 다양성이 유지될 가능성이 있습니다.

북미는 2024년 지출액의 35.23%를 차지했는데, 이는 방위 예산이 메가와트 실증기를 지원하고 FAA가 전기 추진 인증을 위한 초기 경로를 제공했기 때문입니다. 미국의 설립된 Tier-1 공급업체는 실험실, 시험 장비 및 인적 자본 파이프라인을 갖춘 성숙한 생태계를 지원합니다. NASA의 전동 파워트레인 비행 실증 프로그램은 GE와 보잉의 엔지니어를 쌍으로 하여, 2027년까지 지역 플랫폼에서 하이브리드 추진력의 비행 시험을 실시하는 것으로, 지역의 기세를 강화하고 있습니다.

유럽은 Clean Aviation 보조금과 공항의 탈탄소화 정책에 힘입어 금액 기준으로 2위를 차지했습니다. GOLIAT 및 에코펄스와 같은 EU 프로젝트는 액체 수소 취급, 초전도 케이블, 하이브리드 전기 비행 시험 등에 공적 자금을 투입하고 있습니다. EASA와 FAA 간의 정합은 eVTOL의 대서양 횡단 검증을 가속화하고 듀얼 레지스트리 운영자 시장 출시 시간을 단축합니다. 그럼에도 불구하고, 유럽 공급업체는 반도체 조달에서 통화 인플레이션에 직면하고 있으며, 웨이퍼 할당을 보장하기 위해 아시아 주조소와의 합작 투자를 촉구하고 있습니다.

아시아태평양은 12.45%의 연평균 복합 성장률(CAGR)로 가장 높은 성장을 기록합니다. 중국 민용 항공국은 eVTOL 물류 및 여객 셔틀을 위해 전용 저고도 통로를 설정하여 상업 전개 일정을 단축했습니다. 국가는 2030년까지 1조 위안 규모의 일반 항공 산업을 구축할 계획이며, 외국 Tier2 공급업체를 유치하기 위해 보조금과 규제의 확실성을 주입합니다. 일본과 한국은 보다 광범위한 인증 전에 쇼케이스를 제공하기 위해 박람회 유형 이벤트에서 도시 실증 비행에 중점을 둡니다. 하지만 공항 준비는 늦었습니다. 인도는 UDAN 연결 방식 하에서 단거리 노선을 위한 전동 지역 터보프롭을 모색하고 있습니다. 아시아태평양의 다양한 시장 진입은 배터리, 모터 및 바이오닉스 벤더의 지속적인 수주로 이어지며, 아시아태평양이 항공기 전기화 시장의 주요 볼륨 운전사임을 보장합니다.

The more electric aircraft (MEA) market size is valued at USD 5.62 billion in 2025 and is forecasted to reach a market size of USD 9.96 billion by 2030, advancing at a 12.13% CAGR.

Rising fuel prices, carbon-reduction mandates, and the maturation of high-power electronics push airlines and airframers to swap hydraulic and pneumatic subsystems for electrical architectures. Airlines report fuel-burn savings of up to 20% when engines no longer bleed air for environmental control, while power-dense generators and solid-state batteries support longer electric endurance. Fixed-wing programs such as the B787 prove bleed-less operation in service, and eVTOL developers apply the same logic to urban missions. As a result, incumbents and start-ups race to secure wide-bandgap semiconductors, thermal control materials, and high-voltage certification slots to keep pace with demand.

Fuel accounts for 20%-30% of airline operating expense, making kilowatt-class electric powertrains economically attractive in addition to their emission benefits. GE Aerospace's CLEEN III demonstration delivers a 90 kW starter-generator that removes bleed-air plumbing and lets turbofan cores run closer to optimum thrust settings. Collins Aerospace's bleed-less environmental control pack on the 787 illustrates how electrical subsystems lower carbon output while easing maintenance planning. Airlines thus gain predictable inspection intervals and fewer fluid leaks, reducing unscheduled ground time. These dual financial and compliance rewards reinforce continuous investment in electrified line-fit and retrofit programs across fleet types.

Binding rules now supplant voluntary pledges. The US Federal Aviation Administration (FAA) adopted fuel-efficiency standards effective April 2024 that set maximum fuel per seat-kilometer for new jets. The European "ReFuelEU" mandate obliges carriers to uplift 6% sustainable aviation fuel by 2030 and 70% by 2050, prompting hybrid-electric architectures that blend drop-in fuels with electric boost. ICAO's global offset scheme requires verifiable emission cuts, forcing OEMs to accelerate electrical integration because incremental engine tweaks cannot satisfy near-term compliance windows. Airbus, for example, publicly targets a zero-emission commercial model by 2035 to stay within regulatory guardrails.

Electric propulsion routinely exceeds 1,000 V DC, yet historical regulations focus on 270 V architectures. The FAA issued special conditions for BETA Technologies' H500A to address new arc-fault and insulation-breakdown modes. Divergent rule-making between the FAA and EASA complicates global validation, obliging developers to engineer for multiple worst-case scenarios. Boeing's B777-9 still faces additional scrutiny for operations without conventional electrical power, underscoring how legacy programs experience certification delays when voltage envelopes widen. These uncertainties lengthen development cycles and inflate budgets, tempering the headline growth rate of the more electric aircraft market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Commercial airframes contributed 39.56% of the more electric aircraft market in 2024 as airlines replaced hydraulics with distributed electrical subsystems to curb maintenance outlay. Carriers highlight predictable life-cycle costs when line-replaceable units are solid-state rather than fluid-powered. Meanwhile, the eVTOL category posts a 15.65% CAGR to 2030, signaling rising investor confidence in city-pair air-taxi operations. Certification milestones by Joby and Archer shifted perceptions from concept to near-term service, unlocking fleet orders from regional operators. Military programs adopt electric actuation chiefly for radar-signature reduction, while business aviation follows for lower cabin noise and airport emissions.

The segment divergence suggests the more electric aircraft market may recalibrate traditional demand metrics. JSX's plan to accept more than 300 hybrid-electric regional aircraft after 2028 illustrates how regional carriers will leapfrog older fleets when viable. Accelerated orders shrink developmental lead times, forcing supply chains to allocate semiconductors first to eVTOL founders. Limited cell production for high-cycle batteries thus becomes a gating item for legacy narrow-body retrofits. Still, retrofit kits for older commercial types gain traction where full fleet renewal is financially prohibitive, ensuring a balanced order mix across aircraft classes.

Fixed-wing designs held 63.55% of the more electric aircraft market size in 2024, thanks to certified reference programs such as the B787 and A350 demonstrating electric environmental control in revenue service. These examples reassure regulators and lessors when approving high-voltage retrofits to narrow-body fleets. At the same time, rotary-wing and powered-lift concepts expand at 12.4% CAGR, buoyed by the step-change in hover efficiency that direct-drive electric motors deliver.

DARPA's XRQ-73 hybrid-electric drone blends rotor lift with fixed-wing cruise and showcases how power electronics endow vertical assets with stealth and endurance. Electra's short-takeoff regional demonstrator collapses the divide further, hinting that future taxonomy will focus on mission profile rather than wing planform. Rotary programs also exploit the absence of gearbox lubrication lines, cutting weight and maintenance. This blurring of categories could spur unified certification frameworks, smoothing entry for unconventional layouts and sustaining platform diversity inside the more electric aircraft market.

The More Electric Aircraft Market Report is Segmented by Aircraft Type (Commercial Aviation, Military Aviation, and More), Platform (Fixed Wing and Rotary Wing), System (Power Generation and Management, Actuation System, Thermal Management System, and More), End-User (OEM and Aftermarket), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 35.23% of 2024 spending as defense budgets backed megawatt demonstrators and the FAA provided early pathways for electric propulsion certification. Established Tier-1 suppliers in the United States anchor a mature ecosystem that co-locates research laboratories, test rigs, and human-capital pipelines. NASA's Electrified Powertrain Flight Demonstration program pairs GE and Boeing engineers to flight-test hybrid propulsion on a regional platform by 2027, reinforcing regional momentum.

Europe ranks second by value, buoyed by Clean Aviation grants and airport decarbonization policies. EU projects such as GOLIAT and EcoPulse channel public funds into liquid-hydrogen handling, superconducting cables, and hybrid-electric flight tests. EASA harmonization with the FAA accelerates transatlantic validation for eVTOLs, shortening time-to-market for dual-registry operators. Nevertheless, European suppliers face currency inflation in semiconductor procurement, prompting joint ventures with Asian foundries to secure wafer allocations.

Asia-Pacific records the highest growth at a 12.45% CAGR. China's Civil Aviation Administration earmarked dedicated low-altitude corridors for eVTOL logistics and passenger shuttles, compressing commercial deployment timelines. State plans to build a trillion-yuan general-aviation industry by 2030, injecting subsidies and regulatory certainty to attract foreign Tier-2 suppliers. Japan and South Korea focus on urban demonstrator flights for Expo-type events, offering a showcase before broader certification. However, airport readiness lags. India explores electric regional turboprops for short-haul routes under the UDAN connectivity scheme. The region's diverse market entries collectively translate into sustained order books for battery, motor, and avionics vendors, ensuring Asia-Pacific remains the principal volume driver in the more electric aircraft market.