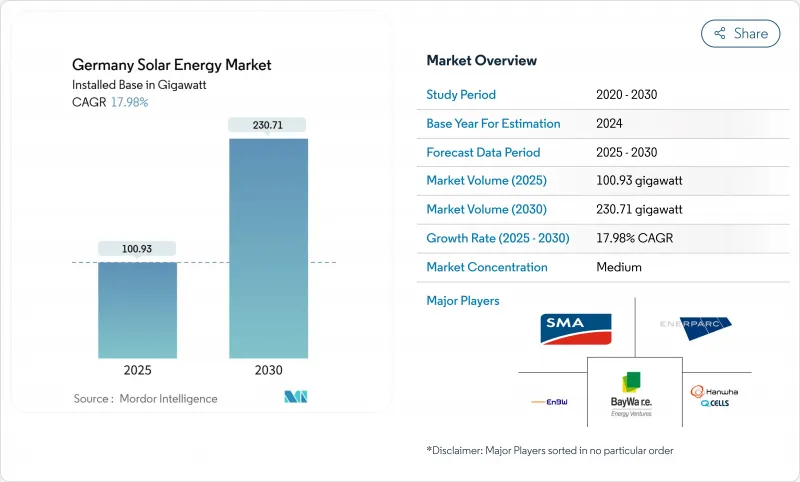

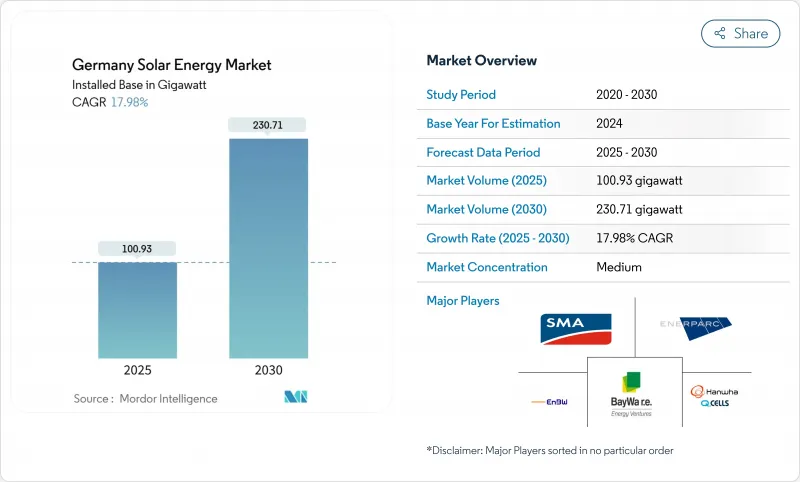

독일의 태양 에너지 설치 기반 시장 규모는 2025년 100.93기가와트로 추정되고, 2030년에는 230.71기가와트까지 성장할 전망이며, 예측 기간(2025-2030년) CAGR 17.98%로 성장할 것으로 예측됩니다.

이 확대는 2030년까지 자연 에너지를 80%로 만드는 국가의 목표와 2025년 초 태양광 발전 설치 용량이 100GW를 돌파한다는 이정표에 의해 강화되고 있습니다. 솔라 패키지 i에서 합리화된 허가, 모듈 가격의 87% 급락, 기업 오프테이크 계약으로 모든 시스템 규모의 프로젝트 파이프라인이 가속화되고 있습니다. 루프탑 의무화, 발코니에 플러그인 도입, 계통 요금 인플레이션 등으로 일반 가정과 중소기업이 매우 중요한 투자자가 되고 있으며, CSP와 같은 발전 전력 기술은 야간 피크 서포트용으로 시험적인 자금을 확보하기 시작하고 있습니다. 기관 투자자의 자금이 유입되어 경쟁이 격화되고 있지만, 송전망의 혼잡과 숙련 노동자의 부족이 신규 송전망 접속의 페이스를 계속 제약하고 있습니다.

솔라 패키지 I은 주택용으로 70%, 상업용으로 45%의 승인 기간을 단축했습니다. 특정 시스템 유형에 대한 고정 가격 구매 장려금의 인상과 새로운 지붕에 대한 주 수준의 의무화가 2026년까지 연간 설치 가능량을 4-5GW 인상하는 다층적인 뒷받침이 되고 있습니다. 법률의 간소화는 설치업체의 파이프라인을 넓히고, 소프트 비용을 줄이며, 도시 개조 기회에 대한 투자자의 신뢰를 강화했습니다.

고정가격 매입제도의 하락으로 전력 사업자는 장기적인 기업용 전력 구매 계약으로 방향전환했습니다. 독일은 2024년까지 유럽 2위의 PPA 시장이 되었으며 계약량은 3자리 성장을 보였습니다. 아마존과 메르세데스 벤츠와 같은 오프 테이커는 가격의 확실성을 보장하고 범위 2의 탈탄소화 목표를 달성하기 위해 PPA를 활용하고 보조금에 의존하지 않고 개발을 진행하도록 장려합니다. 이 추세는 매립된 산업 지역에서 100메가와트 이상의 프로젝트에 박차를 가해 자금 조달을 신속하게 완료하고 기존 경매 이외의 수익원을 다양화하고 있습니다.

2024년에는 2023년보다 97% 많은 태양광 발전의 출력이 억제되어 투자자의 수익이 악화되었습니다. 급속한 용량 증대와 송전망 증강 지연의 불일치로 인해 밸런싱 비용은 40억 유로를 넘어 소매 요금에 반영됩니다. 동적 라인 등급과 하이브리드 발전소 설계가 부분적인 구제책이 되는 한편, 태양 피크법에서는 마이너스 가격 시간대에 피드 인 캡을 도입하고 있습니다. 이러한 조치는 유용하지만, 도선의 확장이나 디지털 변전소의 전개를 대체할 수는 없습니다.

태양광 발전은 모듈 가격이 1W-p당 6-13유로센트로 낮고, LCOE가 1kWh당 3.7유로센트에 가깝기 때문에 2024년에는 독일의 태양광발전 시장 규모의 100%를 차지했습니다. 주택, 상업 시설 및 전력 회사의 이해 관계자는 설치 면적을 확대하지 않고 발전량을 밀어 올리는 고효율의 모노 PERC 모듈과 점점 증가하는 바이 페이셜 모듈을 지지하고 있습니다. 플라운호퍼 ISE의 조사는 페로브스카이트 실리콘 탠덤 셀의 효율이 33% 이상임을 입증하고 있으며, 추가 가격 하락을 지지하는 미래의 상승을 시사하고 있습니다.

집광형 태양광 발전은 현재 점유율 제로이지만, 2030년까지 연평균 복합 성장률(CAGR) 18.5%로 성장할 것으로 예측됩니다. 그 통합 축열은 야간의 피크 전력과 공정 열을 공급하여 태양광 발전의 보급이 진행됨에 따라 우려되는 간헐성을 다룹니다. 유럽 위원회의 로드맵은 CSP를 기존 지역 난방 네트워크 및 산업용 증기 루프와 하이브리드화하는 것으로 나타났으며 실증 시험에 대한 자금 지원을 시사합니다. 현재의 파일럿 플랜트가 운송 능력과 비용 목표를 달성하면, 이 분야는 향후 10년 이내에 독일 태양 에너지 시장을 보완하는 기둥으로 발전할 수 있습니다.

독일의 태양 에너지 시장 보고서는 기술별(태양광 발전, 집광형 태양광 발전), 컴포넌트별(PV 모듈, 인버터, 밸런스 오브 시스템, 축전지 시스템 등), 용도별(유틸리티 규모 태양광 파크, 상업 및 산업용 옥상, 주택 옥상, 기타)로 분류되어 있습니다. 시장 규모 및 예측은 설치 용량(GW)으로 제공됩니다.

The Germany Solar Energy Market size in terms of installed base is expected to grow from 100.93 gigawatt in 2025 to 230.71 gigawatt by 2030, at a CAGR of 17.98% during the forecast period (2025-2030).

The expansion is reinforced by the country's 80% renewables-by-2030 target and the early-2025 milestone of surpassing 100 GW of installed solar capacity . Streamlined permitting under Solar Package I, the 87% plunge in module prices, and corporate off-take agreements are accelerating project pipelines across all system sizes. Rooftop mandates, balcony-plug-in adoption, and grid-fee inflation have turned households and small businesses into pivotal investors, while dispatchable technologies such as CSP are starting to secure pilot funding for evening peak support. Competitive intensity is heightening as institutional capital flows in, yet grid congestion and skilled-labour shortages continue to constrain the pace of new grid connections.

Germany's solar energy market projects now clear rooftops without construction permits, as Solar Package I cut residential approval times by 70% and commercial by 45%. Higher feed-in incentives for specific system types and state-level obligations on new roofs have formed a multi-layered push that lifts annual installation potential by 4-5 GW by 2026. Legal simplification has broadened installer pipelines, reduced soft costs, and strengthened investor confidence in urban retrofit opportunities.

Falling feed-in tariffs redirected utility developers toward long-term corporate power purchase agreements. Germany became Europe's second-largest PPA market by 2024, with triple-digit growth in contracted volumes. Off-takers like Amazon and Mercedes-Benz use PPAs to lock in price certainty and meet Scope 2 decarbonisation goals, encouraging developers to move forward without subsidy dependence. The trend is spurring 100-plus-MW projects on reclaimed industrial land, closing financing swiftly, and diversifying revenue streams beyond traditional auctions.

Queue delays stretch to two years in several rural districts, curtailing 97% more solar output in 2024 than in 2023 and eroding investor returns. The mismatch between rapid capacity additions and slower grid reinforcement elevates balancing costs above EUR 4 billion, which feeds into retail tariffs. Dynamic line rating and hybrid plant designs offer partial relief, while the Solar Peak Law introduces feed-in caps during negative price hours. These measures, though helpful, cannot substitute for expanded conductor upgrades and digital substation roll-outs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solar photovoltaic commanded 100% of Germany's solar energy market size in 2024, enabled by module prices as low as 6-13 euro cents per W-p and LCOE near 3.7 euro cents per kWh. Residential, commercial, and utility stakeholders favour high-efficiency mono-PERC and increasingly bifacial modules that push yield without expanding footprint. Research by Fraunhofer ISE demonstrates perovskite-silicon tandem cell lab efficiencies above 33% , pointing toward future gains that can underpin further price declines.

Concentrated solar power holds no share today, yet is forecast to grow at an 18.5% CAGR through 2030. Its integrated thermal storage delivers evening peaking power and process heat, addressing intermittency concerns as PV penetration rises. European Commission roadmaps identify CSP hybridisation with existing district-heating networks and industrial steam loops, indicating supportive funding for demonstrators. If current pilot plants meet dispatchability and cost targets, the segment could evolve into a complementary pillar of the German solar energy market by the next decade.

The Germany Solar Energy Market Report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Component (PV Modules, Inverters, Balance-Of-System, Battery Energy-Storage Systems, and Others), Application (Utility-Scale Solar Parks, Commercial and Industrial Rooftop, Residential Rooftop, and Others). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).