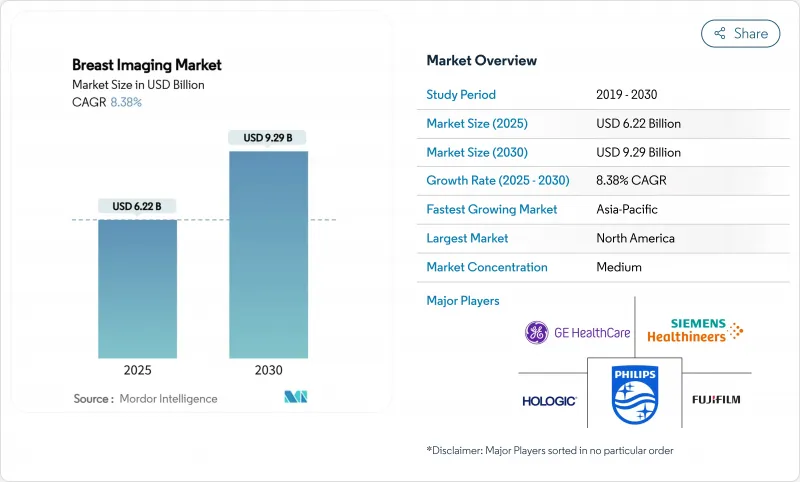

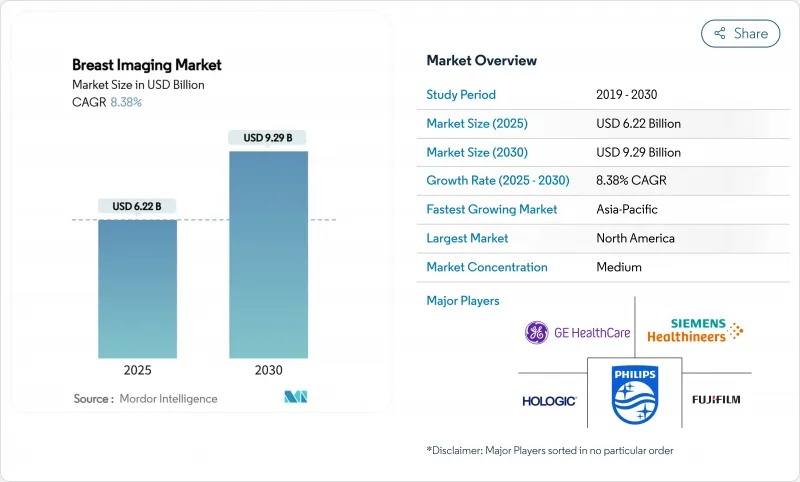

유방 영상 진단 시장 규모는 2025년에 62억 2,000만 달러, 2030년에는 92억 9,000만 달러에 이르고, 예측 기간 중 CAGR은 8.38%를 나타낼 전망입니다.

성장의 배경으로는 독서 시간을 단축하는 AI의 보급, 유방 밀도를 통지하는 FDA 유방 조영술 품질 기준법(MQSA) 규제의 진화, 3차원 스크리닝으로의 꾸준한 변화가 있습니다. 병원이 서비스 제공의 기반이 되는 것은 아니지만, 외래 영상 진단센터는 지불자가 비용이 덜 드는 환경으로 치료를 추진하고 환자가 편의를 요구함에 따라 빠르게 규모를 확대하고 있습니다. 수술 건수 증가는 노동력 부족과 사이버 보안 부족의 긴급성을 높이고 있으며, 이 둘이 새로운 장비의 구매 기준을 형성하고 있습니다. 지역별로는 북미가 선두 자리를 유지하고 있지만 아시아태평양은 정부 자금에 의한 검진의 전개와 중간층 확대를 배경으로 수익 증가가 가장 큽니다. 기존 벤더가 하드웨어의 강점과 독자적인 알고리즘을 결합하는 반면, 소규모 AI 전문 벤더가 가치 있는 워크플로의 틈새 시장을 열어 경쟁이 치열해지고 있습니다.

고위험 여성 인구의 확대는 진보된 영상 진단 수요를 지원합니다. 미국암협회는 2024년 미국에서 새롭게 31만 720명이 침윤성 유방암을 앓았고 4만 2,250명이 사망했으며 조기 발견의 가치를 높였습니다. 이환율은 동유럽에서 가장 급속히 상승하는 반면 비만 증가와 초산연령의 저하로 신흥경제국에서는 검진 코호트가 확대되고 있습니다. 고령화 사회는 폐경 후 위험이 급증하기 때문에 계획 입안자에게 용량을 확장하고 더 민감한 도구로 업그레이드하도록 촉구합니다. 정기적인 검진은 5년 생존율을 향상시키고, 지불자는 검진을 자유 재량 경비가 아니라 경비 절감책으로 취급하게 되어 왔습니다.

디지털 유방 토모신세시스는 조직 중첩 아테팩트를 줄이고 위양성 콜백을 최대 15%까지 줄이는 EU 가이드라인 업데이트를 통해 루틴 검진을 위해 DBT를 권장하고 공공시설에서 2차원 장치를 전반적으로 교체하도록 촉구했습니다. 미국에서 DBT는 환자의 선호도를 끌어들이고 의료법상의 위험을 줄이기 때문에 메디케어 요금 인하에도 불구하고 공급자는 여전히 업그레이드를 계속하고 있습니다. DBT를 트리어지 알고리즘과 결합하면 판독 시간이 단축되고 처리량이 향상되므로 센터는 일일 검사 건수 증가와 장비 보상 감소의 균형을 맞출 수 있습니다.

풀 장비의 스캐너의 가격은 40만-60만 달러로, 독립한 시설의 자본 예산은 늘어나고 있습니다. 2024년 11.72%, 2025년 9.67%라는 연속 메디케어 요금 인하가 투자 회수 계산을 미치게 합니다. 공급업체는 거래 거래 및 이용 기반 금융에 대항하고 있지만, 가격에 민감한 지역에서는 도입이 지연되고 있으며, 노후화된 2차원 플릿으로부터의 대체가 지연되고 있습니다.

Mammography는 2024년 매출의 38.585%를 차지하며 DBT가 모달리티 믹스를 재조합하는 중에서도 유방 영상 진단 시장을 지원했습니다. 3D 업그레이드 경로는 2030년까지 연평균 복합 성장률(CAGR) 12.57%를 나타내며 뛰어난 침윤 암 검출을 강조하는 유럽 위원회의 검진 지침에 의해 검증됩니다. 유방 초음파 검사는 고밀도 조직 및 고위험 집단에서 방사선을 사용하지 않는 평가를 제공하며 주요 보조 검사로 지속됩니다. 자기 공명 영상(MRI)은 유전 위험 집단에 대한 골드 표준의 지위를 유지하지만 비용과 조영제의 벽에 직면하고 있습니다.

영상 가이드하 생검 워크플로우는 영상 진단과 원활하게 통합되어 유방 조영술, 초음파 및 MRI 가이드에서 조직 채취를 간소화합니다. 진공 보조 시스템은 진단 수율과 환자의 편안함을 향상시키고 클립 유치의 진보는 수술 국소화를 지원합니다. MBI(Molecular 유방 영상 진단)는 다른 모달리티에서 결정적인 결과를 얻을 수 없는 경우 표적이 되는 문제 해결 수단이지만, 방사선 피폭 때문에 광범위한 사용에는 한계가 있습니다. 각 기술에 AI를 오버레이함으로써 진단의 일관성을 높이고, 관찰자의 편차를 억제하고, 알고리즘에 의한 지원을 일상 진료에 더욱 통합할 수 있습니다.

전리형 플랫폼은 여전히 세계 매출의 62.345%를 차지하고 있으며 국가 스크리닝 프로그램의 편재성을 재확인하고 있습니다. 그러나 비전리 모달리티는 2030년까지 연평균 복합 성장률(CAGR) 10.46%를 나타내고, 지불자와 환자의 심리가 방사선을 사용하지 않는 솔루션으로 이동하고 있습니다. 자동 유방 초음파 검사(ABUS)와 조영 초음파 검사는 핸드헬드 검사의 범위를 넘어 재현성과 감도의 우려에 대응합니다. 고자계 MRI 시스템은 해부학적 세부사항을 보다 상세하게 그리는 동시에 간소화된 프로토콜이 검사 시간과 비용을 단축합니다.

인공지능은 촬영 파라미터를 최적화함으로써 전리 검사의 피폭을 저감하고, 하이브리드 워크스테이션은 의심스러운 유방 X선 검사를 위한 세컨드룩 초음파 검사를 제안해 양 기술을 융합시키고 있습니다. 자본 비용은 여전히 MRI 쪽이 높지만 방사선에 관한 규제 준수의 경감에 의해 라이프 사이클의 절약이 됩니다. 향후 시장 경쟁은 전리선량을 최소화하거나 0으로 억제한 진단력을 제공할 수 있는지 여부에 달려 있습니다.

북미가 2024년 매출액의 36.29%를 차지했습니다. 유방 영상 진단 시장은 2024년 9월에 시행되는 연방 정부에 의한 고농도 유방 고시의 혜택을 받아 초음파 검사와 MRI의 보완 수요가 높아졌습니다. AI의 채택이 가장 빨리 성숙하는 것은 알고리즘의 조기 클리어런스와 벤처 자금이 폭넓은 전개를 지원하기 때문입니다. 그러나 포화 상태의 설치 기반에서는 교체가 주류이기 때문에 성장이 완만해집니다.

유럽은 스크리닝의 보급률이 높고 DBT를 권장하는 임상 지침이 통일되어 있습니다. 유럽인공지능법(European Artificial Intelligence Act)은 조화로운 승인 경로를 설정하고 검증을 길게 할 수 있지만, 결국 단일 디지털 시장을 창출합니다. 공중보건기구는 갱신주기에 공동 출자하고, 경쟁 입찰은 중간 규모 클리닉에 대한 접근을 확대하는 수량 기준 할인을 장려합니다.

아시아태평양의 CAGR은 10.78%로 가장 높습니다. 중국에서는 정부 보험 제도가 수백만 명의 여성에게 2년에 1번의 유방 그램을 제공하고 인도에서는 아유슈만 발라트(Ayushman Bharat)가 2차 도시로 이동 판매차를 달리고 있습니다. 중류 계급의 의식 향상 캠페인이나 국제 NGO와의 제휴가, 검진의 대상 범위를 한층 더 넓힙니다. 자본 지출은 1급 지하철에서 지방의 핵심 도시로 옮겨지며, 그곳에서는 핸드헬드 초음파와 엔트리 레벨 MRI가 저렴한 서비스를 가능하게 합니다. 규제의 이질성은 근본적이지만 현지 제조 인센티브가 세계 벤더의 합작 사업을 유치합니다.

중동 및 아프리카와 남미는 매출에서는 후진을 숭배하고 있지만, 일자리대의 꾸준한 성장을 이루고 있습니다. 석유 수출국인 걸프 국가는 공공 센터용 고급 스위트를 구입하지만, 사하라 이남의 아프리카는 이동 판매 차량과 기증자의 자금 지원에 의존하고 있습니다. 브라질은 공공 스크리닝 능력을 확대하고 있지만 상환이 지연되고 DBT의 전반적인 채용이 억제되고 있습니다.

The breast imaging market size stands at USD 6.22 billion in 2025 and is on course to reach USD 9.29 billion by 2030, reflecting an 8.38% CAGR over the forecast window.

Growth stems from widespread AI adoption that accelerates reading times, evolving FDA Mammography Quality Standards Act (MQSA) regulations that require dense-breast notifications, and a steady shift toward three-dimensional screening. Hospitals remain the foundation of service delivery, yet outpatient imaging centers scale rapidly as payers push care into lower-cost settings and patients look for convenience. Rising procedure volumes also magnify the urgency of workforce and cybersecurity shortfalls, both of which shape purchase criteria for new equipment. Regionally, North America keeps its leadership position, but Asia-Pacific delivers the greatest incremental revenue on the back of government-funded screening rollouts and middle-class expansion. Competitive intensity tightens as established vendors pair hardware strength with proprietary algorithms while smaller AI specialists carve out high-value workflow niches.

An expanding at-risk female population sustains demand for advanced imaging. The American Cancer Society predicts 310,720 new invasive cases and 42,250 deaths in the United States during 2024, reinforcing the value of early detection. Incidence climbs fastest in Eastern Europe, while rising obesity and later first-birth age widen the screening cohort across emerging economies. Ageing demographics amplify volumes because risk escalates steeply after menopause, driving planners to enlarge capacity and upgrade to higher-sensitivity tools. Regular screening improves five-year survival, and payers increasingly treat it as a cost-saving measure rather than a discretionary expense.

Digital breast tomosynthesis reduces tissue-overlap artefacts and lowers false-positive callbacks by up to 15% Updated EU guidelines recommend DBT for routine screening, prompting wholesale replacement of 2-D units in public fleets. Providers in the United States still upgrade despite Medicare fee cuts because DBT attracts patient preference and mitigates medicolegal risk. When paired with triage algorithms, DBT shortens interpretation time and lifts throughput, enabling centres to balance lower unit reimbursement with higher daily exam counts.

Full-featured scanners list between USD 400,000 and USD 600,000, stretching capital budgets for independent sites. Consecutive Medicare fee cuts of 11.72% in 2024 and 9.67% in 2025 erode payback calculations. Vendors counter with trade-in credits and usage-based financing, yet adoption lags in price-sensitive regions, slowing replacements of ageing 2-D fleets.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Mammography produced 38.585% of 2024 revenue, anchoring the breast imaging market even as DBT reshapes modality mix. The 3-D upgrade path supports a 12.57% CAGR to 2030, validated by European Commission screening guidance that highlights superior invasive-cancer detection. Breast ultrasound persists as the leading adjunct, providing radiation-free evaluation in dense tissue and in high-risk cohorts. Magnetic resonance imaging (MRI) retains gold-standard status for hereditary risk populations but faces cost and contrast-agent barriers.

Image-guided biopsy workflows integrate seamlessly with diagnostic imaging, streamlining tissue sampling under mammographic, ultrasound, or MRI guidance. Vacuum-assisted systems improve diagnostic yield and patient comfort, while clip-placement advances aid surgical localization. Molecular breast imaging (MBI) remains a targeted problem-solver when other modalities deliver inconclusive results, though radiation exposure limits broad use. AI overlays on each technique raise diagnostic consistency and cut observer variability, further embedding algorithmic support in daily practice.

Ionizing platforms still account for 62.345% of global sales, reaffirming their ubiquity in national screening programs. Yet non-ionizing modalities post a 10.46% CAGR through 2030 as payer and patient sentiment shifts toward radiation-free solutions. Automated breast ultrasound (ABUS) and contrast-enhanced ultrasound expand beyond handheld scans, addressing reproducibility and sensitivity concerns. High-field MRI systems push anatomic detail higher, while abbreviated protocols shorten table time and cost.

Artificial intelligence reduces exposure in ionizing studies by optimizing acquisition parameters, and hybrid workstations suggest second-look ultrasound for suspicious mammograms, blending both technology classes. Capital costs still tilt higher for MRI, but lifecycle savings accrue from reduced regulatory compliance on radiation. Over the forecast horizon, market competition will likely hinge on delivering diagnostic power with minimal or no ionizing dose.

The Breast Imaging Market Report is Segmented by Imaging Technique (Mammography, Breast Ultrasound, Breast MRI, Image-Guided Breast Biopsy, Molecular Breast Imaging), Technology (Ionizing Technology, Non-Ionizing Technology), Stage of Care (Screening, Diagnostic, Interventional/Therapeutic), End User (Hospitals, Diagnostic Imaging Centers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America produced 36.29% of 2024 revenue. The breast imaging market benefits from federally mandated dense-breast notifications effective September 2024, which lift demand for supplemental ultrasound and MRI. AI adoption matures fastest here because early algorithm clearances and venture funding support broad deployment. Growth moderates, however, because replacement purchases dominate a saturated installed base.

Europe follows with high screening penetration and unified clinical guidelines that now recommend DBT. The European Artificial Intelligence Act sets a harmonised approval path, lengthening validation but ultimately creating a single digital market. Public health agencies co-finance refresh cycles, and competitive tenders encourage volume-based discounts that widen access to mid-sized clinics.

Asia-Pacific shows the strongest 10.78% CAGR. Government insurance schemes in China fund biennial mammograms for millions of women, while India's Ayushman Bharat drives mobile vans into secondary cities. Middle-class awareness campaigns and international NGO partnerships further widen screening coverage. Capital spending migrates from tier-one metros to provincial hubs, where handheld ultrasound and entry-level MRI enable affordable services. Regulatory heterogeneity persists, but local manufacturing incentives attract global vendors into joint ventures.

The Middle East & Africa and South America trail in revenue but post steady single-digit growth. Oil-exporting Gulf states buy premium suites for public centres, whereas sub-Saharan Africa relies on mobile vans and donor funding. Brazil expands public screening capacity, but reimbursement lags, restraining wholesale adoption of DBT.