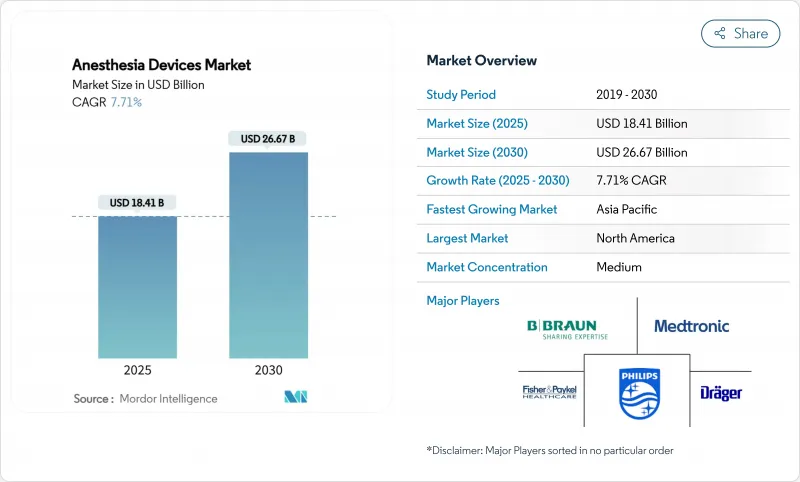

마취 기기 시장 규모는 2025년 184억 1,000만 달러로 추정되고, 2030년 262억 7,000만 달러에 이를 전망이며, CAGR 7.71%로 성장할 것으로 예측됩니다.

성장을 뒷받침하는 것은 마취제 사용량을 최대 50% 절감하는 인공지능 대응 모니터링 플랫폼, 수술 건수의 외래 환경으로의 급속한 시프트, 외래 진료소의 효율 요건에 맞는 휴대용 워크스테이션 수요 급증입니다. 북미는 계속해서 세계적인 수익의 중심이지만, 아시아태평양은 각국 정부가 새로운 수술실에 자금을 공급하고 현지 제조업체가 규모를 확대함에 따라 급속히 확대하고 있습니다. 지구온난화 계수가 높은 마취 가스를 대상으로 하는 환경 규제로 제품 설계의 우선순위는 저유량 공급과 휘발성 가스 포착 시스템으로 변화하고 있습니다. 가장 치열한 경쟁은 전달, 환기 및 분석을 단일 워크플로우로 통합한 통합 플랫폼입니다.

최면제 및 흡입제를 실시간으로 적정하는 폐쇄형 루프 시스템은 약물 소비량을 최대 50% 줄이고 의료 제공업체에게 측정 가능한 비용 절감을 제공합니다. 머신러닝 알고리즘을 활용한 FDA 인가의 침해 수용 지표는 현재 진통제의 깊이를 개인화하고 통증 평가에서 인종적 편향을 줄이고 있습니다. 뇌기능 모니터는 리콜에 대한 인식을 64% 줄이고 고급 모니터링의 가치 제안을 강화하고 있습니다. 공급업체는 터치스크린 인터페이스, HL7 지원 데이터 포트 및 클라우드 게이트웨이를 통합하여 수술 중 데이터를 전자 의료 기록에 통합합니다. 경쟁업체와의 차별화는 회복 속도, 합병증 감소, 총소유비용 감소를 입증할 수 있는지 여부에 달려 있습니다. Algorithmic Devices는 고성능 컴퓨팅 리소스, 임상 데이터 세트 및 시판 후 조사 팀이 필수적이기 때문에 중소기업은 자본 및 규제 측면에서 장애물에 직면하고 있습니다.

외래 센터의 연간 수술 건수는 21% 증가했고, 2034년에는 4,400만 건에 달할 것으로 예측되고 있으며, 정형외과, 척추, 소화기 수술이 그 최전선에 있습니다. 아시아태평양의 60세 이상 인구는 2050년까지 주민의 22.2%를 차지할 전망이며, 심장혈관 및 종양 치료에서 전신 마취 수요가 가속화됩니다. 저침습 수술로의 이행에 의해 종래는 입원 환자였던 심장 절제술이나 척추 고정술이 외래로 실시할 수 있게 되었습니다. 병원 수술실 용량의 제약은 독립형 수술 허브에 수십억 달러 규모의 투자를 유도하고 있습니다. 기기 제조업체는 일회용 회전율의 향상과 수술실 간을 쉽게 이동할 수 있는 컴팩트한 기기의 필요성으로부터 이익을 얻고 있지만, 일괄 상환률에서 오는 비용 압력에도 대처해야 합니다.

저자원 병원의 자본 예산에서는 정가가 20만 달러를 넘는 고급 워크스테이션을 구입할 수 있는 것은 드물고, 서비스 계약에 의해 구입 가격의 10-15%가 매년 가산되는 경우가 많습니다. 바이오메디컬 엔지니어의 훈련이 불충분하고 제조업체의 현장 팀이 넓은 지역을 다루기 때문에 수리 지연이 만연합니다. 자금 조달, 교육, 가동 보증을 결합한 매니지드 기기 서비스 계약이 인기를 끌고 있지만, 구매자를 10년 단위로 구속하기 때문에 재정의 유연성이 손상됩니다. AI 지원 장비는 클라우드 계약 및 보안 업데이트에 추가 비용이 듭니다. 채용 곡선에 편차가 있기 때문에 마취 기기 시장은 하이테크 층과 기본 케어 층으로 나눌 위험이 있습니다.

마취기는 2024년 마취 기기 시장 매출의 42.34%를 차지하였고, 모든 수술실의 자본 기반으로서의 지위를 명확히 했습니다. 교환 사이클은 고속 피스톤 환기 장치, 약물 정량 공급 장치, 실시간 가스 분석기 등 병원 데이터 백본에 피드를 갖춘 프리미엄 유닛을 선호합니다. 15인치 정전용량 터치스크린 및 HL7 상호 운용성을 갖춘 모델과 같은 차세대 워크스테이션은 완벽한 디지털 수술실을 추구하는 시설에 호소하고 있습니다. 대규모 병원에서는 7-9년마다 업그레이드가 이루어지기 때문에 대형 벤더에게는 분기별 수익을 좌우하는 것과 같이 정리된 규모의 주문이 발생합니다. 환경에 대한 고려를 통해 엔지니어는 온실가스 배출을 최대 65%까지 줄이는 휘발성 약물 포착 모듈을 통합하고 있습니다.

일회용 및 액세서리는 CAGR 9.54%로 마취 기기 시장에서 가장 빠른 속도로 성장합니다. 단일 사용 호흡 회로, 성문 에어웨이, 마취 심도 전극은 수술 횟수와 밀접하게 연동된 경상 수익을 제공합니다. 팬데믹 후 감염 제어 프로토콜의 강화 및 즉시 사용할 수 있는 멸균 키트의 편리성이 재사용 가능한 동등품을 계속해서 대체하고 있습니다. 지속가능성에 대한 노력은 퇴비화 또는 재사용 가능한 회로를 조기에 시험적으로 도입하고 수요 패턴을 재구성할 수 있지만, 일회성으로 인한 마취 기기 시장 규모는 10년 후까지 기계 수입을 초과할 것으로 예측됩니다. 독자적인 일회용 하드웨어 플랫폼과 패키징하는 벤더는 락인을 강화해, 마진을 안정시킵니다.

북미는 2024년 매출액의 40.23%를 차지했으며, 수술 건수가 많아, 외래 수술에 대한 상환 확립, AI 대응 플랫폼의 조기 도입 등에 지지를 받았습니다. 미국 지급자는 2023년 외래센터에 68억 달러를 환불했는데, 이는 전년 대비 15.4% 증가했으며 지속적인 절차 전환을 입증하고 있습니다. 상호 운용성을 장려하는 연방 정부의 이니셔티브도 네트워크 지원 워크스테이션으로의 업그레이드를 가속화하고 있습니다. 캐나다는 단일 지불 모델을 채택하고 있기 때문에 자본 투자는 다소 억제되었지만 시뮬레이션 기반 마취 교육은 통합 교육 솔루션 수요를 견인하고 있습니다. 멕시코는 의료 관광의 혜택을 누리고 있으며, 민간 병원은 비용 효율적인 선택적 수술을 요구하는 외국인 환자를 유치하기 위해 프리미엄 전달 시스템에 투자를 촉구하고 있습니다.

아시아태평양은 CAGR 8.34%로 가장 빠르게 성장이 전망되는 지역입니다. 중국과 인도는 공공 예산을 제3차 병원과 대량 조달 제도로 향하게 하고, 비용 경쟁력 있는 장비를 제공하는 국내 벤더를 우대하고 있습니다. 인도네시아는 2025년 IPO 때 1,200만 달러의 IFC 기축 투자를 받아 현지 생산 능력을 확대했습니다. 일본의 원조기관이 국경을 넘어서는 기술 이전에 자금을 제공한 것은 이 지역이 세계적으로 건강의 공평성을 중시하고 있음을 반영하고 있습니다. 벤처 기업의 자금 조달은 2021년 최고 수준에 비해 감소했지만, 저자원 환경을 위한 폐쇄형 루프 솔루션을 제공하는 AI 벤처 기업에 대한 자금 제공은 계속되고 있습니다. 이 지역의 마취 기기 시장 규모는 인구동태의 고령화 및 라이프스타일의 변화에 따른 심혈관질환과 종양학의 업무량 증가로 혜택을 받습니다.

유럽은 데스플루란을 단계적으로 폐지하고 병원의 이산화탄소 배출량을 줄이는 국가적 의무에 힘입어 중요한 지위를 유지하고 있습니다. 영국과 스칸디나비아 병원은 낮은 유량의 세보플루란과 정맥내 프로토콜을 지원하기 위해 파이프라인을 재설계하고 기존 워크스테이션에 설치하는 휘발성 포착 카트리지 수요에 박차를 가하고 있습니다. 독일과 프랑스는 엄격한 시판 후 감시를 부과하고 있으며, 제조업체는 실제 성능 모니터링에 자원을 나누도록 촉구하고 있습니다. 한편 중동 및 아프리카에서는 장비, 서비스, 트레이닝을 다년간 계약에 번들한 매니지드 기기 서비스 모델 하에서 도입이 가속화되고 있습니다. 예를 들어, 케냐의 국립소개병원에서는 세계 벤더와 턴키 계약을 맺고 업타임과 교육을 보장함으로써 기존의 유지보수 장애물을 낮추고 있습니다.

The anesthesia devices market size is valued at USD 18.41 billion in 2025 and is forecast to reach USD 26.27 billion by 2030, advancing at a 7.71% CAGR.

Growth is propelled by artificial-intelligence-enabled monitoring platforms that cut anesthetic agent use by up to 50%, the rapid shift of surgical volumes to ambulatory settings, and surging demand for portable workstations that match the efficiency requirements of outpatient theaters. North America continues to anchor global revenues, yet Asia-Pacific is expanding faster as governments fund new operating suites and local manufacturers scale up. Environmental regulations that target high-global-warming-potential anesthetic gases are reshaping product design priorities toward low-flow delivery and volatile capture systems. Competitive intensity is greatest in integrated platforms that bring delivery, ventilation, and analytics into a single workflow.

Closed-loop systems that titrate hypnotics and inhalational agents in real time are trimming drug consumption by up to 50%, producing measurable cost savings for providers. FDA-cleared nociception indices that harness machine-learning algorithms now personalize analgesic depth and reduce racial bias in pain assessment. Brain-function monitors have cut awareness with recall by 64%, strengthening the value proposition of advanced monitoring. Vendors are embedding touchscreen interfaces, HL7-ready data ports, and cloud gateways that channel intraoperative data into the electronic medical record. Competitive differentiation hinges on demonstrating faster recovery, fewer complications, and lower total cost of ownership. Smaller firms face capital and regulatory hurdles because high-performance compute resources, clinical data sets, and post-market surveillance teams are compulsory for algorithmic devices.

Ambulatory centers are projected to lift annual case throughput by 21%, reaching 44 million procedures by 2034, with orthopedic, spine, and gastroenterology cases at the forefront. Asia-Pacific's population aged 60+ will represent 22.2% of residents by 2050, accelerating demand for general anesthesia in cardiovascular and oncologic interventions. Migration toward minimally invasive techniques enables outpatient cardiac ablations and spine fusions that traditionally remained inpatient. Capacity constraints in hospital operating rooms are triggering multibillion-dollar investments in standalone surgical hubs. Device makers benefit from higher disposable turnover and the need for compact machines that roll easily between theaters, yet they must also address cost pressures stemming from bundled reimbursement rates.

Capital budgets in low-resource hospitals rarely stretch to premium workstations whose list prices can surpass USD 200,000, and service contracts often add 10-15% of purchase price annually. Break-fix delays are widespread because biomedical engineers lack training and manufacturers' field teams cover large territories. Managed-equipment-service contracts that combine financing, training, and uptime guarantees are gaining traction, yet they lock buyers into decade-long commitments that strain fiscal flexibility. AI-enabled units impose further costs for cloud subscriptions and security updates. An uneven adoption curve risks splitting the anesthesia devices market into high-tech and basic-care tiers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Anesthesia machines produced 42.34% of the anesthesia devices market revenue in 2024, underscoring their status as the capital cornerstone of every operating suite. Replacement cycles favor premium units with high-speed piston ventilators, volumetric agent delivery, and real-time gas analysis that feed into the hospital data backbone. Next-generation workstations, such as models equipped with 15-inch capacitive touchscreens and HL7 interoperability, appeal to facilities pursuing fully digital operating rooms. Larger hospitals upgrade every seven to nine years, creating lumpy but sizeable orders that shape quarterly earnings for leading vendors. Environmental imperatives are leading engineers to incorporate volatile-agent capture modules that cut greenhouse emissions by up to 65%.

Disposables and accessories are set to grow at a 9.54% CAGR, the fastest pace in the anesthesia devices market. Single-use breathing circuits, supraglottic airways, and depth-of-anesthesia electrodes deliver recurring revenues tightly aligned with procedure counts. Heightened infection-control protocols post-pandemic and the convenience of ready-to-use sterile kits continue to displace reusable equivalents. The anesthesia devices market size attributed to disposables is expected to outpace machine revenues by the end of the decade, though sustainability initiatives are prompting early pilots of compostable or reusable circuits that could reshape demand patterns. Vendors that package proprietary disposables with hardware platforms strengthen lock-in and stabilize margins.

The Anesthesia Devices Market Report is Segmented by Product Type (Anesthesia Machines and Disposables & Accessories), End User (Hospitals, Ambulatory Surgery Centers, and Clinics & Nursing Facilities), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 40.23% of 2024 revenue in the anesthesia devices market, buoyed by high surgical volumes, established reimbursement for outpatient procedures, and early uptake of AI-enabled platforms. U.S. payers reimbursed ambulatory centers USD 6.8 billion in 2023, a 15.4% year-on-year rise, validating sustained procedural migration. Federal initiatives that encourage interoperability also accelerate upgrades to network-ready workstations. Canada follows a single-payer model that somewhat tempers capital spending, but simulation-based anesthesia education drives demand for integrated training solutions. Mexico benefits from medical tourism, prompting private hospitals to invest in premium delivery systems to attract foreign patients seeking cost-effective elective surgeries.

Asia-Pacific represents the fastest growing territory at an 8.34% CAGR. China and India channel public budgets into tertiary hospitals and mass-procurement schemes that favor domestic vendors offering cost-competitive devices. Indonesia secured a USD 12 million IFC cornerstone investment during a 2025 IPO to enlarge local production capacity. Japanese aid agencies have financed cross-border technology transfers, reflecting the region's outward focus on global health equity. Venture funding dipped relative to 2021 highs, but still underwrites AI start-ups tailoring closed-loop solutions for low-resource settings. The anesthesia devices market size in the region benefits from rising cardiovascular and oncology workloads linked to aging demographics and lifestyle shifts.

Europe retains a significant stake, driven by national mandates to phase out desflurane and cut hospital carbon footprints. Hospitals in the United Kingdom and Scandinavia have re-engineered pipelines to support low-flow sevoflurane and intravenous protocols, spurring demand for volatile capture cartridges that attach to existing workstations. Germany and France impose stringent post-market surveillance, pushing manufacturers to allocate resources for real-world performance monitoring. Meanwhile, the Middle East and Africa see accelerating uptake under managed-equipment-service models that bundle devices, service, and training into multiyear agreements. Kenya's national referral hospitals, for example, run turnkey contracts with global vendors that guarantee uptime and training, easing traditional maintenance hurdles.