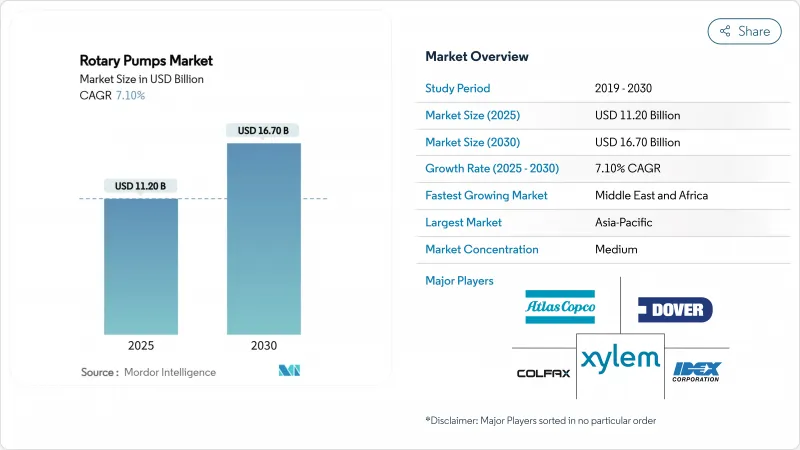

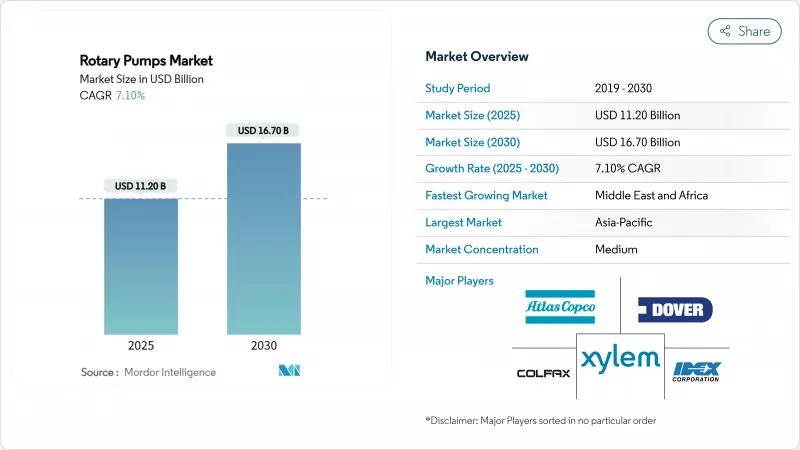

로터리 펌프 시장의 2025년 시장 규모는 112억 달러로 추정되고, 2030년에는 167억 달러에 이를 전망이며, CAGR 7.1%로 성장할 것으로 예측됩니다.

중동의 석유 자산에서의 브라운필드 업그레이드 증가, 중국의 기록적인 정제 처리 능력, 브라질의 신세대 FPSO는 고점도 유체 및 다상 유체를 처리할 수 있는 API-676 준수 유닛에 대한 수요를 확대하고 있습니다. 미국 식품안전근대화법(Food Safety Modernization Act)과 유럽위생지령(Europe's hygienic Directives)에 근거한 엄격한 클린 인플레이스 의무화로 식품용 기어와 편심 디스크 설계의 채용에 박차가 걸리고 있습니다. 또한 석유화학 사업자는 로터리 펌프와 스마트 센서를 통합하여 가동 시간을 향상시키고 플레어링을 줄이기 위해 노력하고 있습니다. 드라이가스 또는 씰리스 구성으로의 기술 업그레이드는 사용자가 VOC 규제를 강화하는 데 도움을 주었으며, 26년간 FPSO 용선이 장기 서비스 계약을 보장하기 때문에 애프터마켓 기회가 확대되고 있습니다.

중동의 국영 석유 회사는 자산 수명을 연장하고 생산을 유지하기 위해 성숙 유전의 현대화를 추진하고 있습니다. 쿠웨이트 석유 회사는 그레이터 버건에 위치한 14개의 석유 센터를 에멀젼과 높은 모래 함량에 내성이 있는 로터리 펌프를 필요로 하는 새로운 분리 트레인으로 오버홀하고 있습니다. 아부다비 해양 석유 회사는 일량 42만 5,000 배럴의 생산을 유지하기 위해 자쿠 웨스트 슈퍼 컴플렉스와 중앙 슈퍼 컴플렉스를 개조하고 있습니다. 사우디 알람코는 크라이스 중앙 플랜트의 스태빌라이저 하단 펌프를 최적화하여 일량 126만 3,000 배럴을 처리하면서 에너지를 줄였습니다. 이러한 리노베이션은 폴리머가 많은 유체 및 증기 주입 온도를 관리하는 야금학 및 가변 속도 드라이브를 업그레이드하는 API-676 호환 트윈 스크류와 기어 펌프를 지정합니다. 공급업체는 수십년전 유닛을 디지털 모니터링 모델로 교체하는 스왑아웃 프로그램에서 애프터마켓 수익을 얻고 있습니다.

중국은 2024년에 일량 1,480만 배럴의 원유를 처리했으며, 2025년으로 예정되어 있는 일량 40만 배럴의 옥룡 프로젝트 등, 정유소와 석유화학의 통합 컴플렉스를 계속 증설하고 있습니다. 이러한 기지에서는 나프타의 수소화 처리, LPG의 이송, 폴리머 피드의 취급이 로터리 펌프에 의존하고 있어 다운타임이 현장 전체에 체인하고 있습니다. 인도에서는 2030년까지 생산 능력을 4,600만 톤으로 끌어올리기 위해 1,420억 달러의 석유화학 투자를 계획하고 있으며, Vadinar에 있는 Nayara Energy사의 80억 달러의 에탄 크래커가 그 하이라이트입니다. 공영의 정제회사인 IndianOil, BPCL, HPCL은 각각 240℃의 용융 단량체를 취급할 수 있는 스크류 펌프 및 기어 펌프를 필요로 하는 폴리프로필렌 트레인을 증설하고 있습니다. 올전화의 정유소 컨셉과 제로 플레어링의 의무화에 의해 실리스의 자기 구동 유닛이 채용되어 도주 배출이 억제됩니다.

인증되지 않은 임펠러, 부싱 및 씰 키트가 공급망에 유입됨으로써 안전성이 위협되고 평균 고장 간격이 짧아집니다. ADMA-OPCO의 위조 방지 프로그램은 검사관을 훈련하고 공급업체를 인증 목록에 잠급니다. 중국의 OEM은 여전히 매출의 2% 미만만 RandD에 투자하고 있으며, 모방품에 대한 인식의 격차에 대항할 수 있는 품질 향상이 제한되어 있습니다. 구매자는 수입 펌프를 선택하고 위조 부품이 정품으로 보이고 보증을 해치는 회색 시장을 강화합니다.

외부 기어식 펌프는 중점도 용도를 위한 견고한 설계로 2024년 로터리 펌프 시장 점유율의 32%를 차지했습니다. FPSO의 톱사이드 및 폴리머 서비스는 맥동을 최소화한 부드러운 흐름이 필요하므로 트윈 스크류 유닛이 CAGR로 가장 빠른 7.71%를 실현합니다. 2019-2024년, 외부 기어 유형은 연률 3.2%의 성장을 기록했지만, 트윈 스크류는 고성능으로의 시프트를 반영하여 6.8%로 전진했습니다. 인터널 기어 크레센트 펌프는 부드러운 취급을 요구하는 과자류 및 제약 배치에 대응하고 있습니다. 베인 펌프는 자동차 윤활유 회로에서 계속 사용되지만 에너지 효율의 압력에 직면하고 있습니다. IIoT 지원 기어 박스의 상승으로 운영자는 클리어런스를 모니터링하고 캐비테이션을 피하기 위해 속도를 조정할 수 있습니다.

원유 증진 회수에 있어서의 트윈 스크류 어셈블리의 채용에 의해 전단 내성과 내가스 락성이 향상됩니다. SMU 코딩된 API-676 기계는 낮은 회전으로 작동하여 씰 수명을 연장합니다. 클라우드 분석과의 통합은 유량 드리프트가 발생하기 전에 마모를 감지하여 예정되지 않은 다운타임을 줄입니다. OEM은 폴리머 마모를 견디는 HVOF 코팅 로터로 차별화를 도모합니다. 비용 중심의 블렌더 스키드에서는 표준화된 부품이 유지보수를 줄이기 때문에 외부 기어 모델이 여전히 선호되고 있습니다. 특허 활동은 소음을 줄이고, 설치 면적을 늘리지 않으며, 높은 토출 압력을 허용하는 나선형 스크류 프로파일에 중점을 둡니다.

석유 및 가스 분야는 정유소, 파이프라인, 탱크팜이 API 준거 장비를 요구하고 있기 때문에 2024년 로터리 펌프 시장에서 27.5%의 점유율을 유지했습니다. 그러나 식품 및 음료는 FSMA와 EC1935 규정이 위생에 대한 기대를 엄격하게 하기 때문에 2030년까지 연평균 복합 성장률(CAGR) 7.91%로 가장 빠른 성장이 전망됩니다. 2019-2024년 석유 및 가스는 연률 4.1% 성장했지만, 식음료은 6.9% 상승했습니다. 발전도 수요를 끌어올리지만, 이것은 플로서브의 3분기 연속 1억 달러를 초과하는 원자력 수주가 이야기하고 있습니다. 화학제품 및 석유화학제품 사업자는 200℃ 이상의 부식성 단량체를 취급하는 실리스 펌프를 지정하고 있습니다.

Midleton 증류소에서는 생산성이 50% 향상된 것을 이유로 식품 가공업자가 초콜릿이나 시럽의 이송에 스테인리스제 인터널 기어 펌프로 전환하고 있습니다. 유럽의 크래프트 맥주 제조업체는 효모 생존율을 유지하는 이녹스파의 저전단 로브 펌프를 채용하고 있습니다. 수도 사업자는 에너지를 30% 줄이는 로터리 로브 블로어를 평가하고 있지만, 고속 터보는 대규모 플랜트에서 경쟁하고 있습니다. 석유화학 제조업체는 로터리 펌프를 디지털 트윈과 통합하여 캐비테이션을 시뮬레이션하고 크래커의 턴어라운드에 맞게 유지보수 일정을 정하고 있습니다.

아시아태평양은 연간 1,350만 대 이상의 펌프 유닛을 판매하는 중국을 필두로, 2024년에는 로터리 펌프 시장에서 38.4%의 점유율을 차지했습니다. 에너지 효율적인 기어 드라이브 및 도시 수도 프로젝트에 대한 베이징 보조금이 수요를 지원합니다. 인도의 1,420억 달러의 석유화학 계획은 국내 펌프 제조를 활발히 하고 세계 OEM 라이선스 계약을 끌어들입니다. 일본은 반도체의 세정 라인에 정밀 정량 펌프를 공급하고, 한국의 조선소는 VLCC 엔진 룸에 API-676 트윈 스크류 유닛을 채용합니다.

중동은 쿠웨이트 및 아부다비가 분리 트레인을 업그레이드했고 사우디 알람코가 펌프를 업데이트하여 에너지를 줄였기 때문에 CAGR로 가장 빠른 7.81%를 기록했습니다. 브라운필드에서는 모래를 포함한 에멀젼을 캐비테이션 없이 처리할 수 있는 스크류 펌프를 채용하고 있습니다. 카타르가스는 LNG 보일오프용 저유량 인터널 기어 펌프에 투자하고 메탄 규제를 추진하고 있습니다. 각국의 챔피언은 담맘과 무스카트에 새로운 조립 허브를 건설하는 원동력이 되는 현지에 뿌리를 둔 함량의 임계값을 만들어 냅니다.

북미는 성숙하지만 기술적으로 진행된 시장입니다. FSMA 규정은 낙농 및 양조업에서 기어 펌프의 매출을 증가시키고 셰일 가스 생산업체는 VOC를 억제하기 위해 자기 결합 펌프를 채택합니다. 슬루자는 남미 캐롤라이나 주 이즐리에 1,000만 스위스 프랑을 투자하여 빌드 미국의 의무에 대응하는 수중 펌프 라인을 증설했습니다. 캐나다의 오일 샌드 사업자는 희석제 펌프를 빙점 하에서 30% 가스 부피 분율을 처리하는 2축 스크류 모델로 교체했습니다.

유럽은 배출가스를 중시합니다. TA-Luft의 개정으로 정유소는 건식 가스 씰을 채택하고 지역의 크래프트 맥주 제조업체는 위생적인 로터리 로브 펌프를 채택합니다. 노르웨이의 전기 해양 유전에서는 메탄을 제한하기 위해 씰이없는 물 주입 펌프가 지정되었습니다. EU의 Horizon 프로그램의 보조금은 화학 펌프의 디지털 트윈 연구를 지원합니다.

남미는 브라질의 80억 달러 규모의 FPSO 투자로 혜택을 받고 있습니다. P-85의 현지 함량이 25%에 달하면서 브라질산 가공 케이스에 대한 수요가 증가하고 있습니다. 아르헨티나의 바카 무에르타 셰일은 고압 스크류 펌프가 필요한 가스 처리 공장을 개발합니다. 콜롬비아의 바이오디젤 확장은 팜유 원료를 위한 스테인리스강 기어 펌프를 설치합니다.

사하라 이남의 아프리카에서는 소규모 기반에서 성장하지만, 고급 스크류 펌프의 채용을 제한하는 유지 보수 기술의 격차에 직면하고 있습니다. 나이지리아의 모듈식 정유소는 저비용 외기어 유닛을 선택하고, 남아프리카의 채굴 펌프는 도난 대책으로 IIoT 센서를 개장하고 있습니다.

The rotary pumps market is valued at USD 11.2 billion in 2025 and is forecast to reach USD 16.7 billion by 2030, advancing at a 7.1% CAGR.

Rising brownfield upgrades across Middle East oil assets, China's record refining throughput, and Brazil's new-generation FPSOs are expanding demand for API-676 compliant units capable of handling high-viscosity and multiphase fluids. Strict clean-in-place mandates under the US Food Safety Modernization Act and Europe's hygienic directives spur uptake of food-grade gear and eccentric-disc designs. Energy-sector retrofit programs favour pump replacement studies that cut energy use and emissions, while petrochemical operators integrate rotary pumps with smart sensors to improve uptime and reduce flaring. Technology upgrades toward dry-gas or seal-less configurations help users meet tightening VOC rules, and aftermarket opportunities grow as 26-year FPSO charters guarantee long service contracts.

Middle East national oil companies are modernizing mature fields to extend asset life and sustain production. Kuwait Oil Company is overhauling 14 gathering centers in Greater Burgan with new separation trains that need rotary pumps tolerant of emulsions and high sand content. Abu Dhabi Marine Operating Company is modifying the Zakum West and Central super complexes to keep 425,000 barrels per day flowing, which requires pumps engineered for variable viscosity crude under corrosive offshore conditions. Saudi Aramco optimised stabilizer bottom pumps at the Khurais central plant, cutting energy while processing 1,263,000 barrels per day. These retrofits specify API-676 compliant twin-screw and gear pumps with upgraded metallurgy and variable-speed drives that manage polymer-rich fluids and steam-injection temperatures. Suppliers gain aftermarket revenues from swap-out programs that replace decades-old units with digitally monitored models.

China processed 14.8 million barrels per day of crude in 2024 and keeps adding integrated refinery-petrochemical complexes, including the 400,000 barrels per day Yulong project scheduled for 2025. Such hubs rely on rotary pumps for naphtha hydrotreating, LPG transfer, and polymer feed handling where downtime cascades across the site. India plans USD 142 billion in petrochemical investment that will push capacity to 46 million tonnes by 2030, highlighted by Nayara Energy's USD 8 billion ethane cracker at Vadinar. Public refiners IndianOil, BPCL, and HPCL are each adding polypropylene trains that demand screw and gear pumps able to handle molten monomers at 240 °C. All-electric refinery concepts and zero-flaring mandates drive adoption of seal-less magnetic-drive units that curb fugitive emissions.

Uncertified impellers, bushings, and seal kits entering supply chains threaten safety and shorten mean-time-between-failure. ADMA-OPCO's counterfeit-prevention program trains inspectors and locks vendors to approved lists. Chinese OEMs still invest less than 2% of sales in RandD, constraining quality upgrades that could combat counterfeit perception gaps. Buyers choose imported pumps, reinforcing a grey market where fake parts appear genuine and undermine warranties.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

External-gear pumps held 32% of the rotary pumps market share in 2024 due to their robust design for medium-viscosity duties. Twin-screw units deliver the fastest 7.71% CAGR as FPSO topsides and polymer services need smooth flow with minimal pulsation. From 2019-2024, external-gear variants posted 3.2% annual growth, while twin-screw advanced at 6.8%, reflecting a shift toward higher performance. Internal-gear crescent pumps cater to confectionery and pharma batches that demand gentle handling. Vane pumps continue in automotive lube circuits but face energy-efficiency pressure. The rise of IIoT-ready gearboxes lets operators monitor clearances and adjust speed to avoid cavitation.

Adoption of twin-screw assemblies in enhanced oil recovery improves shear tolerance and gas-locking resistance. SMU-coded API-676 machines run at lower RPM, extending seal life. Integration with cloud analytics flags wear well before flow-rate drift, cutting unplanned downtime. OEMs differentiate with HVOF-coated rotors that survive polymer abrasives. External-gear models remain favoured in cost-sensitive blender skids were standardised parts lower maintenance. Patent activity focuses on helical screw profiles that reduce noise and allow higher discharge pressures without increasing footprint.

The oil and gas segment retained 27.5% share of the rotary pumps market in 2024 as refineries, pipelines, and tank farms demand API-compliant equipment. However, food and beverage post the quickest 7.91% CAGR through 2030 as FSMA and EC1935 rules tighten hygiene expectations. From 2019-2024, oil and gas grew 4.1% annually, while food and beverage rose 6.9%. Power generation also lifts demand, illustrated by Flowserve's >USD 100 million nuclear orders in three straight quarters. Chemical and petrochemical operators specify seal-less pumps that handle corrosive monomers at temperatures above 200 °C.

Food processors switch to stainless internal-gear pumps for chocolate and syrup transfer, citing 50% productivity gains at Midleton Distilleries. Craft brewers in Europe adopt low-shear lobe pumps from INOXPA that sustain yeast viability. Water utilities evaluate rotary lobe blowers that cut energy by 30%, but high-speed turbos compete on large plants. Petrochemical majors integrate rotary pumps with digital twins to simulate cavitation and schedule maintenance around cracker turnarounds.

Rotary Pumps Market Report is Segmented by Type (External-Gear, Internal-Gear, and More), End-User Industry (Oil and Gas, Power Generation, and More), Discharge Pressure (Up To 10 Bar, 10-25 Bar, 25-100 Bar, Above 100 Bar), Pump Capacity (Up To 50, 51-150, 151-500, Above 500), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commands 38.4% share of the rotary pumps market in 2024, led by China's sale of more than 13.5 million pump units yearly. Beijing's subsidies for energy-efficient gear drives and urban water projects underpin demand. India's USD 142 billion petrochemical plan lifts domestic pump manufacturing and draws global OEM licensing deals. Japan supplies precision metering pumps for semiconductor rinse lines, while South Korea's shipyards adopt API-676 twin-screw units for VLCC engine rooms.

The Middle East posts the fastest 7.81% CAGR as Kuwait and Abu Dhabi upgrade separation trains and Saudi Aramco cuts energy via pump rerates. Brownfield work favours screw pumps that handle sand-laden emulsions without cavitation. QatarGas invests in low-flow internal-gear pumps for LNG boil-off, tackling methane regulations. National champions create local-content thresholds that drive new assembly hubs in Dammam and Muscat.

North America is a mature but technologically advanced market. FSMA rules raise gear-pump sales in dairy and brewing, while shale producers fit magnetically coupled pumps to curb VOCs. Sulzer invested CHF 10 million in Easley, South Carolina, adding submersible lines to meet Build America mandates. Canada's oil-sands operators swap diluent pumps for twin-screw models that handle 30% gas volume fraction at sub-zero temperatures.

Europe emphasizes emissions. Revised TA-Luft pushes refineries toward dry-gas seals, and the region's craft breweries adopt hygienic rotary lobe pumps. Norway's electrified offshore fields specify seal-less water-injection pumps to limit methane. EU grants under Horizon programs support digital-twin research for chemical pumps.

South America benefits from Brazil's USD 8 billion FPSO spree. Local content at 25% on P-85 lifts demand for Brazilian-machined casings. Argentina's Vaca Muerta shale develops gas-processing plants that need high-pressure screw pumps. Colombia's biodiesel expansion installs stainless steel gear pumps for palm oil feedstock.

Sub-Saharan Africa grows from a small base but faces maintenance skill gaps that limit adoption of advanced screw pumps. Nigerian modular refineries choose low-cost external-gear units, while South Africa's mining pumps retrofit IIoT sensors to combat theft.