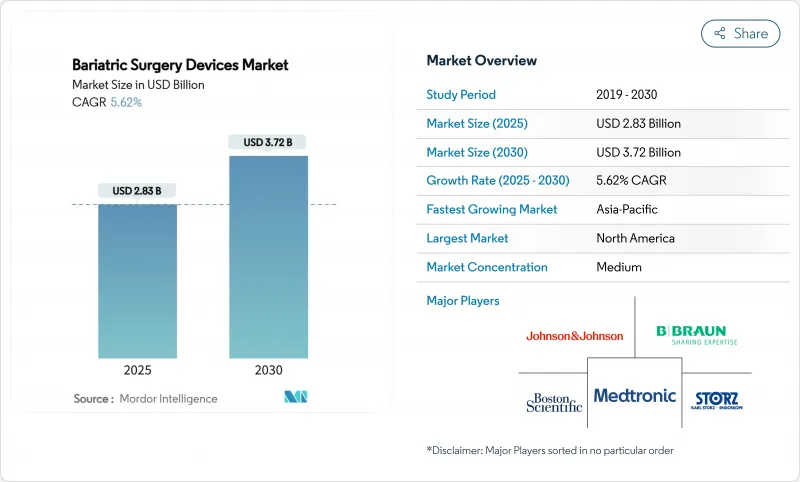

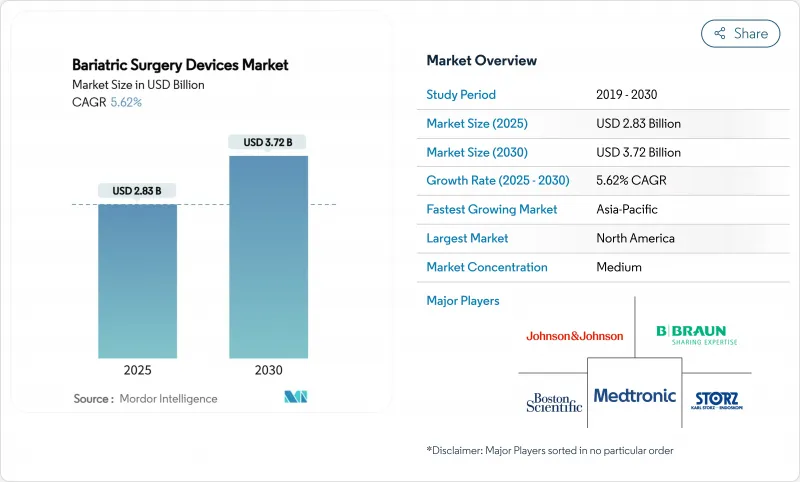

세계의 비만 수술 기기 시장 규모는 2025년 28억 3,000만 달러로, 2030년까지 37억 2,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 5.62%로 예상됩니다.

기기 기반 솔루션이 GLP-1 수용체 작용제와 통합되어 장기적인 체중 관리 결과를 개선하는 유연한 하이브리드 요법을 제공업체에게 제공함으로써 지속적인 성장이 이루어집니다. 로봇 스테이플링, 자기 압박 시스템, 삼키는 풍선 등의 급속한 진보는 수술의 정확성을 높이고, 회복 시간을 단축하고, 합병증 발생률을 낮추고, 지불자와 환자 모두에게 비만 수술 기기 시장의 가치 제안을 강화하고 있습니다. 동시에 경쟁이 심한 분야에서는 토탈 코스트 오브 케어의 절약에 점점 보상되는 상환 기준의 진화에 적응하고 있으며, 그 결과 병원 및 외래수술센터(ASC) 전체에서 기술 도입이 가속되고 있습니다. 북미는 수술 건수로 주도권을 유지하고 있지만, 아시아태평양 수요 곡선은 비만이 젊은층에서 급증함에 따라 가파르게 되어 특수 장비에 대한 미래 수요의 크기를 뒷받침하고 있습니다. 이러한 요인을 종합하면 비만 수술 기기 시장은 2030년까지 한 자리대 중반의 꾸준한 확대가 계속될 것으로 예상되는 탄력적인 시장입니다.

현재 9억 명 이상의 성인이 비만을 가지고 생활하고 있으며, 이 집단은 모든 주요 지역에서 계속 증가하고 있으며 대사 치료에 대응할 수 있는 환자층을 직접 확대하고 있습니다. 체격 지수가 50kg/m2를 초과하는 환자 수요는 특히 강하며, 이러한 환자는 종종 고가로 거래되는 보다 견고한 스테이플 유치술 및 문합술을 필요로 합니다. 아시아태평양 국가에서는 심각한 비만이 가장 급증하고 있으며 보건부는 하류 심혈관 비용을 억제하기 위해 개입 임계치를 낮추고 있습니다. 젊은 환자는 현재 수술 후보자 중 불균형 비율을 차지하고 있으며 공급업체는 더 긴 기능 수명을 가진 장비 개발에 박차를 가하고 있습니다. 이러한 인구 역학의 변화는 비만 수술 기기 시장의 장기적인 확대 기조를 강화하고 있습니다.

지불 측의 정책 개혁은 역사적인 지불 장벽을 해체하고 있습니다. 2026년 메디케어는 비만을 수술과 항비만제를 포함한 종합적 치료가 필요한 만성 질환으로 인증합니다. Blue Cross Blue Shield와 같은 선도적인 민간 보험 회사는 이미 사전 승인 장애물을 제거하고 승인에 소요되는 평균 시간을 14일 단축했습니다. 루이지애나 주 상원 법안 106에 따라 2024년에는 100만 명의 주민이 민간 보험 적용을 받았으며 지역 수술 건수는 즉시 증가했습니다. 지속적인 상환의 추풍은 2030년까지 이 분야의 CAGR을 1.2포인트 밀어 올려 비만 수술 기기 시장을 평생 약물 요법을 대체하는 비용 효율적인 옵션으로 확고히할 것으로 예측됩니다.

세마글루티드와 틸제파티드의 주 1회 제제와 격주 1회 제제는 빠르게 널리 보급되어 처방수 증가 피크 시점에 미국 비만 치료제의 처방수는 25.6% 감소했습니다. 그럼에도 불구하고 외과 수술과 약물 요법을 결합한 요법은 과도한 체중 감소율을 높이고 합병증의 재발을 감소시키는 것이 종단 데이터에서 제안되었습니다. 따라서 시장 진출기업은 기구를 기초적인 개입으로 자리매김하고 약물 치료를 보조요법으로 하는 경향이 강해지고 있습니다. 이 연계는 역풍을 완화하고 CAGR의 마이너스 영향을 1% 포인트 이하로 완화하고 있습니다.

2024년 비만 수술 기기 시장 점유율에서 보조 장비는 59.63%를 차지했으며 스테이플 라인 보강재, 전동 스테이플러 및 첨단 에너지 시스템이 이를 지원합니다. 제품 진화의 중심은 누설 완화이며, 3열 카트리지 형상과 실시간 임피던스 모니터링으로 수술 후 합병증 발생률이 꾸준히 떨어지고 있습니다. 로봇 스테이플링 모듈은 현재 높은 BMI 환자에서 흔히 볼 수 있는 두꺼운 위벽에 해당하는 적응형 클램프 힘 기능을 통합하여 임상적 신뢰성을 더욱 향상시키고 있습니다. 예측 기간 동안 보조 장비는 CAGR 5.78%로 확대될 것으로 예상되지만, 이는 OR 표준화와 반복 구매를 촉구하는 지속적인 업그레이드를 반영합니다.

이식형 기구는 매출 베이스에서는 작지만, 봉합사나 스테이플을 사용하지 않고 문합부를 형성하는 자석 대응의 압박 링 등, 가치가 높은 혁신적인 레이어가 추가되고 있습니다. 경구강으로 유치할 수 있는 스마트 풍선은 수술을 원하지 않는 환자나 수술에 적합하지 않은 환자에 대한 개입의 문턱을 낮추고 있습니다. 이 하위 부문의 새로운 역할에는 전략적 가치가 있습니다. 즉, 장치를 이용한 체중 감량 치료에 새로운 고객층을 도입하고 보다 침습적인 치료에 대한 미래의 파이프라인을 구축함으로써 시장 세분화의 접근 가능한 총 파이를 확대할 수 있습니다.

위소매 절제술은 2024년 비만 수술 기기 시장 규모의 43.49%를 차지하고 중등도에서 중증 비만에 대한 슬리브를 권장하는 임상 지침에 뒷받침됩니다. 제조업체 각사는 수술 시간을 최대 18% 단축하기 위해 첨단이 구부러진 스테이플러나 미리 장전된 버트리스 소재의 개량을 계속하고 있습니다. 그러나 내시경적 위소매 절제술(ESG)은 그 차이를 줄이고 있으며, 12개월 후 총 체중 감소율 13.6%를 최소한의 유해 사건으로 나타낸 임상 증거로 6.45%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 병원은 ESG를 복잡한 재치환 수술을 위해 수술실의 용량을 해제하는 당일 수술의 대체 수단으로 자리매김하고 있으며, 간접적으로 고급 봉합 플랫폼과 내시경용 액세서리의 매출을 자극하고 있습니다.

비용 효과적인 데이터에서 ESG는 세마글루티드에 비해 5년간 3만 3,583달러의 절약이 되어 자비 진료를 하는 고용주에게 매력적인 약이 되고 있습니다. 장비 제조업체는 내시경 봉합 도구에 AI 가이드가 있는 내비게이션을 번들하여 봉합 위치의 정확도를 높이는 것으로 대응합니다. 반면 로봇 지원을 통한 Roux-en-Y는 초비만 환자나 심한 역류가 있는 환자와 여전히 관련되어 있으며 30mm 리로드 스테이플러 및 싱글 사이트 트래커 키트에 대한 수요를 지원합니다. 다양한 기술 포트폴리오가 비만 수술 기기 시장의 대응 가능 영역을 확대합니다.

북미는 2024년 세계 매출의 42.10%를 차지했고 폭넓은 보험 적용 범위와 설치된 외과의사 네트워크에 의해 견인되었습니다. GLP-1 도입에 의해 2024년 증례 수는 감소했지만, 수술 건수는 탈락에 의한 전환을 거쳐 회복해, 2030년까지의 CAGR은 5.15%로 견조한 전망입니다. 캐나다는 미국의 역학을 반영하지만, 주 보조금 상한은 정기적인 대기 환자 수의 변동을 초래하고 분기별 장비 선적을 형성하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 7.02%로 예측되어 가장 빠르게 성장하는 지역입니다. 이는 아시아태평양의 비만 부담 급증과 중간층의 가처분 소득 확대를 반영합니다. 중국과 인도는 2024년에 맞추어 18만 건 이상의 수술을 진행하지만 보급률은 여전히 대상자의 2% 미만이며 미개척의 여지가 큽니다. 의료 관광의 중심지인 태국과 한국에서는 구미 시장보다 30-50% 싼 비용으로 수술을 받을 수 있지만, 국제적인 환자의 흐름은 인정 상태에 대한 감도를 높이고 있어, 프로바이더는 신뢰 보증을 위해 세계 브랜드의 기기를 채용하게 되어 있습니다.

유럽은 증거 기반의 의료기기 도입을 지지하는 전국민 보험제도에 힘입어 5.46%의 완만한 확대를 유지하고 있습니다. 2025년에 발표된 새로운 의료 관광 안전 기준은 해외 비만 치료 센터에 장비 추적성과 외과의 자격 증명서를 문서화하도록 요구하고 있습니다. 남미와 중동 및 아프리카는 합쳐도 현재 매출의 10% 미만에 불과하지만, 민간병원에 대한 투자와 질 높은 의료를 요구하는 외국인구 증가에 따라 활기차고 CAGR 약 6%로 성장합니다. 이러한 신흥 시장이 성숙함에 따라 현지에 뿌리를 둔 교육 이니셔티브와 유통을 일치시키는 공급업체는 추가 점유율을 얻을 수 있습니다.

The bariatric surgery devices market size stood at USD 2.83 billion in 2025 and is forecast to reach USD 3.72 billion in 2030, advancing at a 5.62% CAGR over the period.

Sustained growth unfolds as device-based solutions integrate with GLP-1 receptor agonists, giving providers flexible, hybrid regimens that improve long-term weight-management outcomes. Rapid advances in robotic stapling, magnetic compression systems and swallowable balloons are sharpening surgical precision, shortening recovery times and lowering complication rates, reinforcing the value proposition of the bariatric surgery devices market for both payers and patients. At the same time, the competitive field is adapting to evolving reimbursement criteria that increasingly reward total-cost-of-care savings, thereby accelerating technology adoption across hospitals and ambulatory surgical centers. North America retains leadership on procedure volumes, yet the Asia-Pacific demand curve steepens as obesity prevalence rises sharply among younger cohorts, underlining sizable future demand for specialized devices. Collectively, these factors create a resilient bariatric surgery devices market that is expected to track steady mid-single-digit expansion through 2030.

More than 900 million adults currently live with obesity, a cohort that continues to grow in every major region and directly enlarges the addressable pool for metabolic procedures. Demand is especially strong among patients with body-mass indices >= 50 kg/m2, who often need more robust stapling and anastomosis solutions that command premium prices. Asia-Pacific countries are witnessing the steepest uptick in severe obesity, prompting health ministries to lower intervention thresholds to curtail downstream cardiovascular costs. Younger patients now represent a disproportionate share of surgical candidates, spurring suppliers to engineer devices with longer functional lifespans. Together, these demographic shifts reinforce the long-range expansion arc of the bariatric surgery devices market.

Payer policy reforms are dismantling historical payment barriers. In 2026, Medicare will recognize obesity as a chronic disease that warrants comprehensive treatment, including surgery and anti-obesity medication. Major private insurers such as Blue Cross Blue Shield have already removed prior-authorization hurdles, cutting average approval time by fourteen days. Louisiana's Senate Bill 106 brought an additional 1 million residents under mandatory commercial coverage in 2024, immediately boosting regional procedure volumes. Sustained reimbursement tailwinds are forecast to add 1.2 percentage points to the sector's CAGR through 2030, cementing the bariatric surgery devices market as a cost-effective alternative to lifelong pharmacotherapy.

Weekly and bi-weekly formulations of semaglutide and tirzepatide have achieved rapid uptake, leading to a 25.6% dip in U.S. bariatric volume during peaks in prescription growth. Nonetheless, longitudinal data suggest that combined surgical-pharmacologic regimens boost excess-weight-loss rates and lower comorbidity relapse. Accordingly, market participants increasingly position devices as foundational interventions, with medication acting as adjunct therapy. This linkage tempers the headwind, moderating the negative CAGR impact to below one percentage point.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Assisting devices retained a dominant 59.63% of the bariatric surgery devices market share in 2024, supported by staple-line reinforcement materials, powered staplers, and advanced energy systems. Product evolution centers on leak mitigation, with triple-row cartridge geometry and real-time impedance monitoring steadily reducing postoperative complication rates. Robotic stapling modules now integrate adaptive clamp force features that accommodate thicker gastric walls common in high-BMI patients, further boosting clinical confidence. Over the forecast horizon, assisting devices are projected to expand at a 5.78% CAGR, reflecting continuous incremental upgrades that encourage OR standardization and repeat purchases.

Implantable devices, though smaller in revenue terms, are adding high-value innovation layers such as magnet-enabled compression rings that create anastomoses without sutures or staples. Smart balloons capable of trans-oral placement are lowering thresholds for intervention among patients unwilling or unfit for surgery. This sub-segment's emerging role has strategic value: it introduces new customer groups to device-based weight-loss therapies and builds a future pipeline for more invasive treatments, thereby expanding the total accessible pie of the bariatric surgery devices market.

Sleeve gastrectomy held 43.49% of the bariatric surgery devices market size in 2024, anchored by clinical guidelines that endorse the sleeve for moderate-to-severe obesity. Manufacturers continue to refine curved tip staplers and pre-loaded buttress materials to shorten operative time by up to 18%. However, endoscopic sleeve gastroplasty (ESG) is closing the gap, posting a 6.45% CAGR on the strength of clinical evidence showing 13.6% total body-weight loss at 12 months with minimal adverse events. Hospitals increasingly position ESG as a day-case alternative that frees OR capacity for complex revisional work, indirectly stimulating sales of advanced suturing platforms and endoscopic accessories.

Cost-utility data place ESG at a five-year savings of USD 33,583 versus semaglutide, elevating its attractiveness for self-insured employers. Device makers are responding by bundling endoscopic suturing tools with AI-guided navigation to enhance stitch placement accuracy. Meanwhile, robotic-assisted Roux-en-Y remains relevant for super-obese patients and for those with severe reflux, sustaining demand for 30-mm reload staplers and single-site trocar kits. The procedural mosaic underscores the central thesis: a diversified technique portfolio enlarges the addressable field for the bariatric surgery devices market.

The Bariatric Surgery Devices Market Report is Segmented by Device Type (Implantable Devices and More), Procedure Type (Sleeve Gastrectomy and More), Surgery Type (Minimally Invasive, Non-Invasive), End-User (Hospitals, Bariatric Surgery Clinics, Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 42.10% of 2024 global revenue, propelled by broad insurance coverage and well-established surgeon networks. Although GLP-1 uptake trimmed case numbers during 2024, procedure volumes rebounded after dropout-driven conversions, producing a steady 5.15% CAGR outlook to 2030. Canada mirrors U.S. dynamics, but provincial funding caps introduce periodic wait-list fluctuations that shape quarterly device shipments.

Asia-Pacific is the fastest riser with a predicted 7.02% CAGR through 2030, reflecting the region's rapidly escalating obesity burden and expanding middle-class disposable income. China and India together accounted for more than 180,000 procedures in 2024, yet penetration remains below 2% of eligible candidates, revealing enormous untapped headroom. Medical-tourism hubs in Thailand and South Korea offer procedures at 30-50% lower cost than Western markets, but international patient flow is increasingly sensitive to accreditation status, pushing providers to adopt globally branded devices for trust assurance.

Europe sustains a moderate 5.46% expansion, underpinned by universal health systems that favor evidence-based device adoption. New medical-tourism safety standards released in 2025 compel overseas bariatric centers to document device traceability and surgeon credentials. South America and the Middle East & Africa together represent less than 10% of current revenue, yet advance at roughly 6% CAGR, energized by private-hospital investments and growing expatriate populations seeking quality care. Suppliers that align distribution with localized training initiatives stand to win incremental share as these nascent markets mature.