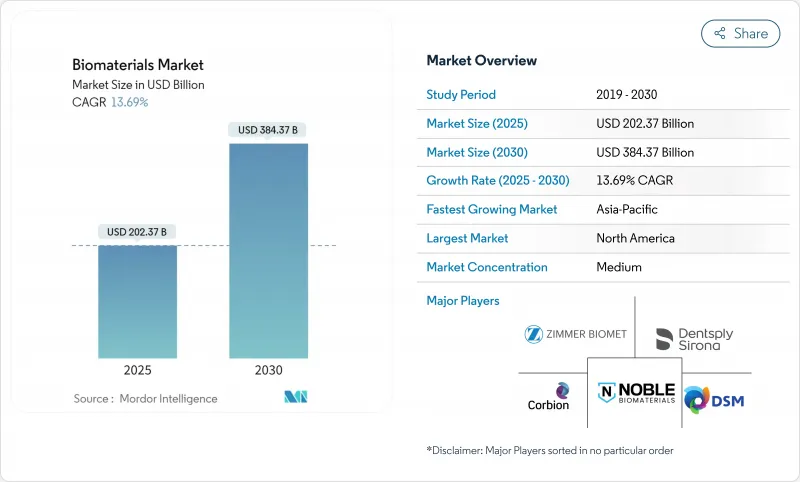

세계의 바이오소재 시장 규모는 2025년 2,023억 7,000만 달러, 2030년까지 3,843억 7,000만 달러에 이를 것으로 예측되며, 기간 동안 13.69%의 연평균 복합 성장률(CAGR)로 확대될 것으로 보입니다.

고령화에 따른 시술량 증가, 재생의료의 비약적 진보, 규제의 합리화 등이 성장의 원동력이 되고 있습니다. 고분자 재료는 심장혈관용 스텐트와 정형외과용 인서트에서의 적응성 덕분에 수요가 호조를 유지하는 반면, 폐기물 유래의 천연 재료는 순환 경제의 의무화가 강화됨에 따라 급속히 확대됩니다. 북미는 FDA의 획기적 의료기기 지정 1,041건이 상업화의 리스크를 경감하고 있지만, 중국의 인공 슬관절 치환술의 5배 증가와 일본의 인공 다능성 줄기세포(iPSC) 혁신에 지지된 2자리 성장으로 아시아태평양이 웃돌고 있습니다. Enovis가 8억 유로를 투자한 LimaCorporate 인수와 같은 전략적 인수는 원자재 부족과 EU MDR 준수 병목 현상을 완화하기 위한 수직 통합의 움직임을 뒷받침합니다.

미국에서만 인공 슬관절 치환술의 건수는 2030년까지 673% 증가할 것으로 예측되고 있으며, 독일에서는 2040년까지 인공 슬관절 치환술의 건수가 55% 증가할 것으로 예측되고 있습니다. 현재, 젊고 활동적인 환자가 대부분의 후보자를 차지하고 있으며, 임플란트 개발자는 내마모성과 골유착능 수명을 우선 할 필요가 있습니다. 콜롬비아에서는 2050년까지 3만 9,270건의 다리 인공관절 치환술이 이루어질 것으로 보이고, 그 중 52.7%가 여성으로 예측되고 있으며, 성별에 특화된 바이오소재의 조합에 박차가 가해집니다. 지속적인 수술 파이프라인은 전통적인 건강 관리 지출 사이클에 대한 바이오소재 시장을 완화하고 있습니다.

캐나다 정부의 Aspect Biosystems에 대한 7,275만 캐나다 달러의 보조금은 바이오프린트 조직에 대한 정책적 신뢰를 나타내는 것으로, 머신러닝 주도의 모델링은 4D 스캐폴드의 형상 예측으로 R2>0.999를 달성했습니다. 최초의 무세포 조직 인공 혈관인 Symvess의 FDA 인가는 선례를 확립하고 임상 응용을 가속시킵니다. 규제의 투명성이 향상됨에 따라 벤처기업의 활동은 아시아태평양으로 퍼져 일본의 iPSC를 이용한 각막상피이식이 지역 경쟁력을 두드러지게 합니다.

인플레이션과 공급망 충격은 2024년 제조 위탁비를 늘렸고, 폴리테트라플루오로에틸렌의 부족은 인소싱과 재고비축을 강요시켜 소형 기기 제조업체의 현금흐름을 악화시켰습니다. 탄탈룸 가격은 2023년 1kg당 5,190달러까지 상승해 특수 임플란트 제조업체의 마진을 계약했습니다. EU MDR에 대응하는 데는 18-24개월과 다액의 인증 비용이 들기 때문에 조사 대상이 된 유럽 기업의 50%가 포트폴리오의 축소를 강요받고 있습니다.

고분자 재료는 2024년 바이오소재 시장에서 40.15%의 점유율을 유지하며 심장혈관 및 정형외과용을 지배하고 있습니다. 생선 유래 콜라겐과 곤충 유래 키토산이 천연 소재의 보급을 가속시켜 CAGR14.67%를 견인해 폴리머의 우위성에 과제합니다. 복합재료의 하이브리드는 금속 강도와 고분자 탄성을 융합시켜 청소년 인공 관절 치환술 환자의 하중지지 선호도를 충족시킵니다. 4D 프린팅에 의해 제조되는 형상 기억 폴리머는 생체 내에서 적합한 비계를 가능하게 하고, 보험 상환 프리미엄을 요구하는 조직 공학 기업에 있어서 차별화 요인이 됩니다.

또한 천연 소재 후보는 EU의 순환형 경제 우대 조치의 혜택을 받아 정어리 비늘에서 콜라겐 추출과 갑각류 폐기물의 업 사이클을 가속화하고 있습니다. 금속 바이오소재은 탄탈과 니오븀 공급 위험에 취약하지만 높은 피로 저항이 요구되는 인공 고관절에는 필수적입니다. 바이오소재 시장은 재활용 및 이중 조달 전략을 통해 원재료 변동을 헤지할 수 있는 공급업체에게 계속 보상되고 있습니다.

북미는 2024년에 바이오소재 시장 점유율의 42.23%를 차지했으며, 1,041건의 FDA(미국 식품의약품국)에 의한 획기적 신약의 지정과 기업의 연구개발에 지지되고 있습니다. 확립된 상환 제도와 견고한 외과의사 교육 프로그램이 프리미엄 임플란트의 급속한 보급을 뒷받침하고 있습니다.

유럽은 MDR의 병목에 시달리고 있으며, 2023년에는 1만 4,539건의 신청에서 4,873건 밖에 증명서가 발행되지 않았습니다. 그럼에도 불구하고 독일에서는 2040년까지 인공 슬관절 치환술의 이환율이 55% 상승할 것으로 예상되고 있으며, 컴플라이언스 장애물이 완화되면 수요는 보장됩니다. EU의 순환형 바이오 경제 보조금은 곤충 유래 키토산 플랜트도 급격히 진행하고 있어 천연 소재에 선행자 이익을 가져오고 있습니다.

아시아태평양은 CAGR이 가장 빠른 15.19%로 성장을 지속하고, 있으며, 이는 중국의 인공 슬관절 치환술이 5배로 뛰어올랐고 일본이 인간 최초의 iPS 세포 각막 이식을 실시한 것에 뒷받침되고 있습니다. 벤처기업의 자금조달액이 2021년 최고치에서 22% 감소하고 있지만, 이 지역의 의료기술 부문은 2030년 매출 2,250억 달러를 목표로 하고 있으며 세계 OEM에 제조 현지화를 촉구하고 있습니다. 한국과 호주는 선진적인 복합재 인쇄허브를 통해 생산능력을 증강하고 인도의 중산계급 증가는 비용효율이 우수한 임플란트의 대량 수요를 증대시킵니다.

The biomaterials market size stands at USD 202.37 billion in 2025 and is forecast to reach USD 384.37 billion by 2030, advancing at a 13.69% CAGR throughout the period.

Growth gathers momentum from aging-driven procedure volumes, rapid regenerative medicine breakthroughs, and streamlined regulatory pathways. Polymeric materials keep demand buoyant thanks to their adaptability in cardiovascular stents and orthopedic inserts, while waste-derived natural materials expand quickly as circular-economy mandates intensify. North America benefits from 1,041 FDA breakthrough device designations that de-risk commercialization, yet Asia-Pacific outpaces with double-digit growth backed by China's fivefold rise in knee replacements and Japan's induced-pluripotent-stem-cell (iPSC) innovations. Strategic acquisitions-such as Enovis' EUR 800 million purchase of LimaCorporate-underscore vertical-integration moves aimed at buffering raw-material shortages and EU MDR compliance bottlenecks.

Primary knee arthroplasty volumes in the United States alone are projected to climb 673% by 2030, and Germany anticipates a 55% rise in knee arthroplasties by 2040. Younger and more active patients now represent a majority of candidates, forcing implant developers to prioritize wear resistance and osseointegration longevity. Colombia projects 39,270 lower-limb arthroplasties by 2050, 52.7% of which will involve women, spurring gender-specific biomaterial formulations. The sustained procedure pipeline cushions the biomaterials market against traditional healthcare spending cycles.

The Canadian government's CAD 72.75 million grant to Aspect Biosystems signals policy confidence in bioprinted tissues, while machine-learning-driven modelling achieves R2 > 0.999 for shape predictions in 4D scaffolds. FDA clearance of Symvess, the first acellular tissue-engineered vessel, establishes precedent and accelerates clinical translation. As regulatory clarity improves, venture activity spreads to Asia-Pacific, where Japan's iPSC-based corneal epithelial transplants underscore regional competitiveness.

Inflation and supply chain shocks inflated contract manufacturing costs during 2024, while polytetrafluoroethylene shortages forced insourcing and inventory stockpiling, impairing cash flow for small device makers. Tantalum prices climbed to USD 5,190 per kg in 2023, tightening margins for specialty implant suppliers. EU MDR compliance adds 18-24 months and significant certification costs, prompting 50% of surveyed European firms to trim portfolios.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Polymeric materials retained a 40.15% share of the biomaterials market in 2024, dominating cardiovascular and orthopedic uses. Fish-waste collagen and insect-derived chitosan speed natural-material uptake, driving a 14.67% CAGR that challenges polymeric supremacy. Composite hybrids marry metallic strength with polymeric elasticity, meeting load-bearing preferences in younger arthroplasty patients. Shape-memory polymers produced via 4D printing enable scaffolds that conform in vivo, a differentiator for tissue-engineering firms seeking reimbursement premiums.

Natural candidates also benefit from EU circular-economy incentives, accelerating collagen extraction from sardine scales and upcycling crustacean waste. Metallic biomaterials, though vulnerable to tantalum-and-niobium supply risks, remain indispensable in hip prostheses demanding high fatigue resistance. The biomaterials market continues to reward suppliers able to hedge raw-material volatility through recycling and dual-sourcing strategies.

The Biomaterials Market Report is Segmented by Material Type (Metals, Polymeric, Ceramic, Composite, Natural), Origin (Synthetic, Natural), Application (Orthopedic, Cardiovascular, Dental, Wound Healing, Neurology, Plastic Surgery, Tissue Engineering & Regeneration, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America held 42.23% of biomaterials market share in 2024, buoyed by 1,041 FDA breakthrough designations and heavy corporate R&D. Established reimbursement and robust surgeon training programs encourage rapid adoption of premium implants signals federal backing for bioprinting ventures.

Europe grapples with MDR bottlenecks-only 4,873 certificates were issued from 14,539 applications in 2023-delaying launches and prompting some manufacturers to withdraw legacy devices. Despite this, Germany expects knee-replacement incidence to climb 55% by 2040, guaranteeing demand once compliance hurdles ease. EU circular-bioeconomy grants also fast-track insect-derived chitosan plants, giving natural materials an early-mover edge.

Asia-Pacific charts the fastest 15.19% CAGR, propelled by China's fivefold jump in knee replacements and Japan's first-in-human iPSC corneal transplants. Even with venture funding down 22% from 2021 highs, the region's medtech sector still targets USD 225 billion in 2030 revenue, encouraging global OEMs to localize manufacturing. South Korea and Australia add capacity through advanced composite printing hubs, while India's growing middle class amplifies volume demand for cost-efficient implants.