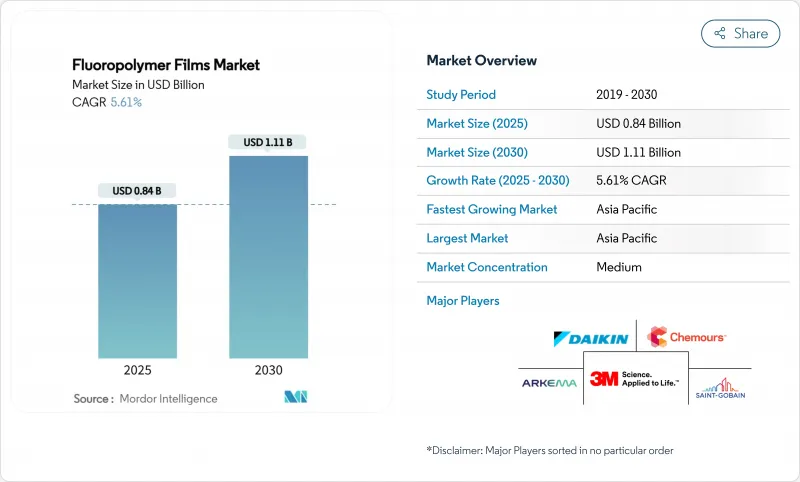

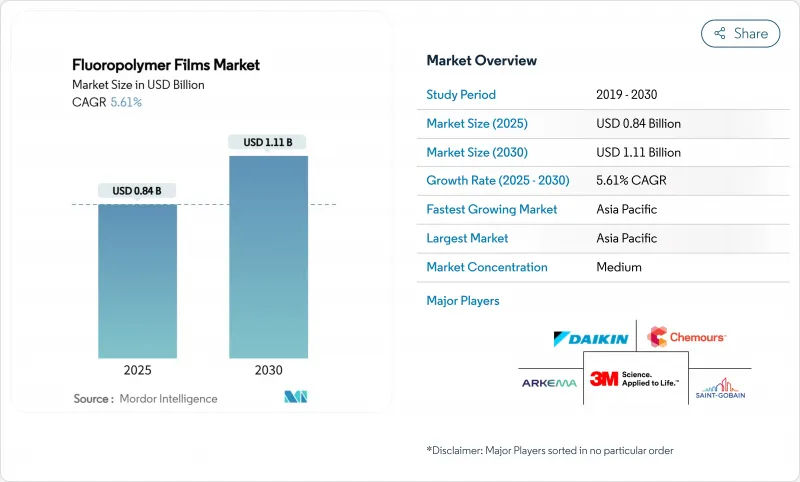

세계의 불소수지 필름 시장 규모는 2025년 8억 4,000만 달러로 추정되며 예측 기간 중(2025-2030년) CAGR은 5.61%로 확대되어 2030년까지 11억 1,000만 달러에 이를 것으로 예측됩니다.

이러한 성장 전망은 특히 화학적 불활성, 저표면 에너지, 폭넓은 온도 안정성 등과 같은 놀라운 성능 특성이 과플루오로알킬 물질(PFAS) 및 폴리플루오로알킬 물질(PFAS)에 대한 규제 압력 증가를 계속해서 이기고 있음을 뒷받침합니다. 태양광 발전(PV)의 급속한 보급, 전기자동차(EV)의 경량화, 반도체 오염 방지는 여전히 가장 영향력 있는 3개 수요 엔진입니다. 기존 업체들은 양만을 추구하는 것이 아니라 미션 크리티컬한 용도를 위한 제품 포트폴리오를 확충하고 있으며, 다운스트림 고객은 내구성과 안전성 보증에 대한 지불 의향을 높이고 있습니다. 아시아태평양은 구조적 비용 우위와 최종 용도에 가깝게 유지하고 있으며, 북미 구매자들은 고순도와 추적성을 선호하며, 유럽 정책 입안자들은 PFAS 준수 화학물질의 혁신을 추진하고 있습니다. 이러한 힘을 종합하면, 불소수지 필름 시장은 향후 5년간 지수적이지 않고 꾸준히 확대될 것으로 예측됩니다.

플렉서블 태양광 발전 설비에서는 투명하고 내후성이 우수한 불소 수지 라미네이트가 무거운 유리를 대체합니다. 수증기 투과율이 낮은 페로브스카이트형 모듈은 2,000시간의 내습열 테스트 후에도 84%의 효율을 유지해 모듈의 보증 기간을 25년으로 연장하고 있습니다. 아시아태평양의 소비 점유율은 태양광 발전 어셈블리의 이점을 반영하며, 미국에서는 커뮤니티 태양광 정책이 수요의 첨단을 강화하고 있습니다. 그 결과, 배리어 필름은 여전히 불소수지 필름 시장에서 가장 큰 용도가 되고 있습니다.

생물학적 제제와 개인화 치료에는 엄격한 수분과 화학 물질의 장벽이 필요합니다. Chemours는 PTFE와 PVDF 등급은 추출물이 적고 생체적합성이 높기 때문에 프리필드 주사기나 마이크로카테터에 필수적인 것으로 확인하고 있습니다. 용기의 밀폐성에 관한 미국 FDA의 지침을 통해 의약품 제조업체는 섬세한 활성 물질을 보호하기 위해 고순도의 불소수지 라이너를 지정했습니다. EU의 부록 1 개정 동향과 일치하여 의료용 필름에 대한 수요가 높아집니다.

미국 환경보호청(EPA)은 심사 없이 329유형의 PFAS의 제조를 금지하고 PFOA와 PFOS를 유해물질로 지정했습니다. 미네소타와 캘리포니아는 2025년 1월부터 일부 소비자 제품에 PFAS를 사용하는 것을 금지하고 EU의 REACH 제안은 임계 농도를 초과하는 10,000개 이상의 물질을 규제하려고 합니다. 컴플라이언스 비용과 잠재적인 대체 리스크는 불소수지 필름 시장 예측 CAGR을 총 1.4% 감소시킵니다.

폴리테트라플루오로에틸렌(PTFE)의 점유율은 46.55%였습니다. 높은 용융 점도와 비교할 수없는 화학적 불활성으로 반도체 제조 챔버, 개스킷 시트 및 고주파 케이블에 사용됩니다. 대만과 미국에서 계속되는 공장 확장은 수요의 탄력성을 지원합니다. 또한 PTFE는 마찰계수가 낮기 때문에 규제의 재검토가 다가오고 있음에도 불구하고 수술용 기구의 라이너에도 사용되고 있습니다.

불소화 에틸렌 프로파일렌(FEP)의 CAGR은 6.09%로 2030년까지 가장 급성장할 것으로 보이는 폴리머 계열입니다. 보다 낮은 용융 온도는 용융 압출 튜브, 컬러 매칭 가능한 시트 및 가전 인클로저용 3D 인쇄 필라멘트 증가를 가능하게 합니다. Archema가 출시한 FluorX 필라멘트는 추가 제조에서 PTFE의 사용을 제한하는 가공상의 제약에 FEP가 어떻게 대처하는지를 보여줍니다. 사용자는 광학 투명성과 200°C의 연속 사용 온도를 평가하여 유연한 인쇄 회로의 채택을 확대하고 있습니다.

불소수지 필름 보고서는 유형별(폴리테트라플루오로에틸렌(PTFE), 폴리불화비닐리덴(PVDF), 기타), 용도별(배리어 필름, 릴리스 필름, 미다공 필름, 보안 필름), 최종 사용자 산업별(자동차, 항공우주, 방위, 건설, 포장, 공업, 전자 및 반도체, 기타), 지역별(아시아태평양, 북미, 유럽, 남아메리카, 중동 및 아프리카)로 구분됩니다.

아시아태평양은 2024년 세계 매출의 48.62%를 창출했으며, 불소수지 필름 시장 규모는 지역 최고 CAGR 6.20%로 확대됩니다. 중국의 통합형 PV 서플라이 체인에서는 PVF 백시트와 ETFE 프론트 시트가 대량으로 소비되는 한편, 정부의 장려책에 의해 옥상 태양광 발전의 개수가 가속하고 있습니다. 인도의 전자기기 제조 방식은 고순도 PTFE 테이프의 국내 조달을 촉진하고 기준선 수요를 높입니다. 일본 자동차 플랫폼은 800V 아키텍처로 전환하여 열 관리 향상을 위해 PEEK와 PTFE 유전체 필름을 선호합니다.

북미는 왕성한 반도체 설비 투자와 의료기기 혁신의 혜택을 받습니다. 미국 CHIPS 법에 따른 칩 제조 공장은 클린 룸 기준을 업그레이드하고 PTFE와 FEP 소모품을 견인하고 있습니다. 미시간에서 조지아까지의 EV 플랫폼에는 바디 인 화이트 패널용 복합 이형 필름이 필요합니다.

유럽은 규제의 엄격함과 기후정책의 균형을 맞춥니다. 독일과 스페인의 그린 수소 전해조 파일럿 시험에서는 불소 수지 PEM을 채용하고 있습니다. 독일과 프랑스의 자동차 OEM은 경량화를 위해 ETFE 루프 스킨을 채택하고 있습니다. 그러나 EU 전반에서 제안된 PFAS 규정은 불확실성을 가져오고 생산자에게 폐쇄 루프 회수와 폐가스 감소에 대한 투자를 촉구하고 있습니다. 이러한 조치로 컴플라이언스 비용이 높아지고 공급이 유지됩니다.

The Fluoropolymer Films Market size is estimated at USD 0.84 billion in 2025, and is expected to reach USD 1.11 billion by 2030, at a CAGR of 5.61% during the forecast period (2025-2030).

This growth outlook underscores how irreplaceable performance attributes, notably chemical inertness, low surface energy, and wide-temperature stability, continue to outweigh mounting regulatory pressures on per- and polyfluoroalkyl substances (PFAS). Rapid photovoltaic (PV) build-out, electric-vehicle (EV) light-weighting, and semiconductor contamination control remain the three most influential demand engines. Incumbent producers are widening product portfolios for mission-critical applications rather than chasing volume alone, while downstream customers signal rising willingness to pay for durability and safety assurances. Asia Pacific retains structural cost advantages and end-use proximity, Northern American buyers prioritize high-purity and traceability, and European policy makers drive innovation in PFAS-compliant chemistries. Together, these forces point to a steady, rather than exponential, expansion path for the fluoropolymer films market over the next five years.

Flexible PV installations rely on transparent and weather-resistant fluoropolymer laminates to displace heavier glass. Lower water-vapor-transmission rates help perovskite modules retain 84% efficiency after 2,000 hours of damp-heat testing, extending module warranties to 25 years. Asia Pacific's consumption share mirrors its photovoltaic assembly dominance, while U.S. community-solar policies reinforce demand peaks. Consequently, barrier films remain the largest application slice of the fluoropolymer films market.

Biologics and personalized therapies require stringent moisture and chemical barriers. Chemours confirms that PTFE and PVDF grades remain essential in pre-filled syringes and micro-catheters because of their low extractables and biocompatibility. U.S. FDA guidance on container-closure integrity pushes drug makers to specify high-purity fluoropolymer liners to protect sensitive actives. Matching trends in EU Annex 1 revisions strengthen demand for medical-grade films.

The U.S. EPA has barred production of 329 PFAS without agency review and designated PFOA and PFOS as hazardous substances. Minnesota and California ban PFAS in select consumer products from January 2025, while an EU REACH proposal seeks to restrict more than 10,000 substances above threshold concentrations. Compliance costs and potential substitution risks collectively shave 1.4 percentage points off the forecast CAGR for the fluoropolymer films market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Polytetrafluoroethylene (PTFE) held a 46.55% share. High melt viscosity yet unmatched chemical inertness anchors its use in semiconductor fabrication chambers, gasket sheets, and high-frequency cables. Continued fab expansions in Taiwan and the United States support demand resilience. The material's low friction coefficient also keeps PTFE relevant in surgical device liners despite looming regulatory review.

Fluorinated Ethylene-Propylene's (FEP) 6.09% CAGR positions it as the fastest-growing polymer family through 2030. Lower melt temperature enables melt-extruded tubing, color-matchable sheets, and increasingly 3-D printed filaments for consumer electronics housings. Arkema's FluorX filament release illustrates how FEP addresses processing constraints that limit PTFE uptake in additive manufacturing. Users value optical clarity combined with 200 °C continuous-use temperature, broadening adoption in flexible printed circuits.

The Fluoropolymer Films Report is Segmented by Type (Polytetrafluoroethylene (PTFE), Polyvinylidene Fluoride (PVDF), and More), Application (Barrier Films, Release Films, Microporous Films, and Security Films), End-User Industry (Automotive/Aerospace/Defense, Construction, Packaging, Industrial, Electronics/Semiconductor, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Asia Pacific generated 48.62% of global sales in 2024, with the fluoropolymer films market size expanding at a region-leading 6.20% CAGR. China's integrated PV supply chain consumes vast volumes of PVF backsheets and ETFE frontsheets, while government incentives accelerate rooftop-solar retrofits. India's electronics manufacturing scheme promotes domestic sourcing of high-purity PTFE tapes, elevating baseline demand. Japan's automotive platforms shift to 800-V architectures, favouring PEEK and PTFE dielectric films for improved thermal management.

North America benefits from strong semiconductor capital expenditure and medical-device innovation. Chip fabs under the U.S. CHIPS Act upgrade clean-room standards, driving PTFE and FEP consumables. EV platforms from Michigan to Georgia require composite release films for body-in-white panels.

Europe balances regulatory stringency with climate-policy pull. Green-hydrogen electrolyser pilots in Germany and Spain incorporate fluoropolymer PEMs. Automotive OEMs in Germany and France integrate ETFE roof skins for weight savings. Yet proposed EU-wide PFAS restrictions inject uncertainty, prompting producers to invest in closed-loop recovery and waste-gas abatement. Such measures sustain supply, albeit at higher compliance cost.