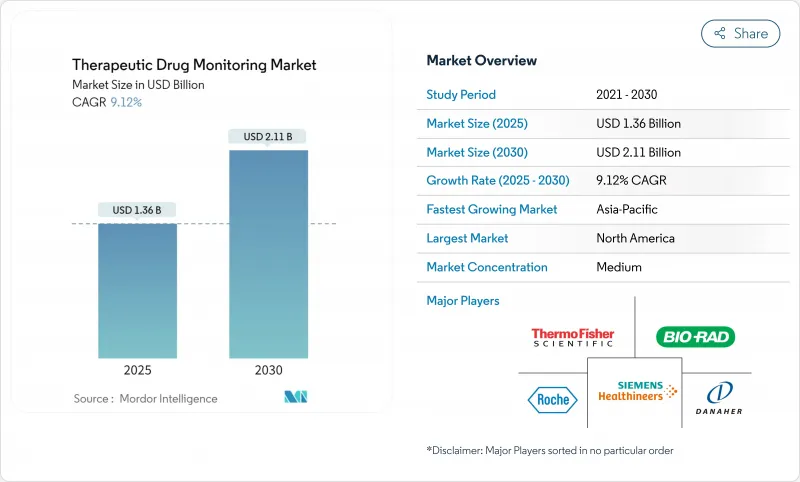

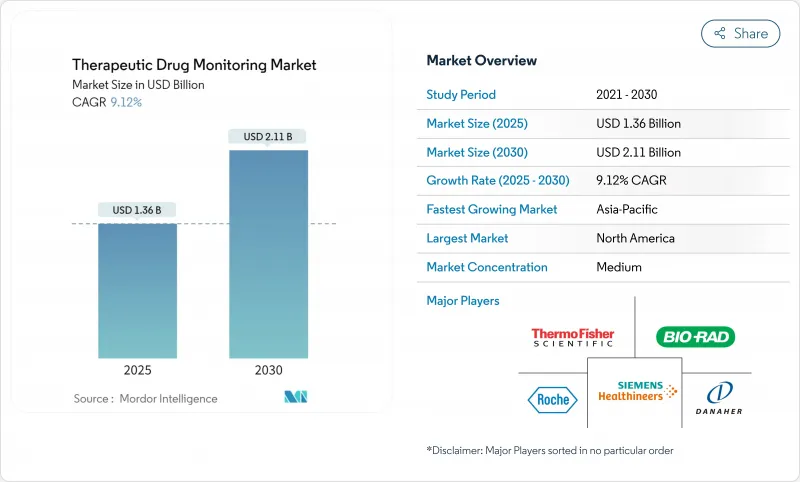

세계의 치료제 모니터링 시장은 2025년 13억 6,000만 달러에 이르고, 2030년까지 21억 1,000만 달러에 이를 것으로 예측되며, CAGR 9.12%로 확대될 것으로 보입니다.

정밀 의학 프로그램 채용 증가, 약리 유전체 결정 툴의 통합, 분산형 임상시험 활동의 확대가 이 확대를 지지하고 있는 한편, 비용 압박을 받고 있는 병원 시스템에서는 루틴 검사량을 유지하기 위해 고처리량 코어 랩 자동화가 점점 지지되고 있습니다. 연속 바이오센서 플랫폼과 건조한 혈액 스폿 샘플링은 3차 의료기관 이외에도 접근을 넓히고, 원격 투여량 적정을 가능하게 하고, 종양학, HIV, 자가면역요법 프로토콜에서 부작용 위험을 감소시킵니다. 미국 식품의약국(FDA)에 의한 임상 실험실 개발 검사의 점진적인 모니터링을 포함한 규제의 무결성은 품질 기준을 높이고 보다 광범위한 검사 패널의 지불자 수락을 가속할 것으로 예측됩니다. 하지만 신흥 시장에서는 자본의 제약으로부터 액체 크로마토그래프 및 탠덤 질량 분석(LC-MS/MS) 분석 장치의 도입이 계속 제한되어 있어 특이성이 높은 검사법의 보급이 억제되고 있습니다.

암 프로토콜에서는 저분자 키나아제 억제제와 단클론항체의 조합이 증가하고 있어 치료 마진이 좁아지고 있습니다. HIV에 대한 장기간 작용하는 카보테그라빌-릴 피비린 병용 요법은 모니터링의 시야를 매일 경구 투여로부터 확대하고, 매월 또는 격월 간격으로 지속적인 농도를 확인해야 합니다. 자가면역질환에서는 현재 항약 항체 형성에 의해 클리어런스 속도가 변화하는 생물학적 질환 개질제가 일상적으로 사용되고 있으며, 치료제 모니터링은 1차적인 비반응과 면역원성의 효능 상실을 구별하기 위한 근거에 따른 경로를 보여줍니다. 고령화와 관련된 심혈관 질환은 디곡신과 항 부정맥제의 수치를 높이고 이소성 독성을 피합니다. 이러한 질병 부담은 치료제 모니터링 시장에 일관된 환자 코호트를 추가하고 예측 가능한 검사량 증가를 지원합니다.

규제당국은 현재 중요한 임상시험에서 다양한 유전자형과 병존질환 프로파일에 있어서 용량 최적화의 근거를 기대하고 있으며, 치료제 모니터링을 시험 프로토콜에 확실히 통합하고 있습니다. 따라서 스폰서는 LC-MS/MS 분석과 파마코유전체학 알고리즘을 통합한 샘플에서 인사이트로의 워크플로우를 도입하여 적응 투여군을 가능하게 하여 후기 단계에서의 이탈을 줄이고 있습니다. 분산형 임상시험 모델은 우편으로 건조한 혈액 스팟 키트의 채택을 가속화하고 데이터 충실성을 유지하면서 시설 방문을 최소화합니다. 임상시험에서 긍정적 경험은 혈청 수준의 지침을 명시한 시판 후 라벨의 확장으로 이어져 일상적인 임상 수요가 확대됩니다. 이러한 피드백 루프를 통해 임상 시장 개척을 위한 지출은 치료제 모니터링 시장 전반의 분석 제조업체 및 서비스 실험실의 지속적인 수익원이 됩니다.

엔트리 레벨 삼중 사중극 시스템은 30만-50만 달러, 연간 보수 계약은 5만 달러로 중저소득국의 2차 병원과 민간 실험실 예산을 압박하고 있습니다. 선진국 시장에서도 재정관리위원회는 구매를 승인하기 전에 확고한 이용 예측을 요구합니다. 높은 구매 기준치는 선적 검사를 길게 하고, 납기를 연장하고, 즉각적인 임상적 가치를 감소시키고, 따라서 루틴 검사의 채용을 지연시킵니다. 공동구매 컨소시엄과 시약 임대 모델은 현금흐름 제약을 부분적으로 완화하고 있지만, 많은 시설들은 특이성이 낮은 면역측정법에 의존하고 있으며, 키나제 억제제나 면역요법 등 교차반응에 민감한 응용은 치료제 모니터링 시장 전체에서 제한됩니다.

2024년 치료제 모니터링 시장 규모에서는 면역 측정법이 59.37%의 점유율을 차지하여 최대 수익 부분을 창출했습니다. 레거시 케미스트리 라인에 통합, 일관된 상환 코딩, 기술자의 숙련도가 이 리드를 유지하고 있습니다. 그러나 바이오센서와 착용가능한 플랫폼은 간질액에서 in-situ 약물 수준 판독을 가능하게 하는 전기화학적 전달의 진보에 힘입어 CAGR 9.87%로 성장을 지속하고, 있습니다. 질량분석법 관련 면역화학의 하이브리드는 저분자의 암 치료제에 대응하는 메뉴를 넓혀 기존 기술의 관련성을 더욱 강화하고 있습니다.

단백질 결합 간섭, 후크 효과, 교차 반응성의 제한으로 인해 3차 의료기관은 복잡한 요법에 대응하는 크로마토그래피나 LC-MS/MS 솔루션으로 이행하여 멀티벤더의 경쟁이 격화되고 있습니다. 한편, 지속적인 웨어러블 프로토타입 파이프라인은 샘플링 간격을 1분 미만으로 약속하고 시장 패러다임을 에피소드 추출에서 동적 약동학 프로파일링으로 재정의합니다. 벤처기업이 제약 스폰서와 연계하여 디바이스를 장시간 작용형의 주사제와 조합함으로써 임상 검증을 가속시킵니다. 규제 경로가 명확해짐에 따라 경쟁력 다이어그램은 분석 감도뿐만 아니라 사용성, 데이터 보안 아키텍처 및 알고리즘을 통한 관리 지침에 점점 더 좌우됩니다.

2024년의 치료제 모니터링 시장 규모에 대한 북미의 기여율은 42.17%인데, 이는 보험상환 정착, 광범위한 이식 프로그램, 파마코유전체학의 리더십에 의한 것입니다. 유럽은 통합 조달 및 결과 기반 가격 설정을 선호하는 비용 억제 압력 하에 있는 성숙도를 반영합니다. 아시아태평양은 2030년까지 CAGR가 10.44%로 예상되는데, 이는 병원 건설 붐, 임상시험에 대한 자금유입, 국가적인 프리시전 헬스 이니셔티브를 반영하고 있습니다.

중국은 공공 부문의 인프라 자금과 현지에서 LC-MS/MS 제조를 장려하는 엄격한 규제 개혁을 연결하여 이 지역의 수량 증가를 주도하고 있습니다. 일본은 초고령화 사회에서 1인당 검사비율이 높고, 인도는 의료보험의 적용범위가 확대되고, 필수 모니터링 패널에 대한 환자 접근이 확산되고 있습니다. 중동과 남미는 실험실 자동화 벤더가 정부 기관과 제휴하여 진단 능력을 근대화하고 치료제 모니터링 시장을 단계적으로 확대하기 위해 노력하고 있기 때문에 도입 곡선은 초기지만 가속화되고 있습니다.

The therapeutic drug monitoring market reached USD 1.36 billion in 2025 and is forecast to attain USD 2.11 billion by 2030, advancing at a 9.12% CAGR.

Rising adoption of precision-medicine programs, integration of pharmacogenomic decision tools, and expanding decentralized clinical-trial activity anchor this expansion, while cost-pressured hospital systems increasingly favor high-throughput core-lab automation to sustain routine testing volumes. Continuous biosensor platforms and dried-blood-spot sampling are widening access well beyond tertiary centers, enabling remote dose titration and reducing adverse-event risk across oncology, HIV, and autoimmune therapy protocols. Regulatory alignment, including the United States Food and Drug Administration's phased oversight of laboratory-developed tests, is expected to raise quality baselines and accelerate payer acceptance of broader test panels. Nonetheless, capital constraints in emerging markets continue to limit deployment of liquid-chromatography tandem mass-spectrometry (LC-MS/MS) analyzers, tempering penetration of highly specific assays.

Cancer protocols increasingly pair small-molecule kinase inhibitors with monoclonal antibodies, creating narrow therapeutic margins that mandate precise serum-level control to avoid suboptimal tumor inhibition or dose-limiting toxicity . Long-acting cabotegravir-rilpivirine combinations for HIV expand monitoring horizons beyond daily oral dosing, requiring confirmation of sustained trough concentrations over monthly or bi-monthly intervals. Autoimmune conditions now routinely employ biologic disease-modifying agents whose clearance rates vary with anti-drug antibody formation, and therapeutic drug monitoring provides an evidence-based path to differentiate primary non-response from immunogenic loss of efficacy. Cardiovascular cases driven by aging populations reinforce volume growth for digoxin and antiarrhythmic level checks to avert iatrogenic toxicity. Together, these disease burdens add consistent patient cohorts to the therapeutic drug monitoring market, underpinning predictable test-volume increases.

Regulators now expect dose-optimization evidence across diverse genotypes and comorbidity profiles during pivotal trials, firmly embedding therapeutic drug monitoring into study protocols. Sponsors therefore integrate sample-to-insight workflows that merge LC-MS/MS analytics with pharmacogenomic algorithms, enabling adaptive dosing arms and reducing late-stage attrition. Decentralized trial models accelerate adoption of mailed dried-blood-spot kits, preserving data fidelity while minimizing site visits. Positive experience in trials subsequently informs post-marketing label expansions that specify serum-level guidance, which in turn grows routine clinical demand. The feedback loop converts clinical-development spending into durable revenue streams for assay manufacturers and service laboratories across the therapeutic drug monitoring market.

Entry-level triple-quadrupole systems list at USD 300,000-500,000, and annual maintenance contracts add USD 50,000, stretching budgets of secondary hospitals and private labs in low- and middle-income economies . Even in developed markets, fiscal stewardship committees demand robust utilization forecasts before approving purchases. High acquisition thresholds perpetuate send-out testing, lengthening turnaround times and diminishing immediate clinical value, which in turn slows routine test adoption. Pooled-purchasing consortia and reagent-rental models partially mitigate cash-flow constraints, yet many facilities remain reliant on less specific immunoassays, limiting cross-reactivity-sensitive applications such as kinase inhibitors and immunotherapies across the therapeutic drug monitoring market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Immunoassays generated the largest revenue portion of the therapeutic drug monitoring market size, holding a 59.37% share in 2024. Integration into legacy chemistry lines, consistent reimbursement coding, and technician familiarity sustain this lead. However, biosensor and wearable platforms are recording a 9.87% CAGR, underpinned by electrochemical transduction advances that enable in-situ drug-level readouts from interstitial fluid. Mass-spectrometry-linked immunochemical hybrids widen menus to encompass small-molecule oncology agents, further reinforcing the incumbent technology's relevance.

Protein-binding interference, hook effects, and cross-reactivity limitations have propelled tertiary centers toward chromatographic and LC-MS/MS solutions for complex regimens, fortifying multivendor competition. Continuous wearables prototype pipelines, meanwhile, promise sub-minute sampling intervals, redefining therapeutic drug monitoring market paradigms from episodic draws to dynamic pharmacokinetic profiling. Venture-backed start-ups align with pharmaceutical sponsors to pair devices with long-acting injectables, accelerating clinical validation. As regulatory pathways clarify, competitive dynamics will increasingly hinge on usability, data-security architecture, and algorithmic dosing guidance rather than analytical sensitivity alone.

The Therapeutic Drug Monitoring Market is Segmented by Technology (Immunoassays, Proteomic, and More), Drug Class (Antiarrhythmic Drugs, Immunosuppressants, and More), End-User (Hospital Laboratories, Independent / Reference Laboratories, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America's 42.17% contribution to the therapeutic drug monitoring market size in 2024 stems from entrenched reimbursement, extensive transplant programs, and pharmacogenomic leadership. Europe mirrors this maturity, albeit under cost-containment pressures that prioritize consolidated procurement and outcome-based pricing. Asia-Pacific exhibits a 10.44% CAGR through 2030, reflecting hospital construction booms, clinical-trial inflows, and national precision-health initiatives.

China commands the region's volume uplift, coupling public-sector infrastructure funding with stringent regulatory reforms that encourage local LC-MS/MS manufacturing. Japan's super-aged demographics sustain high per-capita test ratios, while India's expanding health-insurance coverage widens patient access to essential monitoring panels. Middle East and South America show nascent yet accelerating adoption curves as laboratory automation vendors partner with government agencies to modernize diagnostic capabilities, an endeavor that incrementally enlarges the therapeutic drug monitoring market.