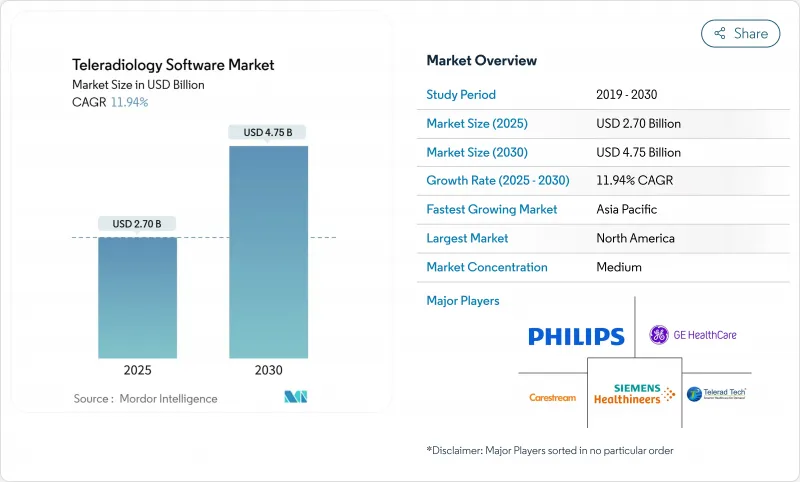

세계의 원격 방사선 진단 소프트웨어 시장 규모는 2025년 27억 달러로, 2030년까지 47억 5,000만 달러에 이를 것으로 추정되며, 예측 기간 중(2025-2030년) CAGR은 11.94%로 확대될 것으로 보입니다.

원격 방사선 진단 소프트웨어 시장 규모의 궤적은 서로 보강하는 세 가지 힘, 즉 세계적인 방사선과 의사 부족 확대, 연간 3-4% 증가하는 영상 처리량, 즉각적인 확장을 가능하게 하는 클라우드 아키텍처를 기반으로 합니다. 병원은 24시간 365일 체제로 전문의를 확보하기 위해 플랫폼을 도입하고, 진단센터는 방사선과 의사를 고용하지 않고 진료 시간을 연장하기 위해 플랫폼을 활용하고 있습니다. 테크놀로지 벤더는 AI 트리어지나 구조화 보고 모듈을 짜넣어, 판독 생산성을 최대 30% 향상시켜, 번아웃 증후군 경감에 도움이 되고 있습니다. 현재는 규제에 의해 원격 판독이 정식으로 인정되고 진료 보수의 평준화가 진행됨에 따라 예산은 디지털 인프라로 향하고 있습니다. 클라우드 네이티브로 AI에 대응한 에코시스템을 둘러싼 경쟁이 격화하는 가운데, 이러한 다이내믹스가 2자리 성장을 지지하고 있습니다.

의료용 영상 수요는 2055년까지 27% 더 증가해, 한정된 방사선과의 자원에 대한 압력이 높아집니다. CT 검사만으로도 25.1% 증가할 가능성이 있으며, 핵의학검사와 X선 검사도 이에 보조를 맞춥니다. 이미 매년 42억 건의 검사가 진행되고 있기 때문에 의료 시스템은 판독 능력을 유연하게 하고, 하위 전문가의 전문 지식을 분배하고, 납기를 품질 기준 내에 유지하기 위해 원격 방사선 진단에 의존하고 있습니다. 오버플로우 검사를 전국적 또는 대륙 네트워크로 라우팅하는 능력은 관리의 연속성을 유지하고 예약 체류를 줄입니다.

미국에서는 2034년까지 최대 12만 4,000명의 의사 부족에 직면할 수 있으며, 방사선과의 포스트는 가장 충족하기 어려운 포스트 중 하나입니다. 영국에서는 방사선과의 부족이 30%에 달하고, 매년 13% 가까이 감소하고 있습니다. 생산성 지표에 따르면, 원격 방사선과 그룹은 전통적인 현장 팀보다 판독자당 최대 3분의 1 더 많은 검사를 처리하고 있습니다. 지방 병원이나 지역 병원이 야근이나 주말 시프트의 인원 확보에 고민하는 중, 아웃소싱은 구조적인 해결책이 되어, 복수 사이트의 워크플로우와 자격 인정을 조정하는 소프트웨어에 대한 수요를 확고하게 하고 있습니다.

미국의 HIPAA 암호화 규칙과 유럽의 GDPR(EU 개인정보보호규정) 규정을 충족시키기 위해 특별히 전임 보안 직원이 없는 소규모 클리닉에서는 도입 비용이 부과됩니다. 국경을 넘어서는 판독을 관리하는 조직은 중복 동의 규제와 인시던트 보고 의무를 탐색해야 하며, 대부분의 경우 총 소유 비용을 늘리는 제3자 감사에 위탁합니다. 헬스케어 조직이 증가하는 사이버 위협에 대처함에 따라 사이버 보안에 대한 투자는 필수가 되고, 견고한 사고 대응 계획이나 암호화 프로토콜을 필요로 하는 임상의는 법적인 의미도 나옵니다.

PACS는 2024년 45.32%의 점유율을 차지하며 여전히 핵심 기술입니다. 동시에 VNA는 13.12%의 연평균 복합 성장률(CAGR)을 기록해 공급업체의 중립성과 기업의 이미지 통합에 대한 전환을 보여줍니다. VNA와 관련된 원격 방사선 진단 소프트웨어 시장 규모는 조직이 사일로화된 아카이브에서 마이그레이션됨에 따라 급증할 전망입니다. 필라델피아 소아 병원은 VNA 전환 후 5년간 300만 달러의 비용 절감을 보고했습니다.

CARPL.ai의 FDA 인증 허브에서 알 수 있듯이 RIS와 신흥 기업 플랫폼은 현재 단일 인터페이스를 통해 110개 이상의 인증된 AI 앱을 통합하고 있습니다. 이러한 상호 운용성은 보고서 작성 시간을 단축하고 비용이 많이 드는 데이터 마이그레이션을 줄여 VNA는 경제적으로나 임상적으로 눈에 보이는 이점을 제공합니다.

클라우드 도입은 2024년에는 원격 방사선 진단 소프트웨어 시장의 62.44%를 차지하고 CAGR 12.88%에 달할 것으로 보입니다. Amazon Web Services는 HealthCare의 Genesis 포트폴리오를 지원하며 원 클릭 신축성과 AI 확장성을 약속합니다.

방위 및 학술 센터에서는 맞춤형 대기 시간과 주권이 요구되므로 On-Premise 시스템이 지속됩니다. 그러나 하이브리드 셋업이 대두되어 기밀성이 높은 연구를 로컬로 남기면서 클라우드 분석을 집단 의료에 활용할 수 있게 되었습니다. 이러한 균형 잡힌 접근 방식은 컴플라이언스와 혁신을 양립시켜 원격 방사선 진단 소프트웨어 시장에서 다층 전개 오케스트레이션에 대한 수요를 강력하게 유지합니다.

북미는 2024년에 39.83%의 점유율로 선두를 두었고, 상환 가능한 원격 의료 정책과 FDA에 의한 1,000개 이상의 임상 AI 도구의 허가가 뒷받침되었습니다. 지역 액세스 이니셔티브는 소규모 병원에 보조금을 흘려 원격 방사선 진단 소프트웨어 시장을 더욱 홍보합니다. ONRAD가 Direct Radiology를 흡수하는 등 현재 진행중인 합병은 독립적인 커버리지 네트워크를 확장하고 표준화된 워크플로우 소프트웨어를 홍보합니다.

아시아태평양은 CAGR 13.64%로 가장 빨리 인도의 아유슈만 바랏 디지털 미션에 지지되고 있습니다. 인도네시아의 PT.Teleradiologi Center Indonesia는 전문의의 접근을 확대하고 호주 National Digital Health Strategy는 안전한 이미지 공유 그리드에 자금을 제공합니다. 이러한 이니셔티브를 결합하면 클라우드 PACS 공급업체와 현지 신흥 기업의 진입 장벽이 낮아집니다.

유럽에서는 40억 유로를 투입한 'Hospital Future Act'에 의해 독일 병원의 디지털화 지수는 100점 만점 중 불과 33.3점이 되어 투자 갭이 부각되었지만 꾸준히 도입이 진행되고 있습니다. EU의 부흥 및 회복 기금(Recovery and Resilience Facility)은 지출의 5분의 1을 디지털 인프라에 채우는 것을 규정하고, 국경을 넘은 이미지 공유 파일럿과 의료법의 틀의 조화를 촉진하고 있습니다. 중동 및 아프리카, 남미는 아직 발전도상이지만, 퍼블릭 클라우드의 전개와 도시의 암센터의 건설이 원격 방사선 진단 소프트웨어 시장의 기초적인 수요를 형성하고 있습니다.

The Teleradiology Software Market size is estimated at USD 2.70 billion in 2025, and is expected to reach USD 4.75 billion by 2030, at a CAGR of 11.94% during the forecast period (2025-2030).

The teleradiology software market size trajectory rests on three mutually reinforcing forces: a widening global radiologist shortfall, imaging volumes that climb 3-4% a year, and cloud architectures that allow instant scale. Hospitals deploy the platforms to secure 24/7 subspecialist coverage, while diagnostic centers harness them to extend hours without hiring on-site radiologists. Technology vendors are embedding AI triage and structured-report modules, which boost reading productivity by up to 30% and help mitigate burnout. Regulations now formally recognize remote preliminary reads, and growing reimbursement parity is steering budgets toward digital infrastructure. Together, these dynamics sustain double-digit growth while intensifying competition around cloud-native, AI-ready ecosystems.

Medical imaging demand is set to climb another 27% by 2055, amplifying pressure on limited radiology resources. CT studies alone could rise 25.1%, while nuclear medicine and X-ray work keep pace. With 4.2 billion examinations already performed each year, health systems depend on teleradiology to flex reading capacity, distribute subspecialist expertise, and keep turnaround times within quality benchmarks. The ability to route overflow studies across national or even continental networks preserves continuity of care and mitigates appointment backlogs.

The United States may face a deficit of up to 124,000 physicians by 2034, and radiology posts are among the hardest to fill. The United Kingdom reports a 30% radiologist gap, while attrition sits near 13% annually. Productivity metrics show teleradiology groups processing as many as one-third more studies per reader than conventional onsite teams. As rural and community hospitals struggle to staff night and weekend shifts, outsourcing becomes a structural solution, solidifying demand for software that coordinates multi-site workflows and credentialing.

Meeting HIPAA encryption rules in the United States and GDPR restrictions in Europe raises deployment expenses, particularly for smaller clinics that lack dedicated security staff. Organizations managing cross-border reads must navigate overlapping consent regulations and incident-reporting duties, often commissioning third-party audits that inflate total cost of ownership. Cybersecurity investments become mandatory as healthcare organizations address increasing cyber threats, with legal implications for clinicians requiring robust incident response plans and encryption protocols.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

PACS remained the anchor technology with 45.32% share in 2024. At the same time, VNA logged a 13.12% CAGR outlook, signaling a pivot toward vendor neutrality and enterprise imaging consolidation. The teleradiology software market size attached to VNA is set to rise sharply as organizations migrate away from siloed archives. Children's Hospital of Philadelphia reported USD 3 million savings in five years after its VNA transition.

RIS and nascent enterprise platforms now integrate over 110 certified AI apps through single interfaces, as shown by CARPL.ai's FDA-cleared hub. Such interoperability compresses report-turnaround times and reduces costly data migrations, giving VNAs tangible economic and clinical advantages.

Cloud installations represented 62.44% of the teleradiology software market in 2024 and are on track for a 12.88% CAGR. Amazon Web Services underpins GE HealthCare's Genesis portfolio, which promises one-click elasticity and AI scalability.

On-premise systems persist in defense and academic centers with bespoke latency or sovereignty mandates. Yet hybrid setups emerge, allowing sensitive studies to remain local while leveraging cloud analytics for population health. This balanced approach reconciles compliance with innovation and keeps demand for multi-tier deployment orchestration strong within the teleradiology software market.

The Teleradiology Software Market Report is Segmented by Solution Type (Radiology Information System (RIS), Picture Archiving & Communication System (PACS) and More), Deployment Mode (Cloud-Based and On-Premise), Imaging Modality Supported (X-Ray, Computed Tomography (CT), and More), End User (Hospitals, and More), and Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led with 39.83% share in 2024, buoyed by reimbursable telehealth policies and FDA clearance of more than 1,000 clinical AI tools, 758 of which target radiology. Rural access initiatives channel grants to small hospitals, further propelling the teleradiology software market. Ongoing mergers, such as ONRAD absorbing Direct Radiology, extend independent coverage networks and promote standardized workflow software.

Asia-Pacific registers the quickest 13.64% CAGR, underpinned by India's Ayushman Bharat Digital Mission that issues unique health IDs ready for image exchange. Indonesia's launch of PT. Teleradiologi Center Indonesia widens subspecialist access, while Australia's National Digital Health Strategy funds secure image-sharing grids. Combined, these initiatives lower entry barriers for cloud PACS vendors and local startups.

Europe shows steady adoption, aided by the EUR 4 billion Hospital Future Act that scored German hospitals at just 33.3 on a 100-point digitization index, spotlighting investment gaps. The EU Recovery and Resilience Facility stipulates that a fifth of spending targets digital infrastructure, catalyzing cross-border image-sharing pilots and harmonized medico-legal frameworks. Middle East, Africa, and South America remain nascent, yet public cloud rollouts and urban cancer-center build-outs are laying foundational demand for the teleradiology software market.