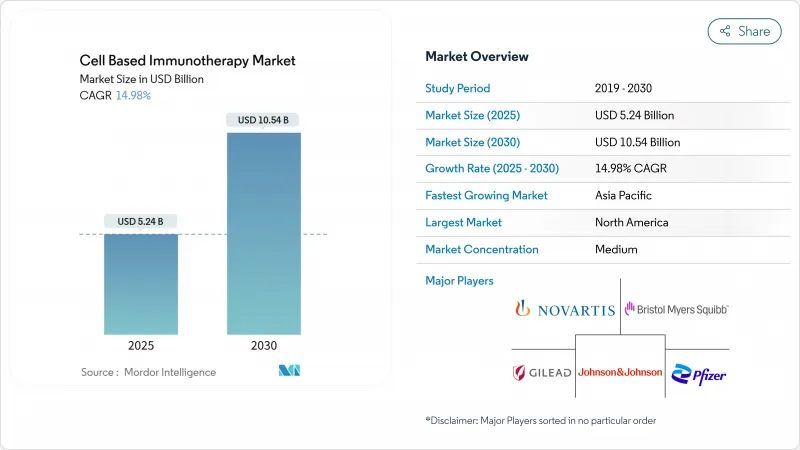

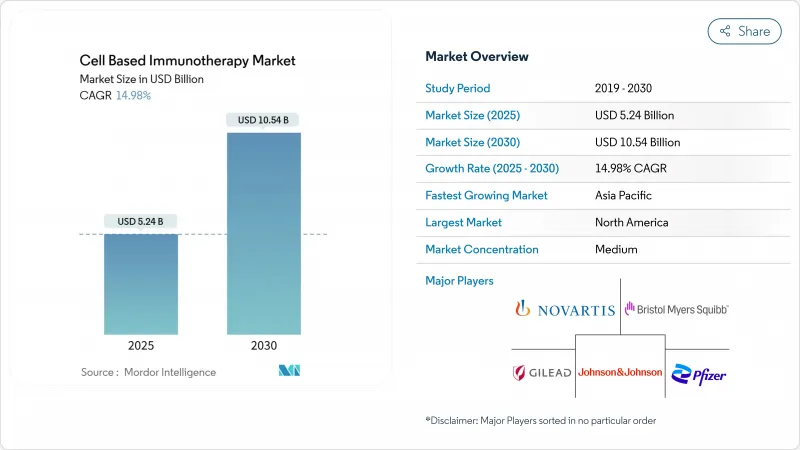

세포 기반 면역요법 시장은 2025년에 52억 4,000만 달러를 창출하고, 2030년에는 105억 4,000만 달러에 달할 것으로 예상되며, CAGR은 14.98%를 나타낼 전망입니다.

CAR-T 플랫폼은 2024년에 FDA로부터 허가된 8가지 신규 세포 제품(최초 간엽계 간질요법인 Ryoncil을 포함)에 힘입어 현재 치료에서 제2 치료의 표준 치료로 전환하고 있습니다. 외래 점적 프로토콜은 총 의료비를 줄임으로써 세포 기반 면역요법 시장을 더욱 재구성하고 있습니다. 등록 데이터에 따르면 외래환자의 25%가 30일간 입원을 피하고 있습니다. 2024년 매출액의 89.55%는 자가제품이 차지했지만 기제품의 편의성에 대한 수요를 반영하고 동종제품은 CAGR 30.25%를 나타낼 전망입니다. 치료상의 초점은 여전히 B세포 악성종양이며, 2024년의 치료증례의 45.53%를 차지했지만, 신세포암이 CAGR 25.15%로 다음의 적응증의 파를 리드하고 있습니다. 북미는 2024년 지출액의 47.72%를 차지했지만, 아시아태평양은 현지 제조업체의 생산 비용 절감으로 CAGR 27.22%로 가장 급속히 확대하고 있습니다.

CARTITUDE-4가 표준 치료에 대해 사망 위험을 45% 감소시켰음을 보여준 후, Carvykti가 FDA의 첨부 문서 확대를 확보함으로써, 제2라인 채용이 가속화되었습니다. CARTITUDE-1의 장기 추적 연구는 5년 시점에 33%의 환자가 생존하고 무증상이었기 때문에 기능적 치유의 가능성을 시사했습니다. 메디케어및메디케이드 서비스센터는 2026년도에 CAR-T의 기본요금을 17% 인상할 예정이며, 병원의 경제성을 개선하고 의사의 채용을 가속시킵니다. CAR-T의 배치가 빨라짐으로써, 보다 짧은 제조 기간을 허용하고, 보다 적은 부작용을 경험하는 보다 적절한 환자의 치료가 가능해져, 세포 기반 면역요법 시장이 확대됩니다. 또한 적응증이 확대됨에 따라 지불보험사의 적용 범위도 확대되고 종양센터 전체에서의 판매량도 증가합니다.

CRISPR 편집의 규제적 선례는 2024년에 FDA가 헤모글로빈 이상증에 대한 최초의 Cas9 변형 요법을 승인할 때 설정되었습니다. 그 후, IL-15로 무장한 GPC3 CAR-T 세포는 고형 종양에서 66%의 질환 제어율을 달성하여 사이토카인 증강 구조를 검증하였습니다. 존슨 엔드 존슨의 CD19/CD20 프로그램과 같은 듀얼 타겟 디자인은 1차 치료의 대세포형 B 세포 림프종에서 100%의 객관적 주효를 나타냈습니다. 한편, 차세대 벡터 플랫폼은 렌티바이러스의 제조를 표준화하고 용량당 비용 곡선을 낮추고 있습니다. 이러한 혁신은 지속성을 높이고 재발 위험을 줄이고 생산 처리량을 향상시키고 세포 기반 면역요법 시장을 직접 확장합니다.

미국 정부 책임국은 많은 개발·제조 수탁기관이 GMP 인력 부족으로 인해 용량 부족에 빠져 있다고 지적하고 있습니다. 렌티바이러스 벡터의 부족은 스케일 업의 비효율성이 개선되지 않는 한 수요가 공급을 초과하고 생산의 연속성을 위협합니다. 자동화에 의해 숙련 오퍼레이터의 필요성은 감소하는 것, 해소되는 것은 아니고, 숙련 기술자의 대부분은 미국과 EU의 소수의 허브 주변에 모여 있기 때문에 세계적인 여행에 의한 혼란시에 지역의 취약성이 높아집니다. 자본 집약적 인 콜드체인 네트워크는 편차가 있으면 제품의 생존을 위협하고 응급 환자의 치료를 지연시키고 세포 기반 면역요법 시장 전체의 수익 인식을 둔화시킬 수 있으므로 위험을 증가시킵니다.

2024년 매출액의 89.55%를 자가면역계가 차지했으며, 같은 해 세포 기반 면역요법 시장 규모는 47억 달러에 달했습니다. 전설적인 치료 성적과 확립된 규제 템플릿은 병원의 선호도를 지원하지만, 각 환자별 배치는 여전히 전문적인 물류와 장기간의 처리가 필요합니다. 한편, 동종요법 분야는 CAGR 30.25%를 나타내 2025년부터 2030년에 걸쳐 세포 기반 면역요법 시장 규모에 대한 기여가 19억 달러 증가할 것으로 예측되고 있습니다. FDA가 소아급성 이식편 대 숙주병에 대한 최초의 기성품 간엽계 간질 제형인 Ryoncil을 승인함으로써 규제상의 선례가 굳어졌습니다.

Cellares사의 Cell Shuttle은 80%의 공간 효율과 75%의 노동력 절감을 보여주며, 동종이식의 가격 곡선을 1회당 15만 달러 이하로 밀어냅니다. 범용 CAR-NK 파이프라인은 이식편 대 숙주병 위험을 줄이고 기증자 스크리닝을 단순화합니다. 아스텔라스 제약과 포지다는 생물학적 제제처럼 스톡 가능한 동종요법 프로그램의 확대에 8억 달러를 투입하여 치료 능력을 크게 확대했습니다. 지급자의 모니터링이 강화됨에 따라 저가격으로 기성품이 자가 이식의 지위를 침식 할 수 있지만 대부분의 암 전문의는 전환하기 전에 경험적 생존율 데이터에 의존하는 것이 현재입니다.

북미의 의료 제공업체는 고급 상환의 확실성과 깊은 소개 네트워크의 혜택을 누리고 있으며, 노동력 부족과 벡터 병목에도 불구하고 치료량의 밀도를 유지하고 있습니다. CMS 지불 증가와 여러 국내 확장 프로젝트는 심각한 백로그 없이 초기 라인 수요를 흡수할 수 있으며, 이 지역은 안정적인 2자리 성장이 가능합니다. UCSF와 같은 아카데믹 센터는 동시에 자가면역 질환에 대한 응용을 모색하고 있으며, 암 영역 이외의 수익원을 다양화할 가능성이 있습니다.

아시아태평양 시장은 중국의 높은 임상시험 밀도와 인도의 비용 효율적인 이동 시설로 대표되는 국내 제조 주권을 지원하는 정책적 인센티브를 받아들입니다. 6만 달러 미만의 현지 가격대는 중간소득층 환자에 대한 적격성을 넓히고 있지만, 의료기관의 인정은 인구 요구보다 늦어서, 구미의 라이선스 보유자와 지역의 계약 제조업자와의 제휴를 촉구하고 있습니다. 일본과 한국은 다국적 기업의 국내 시설 입지를 뒷받침하는 합리화된 규제 인가를 제공하고 있지만 공급망의 회복력은 여전히 수입 벡터와 일회용 바이오리액터 소모품에 달려 있습니다.

유럽의 활동은 규제 프로세스의 중앙 집중화와 성과 연동형 지불을 위한 단계적인 상환 제도 개혁에 견인되어 견조하게 추이하고 있습니다. 노바티스와 브리스톨 마이어스 스퀴브의 현지화 전략은 물류의 복잡성을 완화하고, 학술적인 세포 제조 프로그램은 국가 의료 서비스에 저렴한 비용의 선택을 제공합니다. EBMT는 이식 횟수가 가변적임에도 불구하고 CAR-T 활성이 지속적으로 성장하고 있다고 보고하였으며, 치료 선호도의 변화를 밝히고 있습니다. 그러나 비용 억제 압력으로 인해 치료 성적 데이터가 성숙할 때까지 광범위한 두 번째 라인 사용이 제한되어 확대되는 세포 기반 면역요법 시장에 대한 이 지역의 기여가 완만해졌습니다.

The cell-based immunotherapy market generated USD 5.24 billion in 2025 and is forecast to reach USD 10.54 billion by 2030, yielding a 14.98% CAGR.

CAR-T platforms now move from last-line rescue to second-line standard care, encouraged by eight novel cellular products cleared by the FDA in 2024, including the first mesenchymal stromal therapy, Ryoncil. Outpatient infusion protocols are further reshaping the cell-based immunotherapy market by lowering total care costs; registry data show that 25% of outpatients avoid a 30-day hospital admission. Autologous products held 89.55% of 2024 revenue, yet the allogeneic segment is growing at 30.25% CAGR, reflecting demand for off-the-shelf convenience. Therapeutic focus remains on B-cell malignancies, which comprised 45.53% of treated cases in 2024, but renal cell carcinoma leads the next indication wave with a 25.15% CAGR nature.com. North America commanded 47.72% of 2024 spending, while Asia-Pacific is expanding fastest at 27.22% CAGR as local manufacturers cut production costs.

Second-line adoption accelerated when Carvykti secured an FDA label expansion after CARTITUDE-4 showed a 45% mortality risk reduction against standard care. Long-term follow-up from CARTITUDE-1 found 33% of recipients alive and progression-free at 5 years, suggesting functional cure potential. The Centers for Medicare & Medicaid Services plans a 17% base-rate increase for CAR-T in FY 2026, improving hospital economics and accelerating physician adoption. Earlier-line positioning enlarges the cell-based immunotherapy market by treating fitter patients who tolerate shorter manufacturing windows and experience fewer adverse events. Expanded labels also translate into broader payer coverage, enhancing volume growth across oncology centers.

Regulatory precedent for CRISPR editing was set in 2024 when the FDA cleared the first Cas9-modified therapies for hemoglobinopathies. IL-15-armored GPC3 CAR-T cells subsequently achieved 66% disease-control rates in solid tumors, validating cytokine-enhanced constructs. Dual-target designs such as Johnson & Johnson's CD19/CD20 program posted 100% objective responses in first-line large B-cell lymphoma. Meanwhile, next-generation vector platforms standardize lentiviral manufacture, lowering per-dose cost curves. These innovations enhance persistence, reduce relapse risk and increase manufacturing throughput, directly expanding the cell-based immunotherapy market.

The U.S. Government Accountability Office highlights that many contract development and manufacturing organizations run under capacity because of GMP workforce gaps. Lentiviral vector shortages threaten production continuity, with demand outstripping supply unless scale-up inefficiencies are corrected. Automation reduces but does not eliminate expert-operator needs, and most skilled technicians cluster around a handful of U.S. and EU hubs, raising regional fragility during global travel disruptions. Capital-intensive cold-chain networks compound risk, as any deviation jeopardizes product viability, potentially delaying treatment for high-acuity patients and slowing revenue recognition across the cell-based immunotherapy market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Autologous constructs generated 89.55% of 2024 revenue, anchoring the cell-based immunotherapy market size at USD 4.70 billion that year. Legendary outcomes and well-established regulatory templates sustain hospital preference, though each patient-specific batch still demands specialized logistics and lengthy processing. Meanwhile, the allogeneic segment is forecast to advance at 30.25% CAGR, expanding its contribution to the cell-based immunotherapy market size by an incremental USD 1.9 billion between 2025 and 2030. Regulatory precedent was cemented when the FDA cleared Ryoncil, the first off-the-shelf mesenchymal stromal product for pediatric acute graft-versus-host disease fda.gov.

Automation is narrowing cost differentials; Cellares's Cell Shuttle shows 80% space efficiency and 75% labor savings, translating into lower all-in COGS that push the allogeneic price curve below USD 150,000 per dose. Universal CAR-NK pipelines reduce graft-versus-host-disease risk and simplify donor screening. Astellas and Poseida alone committed USD 800 million to expand allogeneic programs that can be stock-piled like biologics, significantly expanding treatment capacity. As payer scrutiny intensifies, lower-priced, off-the-shelf constructs could erode autologous incumbency, though most oncologists still rely on empirical survival data before switching.

The Cell Based Immunotherapy Market Report is Segmented by Therapy (Autologous and Allogeneic), Primary Indication (B-Cell Malignancies, Prostate Cancer, Renal Cell Carcinoma, Liver Cancer, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North American providers benefit from advanced reimbursement certainty and a deep referral network, keeping treatment volume dense despite workforce shortages and vector bottlenecks. CMS payment increases and multiple domestic expansion projects can absorb earlier-line demand without severe backlog, positioning the region for stable double-digit growth. Academic centers such as UCSF are simultaneously exploring autoimmune applications, which may diversify revenue streams outside oncology.

Asia-Pacific markets embrace policy incentives that support domestic manufacturing sovereignty, exemplified by China's high trial density and India's cost-efficient mobile facilities. Local price points under USD 60,000 broaden eligibility for middle-income patients; however, center accreditation lags behind population need, prompting partnerships between Western license holders and regional contract manufacturers. Japan and South Korea offer streamlined regulatory approvals that encourage multinationals to site facilities domestically, yet supply chain resilience still hinges on imported vectors and single-use bioreactor consumables.

European activity remains steady, driven by centralized regulatory processes and incremental reimbursement reforms toward performance-linked payment. Localization strategies by Novartis and Bristol Myers Squibb mitigate logistical complexity, and academic cell-manufacture programs provide lower-cost options for national health services. The EBMT reports sustained CAR-T activity growth as transplant numbers flatten, underscoring shifting therapeutic preferences. Nonetheless, cost-containment pressures limit broad second-line use until outcomes data mature, moderating the region's contribution to the expanding cell-based immunotherapy market.