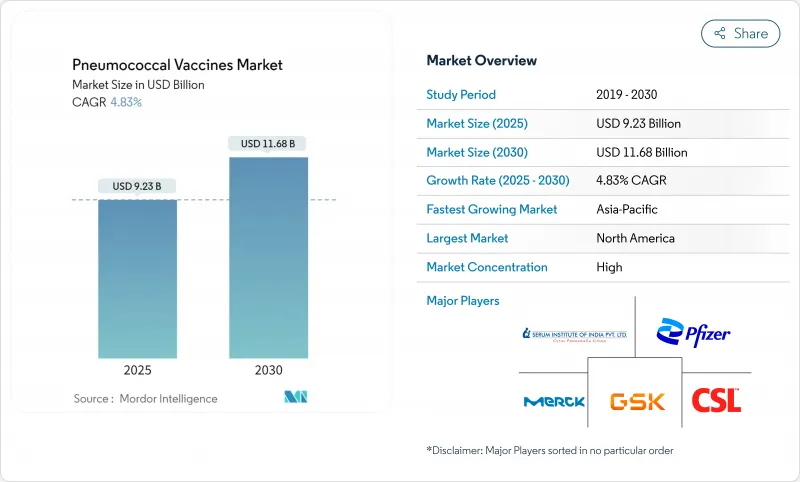

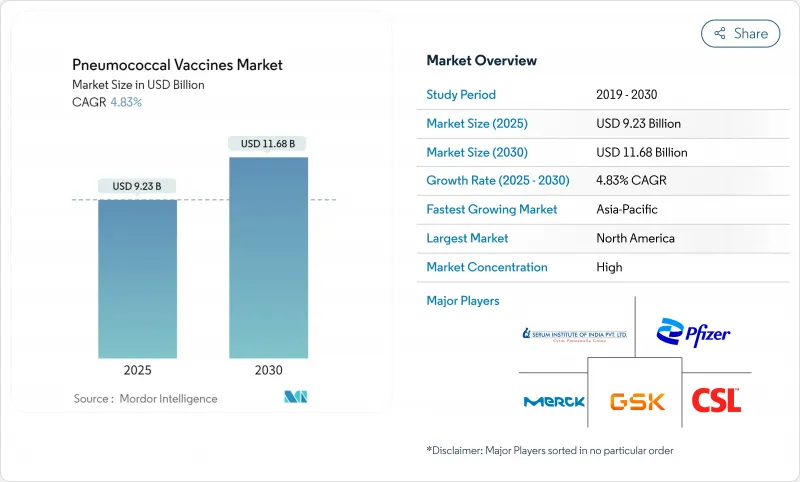

세계의 폐렴구균 백신 시장의 2025년 시장 규모는 92억 3,000만 달러로, CAGR 4.82%를 반영하여 2030년까지 116억 8,000만 달러에 이를 것으로 예측됩니다.

7가, 10가, 13가 제형에서 15가, 20가, 21가의 결합형 백신으로 지속적인 이동, 성인에 대한 백신접종 가이드라인 확대, 신흥국에서의 전개 확대가 이 꾸준한 성장 궤도를 지원하고 있습니다. 북미가 주요 수익의 중심임에 변화는 없지만, 국내 제조업체가 생산량을 확대하고, 각국 정부가 폐렴구균 결합형 백신을 정기 접종에 통합하고 있기 때문에 아시아태평양의 기세가 가장 강해지고 있습니다. Merck의 성인용 Capvaxive 출시, PCV21의 유럽 승인, Vaxcyte의 윤택한 자금을 갖춘 31가 파이프라인에 이어 경쟁이 치열해지고 있습니다. 한편, GAVI 주도의 조달, 투여 가격의 저하, 콜드체인 기술의 진화에 의해 자원에 제약이 있는 지역에서의 액세스가 확대되고 있습니다. 혈청형에 의존하지 않는 단백질 기반 후보 약물의 진입은 제품 차별화, 제조 실적, 가격 전략을 재설정할 수 있는 장기적인 파괴적인 저류를 형성합니다.

대규모 캠페인은 폐렴구균 결합형 백신을 국가 스케줄에 통합하여 여러 해의 조달 예산을 확보함으로써 예방접종률을 일변시킵니다. 인도 프로그램에서는 현재 연간 출생수의 90% 이상이 예방접종을 받고 있으며 매년 추정 5만명의 소아사망을 막고 있습니다. 인도네시아도 GAVI를 통해 160만회 접종 자금을 조달하고 비슷한 길을 걷고 있으며, 관민연계가 수요 안정에 미치는 영향의 크기를 이야기하고 있습니다. WHO의 '수막염 박멸 2030 로드맵'은 기증자의 우선순위를 위험이 높은 피난민에게 맞추는 것으로, 기후로 인한 질병의 만연은 기존의 콜드체인 집약형보다 내열성 제제를 우선하는 포트폴리오의 재검토를 강요하는 것입니다. 따라서 정부의 지속적인 광고는 기증자의 보조금 및 단계적 가격 설정과 함께 폐렴구균 백신 시장 전반에 걸쳐 생산자의 예측 가능한 주문 흐름을 지원합니다.

수십년에 걸친 예방접종의 진보에도 불구하고, 폐렴구균성 폐렴과 수막염은 여전히 5세 미만의 어린이와 노인의 주요 감염 사인이 되고 있습니다. 2023년 토고의 수막염 급증과 같은 집단 발생은 사하라 이남의 수막염 벨트에 취약성이 남아 있음을 뒷받침하고 있습니다. 미국에서는 만성질환을 가진 19-64세 성인의 13.4%밖에 백신 접종을 받지 않았고, 주 수준의 접종률은 0-34%입니다. 홍콩의 병원에서는 폐렴구균 감염으로 입원한 후에도 대상 환자의 1/3 이하만 접종을 받고 있다고 보고하고 있습니다. 항생제 내성 균주의 출현과 함께 이러한 유행 지표는 폐렴구균 백신 시장의 성장을 지원하는 대처 가능한 부담을 보강하고 있습니다.

Prebunal 20의 승인까지 필요했던 시간은 개발자가 시험 단계에 1,434일, 공식 심사에 244일을 보냈고, 총 1,678일에 이르렀습니다. FDA가 Vaxneuvance에 대한 소아 면역 원성 데이터의 추가를 요구했기 때문에 추가 지연이 발생했습니다. 혈청형이 추가될 때마다 임상작업의 부하가 증가하기 때문에 고가의 프로그램은 더욱 장기화되어 비용이 많이 드는 경로에 직면하게 되어, 폐렴구균 백신 시장에서 당면공급 확대를 억제하고 있습니다.

폐렴구균 결합형 백신의 2024년 매출 점유율은 65.25%로, 뛰어난 면역 기억의 증거와 보다 고가의 PCV15, PCV20, PCV21로의 지속적인 이행이 견인하고 있습니다. 이 지배적인 지위는 폐렴 구균 백신 시장에 비례하여 기여할 것입니다. 대조적으로, 다당류 제제는 성인의 캐치업 캠페인과 비용에 중점을 둔 입찰로 주목받았으며, CAGR은 5.25%로 시장 전체를 웃돌고 있습니다. 컨쥬게이트의 혁신자들은 원자가의 한계에 계속 도전하고 있으며, 다당류 제조업체들은 경쟁력을 유지하기 위해 규모 효율성을 강조합니다. MalX와 PrsA와 같은 보존된 지단백질을 표적으로 하는 새로운 단백질 기반 개념은 혈청형에 얽매이지 않는 방어를 제공함으로써 현재의 분류를 모호하게 할 수 있습니다. 혈청형을 넘어서는 효능을 보여주는 초기 동물 데이터는 투자자의 관심을 높입니다.

폐렴구균 백신의 컨쥬게이트 제형 시장 규모는 다당류가 가속화되는 가운데 절대 기준으로 상승할 것으로 예측됩니다. 컨쥬게이트 제제 시장 규모는 프리미엄 가격, 다양한 입찰량, 고소득 성인층으로의 침투에 의해 뒷받침됩니다. 한편, 다당체의 확대는 수량 주도형이며, 정부는 고령자의 보험 적용 격차를 시정하기 위해 비용 효율적인 용량을 조달하고 있습니다. 두 접근법은 여전히 보완적이며, 많은 국가의 지침은 혈청형 폭과 면역 반응의 지속성을 극대화하기 위해 결합 백신, 다당류 백신의 순차 투여를 권장합니다.

Prevenar 13은 오랜 임상 데이터, 안정적인 공급 및 세계 규제 당국의 승인으로 2024년 폐렴구균 백신 시장에서 42.22%의 점유율을 획득했습니다. 후계의 Prevenar 20은 예방 효과를 확대하고 있지만, 성인에서는 Merck의 Capvaxive와 저소득의 소아 분야에서는 Synflorix와 정면에서 경쟁하고 있습니다. 뉴모벅스 23은 구형의 다당류 제제이지만, 의사가 잘 알고 있는 것과 중소득국에서의 입찰을 이기기 위한 저용량 가격이라는 이점이 있고, CAGR이 5.48%임을 설명하고 있습니다. Capvaxive와 24가와 31가의 새로운 진입 후보를 포함한 "기타"클러스터는 다양성을 가지며 2027년 이후 점유율을 확대할 가능성이 높습니다.

다중 항원 제시 시스템 후보와 합성 당쇄 파이프라인을 통해 신규 진출기업은 기존 기업의 이점을 시간이 지남에 따라 침식할 수 있습니다. 그러나 브랜드 주식, 콜드체인 네트워크 및 시판 후 안전 모니터링 인프라는 여전히 기존 기업의 국가 조달에서 협상력을 강화하고 있습니다. 향후 경쟁 포지셔닝은 적용 범위, 성인 또는 소아를 대상으로 한 적응증, 접종 당 가격보다 완전히 예방 접종을받은 사람 당 총 비용에 달려 있습니다.

북미는 2024년 매출액 중 40.56%를 차지했으며 보험 적용, 약사에 의한 예방접종 권한, 기업에 의한 건강 증진에서 계속 이익을 얻고 있습니다. CDC의 연령 한계치 변경에 의해 대상자가 단번에 확대해, Capvaxive의 성인 특유 포지셔닝이 브랜드 전환 캠페인을 뒷받침하고 있습니다. 캐나다의 각 주 프로그램은 미국 가이드라인을 따르며, 멕시코에서는 범미 보건기구의 회전 자금을 이용하여 위험한 성인에 대한 PCV20의 공동 출자를 실시했습니다. 그럼에도 불구하고 사회 경제적 격차는 여전히 남아 있으며, 지방 주에서는 성인 이환율이 45% 미만입니다.

아시아태평양에서는 2030년까지 CAGR이 5.65%로 예측되었으며, 이는 모든 지역에서 가장 빠릅니다. 인도에서는 PNEUMOSIL 브랜드에 의한 국내에서의 저비용 생산을 원동력으로 전국 전개에 의해 연간 3,000만 회분 이상이 공급되고 있습니다. 중국의 혼합 백신 상환 확대, 싱가포르의 선구적인 PCV20의 보급은 프리미엄 혼합 백신에 대한 중간층 수요 증가를 뒷받침하고 있습니다. 인도네시아의 450만 명 목표는 인구가 많은 동남아시아 국가연합(ASEAN) 회원국의 기세를 보여줍니다. 지역의 균주 프로파일 링은 제품 전략에 영향을 미치며, 1, 5, 10A 등 지역 특유의 혈청형이 각국의 입찰을 형성하고 있습니다.

유럽에서는 유럽위원회가 2025년 5월 Capvaxive를 승인하여 독일, 이탈리아, 프랑스에서 성인의 예방접종 캠페인이 활발해져 한 자리수의 완만한 성장을 유지하고 있습니다. 광범위한 감시 능력을 통해 정책 입안자는 대체 동향의 출현 시 신속하게 일정을 검토할 수 있습니다. 중동 및 아프리카에서는 GAVI의 자금이 지속적으로 주요 기폭제가 되어 낮의 기온 40℃를 견디는 남 수단과 같은 혁신적인 태양 콜드체인 프로젝트에 의해 보완되고 있습니다. 라틴아메리카에서는 브라질이 오랜 세월 축적해온 PCV10의 증거 기반을 활용하여 소득 4분의 1 이상의 층에서 유효함을 나타내며, 지역 전체의 입찰 갱신에 정보를 제공합니다.

The pneumococcal vaccines market is valued at USD 9.23 billion in 2025 and is forecast to reach USD 11.68 billion by 2030, reflecting a 4.82% CAGR.

Continued shifts from 7-, 10- and 13-valent formulations toward 15-, 20- and 21-valent conjugate vaccines, broader adult vaccination guidelines, and expanded rollouts in emerging economies anchor this steady growth trajectory. North America remains the primary revenue center, yet Asia-Pacific shows the strongest momentum as domestic manufacturers scale up output and governments integrate pneumococcal conjugate vaccines into routine schedules. Intensifying competition follows Merck's adult-specific Capvaxive launch , the European approval of PCV21 and Vaxcyte's well-funded 31-valent pipeline . Meanwhile, GAVI-driven procurement, declining dose prices and evolving cold-chain technologies widen access in resource-constrained regions. The entrance of serotype-independent, protein-based candidates forms a long-term disruptive undercurrent that could reset product differentiation, manufacturing footprints and pricing strategies.

Large-scale campaigns transform vaccination coverage by embedding pneumococcal conjugate vaccines into national schedules and securing multiyear procurement budgets. India's program now protects more than 90% of annual births, preventing an estimated 50,000 childhood deaths each year. Indonesia follows a similar path with 1.6 million doses financed through GAVI, underscoring the influence of public-private alliances on demand stability. The WHO Defeat Meningitis 2030 Roadmap aligns donor priorities toward at-risk displaced populations, while climate-driven disease spread compels portfolio reviews that favor thermostable presentations over traditional cold-chain-intensive formats. Persistent government advocacy, coupled with donor subsidies and tiered pricing, therefore sustains predictable order flow for producers across the pneumococcal vaccines market .

Despite decades of immunization progress, pneumococcal pneumonia and meningitis remain leading infectious killers of children under five and older adults. Outbreaks such as Togo's 2023 meningitis surge confirm lingering vulnerability in the Sub-Saharan meningitis belt. Adult coverage gaps are pronounced: only 13.4% of US adults aged 19-64 with chronic conditions are fully vaccinated, with state-level rates ranging from 0-34%. Hospitals in Hong Kong report less than one-third of eligible patients receiving a dose even after pneumococcal disease hospitalization. Alongside the emergence of antibiotic-resistant strains, these prevalence indicators reinforce the addressable burden underpinning growth in the pneumococcal vaccines market.

Prevnar 20's path to approval illustrates extended cycles: developers spent 1,434 days in testing phases and 244 days in formal review, stretching total time to 1,678 days. FDA requests for additional pediatric immunogenicity data on Vaxneuvance added further delays. As every additional serotype multiplies clinical workload, higher-valent programs face even longer and costlier pathways, which tempers near-term supply expansion in the pneumococcal vaccines market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Pneumococcal conjugate vaccines held 65.25% revenue share in 2024, driven by evidence of superior immune memory and the ongoing shift to higher-valent PCV15, PCV20 and PCV21. This dominant position translates into a proportional contribution to the pneumococcal vaccines market. In contrast, polysaccharide offerings attract attention for adult catch-up campaigns and cost-sensitive tenders, producing a 5.25% CAGR that outpaces the total market. Conjugate innovators continue to push valency boundaries, while polysaccharide producers emphasize scale efficiencies to maintain competitiveness. Emerging protein-based concepts that target conserved lipoproteins such as MalX and PrsA could eventually blur current categorizations by offering serotype-agnostic protection. Early animal data showing cross-serotype efficacy drives investment interest.

The pneumococcal vaccines market size for conjugate formulations is projected to climb in absolute terms even as polysaccharides accelerate. Conjugate value growth is underpinned by premium pricing, diverse tender volumes and uptake in high-income adult populations. Meanwhile, polysaccharide expansion is volume-led, with governments procuring cost-effective doses to close coverage gaps in older adults. Both approaches remain complementary, and many national guidelines recommend sequential administration of conjugate followed by polysaccharide strains to maximize serotype breadth and immune response durability.

Prevnar 13 captured 42.22% share of the pneumococcal vaccines market in 2024 thanks to long-standing clinical data, consistent supply and global regulatory recognition. Its successor, Prevnar 20, extends protection but still competes head-to-head with Merck's Capvaxive in adults and with Synflorix in low-income pediatric segments. Pneumovax 23, although an older polysaccharide product, benefits from strong physician familiarity and a lower dose price that attracts tender wins in middle-income economies, which explains its 5.48% CAGR. The "Others" cluster-including Capvaxive and potential 24- and 31-valent entrants-adds diversity and is likely to claim incremental share post-2027.

Multiple antigen presenting system candidates and synthetic glycoconjugate pipelines position newer firms to erode incumbent dominance over time. Yet brand equity, cold-chain networks and post-marketing safety surveillance infrastructure still reinforce incumbents' negotiating leverage during national procurements. Future competitive positioning will hinge on breadth of coverage, targeted adult or pediatric indications and total cost per fully immunized person rather than per-dose sticker price.

The Pneumococcal Vaccines Market is Segmented by Vaccine Type (Pneumococcal Conjugate Vaccine (PCV) and More), Product Type (Prevnar 13, Synflorix, and More), Distribution Channel (Government Authorities, Non-Government NGOs & Multilaterals, and More), Age Group (Adults, Geriatric, and More) and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

North America contributed 40.56% revenue in 2024 and continues to benefit from insurance coverage, pharmacist vaccination authority and corporate wellness uptake. The CDC age-threshold change instantly enlarged the eligible pool, and Capvaxive's adult-specific positioning drives brand-switching campaigns. Provincial programs in Canada align with US guidelines, and Mexico taps Pan American Health Organization revolving funds to co-finance PCV20 for adults at risk. Nevertheless, socio-economic disparities persist, with rural states recording adult coverage rates below 45%.

Asia-Pacific is projected to post a 5.65% CAGR to 2030, the fastest among all regions. India's nationwide roll-out supplies more than 30 million doses annually, powered by domestic low-cost production under the PNEUMOSIL brand. China's expansion of combination vaccine reimbursement, plus Singapore's pioneering PCV20 uptake, confirm rising middle-class demand for premium conjugates. Indonesia's 4.5 million-child target illustrates momentum among populous Association of Southeast Asian Nations (ASEAN) members. Local strain profiling influences product strategies, with region-specific serotypes like 1, 5 and 10A shaping national tenders.

Europe maintains moderate single-digit growth as the European Commission's May 2025 approval of Capvaxive boosts adult coverage campaigns across Germany, Italy and France. Widespread surveillance capacity helps policymakers refine schedules promptly when replacement trends emerge. In the Middle East and Africa, GAVI funding remains the principal catalyst, complemented by innovative solar cold-chain projects such as South Sudan's withstanding 40 °C daytime temperatures. Latin America leverages Brazil's long-standing PCV10 evidence base, showing efficacy across income quartiles and informing tender renewals throughout the region.