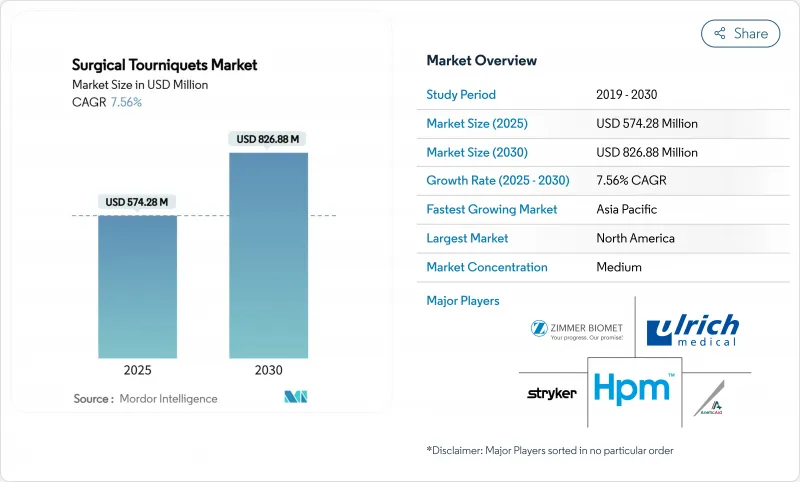

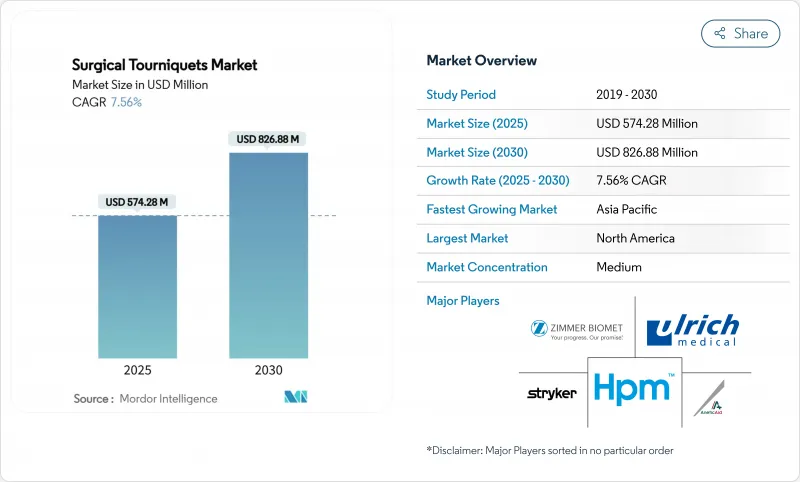

수술용 지혈대 시장은 2025년에 5억 7,428만 달러를 창출하고 2030년에는 8억 2,688만 달러에 이를 전망입니다.

이 기세는 교통사고와 관련된 외상 사례 증가, 군의료부대의 지속적인 근대화, 수술 중 신경손상 발생률을 저하시키는 사지폐쇄압박(LOP) 기술의 급속한 보급이라는 3가지 힘이 교차하고 있기 때문입니다. 분쟁시의 데이터로 전투 시나리오에서의 성공률이 57.1%인 것이 증명되었기 때문에 응급 의료 서비스는 현재, 병원전의 프로토콜에 지혈대의 배치를 짜넣고 있습니다. 또한 감염관리의 의무화에 의해 일회용 커프 수요가 높아진 것과 압박압 조정을 자동화하는 콘솔 기반 시스템에 의해 병원이나 외래 수술 센터 소송위험이 경감된 것도 시장 침투의 요인이 되고 있습니다.

러시아 우크라이나 분쟁으로 대표되는 군사적 사상자 데이터는 지혈대의 유효성을 입증하고 민간 응급의료 도입에 박차를 가했습니다. 현장 연구에 따르면 대량 사상자의 지혈대 장착 시간은 2분 이내이며, 이 능력은 세계 응급 구명사의 커리큘럼에 통합되고 있습니다. 전투용 지혈대는 의복 위에서 착용하더라도 항상 뛰어난 동맥 폐색을 달성하고 보호복을 착용한 구급대원에게 중요한 이점이 됩니다. 시민에 대한 보급은 STOP THE BLEED 캠페인을 통해 가속화되고 있으며, 텍사스의 구급대는 2025년에 비압축성 출혈 제어를 위한 복부 대동맥 접합기구를 배치했습니다. 4,095건의 민간 외상 사례에서 병원 앞에서 지혈대를 사용하면 절단 위험이 높지 않지만 사망률이 52% 감소하는 것으로 입증되었습니다. 이러한 분야 횡단적인 기세는 수술용 지혈대 시장을 수술실뿐만 아니라 병원 전 의료로까지 넓히고 있습니다.

인도의 민간 병원 네트워크만으로도 2025년도에는 2,500층까지 증상하여 관절 치환술의 증례 수를 증가시키는 11-12%의 증수를 전망하고 있습니다. 인구동태의 고령화와 보험 적용 범위의 확대가 수술 건수 증가를 지지하는 한편, 의료 투어리즘은 아시아태평양 전역의 병원의 톱 라인의 10-12%에 공헌하고 있습니다. 연구 데이터에 따르면, 인공 슬관절 전치환술에서 지혈대의 사용은 수술 중 출혈량을 감소시키지만 수술 후 타박상을 약간 증가시키는 것으로 나타났습니다. 실리콘 링의 디자인은 수술 분야를 넓힐 수 있다는 점에서도 호평을 받고 있으며, 이는 두 무릎 수술에서 장점이 됩니다.

메타 분석에 따르면 ACL 재건술 중에 지혈대를 사용하면 수술 후 배액량이 100ml 증가하고 단기 통증이 증가하므로 과오 소송에서 원고의 주장이 선명해집니다. 전신 마취 하에서의 인플레이션은 심장주기의 효율을 현저하게 감소시키고, 수술기의 위험 요인을 추가합니다. 보험 회사는 현재 압력 피드백 콘솔의 병원 채용률에 대한 보험료를 설정하고 있습니다. 법적 판례는 시설이 압력의 지속 시간을 기록하도록 의무화되고 자동 감사 추적을 가진 장비를 조달하도록 촉구하고 있습니다. 병원이 수술용 지혈대 시장의 책임을 헤지하기 위해 연장 보증과 보상 조항을 번들하는 공급업체가 우위를 차지하고 있습니다.

2024년 수술용 지혈대 시장의 54.28%는 공압식 장치가 차지했는데, 이는 신뢰할 수 있는 팽창 제어와 외과의사의 선호의 확립 때문입니다. 그러나 일회용 멸균 커프는 감염 제어 지침이 수술실을 일회용품으로 향하게 하기 때문에 CAGR 8.78%를 나타낼 전망입니다. 재사용 커프는 현재 교차 오염 사건을 추적하는 성능 감사에 직면하고 있으며 이동을 가속화하고 있습니다.

유행 대책이 의무화되고 있는 동안 일회용 커프로 이행한 병원에서는 멸균 인건비가 27% 감소한 것으로 보고되었습니다. 동시에 RFID가 내장된 지능형 커프는 스마트팜프와의 자동 페어링을 용이하게 하고 개별 환자에게 적합한 압력의 정확한 로그를 보장합니다. 방수 드레이프의 기술 혁신으로 무릎 관절경 검사에서 피부 화상이 더욱 감소하고 환자 만족도가 향상되고 도입이 가속화되고 있습니다.

2024년 수술용 지혈대 시장 규모에서는 하지정형외과가 62.84%를 차지하며 무릎관절치환술과 고관절치환술의 지속적인 성장에 지지되었습니다. 하지만 외상·전장 의료가 CAGR 9.18%로 가장 높습니다. 이것은 사지 출혈 후 2분 이내에 지혈대를 사용하기로 결정한 새로운 군용 필드 키트와 응급 의료 프로토콜 덕분입니다.

전투 피해자의 조사는 골반 출혈을 위한 접합형 복부 장치 등의 설계 개량에 불을 붙여 적응 범위를 넓혔습니다. 동시에, 손목 재건술과 미세혈관 플랩 절차에 의한 상지 수요는 안정적이며, 성형 외과의사는 압력을 높이지 않고 절개의 가시성을 확대하는 실리콘 링 시스템을 채용하고 있습니다.

수술용 지혈대 시장은 제품 유형별(공기식 지혈대 시스템, 지능형 LOP 제어 시스템, 기타), 용도별(하지 정형외과, 상지 정형외과, 기타), 최종 사용자별(병원 및 외상 센터, 외래 수술 센터(ASC), 기타), 기술별(단일 채널(1 커프) 콘솔, 기타), 지역별(북미, 유럽)

북미의 2024년 점유율 47.52%는 선진 외상 시스템, 국방 조달, FDA 510(k) 신속 심사 등 조기 승인 경로에 의한 것이지만, 일부 정형외과 센터에서는 지혈대 없는 프로토콜로의 이행도 시작되었습니다. 따라서 지역 매출은 소송을 경계하는 외과의사를 안심시키는 적응 압력 곡선을 가진 콘솔에 기울어집니다. 텍사스의 구급대가 비압축성 출혈에 접합형 지혈대를 채택한 것은 병원 전 틈새 분야에서의 지속적인 성장을 뒷받침합니다. 스트라이커가 49억 달러의 Inari Medical 사 인수로 대표되는 기업 통합은 출혈 제어 기술의 논리적 인접 영역인 혈전 절제술에 경쟁의 폭을 넓히고 있습니다.

아시아태평양의 CAGR은 9.69%로 가장 빠르며 인도 병원 네트워크에서 17억 5,000만 달러의 병상 증가 설계화와 ASEAN 전역에서 기기 승인을 용이하게 하는 규제의 조화가 그 원동력이 되고 있습니다. 의료 투어리즘의 유입이 치료 건수를 밀어 올려, 167개국의 전자 의료 비자 등 정부의 이니셔티브가 한층 더 액세스를 확대합니다. 인도의 Make-in-India의 틀은 현지 조달을 촉구하고, 다국적 기업은 합작 사업의 설립을 강요당하거나 시장 점유율 저하의 리스크를 부담하게 됩니다.

유럽에서는 의료기기 규정이 강화되어 고급 LOP 콘솔에 대한 선호도가 높아지고 있습니다. 울리히 메디컬은 2024년 500만 유로를 생산 규모 확대에 충당해 매출액은 12% 증가한 1억 5,000만 유로가 되었습니다. 중동 및 아프리카는 석유수입을 외상센터 업그레이드로 향하고 있으며, 남미 민간병원그룹은 거시경제의 변동이 여전히 역풍인 것, 스마트콘솔 도입을 조심스럽게 단계적으로 진행하고 있습니다. 이러한 역학을 종합하면, 벤더는 민첩한 채널 전략을 구사해, 수술용 지혈대 시장에서 점유율을 획득해야 하는 성장 포켓을 분산시켜 가게 됩니다.

The surgical tourniquets market generated USD 574.28 million in 2025 and is on track to reach USD 826.88 million by 2030, reflecting a 7.56% CAGR through the forecast window.

Momentum stems from three intersecting forces: rising trauma caseloads linked to road accidents, sustained modernization of military medical corps, and quick uptake of limb-occlusion-pressure (LOP) technology that lowers the incidence of nerve injury during surgery. Emergency medical services now integrate tourniquet deployment into pre-hospital protocols after conflict data proved a 57.1% success rate in combat scenarios. Market penetration also benefits from infection-control mandates that heighten demand for single-use cuffs and from console-based systems that automate pressure adjustment, reducing litigation exposure for hospitals and ambulatory surgery centers.

Military casualty data, notably from the Russia-Ukraine conflict, validated tourniquet efficacy and spurred civilian EMS adoption. Field studies show mass-casualty tourniquet placement times under two minutes, a capability increasingly embedded in paramedic curricula worldwide. The Combat Application Tourniquet consistently achieves superior arterial occlusion when applied over clothing, a critical advantage for first responders wearing protective gear. Civilian uptake accelerates via STOP THE BLEED campaigns, and county EMS agencies in Texas deployed abdominal aortic junctional devices in 2025 for non-compressible hemorrhage control. Evidence across 4,095 civilian trauma cases shows a 52% mortality reduction without higher amputation risk when tourniquets are used pre-hospital. This cross-sector momentum widens the surgical tourniquets market beyond operating rooms into pre-hospital care.

Private hospital networks in India alone are adding up to 2,500 beds in fiscal 2025, with 11-12% revenue growth that lifts joint-replacement caseloads. Aging demographics and broader insurance coverage support higher procedure volumes, while medical tourism now contributes 10-12% of hospital top lines across Asia-Pacific. Study data reveal that tourniquet use in total knee arthroplasty cuts intraoperative blood loss but slightly increases postoperative bruising.Consequently, surgeons gravitate to pressure-feedback consoles that calibrate inflation to LOP readings, mitigating tissue-related complications. Silicone ring designs also gain favor because they extend surgical fields, a benefit in bilateral knee work.

Meta-analyses show tourniquet use during ACL reconstruction elevates postoperative drainage by 100 ml and increases short-term pain, sharpening plaintiff arguments in malpractice suits. Cardiac-cycle efficiency drops markedly during inflation under general anesthesia, adding peri-operative risk factors. Insurers are now pricing premiums against hospital adoption rates of pressure-feedback consoles. Legal precedents increasingly oblige facilities to log pressure duration, prompting procurement of devices with automated audit trails. Vendors that bundle extended warranties and indemnification clauses gain an edge as hospitals hedge liability in the surgical tourniquets market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Pneumatic devices controlled 54.28% of the surgical tourniquets market in 2024 owing to reliable inflation control and established surgeon preference. Disposable sterile cuffs, however, are growing at an 8.78% CAGR as infection-control guidelines push operating rooms toward single-use supplies. Re-usable cuffs now face performance audits that track cross-contamination events, amplifying the shift.

Hospitals that migrated to single-use cuffs during pandemic conservation mandates report 27% lower sterilization labor cost. Simultaneously, intelligent cuffs embedded with RFID facilitate automatic pairing with smart pumps, ensuring pressure accuracy logs match individual patients. Waterproof drape innovations further reduce skin burns in knee arthroscopy, improving patient satisfaction and accelerating adoption.

Lower-limb orthopedic surgery accounted for 62.84% of the surgical tourniquets market size in 2024, supported by sustained growth in knee and hip replacements. Nonetheless, trauma and battlefield care registers the highest CAGR at 9.18%, thanks to new military field kits and EMS protocols that stipulate tourniquet use within two minutes of extremity hemorrhage.

Combat casualty research sparked design improvements such as junctional abdominal devices for pelvic bleeding, broadening indication scope. Concurrently, upper-limb demand remains stable through wrist reconstruction and micro-vascular flap procedures, while plastic surgeons adopt silicone ring systems to expand incision visibility without raising pressure.

The Surgical Tourniquets Market is Segmented by Product Type (Pneumatic Tourniquet Systems, Intelligent LOP-Controlled Systems, and More), by Application (Lower-Limb Orthopedic Surgery, Upper-Limb Orthopedic Surgery, and More), by End User (Hospitals and Trauma Centers, Ambulatory Surgery Centers, and More), by Technology (Single-Channel (1-Cuff) Consoles, and More) and Geography (North America, Europe, Asia-Pacific, and More).

North America's 47.52% share in 2024 rests on advanced trauma systems, defense procurement, and early approval pathways such as FDA 510(k) expedited reviews, but it also sees a nascent shift toward tourniquet-less protocols in select orthopedic centers. Regional sales therefore tilt toward consoles with adaptive pressure curves that reassure surgeons wary of litigation. Texas county EMS adoption of junctional tourniquets for non-compressible bleeds underscores continuing growth in pre-hospital niches. Corporate consolidation, illustrated by Stryker's USD 4.9 billion Inari Medical purchase, extends competitive breadth into thrombectomy-a logical adjacency to bleeding-control technologies.

Asia-Pacific records the fastest CAGR at 9.69%, fueled by USD 1.75 billion bed-expansion programs across Indian hospital networks and by regulatory harmonization that eases device approvals across ASEAN. Medical-tourism inflows fortify procedure volumes, while government initiatives such as e-medical visas for 167 countries further widen access. Domestic manufacturing drives price competition; India's Make-in-India framework encourages local sourcing, which presses multinationals to establish joint ventures or risk market share erosion.

Europe maintains steady uptake under cohesive medical-device regulations and growing preference for premium LOP consoles. Ulrich medical allocated EUR 5 million in 2024 to scale production, reporting a 12% revenue uplift to EUR 150 million-evidence that medium-sized players can prosper in specialized niches. Middle East and Africa funnel petro-revenues into trauma-center upgrades, and South America's private-hospital groups cautiously phase in smart consoles, though macroeconomic volatility remains a headwind. Collectively, these dynamics distribute growth pockets that vendors must navigate with agile channel strategies to capture share in the surgical tourniquets market.