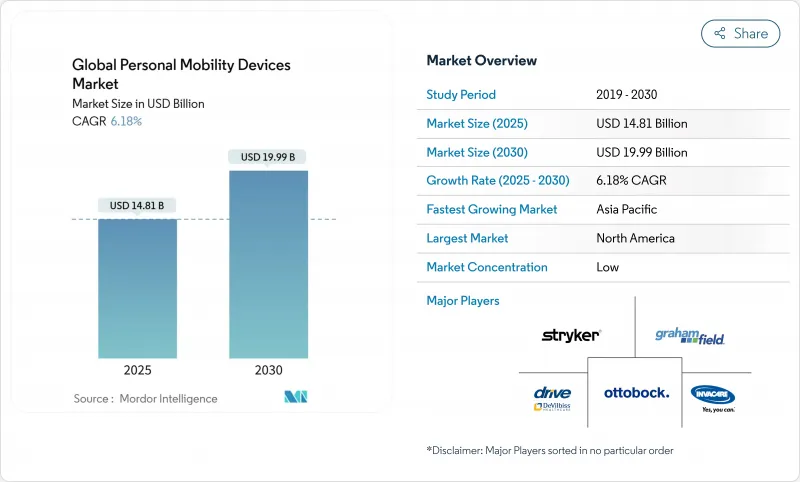

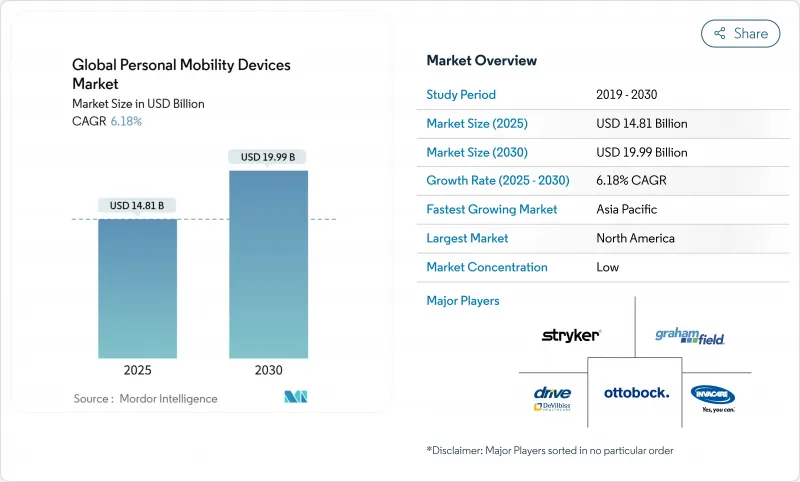

퍼스널 모빌리티 디바이스 시장은 2025년에 148억 1,000만 달러, 2030년에는 199억 9,000만 달러에 이르며 CAGR 6.18%를 나타낼 것으로 예측됩니다.

재택 간호 환불이 확대되고 AI 구동 휠체어가 주류 가격 수준에 도달하고 배터리 밀도 향상으로 전동기기 사용 범위가 넓어짐에 따라 수요가 가속화됩니다. 휠체어는 계속 판매 대수의 기간이 되는 한편, 옥외에서의 자립을 바라는 고령자 사이에서는 모빌리티 스쿠터의 인기가 높아집니다. 수동 장비는 여전히 전기 장비를 능가하지만, 파워 어시스트 기술은 가격 차이를 줄이고 첫 구매자를 유혹합니다. 북미는 보험 적용 규칙이 수립되어 주도권을 유지하고 있지만 아시아태평양의 노인 인구가 증가하고 소비자의 소비력이 높아짐에 따라 퍼스널 모빌리티 디바이스 시장이 가장 급성장하고 있습니다.

메디케어의 2025년 재택치료 긍정적 지급 제도에서는 현재 승인된 이동기구 비용의 80%가 환불되어 지역 기반 케어 목표에 따른 보험 적용이 이루어지고 있습니다. 미국의 민간 보험 회사는 이 메커니즘을 반영하여 상업 계획 간의 연속성을 보장합니다. 간소화된 원격 의료 평가는 관리 마찰을 더욱 완화시켜 구매 의사 결정이 장애인 여행의 초기 단계에서 이루어졌습니다. 유럽의 지불자는 재택 적응 예산에 개인용 이동기구를 추가하는 등 병행하여 조정을 진행하고 있습니다. 보험 상환이 아시아태평양으로 확산됨에 따라 자립 생활 도구를 구입하는 것은 노후 생활 설계에 필수적입니다.

WHILL의 자율 주행 휠체어는 이미 미국의 주요 공항에서 여행자를 탑재하고 있으며, 라이더, 심도 카메라, 드라이브 바이 와이어 시스템이 안전과 비용 목표를 달성하고 있음을 입증했습니다. 일본의 간병 시설에서도, 직원의 부담을 경감하기 위해서 같은 차량이 도입되고 있습니다. 부품 가격이 낮아짐에 따라 중견 제조업체는 처음부터 내비게이션 스택을 빌드하는 대신 라이선스를 부여했습니다. 보험 회사는 인간의 동행이 필요하지 않은 자율 주행 옵션을 다루기 시작하여 데이터 수집 및 보험 수리적 검증의 선순환을 제안합니다.

미국에서 수혜자는 승인된 장비의 20%를 지불하지만, 이는 사회보장비의 몇 달에 해당합니다. 라틴아메리카와 동남아시아의 일부에서는 국가 보험 제도가 내구 의료기기를 제외하고 있기 때문에 보험 적용 격차는 더 큽니다. 민간 보험 회사는 임상 검증을 요구하고 가계를 초과하는 지출을 강요하는 평가 비용을 추가합니다. 시골 지역의 환자는 피팅 세션에 대한 여비가 더해지기 때문에 도시와 원격지 주민 간의 불공평감이 커지고 있습니다.

휠체어는 2024년 매출의 45.21%를 차지하여 퍼스널 모빌리티 디바이스 시장에서 기본적인 역할을 명확히 했습니다. 수동 유형은 여전히 병원 및 예산에 제약을 받은 구매자의 첫 번째 선택이며, 전기 모델은 장거리에서 자립을 요구하는 사용자에게 호소하고 있습니다. WHILL의 조이스틱이 필요없는 미드 휠 플랫폼은 직관적인 조작에 중점을 둔 디자인을 상징합니다. 모빌리티 스쿠터는 2030년까지의 CAGR 예측이 6.66%로 쇼핑이나 레저에 안정적인 옥외 솔루션을 필요로 하는 정년 퇴직자에게 뒷받침되고 있습니다. 계단 승강기와 플랫폼 승강기는 가정에서 수직 접근을 실현하고, 노인 거주자를 위해 다층 주택이 개조됨에 따라 점유율을 확대합니다. 경쟁의 중심은 단순한 속도 사양보다 기성 개념에 얽매이지 않는 연결성, 좌석의 인체 공학, 운송성입니다.

성장의 원동력은 하위 부문에 따라 다릅니다. 수동 의자의 판매는 일관된 상환 제도와 신흥 경제 지역에서 두 번째 유닛을 배치하는 리노베이션 프로그램에 의존합니다. 전동 의자 수요는 토크를 희생하지 않고 경량화를 실현하는 배터리의 획기적인 진보를 쫓고 있습니다. 스쿠터는 OECD 회원국의 많은 도시에서 보도 규제가 자유화된 혜택을 받고 있습니다. 리프트의 설치는 다층 거주 공간을 목표로 하는 부동산 동향과 상관됩니다. 모듈형 플랫폼을 통해 각 틈새 시장에 해당하는 제조업체는 액세서리를 교차 셀링하여 서비스 수입을 보장할 수 있습니다.

수동 설계는 저렴한 가격, 간단한 유지보수 및 보편적인 보험인지로 2024년 50.45%의 시장 점유율을 차지했습니다. 경량 알루미늄 프레임과 퀵 릴리스 휠은 활성 사용자에게 이 카테고리의 경쟁력을 유지합니다. 그러나 전동 시스템은 배터리의 고밀도화와 전자 기기의 비용 하락을 배경으로 CAGR 6.54%를 나타낼 것으로 예상됩니다. 선라이즈 메디컬의 엠펄스와 같은 파워 어시스트 키트는 표준 의자를 하이브리드로 변신시켜 완전 전동화를 주저하는 소비자에게 다리를 합니다. 코발트를 사용하지 않는 리튬 이온 화학의 조사는 재료 위험의 감소와 사이클 수명의 연장을 약속합니다.

미래의 디자인 언어는 에너지 수확 허브, 스마트폰 기반 컨트롤, 무선 진단을 융합시킵니다. 무게와 가격이 수렴함에 따라 보험 회사는 결국 드라이브 시스템이 아닌 기능성으로 급여 수준을 평가할 수 있습니다. 원격 모니터링을 위한 개방형 API를 통합하는 공급업체는 기기 획득뿐만 아니라 모빌리티 결과에 따라 환불을 받는 가치 기반 관리 계약을 향해 스스로를 자리잡고 있습니다.

메디케어의 적용 범위와 ADA 규제가 공급업체에게 예측 가능한 볼륨을 창출했기 때문에 2024년 점유율은 북미가 38.68%로 최고가 되었습니다. 퍼스널 모빌리티 시장은 활동적인 라이프 스타일을 선호하는 아기 부머의 노화로 이익을 얻고 있습니다. 로스앤젤레스 국제 공항과 마이애미 국제 공항에서 자율 주행 의자의 시험 운영은 조기 도입 의욕을 돋보이게합니다. 캐나다는 주의 장비 대여 프로그램을 통해 성장을 지원하고 멕시코는 공적 보험 제도를 확충하고 있지만, 가격에 대한 감응도는 남반구쪽이 높습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 6.82%로 가장 빠를 것으로 전망됩니다. 중국의 중산계급은 교외 이동을 위해 전동 스쿠터를 구입하고 일본은 간병인 부족에 대처하기 위해 로봇 의자를 개척합니다. 인도에서는 관민 파트너십에 의해 저가격의 수동식 의자가 전국에 보급되지만, 대도시권의 병원에서는 고급품 수요가 높아집니다. 정부 주도로 국내 배터리 셀 공장에 자금이 공급되어 수입 의존도의 삭감과 퍼스널 모빌리티 디바이스 시장공급망의 안정화를 목표로 합니다. 동남아시아 국가가 의료기기의 수입관세를 개정하고 세계 브랜드 시장 접근이 확대됩니다.

유럽은 규모가 크지만 성장은 둔화되고 있습니다. 국민 모두 보험제도에 의해 대부분의 이동보조기구가 환불되지만, 정비가 끝난 기구는 교체 사이클을 길게 합니다. 유럽 위원회의 2024년 소형 전기자동차 기준 지침은 국경을 넘어 제품 인증의 조화를 도모하고 EU 전역에서의 유통을 용이하게 했습니다. 중동 및 아프리카에서는 병원 건설 붐과 걸프 협력 회의 회원국에서 새롭게 도입된 강제 의료 보험과 관련하여 초기 단계의 도입을 볼 수 있습니다. 남미에서는 브라질이 간병급여를 확대하고 아르헨티나가 국내 휠체어 생산에 보조금을 내는 등 꾸준히 진전하고 있습니다.

The personal mobility devices market is valued at USD 14.81 billion in 2025 and is projected to touch USD 19.99 billion by 2030, advancing at a 6.18% CAGR.

Demand accelerates as home-care reimbursement expands, AI-driven wheelchairs reach mainstream price levels, and battery density improvements extend powered-device range. Wheelchairs remain the volume backbone, while mobility scooters gain traction among seniors who want independence outdoors. Manual devices still outsell powered units, yet power-assist technologies narrow the affordability gap and tempt first-time buyers. North America retains leadership thanks to established coverage rules, but the personal mobility devices market in Asia-Pacific grows fastest as its elderly population swells and consumer spending power rises.

Medicare's 2025 Home Health Prospective Payment System now reimburses 80% of approved mobility device costs, aligning coverage with community-based care goals. U.S. private insurers mirror this structure, guaranteeing continuity across commercial plans. Streamlined telehealth evaluations further reduce administrative friction, which brings purchasing decisions earlier in the disability journey. European payers adjust in parallel, adding personal mobility devices to home-adaptation budgets. As reimbursement spreads across Asia-Pacific, independent living purchases become integral to retirement planning.

WHILL's autonomous chairs already ferry travelers across major U.S. airports, proving that lidar, depth cameras, and drive-by-wire systems meet safety and cost targets. Japanese nursing homes deploy similar fleets to ease staff workloads. Component price declines invite midsize manufacturers to license navigation stacks rather than build them from scratch. Insurers have begun covering autonomous options when they remove the need for human attendants, suggesting a virtuous cycle of data collection and actuarial validation.

In the United States a beneficiary still pays 20% of an approved device, which may equate to several months of Social Security income. Coverage gaps are wider in Latin America and parts of Southeast Asia where national plans exclude durable medical equipment. Private insurers demand clinical validation, adding evaluation charges that push total expense beyond household budgets. Rural patients face added travel costs for fitting sessions, reinforcing inequity between urban and remote populations.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Wheelchairs captured 45.21% of 2024 revenue, underscoring their foundational role in the personal mobility devices market. Manual variants remain the first choice for hospitals and budget-constrained buyers, while powered models appeal to users seeking independence over longer distances. WHILL's joystick-free mid-wheel platform exemplifies a design pivot toward intuitive control. Mobility scooters follow with a 6.66% CAGR forecast to 2030, fueled by retirees who need a stable outdoor solution for shopping and leisure. Stair and platform lifts create household vertical access, gaining share as multi-story homes retrofit for aging residents. Competition now centers on out-of-box connectivity, seat ergonomics, and transportability rather than simple speed specifications.

Growth drivers vary by sub-segment. Manual chair sales rely on consistent reimbursement and refurbishment programs that place second-life units in emerging economies. Powered chair demand tracks battery breakthroughs that reduce weight without sacrificing torque. Scooters benefit from liberalized sidewalk rules in many OECD cities. Lift installations correlate with real-estate trends toward multi-level living spaces. Manufacturers that serve each niche through modular platforms can cross-sell accessories and lock in service revenue.

Manual designs held 50.45% market share in 2024 due to low price, simple maintenance, and universal insurance recognition. Lightweight aluminum frames and quick-release wheels keep the category competitive for active users. Powered systems, however, should grow at 6.54% CAGR on the back of denser batteries and falling electronics costs. Power-assist kits such as Sunrise Medical's Empulse line transform a standard chair into a hybrid, providing a bridge for consumers hesitant about full electrification. Research into cobalt-free lithium-ion chemistries promises lower materials risk and extended cycle life.

Future design language blends energy-harvesting hubs, smartphone-based controls, and over-the-air diagnostics. As weight and price converge, insurers may eventually grade benefit levels on functionality rather than drive system. Suppliers who integrate open APIs for remote monitoring position themselves for value-based care contracts that reimburse on mobility outcomes rather than device acquisition alone.

The Personal Mobility Devices Market is Segmented by Product (Wheelchair[Manual Wheelchairs, Powered Wheelchairs, and More], Walking Aids, and More), Technology(manual, Powered, and More), End User (Hospitals and Clinics, Home Care Settings, and More), Distribution Channel(Offline and E-Commerce) and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led with 38.68% share in 2024 as Medicare coverage and ADA regulations created predictable volumes for suppliers. The personal mobility devices market benefits from an aging Baby Boomer cohort that prioritizes active lifestyles. Autonomous chair pilots at Los Angeles International Airport and Miami International Airport highlight early adoption appetite. Canada supports growth via provincial equipment loan programs, and Mexico expands public-insurance formularies, though price sensitivity is greater south of the border.

Asia-Pacific delivers the fastest CAGR at 6.82% through 2030. China's middle class purchases powered scooters for suburban travel, while Japan pioneers robotic chairs to cope with caregiver shortages. India's public-private partnerships scale low-cost manual chairs nationwide, yet premium demand rises in metro hospitals. Government initiatives fund domestic battery cell factories, aiming to cut import dependency and stabilize the personal mobility devices market supply chain. Southeast Asian nations revise import tariffs on medical devices, broadening market access for global brands.

Europe holds a sizeable yet slower-growing base. Universal healthcare plans reimburse most mobility aids, but refurbished equipment prolongs replacement cycles. The European Commission's 2024 guidance on light electric vehicle standards harmonizes cross-border product certification, easing pan-EU distribution. Middle East and Africa show early-stage adoption tied to hospital construction booms and newly introduced mandatory health insurance in Gulf Cooperation Council states. South America progresses steadily as Brazil expands long-term care benefits and Argentina subsidizes domestic wheelchair production.