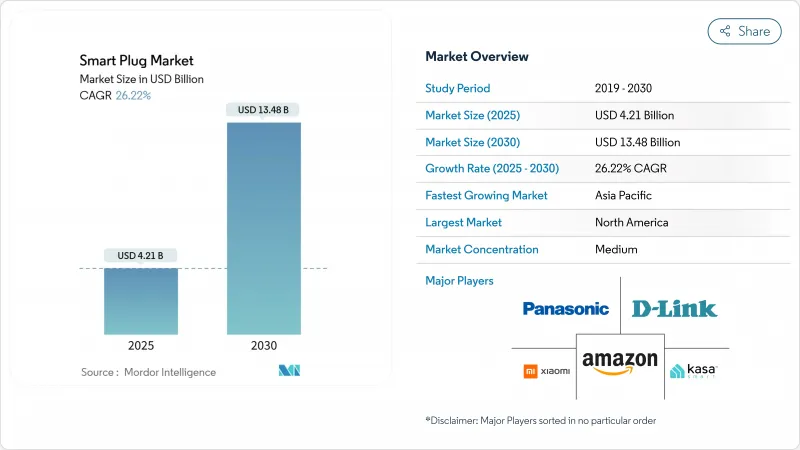

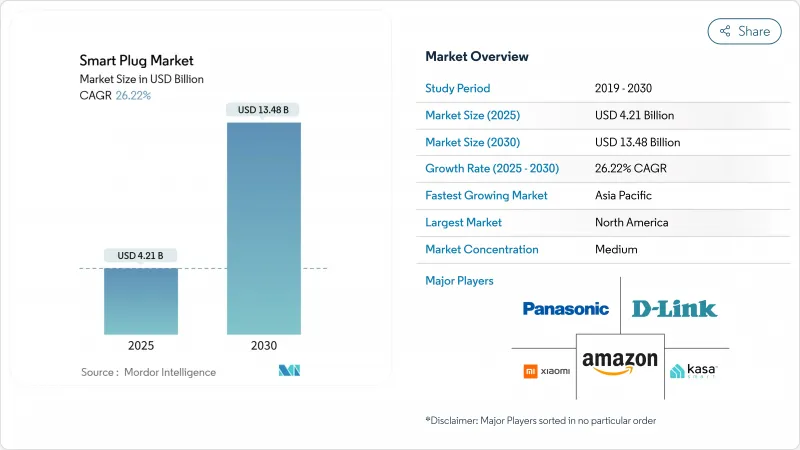

스마트 플러그 시장은 2025년에 42억 1,000만 달러, 2030년에는 134억 8,000만 달러에 이르며, CAGR 26.22%를 나타낼 전망입니다.

이 가속은 플러그 로드 제어를 건축 기준법의 정평으로 하는 에너지 효율 규칙의 의무화, 10달러 이하의 소매 태그를 실현하는 Wi-Fi 칩셋 가격의 급속한 하락, 오랜 생태계의 세로할당을 해소하는 Matter 1.3 상호 운용성 규격에 기인합니다. 또한 초저전력 Wi-Fi 6 MCU는 대기 중 소비 전력을 마이크로암페어 레벨로 줄여 수년간의 배터리 사용을 가능하게 합니다. 시설당 연간 최대 36.8kW의 플러그 부하 낭비를 보여주는 감사에 힘입어 산업계의 관심이 높아짐에 따라 스마트 플러그는 최전선의 효율화 개수로 자리매김하고 있습니다. 아시아태평양은 Alexa 장치의 연결이 인도에서 3배로 증가하여 현지 칩셋 공급업체가 국내 브랜드의 재료비를 절감하고 있습니다.

아마존의 보고에 따르면 인도에서는 3년 이내에 연결된 스마트 홈 기기가 200% 급증합니다. Prime에 번들로 제공되는월19.99달러의 Alexa 생성형 AI 서비스의 2025년 데뷔는 간단한 온/오프 스위칭에서 멀티 디바이스 장면 오케스트레이션에 대한 가치 제안을 재정의합니다. 구독의 경제성은 더 깊은 참여를 촉진하고 스마트 플러그를 레거시 가전 기기로 음성 보조자의 범위를 확장하는 기본 노드로 자리 매김합니다. Alexa의 카탈로그에는 14만대 이상의 대응 디바이스가 게재되고 있어, 네트워크 효과에 의해 도입의 마찰이 경감되어, 소득대를 불문하고 장착율이 상승합니다. 구글이나 애플도 비슷한 전략을 취하고 있으며, 음성 대응 컨트롤은 이제 모든 새로운 플러그인 기기에 기대되는 기본적인 것이라는 인식이 강해지고 있습니다.

Silicon Labs의 SiWx917 MCU는 커넥티드 슬립 전류를 22마이크로 암페어로 줄이고 부품 비용을 줄이고 에너지 보고 기능을 희생하지 않고도 15달러 이하의 소매 가격을 가능하게 합니다. 시냅틱스와 중국의 신참 AIC 마이크로는 32억 달러의 초저전력 IoT SoC 분야에 진출해 가격 경쟁을 격화시키고 공급업체의 선택을 넓히고 있습니다. 대량 생산을 통해 ODM은 Matter 호환 펌웨어를 유지하면서 Wi-Fi/BLE 듀얼 모듈을 컴팩트한 케이스에 패키징할 수 있습니다. 신흥국이 가장 혜택을 받는 것은 유닛의 경제성이 중간소득층의 가계와 일치하게 되어, 얼리어댑터 이외의 인스톨 베이스가 확대하기 때문입니다.

스마트 디바이스의 사이버 공격은 2024년에 두 배 이상으로 증가했으며 주요 브랜드에서 심각한 결함이 표면화되어 소비자의 신뢰가 손상되었습니다. TP-Link를 통한 로컬 통신 취약성 노출과 27억 건의 IoT 기록이 유출된 Mars Hydro 사건은 시스템 위험을 부각시키고 있습니다. 미국 FCC는 아마존과 구글의 지원을 받아 사이버 트러스트 마크를 제정할 예정이며 보다 명확한 표시를 약속하고 있지만 최종 규칙은 아직 시행되지 않았습니다. 엠포리아 에너지가 충격의 위험성을 이유로 스마트 플러그 8만개를 회수한 것 같은 제품 리콜은 불충분한 보안 관리에 의한 금전적 손해를 이야기하고 있습니다. 인증 제도가 의무화되기 전까지는 의심이 남아 있기 때문에 특히 IT 정책이 엄격한 전문가 관리 시설에서는 최초 구매가 지연될 수 있습니다.

2024년 스마트 플러그 시장 점유율은 Bluetooth가 31.7%로 최대를 유지했지만, Zigbee/Thread 프로토콜은 Matter 인증의 기세를 배경으로 CAGR 26.8%로 가속하고 있습니다. 스레드 지원 모델의 스마트 플러그 시장 규모는 스레드 1.4에서 강화된 자격 증명 공유를 통해 엔터프라이즈급 배포가 가능하므로 급격히 확대될 것으로 예측됩니다. Tuya의 15일간 턴키 모듈 프로그램은 표준화가 시장 출시 시간을 단축하고 엔지니어링 장애물을 낮추는 방법을 보여줍니다. Wi-Fi는 비용이 많이 드는 유비쿼터스를 즐기며 고해상도 에너지 계측과 같은 대역폭의 무거운 이용 사례가 뛰어나지만 Z-Wave는 미국의 레거시 보안 시스템에 정착한 채로 있습니다. 독자적인 스택은 소비자가 크로스 플랫폼에서 구매를 보장함으로써 다리를 모으기 때문에 진부화 될 위험이 있습니다.

Thread의 실시간 에너지 보고는 전력 회사 수요 반응에 명확한 이점을 제공합니다. Matter 1.3에서는 스마트 플러그가 순간적인 소비 데이터를 보다 광범위한 가정용 에너지 관리 대시보드에 공급할 수 있습니다. 그 결과 전력회사 리베이트는 Thread 대응 하드웨어에 집중하기 시작하여 설치업체에게 Wi-Fi 전용 SKU로부터의 탈퇴를 촉구하고 있습니다. Thread의 낮은 지연 메쉬 위에 에너지 분석을 오버레이하는 공급업체는 프리미엄 ASP를 청구할 수 있어 상품화하는 카테고리에서 마진의 감소를 완화할 수 있습니다.

2024년 스마트 플러그 시장 규모의 56.2%를 차지한 것은 주택이며 음성 어시스턴트 번들과 DIY의 편의성이 이를 뒷받침했습니다. 그러나 산업용 및 상업용 건물은 시설 관리자가 정량화된 수익을 추구하고 있기 때문에 CAGR 27.7%를 나타낼 것으로 예측됩니다. 현장 조사는 IoT 스케줄링이 적용되면 사이트당 연간 36.8kW의 플러그 로드를 절약할 수 있음을 보여줍니다. 하니웰의 엔터프라이즈 빌딩 관리 시스템용 플러그 로드 모듈은 데이터 중심의 에너지 컴플라이언스에 대한 축족을 보여줍니다.

공장과 창고에서는 스킨화된 산업 등급 스마트 플러그가 주택 유닛에 없는 열 과부하 보호와 과전류 분석을 추가합니다. 병원과 노인 간호 시설에서는 의료기기의 가동 시간을 확인하고, 계획 밖의 절단을 방지하기 위해 스마트 플러그가 도입되어, 고령화 사회에서의 원격 감시를 위한 보조금 제도가 뒷받침하고 있습니다. SLA에 뒷받침되는 하드웨어에 대한 상업적 의욕은 더 높은 가격대를 지원하고 전문 OEM에 대처할 수 있는 스마트 플러그 시장 전체를 확대합니다.

스마트 플러그 시장은 기술별(Bluetooth, Wi-Fi, 기타), 용도별(주택용, 상업용, 기타), 판매 채널별(온라인, 오프라인), 플러그 폼 팩터별(벽 콘센트 어댑터, 벽 내장 콘센트 등), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 에너지 스타 SHEMS 규칙과 광대역의 보급을 배경으로 2024년 32.1%의 리더를 유지했습니다. 이 지역의 음성 어시스턴트의 성숙한 보급은 생태계의 고정화를 촉진하고, 해지를 줄이고, 가정 전체의 개조를 촉진합니다. 캐나다의 에너지 효율 규제 갱신은 미국 기준을 반영한 것이며 제조업체에 통일된 북미 인증 로드맵을 제공합니다.

아시아태평양의 CAGR은 28.3%를 나타낼 것으로 예측되며 스마트 플러그 시장에서 가장 급성장하고 있는 지역이 되고 있습니다. 현지화된 음성 어시스턴트 방언 지원과 경쟁력 있는 가격 설정으로 2022년 이후 인도의 Alexa 장치 수가 3배로 증가했습니다. 중국의 국내 칩셋 생산은 BOM의 변동을 억제하고 화이트 라벨 브랜드의 보급을 가능하게 합니다. 일본과 한국에서는 정부 자금에 의한 스마트 시티의 시험 운용이 이루어지고, 플러그 레벨의 에너지 감시가 지구 전체의 탄소 대시보드에 통합되어 스레드 메쉬 도입에 대한 제도적 수요가 높아지고 있습니다.

유럽에서는 다양한 상황을 볼 수 있습니다. WEEE 지침 2024/884는 제조업체에 전폐 비용을 부과하고 이익률을 압박합니다. 반대로 영국의 2025년 스마트 가전 규칙에서는 그리드 인식 기능이 요구되고 있으며, Matter 대응 스마트 플러그를 개장함으로써 혜택을 받을 수 있는 기기의 풀이 넓어지고 있습니다. Tuya가 런던에서 개최한 레트로핏 포럼에서는 노후화된 주택 스톡의 넷 제로 목표를 달성하기 위해 저가 플러그가 수행하는 역할을 강조했습니다.

남미와 중동 및 아프리카는 설치 베이스에서는 지연을 취하고 있지만, 5G의 전개에 의해 레이턴시와 커버리지가 개선되어, 2자리 성장을 기록합니다. 높은 수입관세가 여전히 장애물이 되고 있으며, 지역의 자유무역구를 활용한 현지조립합작사업이 촉진되고 있습니다. 개발자들은 걸프 협력 회의의 호텔 체인을 활용하여 집중 에너지 대시보드를 시도했으며 스마트 플러그가 보다 광범위한 IoT 인프라의 게이트웨이 제품 역할을 한다는 것을 보여줍니다.

The smart plug market stands at USD 4.21 billion in 2025 and is on course to reach USD 13.48 billion in 2030, charting a 26.22% CAGR.

This acceleration stems from mandatory energy-efficiency rules that make plug-load controls a building-code staple, the rapid decline of Wi-Fi chipset prices that brings sub-USD 10 retail tags into play, and the Matter 1.3 interoperability standard that dissolves long-standing ecosystem silos. Voice-assistant ecosystems now anchor purchasing decisions, while ultra-low-power Wi-Fi 6 MCUs shrink standby draw to micro-amp levels and enable multi-year battery use. Rising industrial interest, driven by audits showing up to 36.8 kW in annual plug-load waste per facility, positions smart plugs as a frontline efficiency retrofit. Regional momentum tilts toward Asia Pacific, where Alexa device connections have tripled in India and local chipset suppliers cut bill-of-materials costs for domestic brands.

Voice control has shifted from novelty to necessity as Amazon reports a 200% jump in connected smart-home devices in India within three years. The 2025 debut of the USD 19.99-per-month Alexa+ generative-AI service, bundled into Prime, redefines the value proposition from simple on/off switching to multi-device scene orchestration. Subscription economics incentivize deeper engagement, positioning smart plugs as foundational nodes that extend voice-assistant reach to legacy appliances. With more than 140,000 compatible devices in the Alexa catalogue, network effects reduce adoption friction and lift attach rates across income bands. Comparable strategies from Google and Apple reinforce the perception that voice-ready control is now the baseline expectation for every new plug-in device.

Silicon Labs' SiWx917 MCU trims connected-sleep current to 22 micro amp, slicing component costs and enabling sub-USD 15 retail pricing without sacrificing energy reporting features. Synaptics and Chinese newcomer AIC Micro have entered the USD 3.2 billion ultra-low-power IoT SoC arena, intensifying price competition and widening vendor choice. Mass-market volumes allow ODMs to package dual Wi-Fi/BLE modules inside compact casings while retaining Matter-ready firmware. Emerging economies benefit most, as unit economics now align with middle-income household budgets, expanding the install base beyond early adopters.

Smart-device cyberattacks more than doubled in 2024, eroding consumer trust as high-profile flaws surfaced in major brands. TP-Link's exposure of local-communication vulnerabilities and the Mars Hydro incident that leaked 2.7 billion IoT records underscore systemic risk. The U.S. FCC's upcoming Cyber Trust Mark, backed by Amazon and Google, promises clearer labeling but final rules are not yet in force. Product recalls such as Emporia Energy's withdrawal of 80,000 smart plugs due to shock hazards illustrate the financial toll of insufficient security controls. Until certification regimes become mandatory, lingering doubts may slow first-time purchases, especially in professionally managed facilities with stricter IT policies.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Bluetooth retained the largest 31.7% slice of smart plug market share in 2024, but Zigbee/Thread protocols are accelerating at a 26.8% CAGR on the back of Matter certification momentum. The smart plug market size for Thread-enabled models is projected to swell sharply as enhanced credential-sharing in Thread 1.4 unlocks enterprise-grade deployments. Tuya's 15-day turnkey module program signals how standardization compresses time-to-market and lowers engineering hurdles. Wi-Fi enjoys cost-led ubiquity and excels in bandwidth-heavy use-cases such as high-resolution energy metering, while Z-Wave remains entrenched in legacy US security systems. Proprietary stacks risk obsolescence as consumers align around cross-platform purchase assurance.

Thread's real-time energy-reporting offers clear advantages in utility demand-response. Matter 1.3 now lets smart plugs feed instantaneous consumption data to broader home-energy-management dashboards. Consequently, utility rebates are beginning to single out Thread-capable hardware, incentivizing installers to pivot away from Wi-Fi-only SKUs. Vendors that overlay energy analytics atop Thread's low-latency mesh can charge premium ASPs, cushioning margin erosion in a commoditizing category.

Residential premises still represent 56.2% of the 2024 smart plug market size, buoyed by voice-assistant bundling and DIY convenience. Yet industrial and commercial buildings are set to expand at a 27.7% CAGR as facility managers chase quantified returns; field studies show 36.8 kW of annual plug-load savings per site when IoT scheduling is applied. Honeywell's plug-load module for enterprise building-management systems exemplifies the pivot to data-driven energy compliance.

In factories and warehouses, skinned industrial-grade smart plugs add thermal-overload protection and over-current analytics that residential units lack. Hospitals and elder-care facilities deploy smart plugs to verify medical-device uptime and prevent unplanned disconnection, aided by subsidy programs for remote monitoring in aging societies. The commercial appetite for SLA-backed hardware supports higher price points, widening the total addressable smart plug market for specialist OEMs.

Smart Plug Market is Segmented by Technology (Bluetooth, Wi-Fi, and More), Application (Residential, Commercial, and More), Sales Channel (Online and Offline), Plug Form Factor (Wall-Plug Adapter, In-Wall Outlet, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained 32.1% leadership in 2024 on the strength of Energy Star SHEMS rules and broadband ubiquity, with utilities offering rebates for demand-response-certified plugs. The region's mature voice-assistant penetration fosters ecosystem lock-in that reduces churn and encourages whole-home retrofits. Canada's updated Energy Efficiency Regulations mirror U.S. standards, giving manufacturers a unified North American certification roadmap.

Asia Pacific is projected to clock a 28.3% CAGR, making it the fastest-expanding territory of the smart plug market. Localized voice-assistant dialect support and competitive pricing have tripled the Alexa device count in India since 2022. China's domestic chipset output curbs BOM volatility and allows white-label brands to proliferate. Government-funded smart-city pilots in Japan and South Korea integrate plug-level energy monitoring into district-wide carbon dashboards, seeding institutional demand for Thread-mesh deployments.

Europe presents a mixed picture. WEEE Directive 2024/884 places full end-of-life costs on manufacturers, pressuring gross margins. Conversely, the UK's 2025 smart-appliance rules require grid-aware functionality, widening the pool of devices that can benefit from retrofitting with Matter-ready smart plugs. Tuya's London retrofit forum underscored the role that low-cost plugs play in hitting net-zero targets for aging housing stock.

South America and the Middle East-Africa trail in installed base but register double-digit growth as 5G rollouts improve latency and coverage. High import duties remain a hurdle, prompting local assembly joint ventures that leverage regional free-trade zones. Developers tapped into hotel chains in the Gulf Cooperation Council to trial centralized energy dashboards, illustrating how smart plugs serve as a gateway product for broader IoT infrastructure.