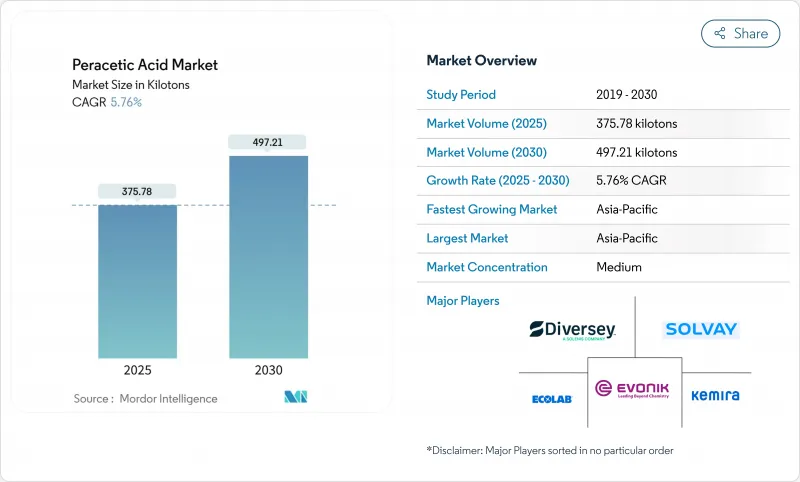

과초산 시장 규모는 2025년에 375.78킬로톤으로 추정되고, 2030년에는 497.21킬로톤에 이를 것으로 예측되며, 예측 기간(2025-2030년) CAGR 5.76%로 성장할 전망입니다.

이 전망에는 염소계 살생물제의 사용을 삼가는 규제 시프트, 저온 살균 시스템의 도입, 물 재이용 인프라에 대한 지속적인 투자가 기여하고 있습니다. 유기적인 취급이나 잔류물이 없는 위생 관리를 위해 인가된 광역 스펙트럼 항균제를 필요로 하는 식품 가공업자에서의 수요 증가가 판매량 증가를 더욱 뒷받침하고 있습니다. 생산자는 또한 수성 혼합물을 안정시키고, 출하 비용을 낮추며, 작업자의 노출 위험을 줄이는 프로세스 혁신을 활용합니다. 아시아태평양과 북미의 인수는 고성장 최종 용도에 신속하게 대응할 수 있는 지역 생산 기지에 대한 전략적 축족을 강조합니다.

과초산은 아세트산, 물, 산소로 분해되므로 규제 대상의 소독 부산물을 피할 수 있기 때문에 지자체와 산업계의 사업자는 과초산으로 전환하고 있습니다. 2024년 PFAS 식수 규칙에 따라 잔류 화학물질에 대한 모니터링이 강화되었지만, 과초산은 광범위한 pH 범위에서 우수한 바이러스 및 원충의 불활성화를 달성하는 것이 파일럿 시험에서 확인되었습니다. 산화제는 기존의 표백제 공급 라인에서 주입할 수 있기 때문에 보수 비용이 낮아지며 자본 지출을 줄일 수 있습니다. 또한, 막에 축적되는 바이오필름이 감소하고, 세정 사이클이 단축되며, 자산 수명이 연장되었다는 보고도 있습니다. 이러한 성능과 컴플라이언스 혜택이 결합되어 2027년까지 대규모 지자체 시스템의 평균 투여량이 증가할 전망입니다.

미국 농무부(USDA)의 유기 규칙은 장비와 표면 위생에 과초산을 허용하고 EPA에 의한 500ppm 잔류 물 면제는 기존 염소 세척에서 일반적이었던 미생물학적 보류 시간 지연을 제거합니다. 건조 또는 거품 안정화 과초산 제제를 채용하는 가공업자는 물 사용량을 줄이고 보다 신속한 라인 전환을 실현함으로써, 고기나 청과 시설의 처리 능력을 향상시키고 있습니다. 연구에 따르면 살생물제는 100ppm 이하의 용량으로 살모넬라균과 리스테리아균에 치사적이며 클린 라벨의 위치를 지지하고 있습니다. 2024년 10월 육류 가공에 대한 OSHA 지침에서는 과초산이 효과적인 박테리아 제어 옵션으로 채택되어 위험이 높은 공장에서의 전환이 촉진되었습니다. 과거에는 유통기한의 단축에 경원하고 있던 소규모 가공업자도, 지금은 6개월 안정성의 희석이 끝난 백 인 박스 시스템을 구입하게 되어, 농촌에서의 새로운 수요 개척이 진행되고 있습니다.

OSHA는 과초산을 위험한 화학물질로 나열하고 있으며, 재고가 1,000파운드를 초과하면 공정 안전 규칙이 적용됩니다. 증기 임계값이 1.24mg/m3이기 때문에 시설은 전용 환기 장치 및 연속 모니터를 설치해야 합니다. 소규모 가공업자에서는 이러한 관리 규칙을 도입하기 위한 자금이 부족할 수 있으며, 도입이 지연되고 있습니다. 예산이 허용되면 작업자는 적합성 시험이 끝난 호흡 마스크 및 화학물질 비산 방지용 PPE가 필요하며 훈련 비용이 부과됩니다. 부드러운 금속에 대한 부식성은 폴리머와 스테인레스 스틸 배관을 요구하고 개조 비용을 증가시킵니다. 자동 주입 시스템은 직접 취급을 줄이지만 보험 회사는 다년간의 사고율이 양호하다는 것이 입증될 때까지 여전히 높은 보험료를 부과합니다.

2024년 과초산 시장의 68.17%를 액체 솔루션이 차지하였고, 255킬로톤 이상에 해당합니다. 신뢰성, 공급 익숙성 및 배합의 낮은 복잡성이 리드를 지원합니다. 액체 제품의 과초산 시장 규모는 지자체, 낙농장, 음료 제조업체가 확립된 사료 시스템에 고집하고 있기 때문에 꾸준히 상승할 것으로 예측됩니다. 그러나 수성 블렌드는 CAGR 5.98%에서 가장 급속히 확대되고 있습니다. 공급업체는 현재 과산화수소와 안정화제로 완충된 과초산을 혼합하여 보존 기간을 12개월까지 연장하여 폐기 비용을 절감하고 있습니다. 블렌드는 저농도로 출하되기 때문에 운송 코드가 더 엄격하지 않게 되어 지역에서의 사용 범위가 넓어집니다. 장비 제조업체는 이러한 블렌드와 작업자의 노출을 줄이는 인라인 희석 모듈을 결합하여 크래프트 맥주 양조장과 분산형 물 재사용 장비에서의 채택을 뒷받침합니다. 분말과 과립은 한적한 광산이나 군 주방 등 장기 보관이나 제로 스필 수송이 불가결한 틈새 위생 요구에 대응합니다.

기술의 진보는 형태의 다양화를 지원합니다. 거품으로 안정화된 스프레이는 수직면에 부착하기 때문에 부란장이나 육류 처리장에서의 접촉 시간이 길어집니다. 드라이브 렌드의 파우치는 현장에서 용해되어, 농산물의 세정에 적당한 강도를 만들어, 중량과 화물을 삭감합니다. 공급업체는 건조 제품 유통에 걸리는 이산화탄소 배출량을 20% 줄일 수 있다고 주장합니다. 예측 기간 동안 에너지 비용 상승과 순 0 목표는 재구성 단계에도 불구하고 사용자를 풍부한 건조한 형태로 향하게 합니다. 전반적으로 형태의 다양성은 공급업체의 탄력성을 강화하고 커스터마이징을 촉진하지만, 규제의 움직임과 보험료가 고강도 저장에 결정적인 벌금을 부과할 때까지 액체가 벌크의 우위를 유지할 가능성이 높습니다.

과초산 시장에서는 2024년 중형(5-15%) 범위의 점유율이 54.17%(약 200킬로톤)로 보고되었습니다. 이 범위는 방폭 보관을 요구하는 임계값 아래로 떨어지는 반면 6-log 미생물 살멸을 실현하여 사용자에게 최고의 비용 대 컴플라이언스 비율을 제공합니다. 수요는 음료 필러, 치즈 휠 및 운영자가 교대마다 소독하는 가금류 공장의 스프레이 칠러에서 발생합니다. 2030년까지의 CAGR은 6.02%로 성장할 전망입니다. 이는 동남아시아의 신규 진입 기업이 수입기기의 사양에 맞는 중간 강도의 패키지를 선택하기 때문입니다. 5% 미만의 저강도 범위는 레스토랑 체인 및 의료용 표면 닦기 등 즉시 사용할 수 있는 틈새 팩에 사용됩니다. 15% 이상의 고강도 범위는 연성 내시경 재처리 및 의약품 클린룸용 벌크 멸균제에 공급되지만, 취급상의 할고감으로부터 광범위한 보급에는 한계가 있습니다.

제형업자는 알루미늄 컨베이어 및 투여 펌프와의 접촉을 허용하는 방청 첨가제가 들어 있는 중급 등급 배합을 설계합니다. 이 호환성을 통해 고객은 비용이 많이 드는 스테인레스 스틸 업그레이드에서 해제됩니다. 병행하여 클라우드에 연결된 미터는 감사 추적을 위해 농도 데이터를 기록하고 FDA 및 EU 위생 기록의 의무화를 완화합니다. 이러한 향상은 전환 비용을 증가시키고 공급업체의 봉쇄를 조장합니다. 원료의 변동은 이폭을 압박할 수 있지만, 생산자는 이중 아세트산 조달과 선물 계약으로 헤지하고 있습니다. 경쟁가격의 가시성으로 인해 중급의 스프레드는 지속가능한 범위 내로 유지되며 앞으로 수년간 안정적인 위치를 유지할 수 있습니다.

아시아태평양은 중국, 인도, 태국이 견인하여 2024년 세계 매출의 38.24%를 차지했습니다. 가처분 소득 증가가 포장 식품 수요에 박차를 가하는 반면 중국의 GB 31604.1 식품 접촉 재료 표준과 같은 엄격한 규칙은 가공업자를 염소 대체품으로 향하게 합니다. 일본 유일의 제조업체는 고순도 전자기기나 의약품의 고객에게 어필하는 비염소계 기술을 활용하고 있습니다. 스마트 수도망에 대한 정부 투자도 과초산을 3차 소독 단계로 끌어들이고 있습니다. 이 지역의 예상 CAGR은 6.75%인데, 이는 인도와 인도네시아에서 병원 건설을 뒷받침하고 있습니다.

북미는 여전히 성숙한 시장이지만 규모는 큽니다. 2024년 PFAS 규정 및 EPA의 증기 멸균 배출에 관한 제안은 공익 기업과 병원이 준수를 위해 과초산을 검토하도록 촉구하고 있습니다. 육류와 닭고기의 수출은 미국 농무부 허가 제균제에 의존하며, 대규모 가공업자는 화학물질 및 자동 스프레이 캐비닛을 결합하는 경우가 많습니다. 미국 중서부의 혁신 클러스터에는 건조 및 완충 등급을 제공하는 여러 제제 전문 기업이 있습니다. 캘리포니아 주 퓨어 워터 샌디에고 프로젝트와 같은 지방 자치 단체의 재사용 계획은 기준 수요를 높이고 있습니다. 지역 전체의 성장은 리노베이션 활동과 제품 다양화로 세계 평균에 가깝습니다.

유럽은 지속가능성의 의무화에 뒷받침되는 안정적인 확대를 보여줍니다. 스칸디나비아의 펄프 공장은 에코 라벨의 상태를 보장하기 위해 과초산 표백을 도입하고, 독일과 벨기에의 맥주 공장은 라인 세척에 낮은 발포성 혼합물을 채택하고 있습니다. EU의 고용 안전 지침은 운영자의 노출량을 제한하고 폐쇄 피드 시스템을 장려합니다. 신흥 동유럽 국가들은 결속기금의 지원을 받아 지자체의 치료 시설을 개선하고 2차 소독에 과초산을 도입하고 있습니다. 현재, 처리량 증가는 완만하지만, 탄소와 염소의 배출 제한이 엄격해져 2030년까지 추가적인 도입이 가능합니다.

The Peracetic Acid Market size is estimated at 375.78 kilotons in 2025, and is expected to reach 497.21 kilotons by 2030, at a CAGR of 5.76% during the forecast period (2025-2030).

The outlook benefits from regulatory shifts that discourage chlorine-based biocides, uptake in low-temperature sterilization systems, and ongoing investment in water reuse infrastructure. Rising demand from food processors that require broad-spectrum antimicrobials approved for organic handling and residue-free sanitation further supports volume gains. Producers are also capitalizing on process innovations that stabilize aqueous blends, lower shipping costs, and cut worker exposure risks. Acquisitions in Asia-Pacific and North America underline a strategic pivot toward regional production hubs able to serve high-growth end-uses quickly.

Municipal and industrial operators are switching to peracetic acid because it breaks down into acetic acid, water, and oxygen, thus avoiding regulated disinfection by-products. The 2024 PFAS drinking-water rule has intensified scrutiny of residual chemicals, and pilot trials confirm that peracetic acid achieves superior virus and protozoa inactivation across wide pH ranges. Retrofit costs stay low because the oxidant can be dosed through existing bleach feed lines, trimming capital outlays. Operators also report lower biofilm build-up in membranes, which reduces cleaning cycles and extends asset life. These performance and compliance benefits combine to raise average dose volumes in large municipal systems, particularly through 2027 when tighter effluent targets phase in across China and the United States.

USDA organic rules permit peracetic acid for equipment and surface sanitation, and a 500 ppm residue exemption by the EPA removes microbiological hold-time delays common with legacy chlorine rinses. Processors that adopt dry or foam-stabilized peracetic acid formulations are cutting water usage and achieving quicker line changeovers, which improves throughput in meat and produce facilities. Studies show the biocide is lethal to Salmonella and Listeria at sub-100 ppm doses, supporting clean-label positioning. The October 2024 OSHA guidance for meat-packing highlighted peracetic acid as a validated bacterial control option, accelerating conversions in high-risk plants. Smaller processors, once deterred by short shelf life, now purchase diluted bag-in-box systems with six-month stability, opening new rural demand pockets.

OSHA lists peracetic acid among highly hazardous chemicals, triggering process-safety rules at inventories above 1,000 lb. Facilities must install dedicated ventilation and continuous monitors because the vapor threshold limit is 1.24 mg/m3. Small processors sometimes lack capital for these controls, slowing adoption. Even where budgets allow, staff require fit-tested respirators and chemical splash PPE, raising training costs. Corrosivity toward soft metals demands polymer or stainless piping, adding to retrofit expenses. Although automatic dosing systems reduce direct handling, insurers still impose higher premiums until multi-year incident rates prove favorable.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Liquid solutions represented 68.17% of the peracetic acid market in 2024, equivalent to more than 255 kilo tons. Reliability, supply familiarity, and low formulation complexity sustain this lead. The peracetic acid market size for liquid products is projected to climb steadily as municipalities, dairies, and beverage lines stick with established feed systems. However, aqueous blends are scaling fastest at a 5.98% CAGR. Suppliers now formulate buffered peracetic acid with hydrogen peroxide and stabilizers that extend shelf life up to 12 months, slashing disposal costs. Blends are shipped at lower concentrations, qualifying for less stringent transport codes that widen rural reach. Equipment makers are pairing these blends with inline dilution modules that trim worker exposure, stoking adoption across craft breweries and decentralized water reuse units. Powder and granule formats occupy niche hygiene needs where long storage or zero-spill transport is vital, such as remote mines and military kitchens.

Technological progress supports form diversification. Foam-stabilized sprays cling to vertical surfaces, giving longer contact time in hatcheries and slaughterhouses. Dry-blended sachets dissolve on-site and generate targeted strengths for produce washes, reducing weight and freight. Suppliers claim 20% lower carbon footprints for dry product distribution. Over the forecast window, rising energy costs and net-zero goals should push users toward concentrated dry forms despite reconstitution steps. Overall, form variety strengthens supplier resilience and encourages customization, yet liquids will likely retain bulk dominance until regulatory moves or insurance premiums decisively penalize high-strength storage.

The peracetic acid market reported 54.17% share for the medium (5-15%) range in 2024, roughly 200 kilo tons. This span delivers six-log microbial kill while staying below thresholds that demand explosion-proof storage, giving users the best cost-to-compliance ratio. Demand stems from beverage fillers, cheese wheels, and spray chillers in poultry plants where operators sanitize every shift. The medium segment is set for a 6.02% CAGR through 2030 as new entrants in Southeast Asia choose mid-strength packages that match imported equipment specs. Low ranges under 5% serve ready-to-use niche packs for restaurant chains and medical surface wipes. High ranges above 15% feed bulk sterilizers for flexible endoscope reprocessing and pharmaceutical clean rooms but face handling premiums that limit broad uptake.

Formulators are engineering medium-grade blends with anti-corrosive additives, allowing contact with aluminum conveyors and dosing pumps. This compatibility saves clients from costly stainless upgrades. In parallel, cloud-connected meters log concentration data for audit trails, easing FDA and EU hygiene record mandates. These enhancements raise switching costs and foster supplier lock-in. Although feedstock volatility can squeeze margins, producers hedge with dual acetic acid sourcing and forward contracts. Competitive price visibility keeps medium-grade spreads within sustainable bands, preserving its anchor position in coming years.

The Peracetic Acid Market Report Segments the Industry by Product Form (Liquid Solutions, Powder/Granules, and Aqueous Blends), Concentration Grade (Less Than 5 % PAA (Low), and More), Application (Disinfectant, Oxidizer, and More), End-User Industry (Food and Beverage, Water Treatment, Pulp and Paper, Chemical, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Asia-Pacific generated 38.24% of global revenue in 2024, led by China, India, and Thailand. Rising disposable incomes spur packaged food demand, while stringent rules such as China's GB 31604.1 food-contact material standard are nudging processors toward chlorine alternatives. Japan's sole producer leverages chlorine-free technology that appeals to high-purity electronics and pharmaceutical clients. Government investments in smart water grids also pull peracetic acid into tertiary disinfection stages. The region's forecast 6.75% CAGR is further backed by hospital construction in India and Indonesia, where low-temperature sterilizers suit power-constrained facilities.

North America remains a mature but sizable market. The 2024 PFAS rule and the EPA's steam sterilization emission proposals are pushing utilities and hospitals to consider peracetic acid for compliance. Meat and poultry exports rely on USDA-approved sanitizers, and large processors often pair the chemistry with automated spray cabinets. Innovation clusters in the United States Midwest house multiple formulation specialists that supply dry or buffered grades. Adoption in municipal reuse schemes like California's Pure Water San Diego project boosts baseline demand. Overall regional growth runs near the global average thanks to retrofit activity and product diversification.

Europe demonstrates stable expansion anchored by sustainability mandates. Scandinavian pulp mills deploy peracetic acid bleaching to secure eco-label status, and breweries in Germany and Belgium integrate low foaming blends for line cleaning. The EU Employment Safety Directive caps operator exposure, encouraging closed-feed systems. Emerging Eastern European members are upgrading municipal treatment works with support from cohesion funds, inserting peracetic acid into secondary disinfection. Although volume gains are moderate at present, tight carbon and chlorine discharge limits provide a long runway for additional uptake through 2030.