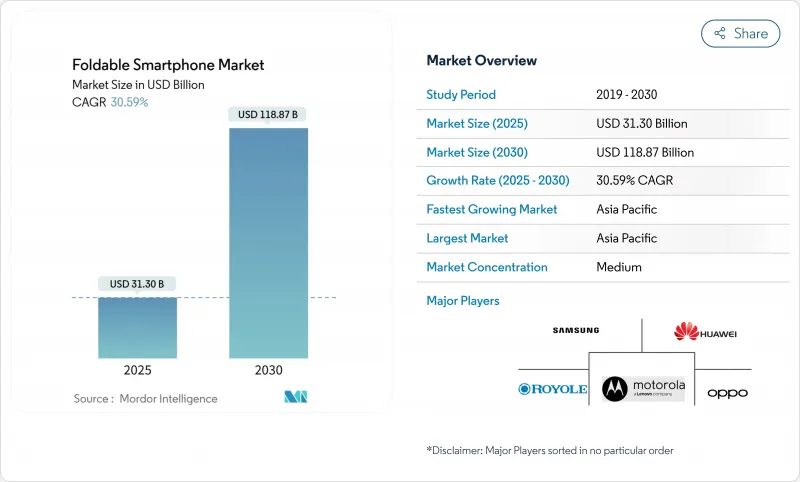

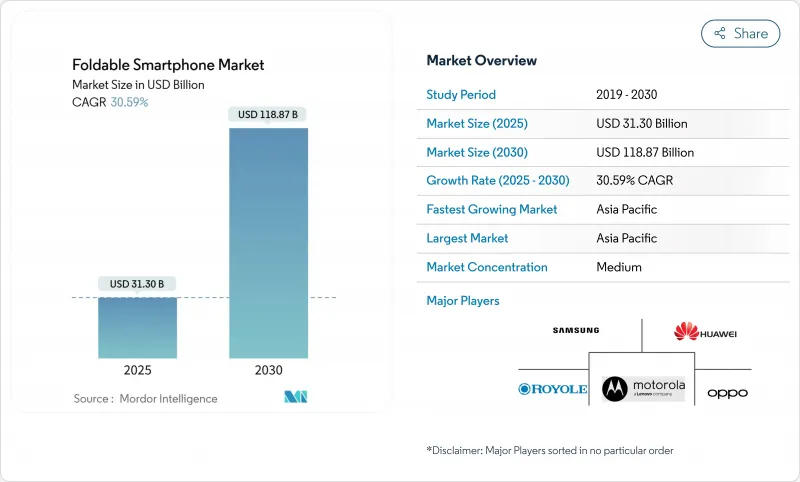

폴더블 스마트폰 시장 규모는 2025년 313억 달러로 추정되고, 예측기간(2025-2030년)의 CAGR은 30.59%를 나타낼 전망이며, 2030년에는 1,188억 7,000만 달러에 달할 것으로 예상됩니다.

초박형 유리(UTG) 제조, 힌지 공학, 패널 수율의 진보는 내구성을 향상시키면서 단가를 낮추고 있습니다. 아시아태평양은 중국의 OEM 제조업체가 다세대 라인의 생산 능력을 확대하고 한국의 디스플레이 제조업체가 프로세스 노하우를 보호함으로써 수요 및 공급의 원동력이 되고 있습니다. 기존 스마트폰의 성장이 한 자리에 진정되는 가운데도, 캐리어 주도의 단말 보조금과 프리미엄 5G 플랜, 생산성 중시의 이용 사례에 대한 기업의 관심의 높아짐, 컨텐츠 스트리밍 파트너십의 확대는 보급의 기세를 강화하고 있습니다. 제조업체 각사는 스타일 중시의 구매층용으로 클램쉘형 디자인을 연마해, 생산성 중시의 구매층용으로 북형 플래그쉽기를 발표하고 있어, 폼 팩터 혁신의 다음의 물결을 확실히 하기 위해서 3개 접어 시제품에 투자하고 있습니다.

지속적인 공정 개선으로 UTG의 수율이 향상되고 보다 강한 커버층이 가능해졌습니다. 삼성의 최신 Galaxy Z세대는 20만회 이상의 접힘에 견딜 수 있는 강화 유리를 채용해, 모토로라의 2025년 Razr 시리즈는 힌지의 내구성을 35% 향상시키는 티탄제 백본을 채용해, IP48의 방수·방진 인증을 취득하고 있습니다. 신뢰성 이정표는 소비자 주저를 줄이고 스크랩 손실이 줄어들고 처리량이 향상됨에 따라 더 광범위한 가격 세분화에 대한 길을 열고 있습니다.

고ARPU의 5G 플랜과 연동한 월별 할부가 최종 사용자의 프리미엄 가격을 중화하고 있기 때문에 통신사업자의 점포는 여전히 폴더블폰 판매 점유율의 60%를 차지하고 있습니다. 일반적인 보조금 제도는 24개월 계약으로 소매가를 30-45% 낮추는 것으로, 접이식 휴대전화의 소유자는 슬래브식 휴대전화 사용자보다 1.8배 더 많은 동영상 트래픽을 스트리밍하므로 유지율을 높여 데이터 소비를 자극합니다. 이 전술은 데이터 무제한 요금 플랜의 보급률이 이미 높은 북미와 유럽에서 특히 효과적이며, 경력에게 마진의 여유와 5G 업그레이드 사이클의 동경의 선택지로서 접이식을 위치시키는 마케팅력을 부여하고 있습니다.

상대 습도가 높으면 힌지핀과 유연한 접착제층의 부식이 가속되어 유효 수명이 실험실에서 평가되고 있는 20만회 미만으로 구매 후 18개월 이내에 고객으로부터 불만이 전해집니다. OEM은 방청 합금과 추가 나노 코팅으로 대항하고 있지만, 이러한 업그레이드는 재료비를 높이고 열 예산을 복잡하게합니다. 스마트폰의 교체 빈도가 높음에도 불구하고, 인도네시아, 태국, 브라질의 해안 지역에서의 보급률이 평균 이하인 이유는 견고성과 저렴한 양립이 어렵기 때문입니다.

2024년 세계 출하 대수의 62%를 북형 단말이 차지해, 폴더블 스마트폰 시장의 상당한 부분을 지지했습니다. 태블릿 클래스의 7-8인치 내장 디스플레이는 3페인의 멀티태스킹이나 스타일러스에 적합한 묘화 화면을 실현해 모놀리식인 박형 단말과는 일선을 그립니다. 삼성의 갤럭시 Z 폴드 라인과 화웨이의 메이트 X 시리즈는 이런 이점을 뒷받침하고 있으며, 금융, 디자인, 얼리어댑터의 소비자 틈새의 파워 유저를 대상으로 하고 있습니다. 클램쉘형 하위 부문은 희망 소매 가격의 문턱의 낮음과 플립폰의 인체공학에의 향수를 활용해 패션 지향의 구매층에 어필하고 있기 때문에 CAGR은 33.4%를 나타낼 전망입니다.

2025년에 한정 생산이 예정된 삼중 프로토타입은 내부 패널을 10인치까지 확장할 수 있어 핵심 모델을 탄력화하지 않고 증수를 획득할 수 있습니다. 외부로 접히는 유형은 노출된 유연한 매트릭스를 마모로부터 보호하는 엔지니어링 과제에 의해 제한된 채로 있습니다. 실험적인 시도에도 불구하고, 북형과 관련된 폴더블 스마트폰 시장 규모는 2030년까지 650억 달러 이상에 달할 것으로 예상되는 반면, 크램쉘은 호조적인 수량 증가로 그 차이를 줄여 미래 포트폴리오의 이중주 구조를 재확인하게 됩니다.

2024년의 세계 출하 대수의 55%를 7-8인치의 패널이 차지해, 노트북 PC 수준의 생산성과 접을 때의 한손으로의 휴대성을 양립시키는 스위트 스폿을 반영했습니다. OEM 로드맵에 따르면 액티브 디스플레이의 제곱인치당 조익률이 가장 높기 때문에 이 대역을 계속 선호합니다. 8인치를 초과하는 디스플레이는 복잡한 멀티 기어 힌지가 슬림하고 폴리머 백플레인이 딱딱해지고 접힌 선이 줄어들기 때문에 CAGR 32.5%를 나타낼 전망입니다.

소형<=6.9-inch clamshell screens remain attractive in the fashion and youth segments where pocketability and colour-matched accessories trump raw workspace. Nevertheless, larger canvases attract premium ARPU content partnerships. By 2030, the>8인치 코호트는 폴더블 스마트폰 시장 규모의 23%에 이를 것으로 예상되지만, 가격 압축 때문에 수익 점유율은 아직 늦어지고 있습니다.

아시아태평양은 2024년 출하량의 68%를 차지하며 디스플레이 제조, 힌지 단조, UTG 연마의 긴밀한 수직 통합을 통해 지역 리더십을 확보했습니다. 중국이 공급과 내수를 모두 지원하고 있으며, 현지 OEM은 지방 보조금을 활용하여 8.6세대 OLED 공장을 확장하여 규모의 이점을 실현하고 있습니다. 한국은 견고한 5G 실적와 삼성의 자국 브랜드 에퀴티 덕분에 1인당 접을 수 있는 기기의 보급률이 세계 제일을 자랑하고 있습니다. 일본은 컴팩트한 휴대 단말기의 전통에 따라 소형의 클램쉘형으로 기울어져 있으며, 인도의 보급 페이스는 평균 가처분 소득에 대한 비싼 가격 설정에 의해 억제되고 있지만, 그래도 도시에서는 급경사의 궤적을 그리고 있습니다.

북미는 초기 비용을 중화하는 경력의 적극적인 보조금으로 세계 2위를 차지하고 있습니다. 미국은 데이터 무제한 계획의 광범위한 보급 외에도 프리미엄 5G 경험의 마케팅을 강력하게 추진하고 통신량을 선도하고 있습니다. 캐나다는 절대 규모가 작고 미국의 먼지를 숭배합니다. 중남미에서의 보급은 브라질과 멕시코에 집중하고 있으며, 도시의 부유층이 스테이터스가 있는 단말을 요구하고 있습니다.

독일, 프랑스, 영국 등 북부와 서부 시장에서는 생산적인 용도로 북형 접이식이 채용되고 있지만, 남부 시장은 여전히 비용에 민감하고 전환이 늦어지고 있습니다. 중동의 걸프 협력 회의 국가는 고급 지향 수요를 보여주고, 접이식 가방을 라이프 스타일의 플래그쉽으로 자리 매김하고 있습니다. 아프리카는 남아프리카의 도시 클러스터를 제외하면 아직 발전도상이며 구매력평가 제약을 받으면서도 1,000달러 이하의 모델이 보급되면 기회도래를 예감시킵니다. 아시아태평양은 2030년까지 폴더블 스마트폰 시장 점유율을 계속 확대할 것이지만, 성장은 북미와 서유럽의 기업 구매와 신흥 시장의 저렴한 가격대 제품에 점점 의존할 것으로 보입니다.

The Foldable Smartphone Market size is estimated at USD 31.30 billion in 2025, and is expected to reach USD 118.87 billion by 2030, at a CAGR of 30.59% during the forecast period (2025-2030).

Advances in ultra-thin glass (UTG) manufacturing, hinge engineering, and panel yields are bringing unit costs down while improving durability, a combination that is repositioning foldables from niche status to a mainstream upgrade path. Asia Pacific remains the engine of demand and supply, anchored by Chinese OEMs scaling multi-generation line capacity and South Korean display makers safeguarding process know-how. Carrier-led device subsidies tied to premium 5G plans, rising enterprise interest in productivity-focused use cases, and widening content-streaming partnerships are reinforcing adoption momentum even as conventional smartphone growth settles into single-digit territory. Manufacturers are honing clamshell designs for style-driven buyers and launching book-style flagships for productivity enthusiasts, and they are investing in tri-fold prototypes to secure the next wave of form-factor innovation.

Continuous process refinements have raised UTG yield rates and enabled tougher cover layers. Samsung's latest Galaxy Z generation incorporates reinforced glass that tolerates more than 200,000 folds, while Motorola's 2025 Razr family uses a titanium backbone that raises hinge endurance by 35% and carries IP48 water- and dust-resistance certification . Reliability milestones are reducing consumer hesitation and paving the way for broader price segmentation as scrap losses fall, and throughput improves.

Operator stores still control a 60% share of foldable sales because monthly instalments tied to high-ARPU 5G plans neutralize premium pricing for end users. Typical subsidy schemes shave 30 - 45% off retail prices over 24-month contracts, lifting retention rates and stimulating higher data consumption as foldable owners stream 1.8 times more video traffic than slab-phone users. The tactic is especially potent in North America and Europe, where penetration of unlimited-data tariffs is already high, giving carriers both the margin headroom and marketing muscle to position foldables as the aspirational choice for 5G upgrade cycles.

High relative humidity accelerates corrosion on hinge pins and flexible adhesive layers, reducing effective life cycles below the laboratory-rated 200,000 folds and triggering client complaints within 18 months of purchase. OEMs are countering with rust-resistant alloys and additional nano-coatings, yet these upgrades raise bill-of-materials costs and complicate thermal budgets. Difficulty in balancing ruggedization with affordability explains the below-average penetration across Indonesia, Thailand, and coastal Brazil, despite high smartphone replacement frequency.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Book-style devices controlled 62% of global shipments in 2024, underpinning a substantial slice of the foldable smartphone market. Their tablet-class 7 - 8-inch internal displays unlock three-pane multitasking and stylus-friendly drawing surfaces that differentiate them from monolithic slabs. This dominance is underpinned by Samsung's Galaxy Z Fold line and Huawei's Mate X series, which both target power users in finance, design, and early-adopter consumer niches. The clamshell sub-segment is expanding at a forecast 33.4% CAGR as it leverages lower MSRP thresholds and nostalgia for flip-phone ergonomics to appeal to fashion-oriented buyers.

Tri-fold prototypes scheduled for limited production in 2025 could stretch internal panels to 10 inches, potentially capturing incremental revenue without cannibalising core models. Outward-fold variants remain constrained by the engineering challenge of protecting exposed flexible matrices from abrasion. Despite the experimentation, the foldable smartphone market size attached to book-style lines is set to stay above USD 65 billion by 2030, while clamshells will narrow the gap through brisk volume gains, reaffirming the dual-pillar architecture of future portfolios.

Panels between 7 and 8 inches accounted for 55% of global shipments in 2024, reflecting a sweet spot that marries laptop-lite productivity with one-hand portability in folded mode. OEM roadmaps indicate a continued preference for this band because it delivers the highest gross margin per square inch of active display. Displays beyond 8 inches will scale at a 32.5% CAGR as complex multi-gear hinges slim down and polymer backplanes stiffen, shrinking crease lines.

Smaller <= 6.9-inch clamshell screens remain attractive in the fashion and youth segments where pocketability and colour-matched accessories trump raw workspace. Nevertheless, larger canvases attract premium ARPU content partnerships. By 2030, the > 8-inch cohort is expected to reach 23% of the foldable smartphone market size, though still lagging in revenue share due to price compression.

The Foldable Smartphone Market Report is Segmented by Form Factor (Clamshell, Book-Style, and More), Screen Size ( Less Than Equal To 6. 9 Inch, 7-8 Inch, and More), Price Range (Less Than USD 1, 000, and More), Sales Channel (Carrier/Operator Stores, Consumer Electronics and Specialty Retail, and More), End User (Consumer, Enterprise/Corporate, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific commanded 68% of 2024 shipments, securing regional leadership through its tight vertical integration of display fabrication, hinge forging, and UTG polishing. China anchors both supply and domestic demand, with local OEMs leveraging provincial subsidies to expand Gen 8.6 OLED fabs and achieve scale economies. South Korea boasts the world's highest per-capita foldable uptake thanks to a robust 5G footprint and Samsung's home-field brand equity. Japan leans toward petite clamshells in keeping with compact handset traditions, while India's adoption pace is gated by premium pricing relative to average disposable income, yet still plots a steep trajectory in metro areas.

North America ranks second globally, driven by aggressive carrier subsidies that neutralise upfront costs. The United States leads volume on the back of broad unlimited-data plan penetration, coupled with a heavy marketing push behind premium 5G experiences. Canada shadows the US curve, albeit at a lower absolute scale. Latin American adoption is concentrated in Brazil and Mexico, where affluent urban consumers seek status devices; however, sticky import tariffs and volatile foreign-exchange conditions temper mass-market momentum.

Europe presents a mosaic picture: Northern and Western markets such as Germany, France, and the UK exhibit productive-use adoption of book-style folds, while Southern markets remain cost-sensitive and slower to migrate. Gulf Cooperation Council states in the Middle East display luxury-driven demand, positioning foldables as lifestyle flagships. Africa remains nascent except for South Africa's urban clusters, constrained by purchasing-power parity yet signalling opportunity once sub-USD 1,000 models proliferate. Collectively, Asia Pacific will continue to raise its foldable smartphone market share through 2030, but incremental growth will increasingly hinge on North American and Western European enterprise purchases and emerging-market affordability plays.