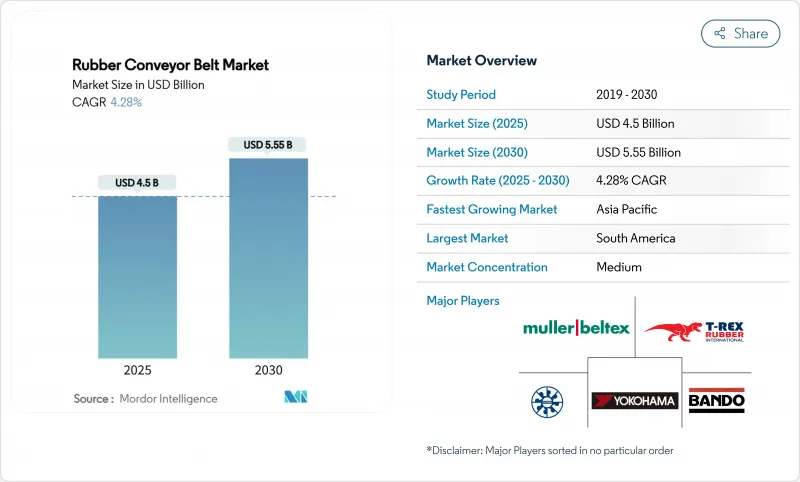

고무 컨베이어 벨트 시장 규모는 2025년에 45억 달러로 추정되고, 2030년에는 55억 5,000만 달러에 이를 것으로 예측되며, CAGR 4.28%로 추이할 전망입니다.

수요가 확대되고 있는 이유는 광업, 물류, 재활용, 공정 산업의 사업자가 벌크 자재 관리 시스템을 근대화해, 긴 수명으로 고속 주행이 가능한 내열성, 내화성, 내유성의 벨트를 지정하고 있기 때문입니다. 안전 규칙 강화, 자동화 가속, 에너지 전환 광물의 급성장이라는 세 가지 구조적 힘이 작동합니다. 최종 사용자는 현재 고급 벨트를 소모품이 아닌 생산성 레버로 취급하고 있으며, 이 인식은 서비스 계약을 늘리고 공급업체의 수익을 원활하게 하고 있습니다. 동시에, 특히 부타디엔과 카본블랙에 길어지는 원재료의 변동이 제조업체를 다년간 공급계약 확보 및 바이오기반 필러 시용에 몰두하고 있어 비용 리스크가 적극적으로 관리되고 있음을 나타내는 초기 징후가 되고 있습니다.

중국, 한국, 인도네시아의 양극 및 전구체 공장에서는 200℃ 이상의 반응기 가동이 증가하고 있으며, 열 안정성 및 정전기 방산성을 겸비한 그래핀 나노튜브 강화 벨트의 급속한 보급이 진행되고 있습니다. 이 벨트는 냉각 능력을 추가하지 않고 처리 능력을 향상시킬 수 있으며, 결과적인 생산성 향상은 수직 통합 광산업자에게 다년간 공급 계약을 맺을 설득력을 가지고 있습니다. 새로운 추론은 고열 화합물의 조기 인증이 이제 프로젝트 일정의 신뢰성을 대체하는 역할을 한다는 것입니다.

도시 지역의 마이크로 풀필먼트 센터는 10,000 평방 피트 이하의 면적을 차지하고 비틀림, 상승, 정지를 mm 단위로 하는 컴팩트한 경량 벨트에 의존하고 있습니다. 다층 구조에서 단층 구조로 전환한 운영자는 20% 이상의 에너지 절약을 보고하고 있으며, 벨트의 질량이 어떻게 총 운전 비용에 영향을 미치는지를 밝혔습니다. 노동력 부족은 계속되고 있기 때문에 저신축 패브릭과 관련된 피킹 정밀도의 향상은 창고 경제성의 중심에 재료 과학을 설치함으로써, 평방 피트당의 수익을 직접적으로 향상시킵니다.

오디샤 주에서 계획된 6GW 태양전지 모듈 공장에서는 기존의 커버를 열화시키는 가소제나 밀봉제를 취급하기 위해 내유성 벨트를 채용하고 있습니다. 니트릴 블렌드와 내마모성 카커스를 결합하여 층간 박리를 방지하고 예정되지 않은 다운타임을 줄입니다. 특수화학 및 신재생에너지 전개의 결합은 국가의 산업 정책이 고무 컨베이어 벨트 시장 규모를 프리미엄 제품으로 향하게 할 수 있는 방법을 명확하게 보여줍니다.

2024년 고무 컨베이어 벨트 시장 점유율은 내열 벨트가 29%를 차지했습니다. 실리카를 많이 함유하는 화합물의 진보에 의해 이러한 벨트는 200°C 이상으로 연속 운전할 수 있게 되어, 킬른 오퍼레이터는 노의 설정 온도를 올려, 처리 능력을 향상시킬 수 있습니다. 열 균열이 적다는 것은 유지 보수의 종료가 짧다는 것이며, 플랜트의 유효 가동률을 확대하는 결과가 됩니다.

내화성 벨트는 2025-2030년 연평균 복합 성장률(CAGR) 5.9%를 보일 것으로 예측됩니다. CAN/CSA-M422에 근거한 유형 A 또는 B의 인증을 취득한 벨트는 프리미엄을 획득해, 많은 현장이 이러한 등급만을 지정하게 되어, 비인증의 경쟁자에게 있어서 장벽이 높아지고 있습니다.

중량 벨트는 2024년 고무 컨베이어 벨트 시장 규모의 45%를 차지했습니다. 폴리에스테르 나일론의 카커스는 강도와 유연성의 균형을 이루며, 소화물 허브는 드라이브를 업그레이드하지 않고 벨트의 수명을 연장할 수 있습니다. 그 결과, 에너지가 절약되고 구조용 강재의 요건이 저하되기 때문에 특히 전기 요금이 높은 지역에서는 투자 회수가 촉진됩니다.

광산이 더 긴 육상 컨베이어를 채택함에 따라 무게 벨트의 CAGR은 5.5%로 성장할 것으로 예측됩니다. 굿이어의 초강성 폴리에스테르 및 나일론 설계는 수 킬로미터의 비행에서의 신장을 최소화하고 처짐을 설계 한계 내에 유지합니다. 신장을 억제하면 반송 포인트 수를 줄이고 분진 배출량과 유지 보수 시간을 줄이는 단일 비행 레이아웃이 가능합니다.

고무 컨베이어 벨트 시장 세분화 : 벨트 유형별(내열, 내유, 기타), 벨트 중량별, 보강 재료별(직물 및 직물 카커스, 스틸 코드, 직물), 최종 사용자 산업별(물류 및 창고, 광업 및 채석, 기타), 지역별로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

아시아는 2024년 매출의 34%를 차지했으며, 중국의 대규모 제조 거점 및 인도의 인프라 정비에 힘쓰고 있습니다. 태국과 말레이시아에서 천연 고무 원료를 입수할 수 있어 비용 충격이 완화되고, 이 지역의 생산자는 인풋 면에서 우위를 차지합니다. 배터리 금속 정제 및 태양광 모듈 제조에 대한 정책적 인센티브는 벨트 수요를 내열 및 내유 유형으로 향하게 하여 성장을 특수한 틈새에 집중시킵니다.

2030년까지 연평균 복합 성장률(CAGR)은 남미가 가장 높은 6.3%로 성장할 것으로 예측됩니다. 칠레, 페루, 브라질의 주요 구리 프로젝트는 운반 트럭을 육상 컨베이어로 대체하고 고하중 스틸 코드 벨트의 대량 주문을 견인하고 있습니다. 안타미나의 20억 달러에 이르는 연명 공사에서는 새로운 컨베이어에 많은 자본이 투입되어 측벽과 급각 설계를 제공하는 공급업체는 프리미엄 계약을 획득하고 있습니다. 이 지역의 광산에서는 신재생에너지에 대한 노력이 진행되고 있어 에너지 소비량을 삭감하는 저신축 벨트에 대한 관심이 더욱 높아지고 있습니다.

북미와 유럽은 큰 점유율을 유지하고 있지만 그 이유는 다릅니다. 북미 창고는 가동 시간 예측을 우선하기 위해 센서가 달린 벨트를 구입했으며 유럽 공장은 건강 기준을 충족하기 위해 낮은 니트로소아민 배합에 중점을 둡니다. 중동 및 아프리카는 아직 개발 도상이지만 유망합니다. 철도 프로젝트 및 철광석 광산은 고열 및 연마 분진을 견딜 수 있는 벨트를 요구하고 있으며, 구매자는 자외선에 안정적인 커버를 갖춘 합성 고무와 천연 고무의 혼합 벨트를 선택합니다.

The rubber conveyor belt market size is estimated at USD4.5 billion in 2025 and is forecast to reach USD5.55 billion by 2030, advancing at a 4.28% CAGR.

Demand is expanding because operators in mining, logistics, recycling, and process industries are modernizing bulk-material-handling systems and specifying heat-, fire-, and oil-resistant belts that last longer and run at higher speeds. Three structural forces are at work: stricter safety rules, accelerating automation, and rapid growth in energy-transition minerals. End-users now treat premium belts as productivity levers rather than consumables, a perception that is lengthening service contracts and smoothing revenue for suppliers. Concurrently, lingering raw-material volatility-especially in butadiene and carbon black-has pushed manufacturers to secure multi-year supply agreements and trial bio-based fillers, an early sign that cost risk is being actively managed.

Cathode and precursor plants across China, Korea, and Indonesia increasingly operate reactors above 200°C, driving rapid uptake of graphene-nanotube-enhanced belts that combine thermal stability with static dissipation. These belts allow processors to raise throughput without adding cooling capacity, and the resulting productivity gain is convincing vertically integrated miners to lock in multi-year supply agreements. A fresh inference is that early certification of high-heat compounds now serves as a proxy for project schedule reliability.

Urban micro-fulfilment centers occupy footprints under 10,000 sq ft and rely on compact lightweight belts that twist, climb, and stop within millimetres. Operators switching from multi-ply to single-ply constructions report energy savings exceeding 20%, highlighting how belt mass influences total operating cost. Because labour shortages persist, gains in picking accuracy linked to low-stretch fabrics directly elevate revenue per square foot, placing materials science at the heart of warehouse economics.

A planned 6 GW solar-module plant in Odisha will employ oil-resistant belts to handle plasticisers and encapsulants that degrade conventional covers. Pairing nitrile blends with abrasion-resistant carcasses prevents delamination, cutting unplanned downtime. This linkage between specialty chemistry and renewable-energy rollout underscores how national industrial policy can redirect rubber conveyor belt market size toward premium variants.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Heat-resistant belts held 29% of the rubber conveyor belt market share in 2024. Advances in silica-rich compounds let these belts run continuously above 200 °C, enabling kiln operators to raise furnace set-points and unlock throughput gains. Fewer thermal cracks mean shorter maintenance shutdowns, an outcome that expands effective plant availability.

Fire-resistant variants are forecast to grow at a 5.9% CAGR between 2025-2030, fuelled by underground-mine safety codes and EU recycling mandates. Belts achieving Type A or B certification under CAN/CSA-M422 command premiums, and many sites now specify only these grades, elevating barriers for non-certified competitors.

Medium-weight belts provided 45% of the rubber conveyor belt market size in 2024. Polyester-nylon carcasses balance strength and flexibility, letting parcel hubs extend belt life without upgrading drives. The resulting energy savings and lower structural-steel requirements reinforce payback, especially where electricity tariffs are high.

Heavy-weight belts are projected to post a 5.5% CAGR as mines adopt longer overland conveyors. Goodyear's extra-stiff polyester/nylon designs minimise stretch on multi-kilometre flights, keeping sag within design limits. Lower elongation allows single-flight layouts that reduce the number of transfer points, cutting dust emissions and maintenance hours.

Rubber Conveyor Belt Market Segmented by Belt Type (Heat-Resistant, Oil-Resistant and More), Belt Weight, Reinforcement Material (Textile / Fabric Carcass, Steel Cord and Solid-Woven), End-User Industry (Logistics & Warehousing, Mining & Quarrying and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia dominated with 34% of 2024 revenue, propelled by China's large manufacturing base and India's infrastructure push. Access to natural rubber feedstock from Thailand and Malaysia buffers cost shocks, giving regional producers an input advantage. Policy incentives for battery-metal refining and solar-module manufacturing channel belt demand toward heat- and oil-resistant variants, effectively concentrating growth in specialised niches.

South America is forecast to record the highest 6.3% CAGR to 2030. Major copper projects in Chile, Peru, and Brazil are replacing haul trucks with overland conveyors, driving large orders for heavy-duty steel-cord belts. Antamina's USD 2 billion life-extension dedicates substantial capital to new conveyors, and suppliers that offer sidewall or steep-angle designs are capturing premium contracts. The region's commitment to renewable power for mines further raises interest in low-stretch belts that cut energy draw.

North America and Europe retain significant shares, but for different reasons. North American warehouses prioritise predictive uptime and thus purchase sensor-equipped belts, while European factories focus on low-nitrosamine formulations to meet health standards. The Middle East and Africa remain nascent yet promising: rail projects and iron-ore mines require belts that withstand high heat and abrasive dust, pushing buyers toward blended synthetic-natural rubbers with UV-stable covers.