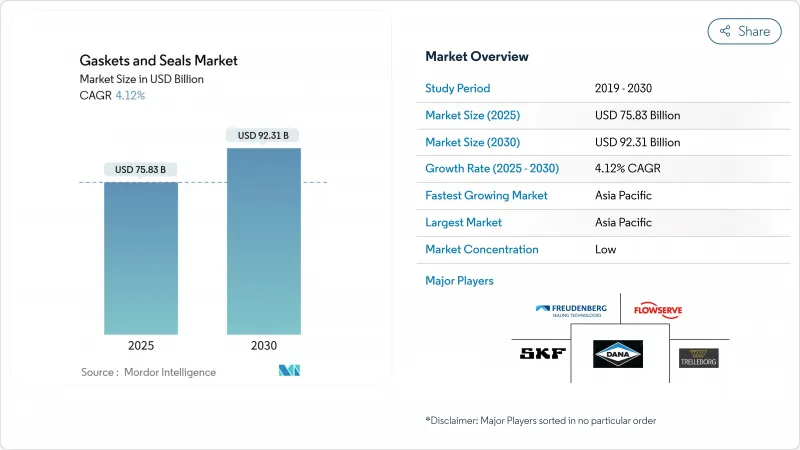

개스킷 및 씰 시장 규모는 2025년에 758억 3,000만 달러로 추정되고 예측 기간(2025-2030년)의 CAGR은 4.12%로, 2030년에는 923억 1,000만 달러에 달할 것으로 예상됩니다.

석유 및 가스, 화학처리, 자동차전화, 산업 자동화로부터의 왕성한 수요는 계속 꾸준한 확대를 보강할 것으로 보입니다. 특히 바이오 엘라스토머와 PFAS 프리 화합물의 급속한 재료 혁신은 한때 지속 가능한 옵션을 제한했던 성능 트레이드 오프를 제거합니다. 디지털 모니터링은 정적 부품을 데이터 포인트로 변환하여 예기치 않은 다운 타임을 줄이고 새로운 수익원을 창출하는 예보 유지보수 서비스를 가능하게 합니다. 제조업체 각 회사는 장기적인 애프터마켓 가치를 보장하기 위해 윤활 관리 및 서비스 계약 인수로 대응합니다. 불소 고무 원료를 둘러싼 공급망의 압력은 이중 조달 전략과 대체 화학 물질의 조사 가속을 촉진하여 가격 충격에 대한 취약성을 완화합니다.

비전통적인 매장량의 탐사와 안전규칙의 엄격화에 의해 사업자는 극도의 압력과 공격적인 매체를 견디는 고급 밀봉 솔루션을 지정하도록 요구되고 있습니다. 니트릴이나 바이톤의 O링은 내약품성이 뛰어나므로 현재는 방분장치와 갱정의 표준이 되고 있습니다. 탈산성 배출을 방지하는 기계적 씰은 제품 손실 및 온실가스 배출을 줄이는 동시에 규제 준수를 지원합니다. 파이프 테크의 DeltaV-Seal과 같은 전용 제품은 플랜지 연결부에 10년간의 타이트 가스 보증을 제공합니다. 액화천연가스 수출터미널에서의 채용이 가장 진행되고 있으며, 거기서는 다운타임 비용이 급속히 확대되고 있습니다. 중동과 북미의 중류 자산에 대한 자본 투자로 중동 시장은 에너지 인프라의 성장과 밀접하게 관련되어 있습니다.

공정의 고도화와 화학제품 포트폴리오의 확대로 인해, 씰재는 가혹한 용매, 산화제, 산에 노출되어 보다 높은 재료 적합성이 요구되고 있습니다. 유연한 흑연 씰은 현재 고온 반응기에서 최대 5,400°F까지 지원합니다. 제조업체는 기존 화합물을 공격하는 그린 케미컬 원료에 대한 퍼플로로 엘라스토머 블렌드를 조정합니다. 아시아의 새로운 석유화학 생산 능력에 대한 총 870억 달러의 투자 발표는 플랜트가 가동되면 대량의 정적·동적 씰이 필요하다는 것을 보여줍니다. 종합적인 공급업체는 설계된 씰링 세트와 예측 모니터링 모듈을 번들하여 미래 애프터마켓 계약을 잠급니다. 이러한 움직임으로 인해 화학기업이 탈탄소화를 진행해도 개스킷 및 씰 시장은 유지됩니다.

산업용 기계의 운전자는 운전 시간을 연장하기 위해 노력하고 있지만, 여전히 씰은 조기 마모를 피하기 위해 적절한 윤활에 의존합니다. 윤활유 고갈로 인한 베어링 고장은 여전히 가동 중지 시간의 가장 큰 원인이 되었습니다. SKF는 존 샘플 그룹의 윤활 사업 및 유량 관리 사업을 인수함으로써 이러한 격차를 해결하고 통합 윤활 프로그램을 제공합니다. 자체 윤활 설계는 존재하지만 초기 비용이 높기 때문에 고가치의 기계 이외에는 보급이 제한되어 있습니다. 소규모 가공 공장에서는 예방 유지보수가 지연되기 쉽고 운영자가 갑작스런 씰 누출에 노출됩니다. 이러한 정기적인 유지보수의 필요성은 유지보수가 필요없는 솔루션의 급속한 확장을 억제하고 최종 사용자에게는 운전 비용을 증가시킵니다.

씰은 2024년 매출의 67%를 차지했고 회전 기계 업그레이드와 전기자동차 플랫폼의 확대에 따라 2030년까지의 CAGR은 5.3%를 나타낼 것으로 예측됩니다. 펌프나 컴프레서용 샤프트 씰은 불안정한 에너지 시장이나 화학 시장에서 신뢰성 요건이 엄격해져 판매량이 크게 늘어납니다. 온도 측정치로부터 마찰력을 추측하는 소프트 센서 기술은 분해하지 않고 실시간 인사이트를 제공하여 서비스 비용 절감과 사용자 신뢰를 높입니다.

개스킷은 여전히 정적 조인트에 필수적이며 기술 혁신은 수소 파이프라인의 열 사이클을 견디는 전체 금속 설계에 중점을 둡니다. 일체형 DeltaV Seal Unit은 설치 후 토크 유지의 필요성을 없애고 시운전 작업을 간소화합니다. 이 하위 부문은 절대적인 수익으로 후진을 겪는 반면, 사업자가 프리미엄 제품으로 오래된 자산을 개조할 때마다 단가가 증가함에 따라 개스킷 및 씰 시장 가치가 상승합니다. 설비 제조업체는 견적시 개스킷 씰 키트를 지정하는 것이 증가하고 있으며, 상호 호환성을 확보하고 재주문의 복잡성을 최소화합니다.

금속은 2024년 개스킷 및 씰 시장 규모의 35%를 차지했습니다. 스테인레스 스틸 나선형 권선 개스킷과 인코넬 스프링 통전 씰은 가혹한 응용 분야에서 여전히 기본 옵션입니다. 그러나 고무 컴파운드는 CAGR 예측 6.3%로 가장 기세가 높습니다. TFE는 초저 마찰 밸브의 전략적 틈새를 유지하고 있지만, PFAS의 조사에 의해 개질 PEKK와 PEEK 블렌드의 병행 테스트가 추진되고 있습니다. 예측 기간 동안 금속 캐리어와 엘라스토머 오버레이를 결합한 혼합 재료 솔루션은 강성과 열팽창 차이에 대한 탄성의 균형을 유지하면서 점유율을 늘릴 것으로 예측됩니다.

제조업체 각 회사는 제품 라인을 재료 원산지별로 구분하고 사내 지속가능성 목표를 달성하기 위한 투명한 옵션을 구매자에게 제공합니다. 특히 유럽의 선도적인 구매자는 라이프 사이클 분석 임계 값을 입찰에 통합하고 생물 유래 함량을 검증 할 수있는 공급업체를 선호합니다. 이러한 역학은 개스킷 및 씰 시장 내 차별화를 촉진하고 문서화 된 탄소 세이브에 보상하는 가격 결정 회랑을 형성합니다.

아시아태평양은 2024년의 수익 점유율 47%로 개스킷 및 씰 시장을 독점했고, 2030년까지의 CAGR은 6.2%를 나타낼 전망입니다. 중국, 인도 및 동남아시아의 산업화 계획은 샤프트 씰과 개스킷 세트에 의존하는 대량의 회전 장비를 지원합니다. 인도에서는 석유화학 설비에 대한 정부의 우대조치가 새로운 수요에 박차를 가하고, 각 지역공급업체는 엄격한 현지 조달률 규칙에 맞추어 포트폴리오를 정돈하고 있습니다.

미국의 심해 탐사와 북미의 셰일 공정에서는 블로킹을 방지하기 위해 견고한 개스킷 재료가 필요하며 평균 판매 가격이 상승합니다. 퍼셉티브 대응 씰의 채용이 식품 가공이나 펄프·제지 공장에 퍼져 디지털·유지관리·플랫폼의 상업적 가치가 증명됩니다. 멕시코에서는 자동차산업이 확대되고 있으며, 무역협정에 의해 지역별 함유 기준이 강화된 것도 도와 대량의 몰드 씰을 흡수하고 있습니다.

유럽은 성숙하면서도 혁신 주도의 상황입니다. 자동차 제조업체는 내화성 배터리 모듈 개스킷을 추진하고 오프 하이웨이 장비 제조업체는 규제 기한을 이전에 PFAS가없는 유압 씰로 전환합니다.

The Gaskets And Seals Market size is estimated at USD 75.83 billion in 2025, and is expected to reach USD 92.31 billion by 2030, at a CAGR of 4.12% during the forecast period (2025-2030).

Robust demand from oil and gas, chemical processing, automotive electrification, and industrial automation will continue reinforcing steady expansion. Rapid material innovation, particularly in bio-based elastomers and PFAS-free compounds, removes performance trade-offs that once limited sustainable options. Digital monitoring transforms static components into data points, enabling predictive maintenance services that cut unplanned downtime and create new revenue streams. Manufacturers are responding with acquisitions in lubrication management and service agreements that lock in long-term aftermarket value. Supply chain pressures surrounding fluoro-rubber feedstocks are prompting dual-sourcing strategies and accelerated research into alternative chemistries, reducing vulnerability to price shocks.

The exploration of unconventional reserves and tighter safety rules is pushing operators to specify advanced sealing solutions that survive extreme pressures and aggressive media. Nitrile and Viton O-rings are now standard in blowout preventers and wellheads due to their strong chemical resistance. Mechanical seals that prevent fugitive emissions support regulatory compliance while reducing lost product and greenhouse-gas releases. Purpose-built products such as Pipeotech's DeltaV-Seal provide a 10-year gas-tight warranty for flange connections. Adoption is strongest in liquefied natural gas export terminals, where downtime costs escalate rapidly. Capital spending on midstream assets across the Middle East and North America keeps the gaskets and seals market firmly linked to energy infrastructure growth.

Process intensification and wider chemical portfolios expose sealing materials to harsher solvents, oxidizers, and acids, requiring greater material compatibility. Flexible graphite seals now support temperatures up to 5,400°F in high-temperature reactors. Manufacturers are tailoring perfluoroelastomer blends for green-chemistry feedstocks that attack legacy compounds. Investment announcements totaling USD 87 billion for new Asian petrochemical capacity indicate large volumes of static and dynamic seals will be needed once plants come online. Integrated suppliers bundle engineered sealing sets with predictive monitoring modules, locking in future aftermarket contracts. Together, these moves sustain the gaskets and seals market even as chemical companies decarbonize.

Industrial operators strive to extend runtimes, yet seals still rely on correct lubrication to avoid premature wear. Bearing failures linked to lubricant starvation remain a top cause of downtime. SKF addressed this gap by acquiring John Sample Group's lubrication and flow-management businesses to deliver integrated lubrication programs. Although self-lubricating designs exist, higher upfront costs limit widespread adoption outside high-value machinery. Smaller processing plants often delay preventive maintenance, exposing operators to sudden seal leaks. This need for routine service restrains rapid scaling of maintenance-free solutions and adds operating cost for end-users.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Seals held 67% of 2024 revenue and are projected to post a 5.3% CAGR through 2030 as rotating machinery upgrades and electric-vehicle platforms expand. Shaft seals for pumps and compressors see strong unit growth because reliability requirements tighten in volatile energy and chemical markets. Soft-sensor technology that infers friction power from temperature readings offers real-time insight without disassembly, lowering service costs and boosting user confidence.

Gaskets remain integral to static joints, and innovation is focused on all-metal designs that withstand thermal cycling in hydrogen pipelines. One-piece DeltaV-Seal units eliminate the need for torque retention after installation, simplifying commissioning tasks. Although this sub-segment trails in absolute revenue, higher unit pricing lifts gaskets and seals market value whenever operators retrofit older assets with premium products. Equipment builders increasingly specify gasket-seal kits during quoting, ensuring cross-compatibility and minimizing reorder complexity.

Metals contributed a 35% share of the gaskets and seals market size in 2024. Stainless steel spiral-wound gaskets and Inconel spring-energized seals remain default choices for severe service. However, rubber compounds show the fastest momentum with a 6.3% CAGR forecast. TFE maintains a strategic niche for ultra-low friction valves, but PFAS scrutiny drives parallel testing of modified PEKK and PEEK blends. Over the forecast window, mixed-material solutions that pair metal carriers with elastomer overlays are expected to gain share, balancing rigidity and elasticity for differential thermal expansion.

Manufacturers segment product lines by material origin, granting buyers transparent options to meet internal sustainability targets. Large buyers, especially in Europe, embed life-cycle analysis thresholds into tenders, which favors suppliers able to validate bio-attributed content. These dynamics increase differentiation inside the gaskets and seals market and create pricing corridors that reward documented carbon savings.

The Gaskets and Seals Market Report Segments the Industry by Product (Gaskets and Seals), Material (Fiber, Graphite and Flexible Graphite, and More), Sales Channel (OEM and After-market/MRO), Application (Aerospace and Defense, Automotive OEM, Electronics, Oil and Gas, Power Generation, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Asia-Pacific dominated the gaskets and seals market with a 47% revenue share in 2024 and is tracking 6.2% CAGR to 2030. Industrialization programs in China, India, and Southeast Asia underpin large volumes of rotating equipment that rely on shaft seals and gasket sets. Government incentives in India for petrochemical capacity spur fresh demand, and regional suppliers align portfolios with strict local content rules.

The United States' deepwater exploration and shale processing in North America need robust gasket materials to prevent blowouts, raising average selling prices. Adoption of Perceptiv-enabled seals spreads across food processing and pulp and paper mills, proving the commercial value of digital maintenance platforms. Mexico's expanding automotive clusters absorb high-volume molded seals, aided by trade agreements that tighten regional content thresholds.

Europe presents a mature yet innovation-driven landscape. Automakers push fire-resistant battery-module gaskets while off-highway equipment producers convert to PFAS-free hydraulic seals ahead of regulatory deadlines.