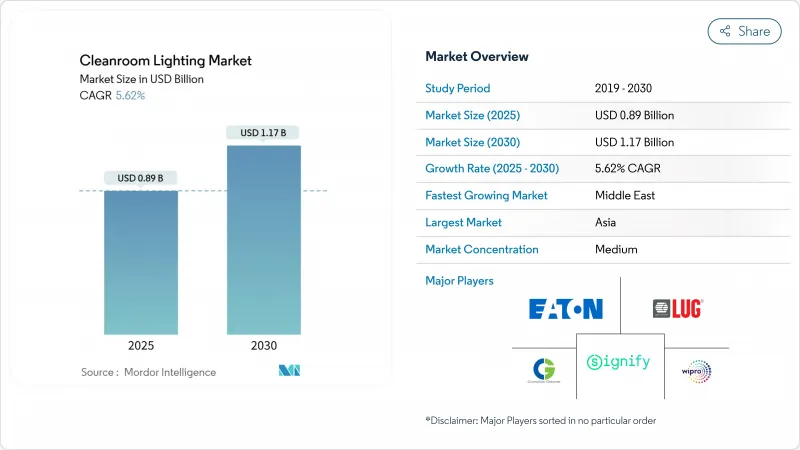

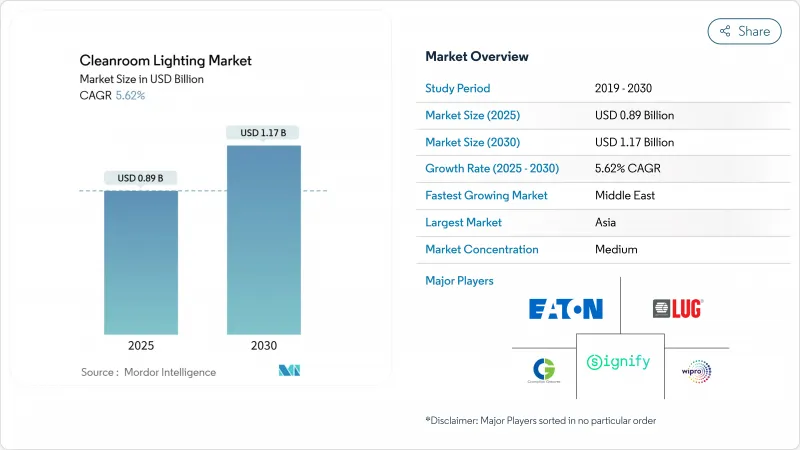

클린룸 조명 시장 규모는 2025년 8억 9,000만 달러로 추정되고, 2030년 11억 7,000만 달러에 이를 전망이며, CAGR 5.62%로 성장할 것으로 예측됩니다.

반도체 공장, 바이오제약실, 첨단연구실에서의 오염관리 요건의 고조가 현재 수요를 지지하는 한편, EU의 에코디자인 규칙 및 북미의 형광등 금지령에 의한 적극적인 LED 개수가 5년간의 전망을 강화합니다. 반도체 제조업체가 여전히 가장 큰 구매자임에 변함이 없지만, 생물학적 제제 및 세포 치료 사업자는 섬세한 세포 배양을 위해 깜박임이 없는 밀폐형 조명기구를 표준화하고 있기 때문에 그 차이를 줄이고 있습니다. UV-C 일체형 LED 기구의 채용은 팬데믹 후 감염 제어의 우선순위를 반영하여 병원과 제약회사의 아이솔레이터에서 기세를 늘리고 있습니다. 공급면에서 평판이 좋은 조명 브랜드 간의 수직 통합은 원재료의 변동과 인증 비용의 상쇄에 도움이 되는 한편, 틈새 전문 기업은 위험 장소와 먼 UV-C 분야에서 두각을 나타내고 있습니다.

EU의 GMP Annex 1 요건이 개정되어, 무균 의약품 제조실 전체의 미립자 규제가 강화됨에 따라, 오퍼레이터는 기존의 형광등을, 탈락을 최소화하고 강력한 소독제를 견디는 IP65의 밀폐형 LED 패널로 교체할 필요가 있습니다. 계약 제조자, 백신 제조자 및 신흥 유전자 치료 기업은 모두 유럽 연합(EU)에서 시장 접근을 보장하기 위해 교환 주기를 진행하고 있습니다.

대만, 일본, 중국 본토의 극단적 자외선 리소그래피 라인에 대한 기록적인 설비 투자로 ISO 클래스 1 환경에서 동작할 수 있는 ULPA 필터가 장착된 EUV 대응 조명기구에 대한 수요가 높아지고 있습니다. 남아과기의 96억 달러의 더블 데크 공장은 이러한 프로젝트의 전형이며, 조명 패키지는 엄격한 스펙트럼 및 밀봉 기준을 충족하기 위해 조기에 지정되었습니다.

저가스 방출 알루미늄 합금 및 클린룸 등급 폴리카보네이트의 상품 가격의 급격한 변동은 재료비를 늘리고 고정 가격 프로젝트 계약에 부담을 줍니다. 공급업체의 수가 제한되어 비용에 대한 민감도가 높아지며 수직 통합 조명 브랜드는 원재료의 전면 구매와 하우징의 재 설계를 강요합니다.

LED는 2024년 수익의 80.4%를 차지하였고, 형광등과 무전극 기술을 크게 웃돌았습니다. UV 하위 부문은 현재 겸손하지만, 원자외 UVC와 살균 LED가 조명과 살균을 융합시켜 8.7%의 성장률로 추이하고 있습니다. 에너지 효율의 의무화, 즉각적인 디밍 기능, 뛰어난 색 안정성이 LED 선호도를 지원하고 스마트 센서 패키지는 ISO 클래스 공간의 예지 보전을 가능하게 합니다.

2세대 LED는 밀폐된 석영창 뒤에 222nm 이미터를 내장하고 있어, 실내를 배기하지 않고 연속적인 살균이 가능합니다. 이 이중 기능을 통해 천장 그리드의 혼잡을 완화하면서 기구의 ASP를 높일 수 있습니다. 형광등은 2025년에 시행되는 EU의 에코디자인 금지령의 제약을 받아 단계적으로 폐지되는 레트로핏 틈새에 쫓기고 있습니다. 프리미엄 UV-C 제품이 확대됨에 따라 LED 기반 솔루션의 클린룸 조명 시장 규모는 2030년까지 10억 달러 이상에 달할 것으로 예측됩니다.

패널 및 트로퍼 조명기구는 2024년 매출의 45.1%를 차지했으며, 선반과 입자 트랩을 최소화하는 플래시 마운트를 지원합니다. 퀵 디스커넥트 기어 트레이를 갖춘 모듈식 패널 시스템은 검증 사이클을 단축하고 개스킷 교환을 간소화하며 낭비 없는 시설 관리 목표에 부합합니다.

위험 장소용 픽스처는 현재 한 자리수 중반의 점유율에 불과하지만 CAGR 6.5%로 전진하고 있습니다. 제약용제실이나 리튬 전지 라인에서는 ATEX, IECex, NEC의 인증을 받은 존 1/디비전 1의 LED가 지정되어 있습니다. 인증제품 공급 압박은 기존 벤더의 마진을 높이고 방폭 라인을 제공하는 벤더의 클린룸 조명 시장 점유율을 밀어 올리고 있습니다.

아시아태평양은 대만, 일본, 한국, 중국 연안부에서의 반도체 집적 덕분에 2024년 매출의 27.8%를 차지해 최대 지역을 유지했습니다. TSMC의 구마모토 합작 사업과 남아의 New Taipei City 메가팹 등의 프로젝트가 다년간의 조명 패키지 파이프라인을 확보하고 있습니다. 태양전지 제조업체도 헤테로접합 태양전지 모듈용 ISO 7 셀을 표준화하여 신재생 에너지 공급망에 대응 가능한 수요를 확대하고 있습니다. 인도는 단편적이고 가격에 민감한 하위 시장으로 부상하고 있으며 현지 OEM과의 제휴가 보급을 가속화할 수 있습니다.

중동은 헬스케어 민영화 및 백신 자급 프로그램이 대규모 병원과 제약 회사의 복합 시설을 촉진하기 때문에 2030년까지 연평균 복합 성장률(CAGR) 6.7%로 성장을 이끌 전망입니다. 리야드와 아부다비에서의 원자외선 살균 장치의 도입은 이 지역이 프리미엄 감염 제어 솔루션에 자금을 공급할 준비가 되어 있음을 뒷받침합니다. 사우디아라비아의 바이오 제약 공장에서는 솔벤트 취급과 관련된 위험 지역에서의 수주가 이 지역의 수익을 더욱 밀어올리고 있지만 인증 제품 부족으로 프로젝트 이정표가 지연될 수 있습니다.

북미는 견조한 생물제제 파이프라인과 CHIPS 및 과학법 하에서 부활한 웨이퍼 팹 건설의 혜택을 누리고 있습니다. Fujifilm의 North Carolina의 확장 공사는 새로운 바이오 제조 캠퍼스에서 높은 사양 조명 수요를 보여줍니다. 공인 전기 기술자의 노동력 부족이 단기적인 병목 현상이지만 기존 하우징의 절반으로 설치할 수 있는 모듈식 패널 시스템이 일정 위험을 완화합니다. 2025년에 T8 형광등을 폐지하는 에코디자인 규칙이 계기가 된 유럽의 레트로핏의 물결은 매크로적인 불확실성이 그린필드에 대한 지출을 억제하는 중에서도, 안정된 리플레이스 수입을 가져옵니다. 북유럽 국가, 독일, 프랑스는 ISO와 GMP의 추적성을 요구하는 컴플라이언스 리더로 지속적으로 확립된 인증 보유자를 우대하고 있습니다.

The cleanroom lighting market size stood at USD 0.89 billion in 2025 and is forecast to reach USD 1.17 billion by 2030, advancing at a 5.62% CAGR.

Heightened contamination-control requirements in semiconductor fabs, biopharmaceutical suites, and advanced research labs anchor current demand, while aggressive LED retrofits driven by EU EcoDesign rules and North American fluorescent bans reinforce the five-year outlook. Semiconductor manufacturers remain the single largest buyers, yet biologics and cell-therapy operators are closing the gap as they standardize flicker-free, sealed luminaires for sensitive cell cultures. Uptake of UV-C-integrated LED fixtures is gaining momentum in hospitals and pharmaceutical isolators, reflecting post-pandemic infection-control priorities. On the supply side, vertical integration among established lighting brands is helping offset raw-material volatility and certification costs, whereas niche specialists are finding headroom in hazardous-location and Far-UVC segments.

Revised EU GMP Annex 1 requirements tighten particulate limits across sterile drug-manufacturing suites, forcing operators to swap legacy fluorescents for sealed IP65 LED panels that minimize shedding and withstand aggressive sanitizing agents. Contract manufacturers, vaccine producers, and emerging gene-therapy firms are all advancing replacement cycles to safeguard market access in the European Union.

Record capital outlays for extreme-ultraviolet lithography lines in Taiwan, Japan, and mainland China are driving demand for ULPA-filtered, EUV-compatible luminaires able to operate in ISO Class 1 environments. Nanya Technology's USD 9.6 billion double-deck fab typifies these projects, with lighting packages specified early to meet rigorous spectral and sealing criteria.

Rapid swings in commodity prices for low-outgassing aluminum alloys and cleanroom-grade polycarbonates inflate bills of material and strain fixed-price project contracts. Limited supplier pools amplify cost sensitivity, compelling vertically integrated lighting brands to forward-buy raw materials or redesign housings.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

LEDs anchored 80.4% of 2024 revenue within the cleanroom lighting market, far outstripping fluorescent and induction technologies. UV sub-segments, although modest today, are growing at an 8.7% clip as Far-UVC and germicidal LEDs merge illumination and disinfection. Energy-efficiency mandates, instant-dimming capability, and superior color stability underpin LED preference, with smart-sensor packages enabling predictive maintenance for ISO-classified spaces.

Second-generation LEDs integrate 222 nm emitters behind sealed quartz windows, allowing continuous sterilization without room evacuation. This dual-functionality increases fixture ASPs while shrinking ceiling-grid congestion. Fluorescents, constrained by EU EcoDesign bans taking force in 2025, are relegated to retrofit niches set for phased retirement. As premium UV-C products scale, the cleanroom lighting market size for LED-based solutions is forecast to exceed USD 1 billion by 2030.

Panel and troffer luminaires represented 45.1% of 2024 revenue, favored for flush mounting that minimizes ledges and particle traps. Modular panel systems with quick-disconnect gear trays shorten validation cycles and simplify gasket replacement, aligning with lean facility-management goals.

Hazardous-location fixtures, though only a mid-single-digit share today, are advancing at 6.5% CAGR. Pharmaceutical solvent suites and lithium-battery lines specify Zone 1/Division 1 LEDs certified under ATEX, IECEx, or NEC. Supply tightness in certified products raises margins for incumbents, boosting the cleanroom lighting market share of vendors offering explosion-proof lines.

The Clean Room Lighting Market Report is Segmented by Light Source (LED, Fluorescent, and More), Fixture Design/Form Factor (Panel/Troffer, Wrap-around/Strip, and More), Mounting Type (Recessed, Surface, and Pendant/Suspended), End-User Industry (Semiconductor and Electronics, Healthcare and Life Sciences, and More), Sales Channel (Direct OEM, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific remained the largest territory, holding 27.8% of 2024 revenue thanks to dense semiconductor clustering in Taiwan, Japan, Korea, and coastal China. Projects such as TSMC's Kumamoto joint venture and Nanya's New Taipei City megafab secure multi-year lighting-package pipelines. Photovoltaic manufacturers are also standardizing ISO 7 cells for heterojunction solar modules, extending addressable demand into renewable-energy supply chains. India is emerging as a fragmented, price-sensitive sub-market where local OEM alliances can accelerate penetration.

The Middle East leads growth at 6.7% CAGR through 2030 as healthcare privatization and vaccine self-sufficiency programs drive large hospital and pharma complexes. Far-UVC deployments in Riyadh and Abu Dhabi underscore the region's readiness to fund premium infection-control solutions. Hazardous-location orders tied to solvent handling in Saudi biopharma plants further buoy regional revenue, though scarcity of certified products can delay project milestones.

North America benefits from a robust biologics pipeline and resurgent wafer-fab construction under the CHIPS and Science Act. Fujifilm's North Carolina expansion exemplifies high-spec lighting demand in new biomanufacturing campuses. Labor shortages among certified electricians present a short-term bottleneck, yet modular panel systems that install in half the time of legacy housings mitigate schedule risk. Europe's retrofit wave, catalyzed by EcoDesign rules that shutter T8 fluorescents in 2025, provides steady replacement revenue even as macro uncertainty tempers greenfield spending. Nordic countries, Germany, and France remain compliance leaders, requiring ISO and GMP traceability that favors established certificate holders.