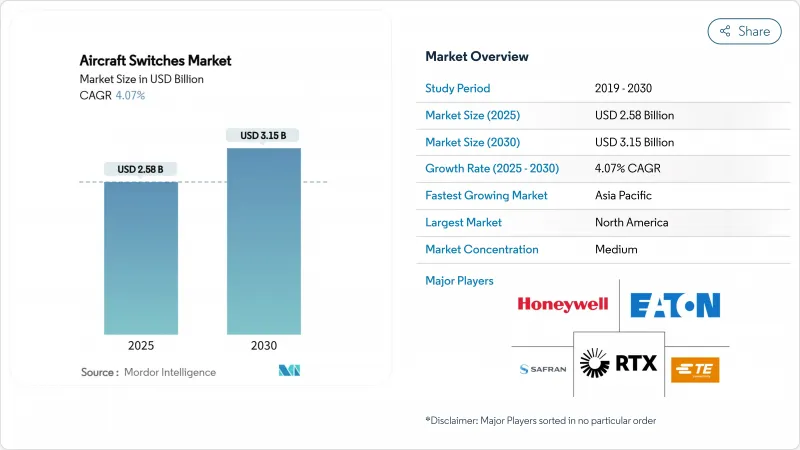

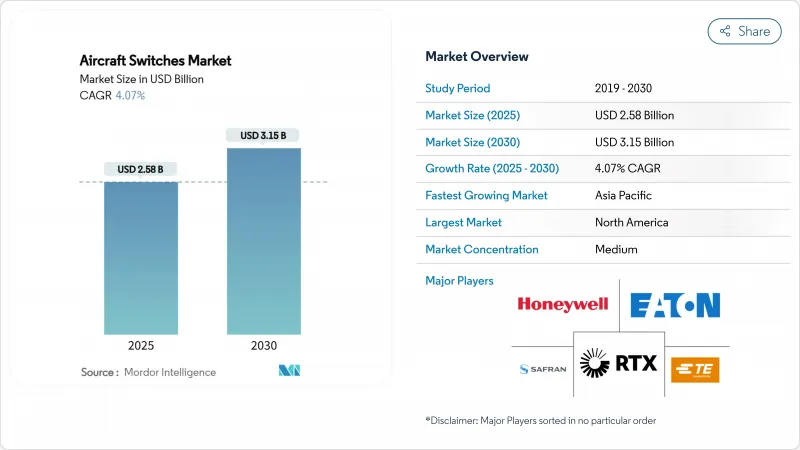

항공기 스위치 시장 규모는 2025년에 25억 8,000만 달러로 평가되고, 2030년에는 31억 5,000만 달러로 확대되며 CAGR 4.07%를 나타낼 것으로 예측됩니다.

이 궤적은 전기 서브시스템이 전통적인 기계 부품 및 유압 부품을 대체하고 항공기 전체의 스위칭 포인트 수를 증가시키는 전동화 아키텍처에 대한 항공 부문의 꾸준한 축족을 반영합니다. 항공사의 기체 갱신 스케줄과 국방 근대화 프로그램에 의해 2024년부터 2025년 초에 걸쳐, 민간과 군용의 양 플랫폼에 일관된 주문의 흐름이 확보되었습니다. 솔리드 스테이트 파워 컨트롤러, 실리콘 카바이드 디바이스, 진단 기능 내장의 스마트 스위치가 주류가 되어, 이산적인 전기 기계 부품으로부터, 예지 보전 통합이 가능한 소프트웨어 정의의 데이터 공유 모듈로 중점이 옮겨졌습니다. 공급업체의 선택 기준에는 사이버 보안 컴플라이언스와 공급망의 무결성이 점점 더 포함되고 있으며, 중견 공급업체는 인증 업그레이드에 투자하거나 선도 기업의 통합 제안을 수락할 수 없게 되었습니다. 지역별로는 북미가 지속적인 국방 지출로 매출을 이끌고 있습니다. 그러나 중국과 인도가 항공기 생산과 MRO의 능력 확대를 가속화 했기 때문에 아시아태평양은 가장 빠른 성장을 기록했습니다.

항공 아키텍처는 2024년 노후화된 단일 통로 항공기의 업데이트를 가속화하고 배전 및 비행 데크 제어에 고밀도 스위칭 네트워크가 필요한 전기 아키텍처를 지정했습니다. 보잉의 B777X 인증 획득을 위한 노력과 에어 인디아의 대형 멀티 오더 패키지는 신규 납품 때마다, 콕피트, 어비오닉 베이, 객실 존에 걸치는 스위치의 번들 설치가 어떻게 행해졌는지를 전형적으로 나타내고 있습니다. 오퍼레이터는 20년의 기체 수명에 걸쳐 소프트웨어 업그레이드에 대응할 수 있는 향후 하드웨어를 요구하고, 헬스 모니터링 출력을 갖춘 구성 가능한 솔리드 스테이트 유닛을 제공하는 공급업체를 선호했습니다.

항공기 전기는 2차 시스템에서 고전력 작동 라인으로 확장되었으며 스위치 정격은 500A 및 1,000V를 초과했습니다. Collins Aerospace는 Clean Aviation SWITCH 프로그램 하에서 메가와트급 전력 분배 모듈을 프로토타입하여 연속 고온 작동에 대응하는 실리콘 카바이드 장치를 검증했습니다. 하니웰의 실리콘 온 절연체 CMOS 공정은 300°C 정격 구성요소를 지원하여 전력 변환 베이를 엔진에 가깝게 하여 하네스의 무게를 줄일 수 있게 했습니다. 이러한 발전은 플랫폼 OEM이 분산형 전기 추진 개념으로 전환하면서 항공기 스위치 시장을 지원했습니다.

FAA와 EASA의 엔지니어링 부문은 사이버 보안 및 소프트웨어 보증 심사가 심화됨에 따라 안건 체류에 직면해 구성 요소 인가 리드 타임이 12개월에서 24개월 이상으로 늘어났습니다. 보잉의 B777X 프로그램의 지연은 생산 릴리즈를 확정하기 위한 형식 인증 데이터를 기다리는 Tier-1 및 Tier-2 공급업체에 연쇄적인 영향을 미쳤습니다. 전임 인증 팀이없는 소규모 스위치 공급업체는 라인 맞춤 위치를 잃을 위험이 있으며 항공기 스위치 시장 전체의 기세를 약화시킵니다.

조종석 스위치는 파일럿이 비행에 필수적인 작업을 촉각 푸시 버튼, 가드 토글, 회전식 셀렉터에 의존하고 있었기 때문에 2024년 매출의 35.65%를 유지했습니다. 디스플레이 및 데이터 버스에 장애가 발생하면 레귤레이터는 물리적 백업 제어 라인을 필요로 하기 때문에 수동 설계가 주류였습니다. 이 부문은 표준화된 오버헤드 패널로 통합이 간소화되었으며 단위당 비용이 낮아진 단일 통로 항공기의 지속적인 납품으로 이익을 얻었습니다.

2030년까지의 CAGR 예측에서는 항공전자공학 설치가 가장 빠른 5.04%를 나타낼 전망입니다. 다기능 디스플레이, 비행 관리 컴퓨터 및 건강 모니터링 장치에는 이더넷 기반 백본으로 연결된 고밀도, 저 바운스 자동 릴레이가 필요했습니다. 항공사는 사용 데이터를 예측 유지보수 플랫폼으로 스트리밍하는 스마트 스위치를 통합하여 파견의 신뢰성을 향상시켰습니다. 전반적으로, 아비오닉스의 성장은 통합형 모듈식 아비오닉스 스위트 항공기 스위치 시장 규모 증가를 지원했습니다.

2024년 매출의 65.40%는 수동식 유닛으로 명확한 촉각 확인과 간단한 라인 유지보수를 위해 선호되는 푸시 버튼 어셈블리가 견인되었습니다. 로커 유형은 디자인 언어와 조명 효과에 의해 승객의 지각을 향상시키는 객실의 포지션을 획득했습니다. 수동 수요는 제조 규모의 이점과 여러 함대에 걸쳐 안정적인 교체 부품 수를 유지했습니다.

자동 스위치는 전기화 아키텍처가 전기 기계식 접촉기를 솔리드 스테이트 컨트롤러로 대체하기 때문에 CAGR 5.91%에서 상승할 것으로 예측됩니다. 아크 프리 반도체 경로와 기계적 리던던시를 결합한 하이브리드 릴레이가 연속 생산을 시작하여 저전압 강하와 페일 세이프의 위치 결정을 조합했습니다. 각 배전센터에는 기존의 브레이커를 대신해 지능적으로 어드레싱 가능한 스위치가 수십개 설치되어, 이 전환이 항공기 스위치 시장을 확대하고 있습니다.

북미는 종합적인 방어 예산과 활발한 상업 생산 라인에 힘입어 2024년 매출의 37.80%를 차지했습니다. 보잉, 하니웰, 커티슬라이트, 이튼이 이 지역공급업체 생태계를 지원하고 FAA 인증 전문 지식이 미국 내 프로그램 승인을 집중시켰습니다. NGAD와 헬리콥터 업그레이드를 위한 100억 달러 이상의 계약이 있었고, 전투기, 유조선, 회전익기 카테고리에 걸쳐 일관된 스위치 수요가 확보되었습니다.

CAGR 5.60%로 확대가 예상되는 아시아태평양은 중국의 MRO 밸류체인 상승과 인도 항공기 수주 급증으로 혜택을 받았습니다. 에어버스는 중국 서비스 부문이 2043년까지 610억 달러에 이르렀고 정비가 83%를 차지할 것으로 예측했습니다. 인도 정부는 공항 확장을 위해 120억 달러를 기록하고 현지 부품 생산을 장려했기 때문에 Eaton과 SIAEC의 제휴에서 볼 수 있듯이 서유럽 공급업체는 합작 회사를 설립하게 되었습니다. 이 지역의 국산화 중시의 자세는 중견 제조업체에게 기술의 라이선스 공여와 국산 부품 할당을 획득할 기회를 제공했습니다.

유럽은 에어버스 조립, GCAP 하에서의 방위 협력, EU의 기후 변화 기금에 지원된 R&D 프로젝트에 지지되어 안정을 유지했습니다. 프랑스와 아일랜드에서 열린 콜린스 에어로스페이스의 Clean Aviation SWITCH 프로토타입은 하이브리드 전기 실증기의 고전압 배전 전략을 검증하고 지역의 지적 재산권을 향상시켰습니다. 동시에 EASA의 사이버 보안 의무화는 인증 복잡성을 높이고, 사내에 컴플라이언스 리소스를 가진 공급자를 우대하고, 항공기 스위치 시장에서 적당한 진입 장벽을 유지했습니다.

The aircraft switches market size was valued at USD 2.58 billion in 2025 and is forecasted to expand to USD 3.15 billion by 2030, advancing at a 4.07% CAGR.

This trajectory mirrors the aviation sector's steady pivot toward more-electric architectures, where electrical subsystems replace legacy mechanical and hydraulic components, multiplying the number of switching points across each airframe. Airlines' fleet-renewal schedules and defense modernization programs ensured a consistent order flow for both commercial and military platforms in 2024 and early 2025. Solid-state power controllers, silicon-carbide devices, and smart switches with built-in diagnostics became mainstream as the emphasis shifted from discrete electromechanical parts to software-defined, data-sharing modules capable of predictive maintenance integration. Vendor selection criteria increasingly include cybersecurity compliance and supply-chain integrity, forcing mid-tier suppliers either to invest in certification upgrades or accept consolidation offers from larger peers. Across regions, North America retained the revenue lead owing to sustained defense spending. Yet, Asia-Pacific posted the fastest growth as China and India accelerated aircraft production and MRO capacity expansion.

Airlines accelerated replacement of aging single-aisle fleets in 2024, specifying electrical architectures that require denser switching networks for power distribution and flight-deck controls. Boeing's B777X certification effort and Air India's large multitype order packages typified how every new delivery triggered bundled switch installations spanning cockpit, avionic bay, and cabin zones.Operators insisted on future-proof hardware able to accommodate software upgrades across the 20-year airframe life, favoring suppliers offering configurable solid-state units with health-monitoring outputs.

Aircraft electrification expanded from secondary systems to high-power actuation lines, pushing switch ratings beyond 500A and 1,000V. Collins Aerospace prototyped megawatt-class power-distribution modules under the Clean Aviation SWITCH program, validating silicon-carbide devices for continuous high-temperature operation. Honeywell's silicon-on-insulator CMOS processes supported components rated to 300°C, enabling power-conversion bays to migrate closer to engines and reducing harness weight. These advances underpinned the aircraft switches market as platform OEMs shifted to distributed electrical propulsion concepts.

FAA and EASA engineering directorates faced case backlogs as cybersecurity and software assurance reviews deepened, stretching component approval lead times from 12 months to more than 24 months. Boeing's B777X program delays highlighted the cascading impact on tier-1 and tier-2 suppliers waiting for type-certification data to finalize production release. Smaller switch vendors lacking dedicated certification teams risked losing line-fit positions, tempering overall aircraft switches market momentum.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cockpit switches retained 35.65% of 2024 revenue as pilots relied on tactile pushbuttons, guarded toggles, and rotary selectors for flight-critical tasks. Manual designs dominated because regulators required physical backup control lines in case of display or data bus failure. The segment benefited from sustained deliveries of single-aisle aircraft, where standardized overhead panels simplified integration and lowered per-unit costs.

Avionics installations generated the fastest 5.04% CAGR forecast through 2030. Multi-function displays, flight-management computers, and health-monitoring units demanded high-density, low-bounce automatic relays linked over Ethernet-based backbones. Airlines embedded smart switches that streamed usage data into predictive-maintenance platforms, improving dispatch reliability. Overall, avionics growth supported incremental additions to the aircraft switches market size for integrated modular avionics suites.

Manual units supplied 65.40% revenue in 2024, led by pushbutton assemblies preferred for clear tactile affirmation and straightforward line maintenance. Rocker variants won cabin positions where design language and illumination effects improved passenger perception. Manual demand preserved manufacturing economies of scale and stable replacement part numbers across multiple fleets.

Automatic switches are projected to climb at a 5.91% CAGR as more-electric architectures substitute electromechanical contactors with solid-state controllers. Hybrid relays that pair arc-free semiconductor paths with mechanical redundancy entered serial production, combining low voltage drop with fail-safe positioning. This migration enlarges the aircraft switches market as each power-distribution center now contains dozens of intelligent, addressable switches instead of a handful of legacy breakers.

The Aircraft Switches Market Report is Segmented by Application (Cockpit, Cabin, Engine and Power Auxiliary Power Unit (APU), Avionics, and Others), Switch Type (Manual and Automatic), Platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft, and Unmanned Aerial Vehicles), End User (OEM and Aftermarket), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 37.80% of 2024 revenue, underpinned by comprehensive defense budgets and active commercial production lines. Boeing, Honeywell, Curtiss-Wright, and Eaton anchored the regional supplier ecosystem, while FAA certification expertise concentrated program approvals within the United States borders. Several USD 10 billion-plus contracts for NGAD and helicopter upgrades ensured consistent switch demand across fighter, tanker, and rotorcraft categories.

Asia-Pacific, forecast to expand at 5.60% CAGR, benefited from China's climb up the MRO value chain and India's surging aircraft orders. Airbus projected China's services segment to reach USD 61 billion by 2043, with maintenance representing 83%-a switch-intensive activity. India's government earmarked USD 12 billion for airport expansion and encouraged local component production, prompting Western suppliers to establish joint ventures, as seen in Eaton's partnership with SIAEC. The region's focus on indigenization opened opportunities for mid-sized players to license technology and capture domestic content quotas.

Europe remained stable, supported by Airbus assembly, defense cooperation under GCAP, and R&D projects backed by EU climate funds. Collins Aerospace's Clean Aviation SWITCH prototypes in France and Ireland validated high-voltage distribution strategies for hybrid-electric demonstrators, elevating regional intellectual-property stakes. Simultaneously, EASA's cybersecurity mandates heightened certification complexity, favoring suppliers with in-house compliance resources and thus maintaining moderate barriers to entry within the aircraft switches market.