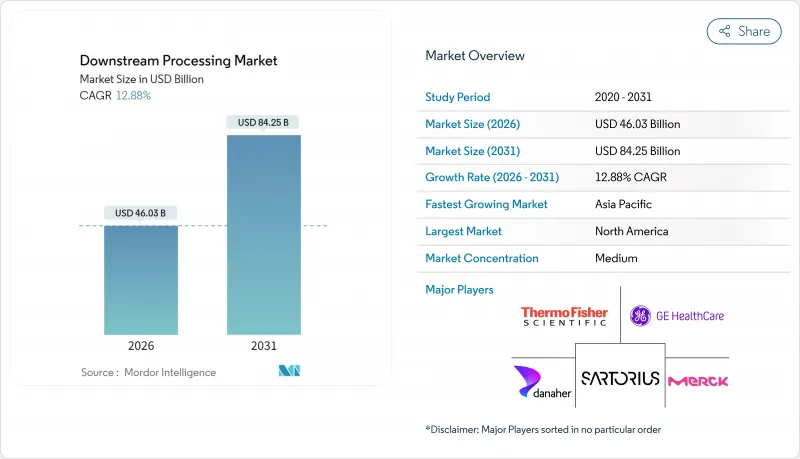

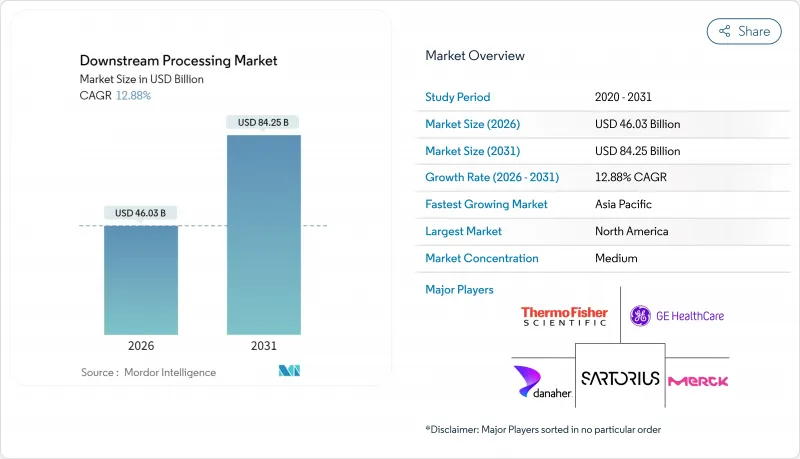

세계의 다운스트림 가공 시장은 2025년 407억 8,000만 달러에서 2026년까지 460억 3,000만 달러로 성장하고, 2026년부터 2031년까지는 CAGR 12.88%로 성장을 지속하여 842억 5,000만 달러에 달할 것으로 예측됩니다.

2024년부터 2025까지, Eli Lilly의 90억 달러 규모 인디애나주 사이트나 Novo Nordisk의 41억 달러 규모 노스캐롤라이나주 시설 등, 총액 500억 달러를 넘는 생산 능력 확장이 실시되어, 지금까지 없었던 설비 수요를 만들어 숙련 노동자에 대한 경쟁 일회용 시스템, 연속 바이오프로세싱, 디지털 트윈이 주류가 되어 운영비용 절감과 검증 기간의 단축을 실현하는 한편, 공급업체는 신규제 발효 전에 PFAS 규제 대응막의 도입을 서두르고 있습니다. CDMO가 바이러스 벡터나 지질 나노입자 생산과 같은 틈새 모달리티를 위해 다년간의 생산 프레임을 확보하는 가운데 아웃소싱의 기세가 가격 형성과 기술 도입을 더욱 견인하고 있습니다. 한편, 제조업체는 공급망의 탄력성을 최우선으로 하고, 필터, 가방, 수지 등의 지역 조달 전략과 이중 공급자 체제를 추진하고 있습니다.

Samsung Biologics는 2025년 4월 제5공장을 완성시켜 세계 생산능력을 78만 4,000리터로 확대했습니다. 이로 인해 생산량 경쟁이 치열해지고 대규모 크로마토그래피 시스템과 일회용 생물 반응기 수요가 증가하고 있습니다. 신설 라인에서는 연속 생산 방식이 주류가 되어, 완충액 소비량을 최대 40% 삭감해, 주사용수의 필요량을 저감하고 있습니다. 지역 정부는 바이오 제조를 전략적 성장 엔진으로 자리매김하고 있으며, 사우디아라비아가 2040년까지 비석유 GDP를 346억 달러 증가할 계획이 그 예입니다. 일부 CDMO(수탁개발제조기관)의 생산 능력 과잉 공급에 의해 가동률은 일시적으로 50%를 밑돌고 있지만, 집약화된 다운스트림 공정 스키드의 처리량 유연성에 의해 품질을 손상시키지 않고 신속한 재스케줄이 가능합니다. 이 때문에 벤더 각사는 컬럼, 수지, 분석용 센서를 번들한 통합 플랫폼을 제공해, 단일클론항체 제품과 바이러스 벡터 제품을 몇 시간 이내로 전환할 수 있도록 하고 있습니다.

대기업은 예산을 늘리는 반면 중소기업은 자본 배분 제약에 직면하고 있습니다. Eli Lilly는 임상 공급을 가속화하기 위해 'Lilly Medicine Foundry'에 45억 달러를 단독으로 할당하여 모듈형 크로마토그래피 및 탄젠트 플로우 여과 시스템에 대한 추가 주문을 만들었습니다. 벤처 자본에 의한 스타트업 기업은 세포 및 유전자 치료 파이프라인을 우선적으로 추진하고 있으며, 이는 항체 워크플로우와는 크게 다른 저전단력에 의한 청징화 및 뉴클레아제 제거 공정이 요구됩니다. 그 결과, 수요의 다양화가 진행되고, 구성 변경 가능한 스키드나 일회용 플로우 패스를 제공하는 공급자에게 장점이 탄생하고 있습니다. 한때 틈새 기술이었던 연속 다중 컬럼 크로마토그래피는 제품 1kg당 수지 사용량을 50% 절감하여 수지 비용의 급등을 상쇄할 수 있기 때문에 채용 프로그램이 증가하고 있습니다.

단백질 A 수지는 여전히 높은 가격대를 유지하고 있으며 다운스트림 공정의 자본 예산의 최대 60%를 차지합니다. 퓨로라이트는 공급 안정화와 가격 변동 억제를 위해 펜실베니아 공장에 2억 달러를 투자했지만 중소기업은 여전히 비용 제약에 직면하고 있습니다. 다단 컬럼 작업을 강화하면 수지 사용량이 50% 줄어들어 면적당 생산성이 향상되지만, 훈련된 직원을 필요로 하는 자동화의 복잡성이 더해집니다. 양극화된 시장이 형성되고 있으며, 대기업 제약 기업은 고부가가치 포착 수지를 구입하는 반면, 비용에 중점을 둔 기업은 혼합 모드와 연속 처리의 대체 기술을 탐구하고 있습니다.

2025년 다운스트림 공정 시장의 수익 구성비에서는 정제 기술이 32.05%를 차지하고 바이오 의약품 품질 관리에 있어서 핵심적인 역할을 뒷받침하고 있습니다. 세포 파쇄 기술은 미생물 발현 시스템이나 세포내 발현 시스템의 보급에 따라 14.88%라는 가장 높은 CAGR을 기록하고 있습니다. 정제분야의 다운스트림 가공 시장 규모는 2026년 147억 5,000만 달러를 넘어 수지 용량 확대와 멀티 컬럼 기술 혁신을 배경으로 2031년까지 270억 달러를 돌파할 전망입니다. 한편, 균질화기와 마이크로플루이다이저는 세포 파쇄의 주력장치로 계속되고 있지만, 발열을 저감하는 저주파 음향법이 파일럿 스케일 시험에서 주목을 받고 있습니다.

연속 크로마토그래피는 완충액 사용량을 줄이고 유럽에서의 조달에 영향을 미치는 지속가능성 목표를 따릅니다. 일회용 원심분리기와 심층 여과 카세트는 청징 처리의 생산성을 향상시키고 오염 위험을 최소화하기 위해 다제품 대응 CDMO 시설에서 높은 평가를 받고 있습니다. 청징 단계와 포착 단계의 센서 판독값을 통합하는 소프트웨어는 배치 릴리스 시간을 단축하고 조기 도입 기업에 경쟁 우위를 가져옵니다.

크로마토그래피 컬럼 및 수지는 2025년에 35.10%의 수익 점유율을 차지했으며, 항체 포획의 기준으로 계속 주류입니다. 그러나, PFAS 프리폴리머의 진전이 치환 사이클을 촉진하는 가운데, 여과 및 막 장치는 14.12%라는 최고 CAGR을 나타내고 있습니다. 여과 제품의 다운스트림 처리 시장 규모는 2026년에 122억 달러에 이르고 2031년까지 236억 달러에 이를 것으로 예측됩니다. 다층 심도 여과는 청징과 정밀 여과를 단일 하우징으로 통합하여 공정 수를 줄이고 시설 생산성을 향상시킵니다.

적응 제어 밸브와 감마 안정성 흐름 경로는 모듈식 스키드의 재구성을 용이하게 하고 다양한 클라이언트 분자를 다루는 CMO(수탁 제조 기관)에 매력적입니다. 크로마토그래피 공급업체는 공정 개발 시간을 30% 단축하는 높은 처리량 수지 스크리닝 키트를 지원합니다. 폐기 비용에 대한 논의가 있음에도 불구하고, 일회용 하드웨어의 채용은 증가하고 있으며, 운영자는 검증 부담의 경감을 중시하고 있습니다.

북미는 2025년 32.50%의 수익 점유율을 기록했으며, Johnson & Johnson의 노스캐롤라이나 주에 대한 20억 달러 규모 프로젝트 등 대규모 투자가 견인했습니다. 지역 제조업체는 신규 라인의 75%로 연속 제조를 채용해, 3년 이내에 인공지능의 통합을 계획하고 있습니다. 다운스트림 공정 시장은 FDA의 혁신적인 제조 지침에 대한 적극적인 태도의 혜택을 받아 새로운 정제 플랫폼에 대한 투자자의 신뢰를 높이고 있습니다.

아시아태평양은 한국, 중국, 싱가포르, 인도의 대규모 시설로 인해 14.35%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. Samsung Biologics가 18만리터의 생산능력을 추가하고 Novartis가 싱가포르 거점을 확장하는 등 세계 공급을 지원하는 메가시설로의 동향이 현저합니다. 인도의 CDMO 기업은 미국 바이오보안법에 따라 대체 옵션으로 자리를 잡고 있습니다. 지역 당국은 공정 엔지니어링 인력의 부족을 해소하기 위해 노동력 육성에 대한 보조금을 지급하고 필터와 가방의 현지 조달을 촉진하고 있습니다.

The downstream processing market is expected to grow from USD 40.78 billion in 2025 to USD 46.03 billion in 2026 and is forecast to reach USD 84.25 billion by 2031 at 12.88% CAGR over 2026-2031.

Capacity expansions valued above USD 50 billion in 2024-2025, including Eli Lilly's USD 9 billion Indiana site and Novo Nordisk's USD 4.1 billion North Carolina facility, have created unprecedented equipment demand and intensified competition for skilled labor. Single-use systems, continuous bioprocessing, and digital twins are now mainstream, cutting operating costs and shortening validation timelines, while suppliers race to introduce PFAS-compliant membranes before incoming regulations take effect. Outsourcing momentum further shapes pricing and technology adoption as CDMOs secure multi-year slots for niche modalities such as viral vector and lipid nanoparticle production. Meanwhile, manufacturers prioritize supply-chain resilience, driving regional sourcing strategies and dual-supplier frameworks for filters, bags, and resins.

Samsung Biologics completed its fifth plant in April 2025, lifting global capacity to 784,000 L and reinforcing a volume race that lifts demand for large-scale chromatography systems and single-use bioreactors. Newly built lines favor continuous modalities that lower buffer consumption by as much as 40% and reduce water-for-injection requirements. Regional governments position biomanufacturing as a strategic growth engine, illustrated by Saudi Arabia's plan to add USD 34.6 billion to non-oil GDP by 2040. Capacity oversupply among some CDMOs temporarily suppresses utilization to below 50%, yet the throughput flexibility of intensified downstream skids allows quick re-scheduling without quality compromise. Vendors consequently bundle columns, resins, and analytical sensors to deliver integrated platforms that can switch between monoclonal and viral-vector products within hours.

Large enterprises lift budgets even while smaller firms face capital rationing. Eli Lilly alone earmarked USD 4.5 billion for the Lilly Medicine Foundry to accelerate clinical supply, creating incremental orders for modular chromatography and tangential flow filtration systems. Venture-backed start-ups prioritise cell and gene therapy pipelines, which require low-shear clarification and nuclease removal steps that differ substantially from antibody workflows. The result is broadened demand diversity that benefits suppliers offering configurable skids and disposable flow paths. Continuous multicolumn chromatography, once niche, is now adopted by a growing number of programs because it offsets resin cost spikes with 50% smaller bed volumes per kilogram of product.

Protein A resin still commands premium pricing, consuming up to 60% of downstream capital budgets. Purolite invested USD 200 million in a Pennsylvania plant to ease supply and blunt price volatility, yet smaller firms remain cost-constrained. Intensified multicolumn operations cut resin use by 50% and raise output per square foot, but they add automation complexity that demands trained staff. A two-tier market is emerging in which large pharma pays for premium capture resins while cost-sensitive players explore mixed-mode or continuous alternatives.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Purification techniques accounted for 32.05% of downstream processing market revenue in 2025, confirming their centrality to biologics quality. Cell disruption registers the fastest 14.88% CAGR as microbial and intracellular expression systems gain adoption. The downstream processing market size for purification surpassed USD 14.75 billion in 2026 and is poised to cross USD 27 billion by 2031, supported by resin capacity expansions and multicolumn innovations. In parallel, homogenisers and microfluidisers remain the workhorses for cell disruption, but low-frequency acoustic methods are attracting pilot-scale trials because they reduce heat generation.

Continuous chromatography reduces buffer use, aligning with sustainability objectives that influence procurement in Europe. Single-use centrifuges and depth-filtration cassettes improve clarification throughput and minimise contamination risk, a feature valued in multi-product CDMO suites. Integration software that harmonises sensor readings across clarification and capture stages shortens batch release times, offering a competitive edge to early adopters.

Chromatography columns and resins commanded 35.10% revenue share in 2025 and continue as the reference standard for antibody capture. Yet filtration and membrane devices exhibit the highest 14.12% CAGR as PFAS-free polymer advances spur replacement cycles. The downstream processing market size for filtration products reached USD 12.2 billion in 2026 and is projected to hit USD 23.6 billion by 2031. Multi-layer depth filters reduce step count by combining clarification and fine filtration in one housing, enhancing facility productivity.

Adaptive control valves and gamma-stable flow-paths facilitate modular skid reconfiguration, appealing to CMOs juggling varied client molecules. Chromatography suppliers respond with high-throughput resin screening kits that cut process development time by 30%. Single-use hardware adoption rises despite disposal cost debates, as operators value the reduced validation burden.

The Downstream Processing Market Report is Segmented by Technique (Purification Techniques, Solid-Liquid Separation, and More), Product (Chromatography Columns and Resins, and More), Application (Antibodies Production, Vaccines Production, and More), End User (Biopharmaceutical & Bio-Similar Manufacturers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America recorded 32.50% revenue share in 2025, powered by large-scale investments such as Johnson & Johnson's USD 2 billion project in North Carolina. Regional producers adopt continuous manufacturing in 75% of new lines and plan artificial intelligence integration within three years. The downstream processing market benefits from the FDA's proactive stance on innovative manufacturing guidance, fostering investor confidence in novel purification platforms.

Asia-Pacific is the fastest growing region at 14.35% CAGR thanks to large-scale facilities in South Korea, China, Singapore, and India. Samsung Biologics adds 180,000 L capacity while Novartis expands its Singapore site, exemplifying a trend toward mega-facilities supporting global supply. Indian CDMOs position themselves as alternatives following the US Biosecure Act. Regional authorities subsidise workforce training to bridge process-engineering talent gaps and encourage local sourcing of filters and bags.