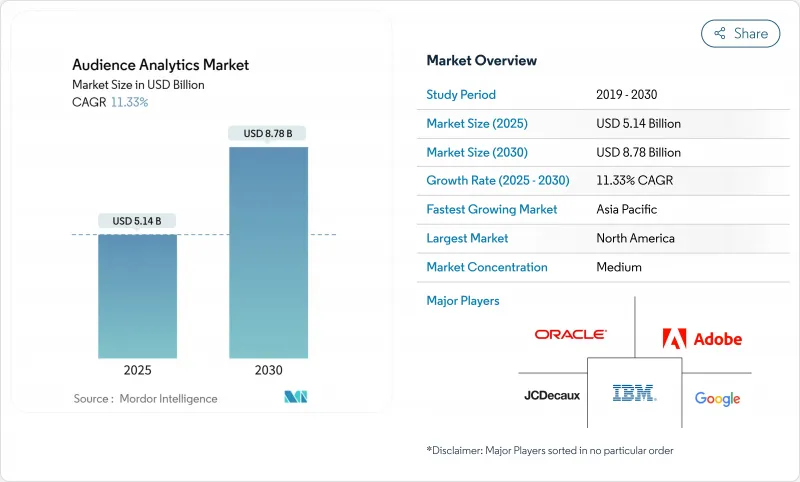

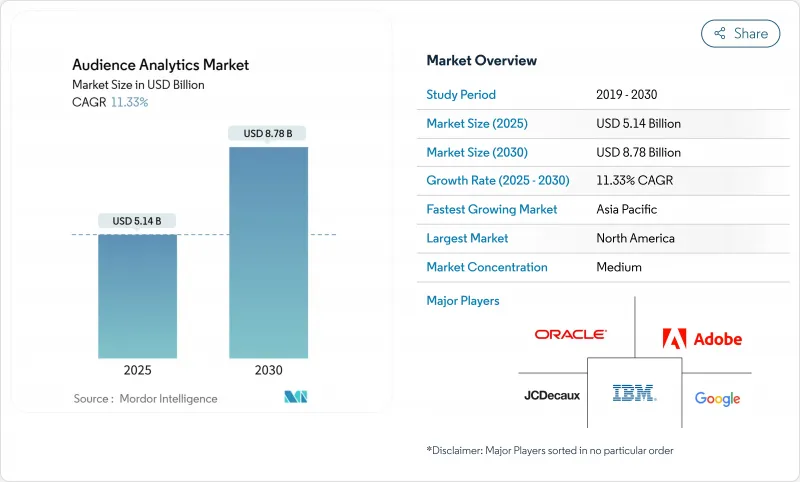

잠재고객 분석 시장은 2025년에 51억 4,000만 달러로 추정되고, 2030년에는 87억 8,000만 달러에 이를 전망이며, CAGR 11.3%로 성장할 것으로 예측됩니다.

동의 기반 아이덴티티 해결, 강력한 AI 툴킷, 소매 미디어 네트워크에서 퍼스트 파티 데이터의 급속한 수익화에 대한 수요 증가가 이 확대를 지원하고 있습니다. 조직은 점점 더 많은 참여 시점에서 실용적인 인사이트를 창출하면서 프라이버시를 보호하는 실시간 엣지 기반 분석을 도입하고 있습니다. 솔루션이 가장 큰 판매 기여자라는 점은 변함이 없지만, 기업이 확장성과 비용 최적화를 요구하기 때문에 클라우드 네이티브 서비스가 가장 급속한 성장을 기록하고 있습니다. 반면 대기업의 지출은 압도적으로 많지만 고급 분석에 대한 진입 장벽을 낮추는 노코드 인터페이스와 소비 기반 가격 모델로 중소기업 도입이 가속화되고 있습니다.

브랜드는 온 인터랙션 포인트를 중심으로 데이터 아키텍처를 재구성하여 매장에서의 행동, 모바일 참여 및 연결 장치 신호를 통합합니다. 소매업체는 현재 물리적 저니와 디지털 저니를 정합시키는 정교한 미디어 네트워크를 운영하고 있으며, 한때는 타사 데이터 브로커가 독점했던 달러 수준의 수익 채널을 열고 있습니다. 오프라인과 온라인 인사이트를 통합하는 능력은 평생 가치 모델링을 개선하고 세분화의 정확성을 향상시킵니다.

머신러닝 알고리즘은 현재 주류 플랫폼 전체에서 행동 모델링, 전환 예측, 자동 코호트 생성을 지원합니다. Google Analytics 4와 Adobe Experience Cloud는 예측 정확도를 30% 이상 향상시키면서 인사이트 대기 시간을 몇 주에서 몇 분으로 단축하는 AI 엔진을 전시하고 있습니다. 클라우드 딜리버리를 통해 인프라 비용과 인력 부족으로 제한된 중견기업도 이러한 기능에 액세스할 수 있습니다.

GDPR(EU 개인정보보호규정), CPRA, 디지털 시장법은 기업에 데이터 흐름을 재구축하고 있으며 분석 예산의 15-20%를 컴플라이언스 대책으로 돌이키는 경우가 많습니다. 쿠키가 없는 웹 분석과 같은 프라이버시를 보호하는 솔루션은 행동 인사이트의 품질을 유지하면서 개인 식별 정보에 대한 의존도를 줄입니다. 공급업체는 규제 요구사항 및 상업적 목표를 양립하기 위해 컨텍스트 타겟팅 및 엣지 처리를 판매합니다.

솔루션은 2024년 매출의 67.8%를 차지했으며, 여전히 잠재고객 분석 시장의 핵심입니다. 이러한 솔루션은 데이터 통합 허브, 고객 데이터 플랫폼 및 AI 추론 엔진으로 구성되어 채널을 통한 인사이트 생성을 가능하게 합니다. 조직은 확장 가능한 인프라에 엄청난 초기 투자를 수행하고 높은 스위칭 비용과 공급업체 간의 견고한 관계를 구축하고 있습니다. 그러나 신원 확인, 모델 거버넌스 및 컴플라이언스 감사의 전문 지식을 아웃소싱함으로써 서비스는 CAGR 12.7%를 달성합니다. 매니지드 서비스는 지속적인 최적화를 실현하고 데이터 엔지니어링의 인력 격차를 메우면서 전체 프로젝트의 성공률을 높입니다.

애널리틱스 애즈 어 서비스의 상승은 영구 라이선스에서 소비 기반 계약으로의 전략적 변화를 시사합니다. 컨설팅 회사 및 시스템 통합사업자는 기술 스택에 권고 지원을 패키징하여 비즈니스 목표가 구현 선택을 뒷받침합니다. 개인 정보 보호 규제가 강화됨에 따라 동의 관리 및 엣지 전개에 특화된 서비스는 가격이 비싸고 정기적인 전문 지원으로의 수익 구성 전환이 가속화되고 있습니다.

2024년 잠재고객 분석 시장 점유율에서 온프레미스 시스템은 65.8%를 차지했습니다. 이는 데이터 주권 및 대량 스트리밍 분석에서 대기 시간에 대한 우려가 근본적임을 반영합니다. 은행과 정부 기관과 같은 분야에서는 개인을 식별할 수 있는 기밀 정보를 보유하기 위해 자체 호스트 플랫폼에 의존합니다. 하지만 클라우드 인스턴스는 공급업체가 지역별 암호화, 소블린 클라우드 옵션 및 고급 컴플라이언스 인증을 도입하여 CAGR 13.1%로 성장합니다. Adobe와 AWS가 공동으로 제공하는 클라우드 솔루션은 실시간 고객 프로파일링을 위한 맞춤형 솔루션입니다.

하이브리드 아키텍처는 일반적인 모델로 떠오르고 있으며 금형 고객 프로파일을 온프레미스로 유지하면서 컴퓨팅 부하가 높은 워크로드를 클라우드로 마이그레이션합니다. 이렇게 하면 인프라의 자본 지출을 억제하고 계절별 캠페인이나 갑작스러운 데이터 수집에도 대응할 수 있는 탄력적인 처리가 가능해집니다. 클라우드 구축을 통한 잠재고객 분석 시장 규모는 퍼블릭 클라우드 보안에 대한 신뢰가 성숙함에 따라 2030년 이후 온프레미스 수익을 초과할 것으로 예측됩니다.

잠재고객 분석 시장 보고서는 컴포넌트별(솔루션 및 서비스), 전개 모드별(온프레미스 및 클라우드), 조직 규모별(대기업 및 중소기업), 용도별(영업 및 마케팅 최적화, 고객 경험 관리 등), 최종 사용자 산업별(미디어 및 엔터테인먼트, 소매 및 전자상거래 등), 지역별로 분류됩니다.

북미는 2024년에 40.3%의 매출을 차지했으며, 정교한 광고 생태계, 대규모 기술 투자, 프라이버시 퍼스트 툴의 조기 도입에 지원되었습니다. 미국에서는 Walmart 및 Target과 같은 소매업체가 소매 미디어 수익 창출에서 주도하고 있으며, 캐나다에서는 컴플라이언스를 준수하는 애널리틱스 아키텍처로 기업을 유도하는 고급 프라이버시 법의 혜택을 누리고 있습니다. 멕시코에서는 전자상거래의 도입이 가속화되고 확장 가능한 클라우드 기반 인사이트 엔진의 사용자층이 넓어지고 있습니다.

유럽은 GDPR(EU 개인정보보호규정) 및 디지털 시장법에 의해 꾸준한 성장 단계에 있으며, 개인 데이터에 대한 의존도를 최소화하는 동의 기반 솔루션에 대한 수요가 증가하고 있습니다. 독일과 영국은 데이터를 상주하고 국경을 넘어 이전의 복잡성을 줄이는 엣지 프로세싱의 조종사를 지지합니다. 프랑스와 이탈리아는 광고 효율을 유지하기 위해 컨텍스트 타겟팅을 모색하고 있습니다. 여러 ID 프레임워크에서 상호 운용 가능한 독립 벤더가 유연한 컴플라이언스를 요구하는 중견 시장의 채용자를 끌어들입니다.

아시아태평양은 8,800억 달러의 모바일 경제와 18억 명의 모바일 가입자에게 지원되며 CAGR 12.2%에서 가장 급성장이 전망되고 있는 지역입니다. 중국은 동영상, 메시징 및 결제를 융합하고 세밀한 실시간 인사이트 스트림을 만드는 소셜 커머스 분석의 선구자입니다. 인도의 핀테크 붐은 거래 데이터 세트를 확대하고 일본과 한국은 잠재고객 분석을 게임 생태계에 통합하여 보존을 최적화하고 있습니다. 호주 및 뉴질랜드는 옴니채널 소매 및 공공 서비스의 현대화를 지원하기 위해 엔터프라이즈 애널리틱스를 채택하고 있습니다. 동남아시아에서는 스마트폰의 보급률 상승과 정부의 디지털화 정책이 추가 수요를 촉진하여 잠재고객 분석 시장의 장기적인 기세를 강화하고 있습니다.

The audience analytics market stands at USD 5.14 billion in 2025 and is expected to reach USD 8.78 billion by 2030, advancing at an 11.3% CAGR.

Heightened demand for consent-based identity resolution, powerful AI toolkits, and the rapid monetisation of first-party data in retail media networks underpin this expansion. Organisations increasingly deploy real-time, edge-based analytics that protect privacy while generating actionable insights at the point of engagement. Solutions remain the largest revenue contributor, yet cloud-native services record the quickest growth as firms seek scalability and cost optimisation. Meanwhile, large enterprises dominate spending, but small and medium enterprises accelerate adoption thanks to no-code interfaces and consumption-based pricing models that lower entry barriers to sophisticated analytics.

Brands are rebuilding data architectures around owned interaction points, integrating in-store behaviour, mobile engagement, and connected-device signals. Retailers now operate sophisticated media networks that align physical and digital journeys, opening USD-level revenue channels once dominated by third-party data brokers. The ability to merge offline and online insights improves lifetime value modelling and elevates segmentation precision.

Machine-learning algorithms now underpin behavioural modelling, conversion prediction, and automated cohort creation across mainstream platforms. Google Analytics 4 and Adobe Experience Cloud showcase AI engines that slash insight latency from weeks to minutes while improving forecast accuracy by more than 30%. Cloud delivery makes these functions accessible to mid-market firms previously constrained by infrastructure costs and talent shortages.

GDPR, CPRA, and the Digital Markets Act compel firms to re-engineer data flows, often diverting 15-20% of analytics budgets to compliance efforts. Privacy-preserving solutions, such as cookieless web analytics, reduce dependence on personal identifiers while sustaining behavioural insight quality. Vendors tout contextual targeting and edge processing to balance regulatory demands with commercial goals.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions generated 67.8% of 2024 revenue and remain the backbone of the audience analytics market. They comprise data-integration hubs, customer data platforms, and AI inference engines that enable cross-channel insight generation. Organisations invest heavily at the outset in scalable infrastructures, creating high switching costs and entrenched vendor relationships. Services, however, achieve a 12.7% CAGR as firms outsource expertise in identity resolution, model governance, and compliance auditing. Managed offerings deliver continuous optimisation and bridge the data-engineering talent gap, elevating overall project success rates.

The rise of analytics-as-a-service signals a strategic shift from perpetual licences to consumption-based engagements. Consultancies and system integrators package technology stacks with advisory support, ensuring business objectives drive implementation choices. As privacy regulation tightens, specialised services in consent management and edge deployment command premium pricing, accelerating the revenue mix transition toward recurring professional support.

On-premises systems held 65.8% of the audience analytics market share in 2024, reflecting enduring concerns over data sovereignty and latency for high-volume streaming analyses. Sectors such as banking and government rely on self-hosted platforms to retain sensitive personally identifiable information. Nevertheless, cloud instances grow at a 13.1% CAGR as vendors implement region-specific encryption, sovereign-cloud options, and advanced compliance certifications. Adobe's joint offering with AWS exemplifies tailored cloud solutions for real-time customer profiling.

Hybrid architectures surface as the prevailing model, retaining golden customer profiles on-premises while bursting compute-intensive workloads to the cloud. This arrangement curbs infrastructure capital expenditure and unlocks elastic processing for seasonal campaigns and sudden surges in data ingestion. The audience analytics market size represented by cloud deployments is forecast to overtake on-premises revenue in the post-2030 horizon as confidence in public-cloud security matures.

The Audience Analytics Market Report is Segmented by Component (Solutions and Services), Deployment Mode (On-Premises and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), Application (Sales and Marketing Optimisation, Customer Experience Management, and More), End-User Industry (Media and Entertainment, Retail and ECommerce, and More), and Geography.

North America held 40.3% revenue in 2024, anchored by a sophisticated advertising ecosystem, heavy technology investment, and early adoption of privacy-first tools. United States retailers such as Walmart and Target lead in retail media revenue generation, while Canada benefits from progressive privacy laws that nudge firms toward compliant analytics architectures. Mexico's accelerating e-commerce adoption widens the regional user base for scalable, cloud-delivered insight engines.

Europe sits in a steady growth phase shaped by GDPR and the Digital Markets Act, which elevate demand for consent-based solutions that minimise personal data dependence. Germany and the United Kingdom endorse edge-processing pilots that keep data resident, reducing cross-border transfer complexity. France and Italy explore contextual targeting to maintain advertising efficiency. Independent vendors that can interoperate across multiple identity frameworks attract mid-market adopters seeking flexible compliance.

Asia-Pacific is the fastest-growing region at a 12.2% CAGR, supported by a USD 880 billion mobile economy and 1.8 billion mobile subscribers. China pioneers social commerce analytics that blend video, messaging, and payments, creating granular, real-time insight streams. India's fintech boom expands transactional datasets, while Japan and South Korea integrate audience analytics into gaming ecosystems to optimise retention. Australia and New Zealand embrace enterprise analytics to support omnichannel retail and public-service modernisation. Rising smartphone penetration and government digital initiatives propel additional demand across Southeast Asia, reinforcing long-term momentum for the audience analytics market.