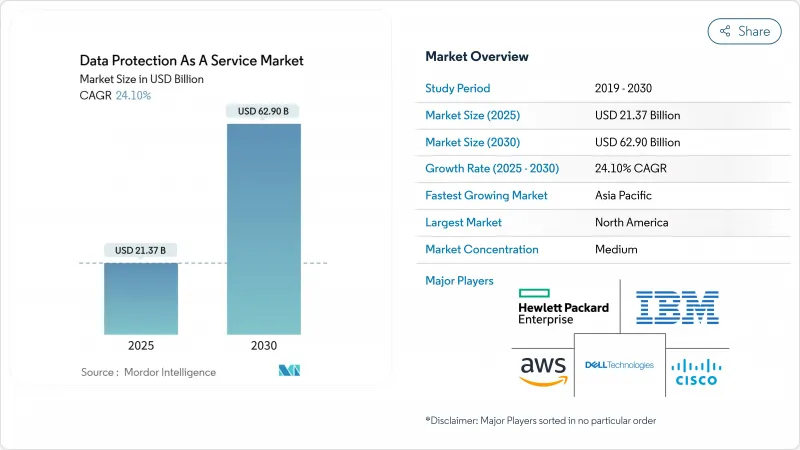

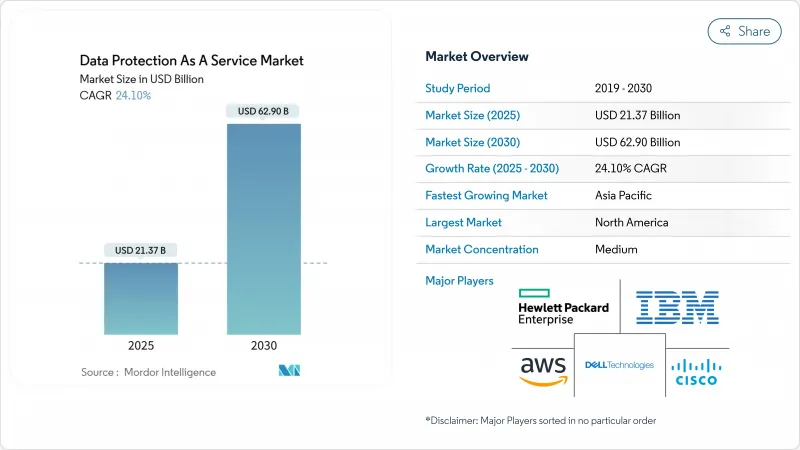

DPaaS(Data Protection As A Service) 시장의 규모는 2025년에 213억 7,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 24.10%로, 2030년에는 629억 달러에 달할 것으로 예측됩니다.

성장을 뒷받침하는 것은 비구조화된 데이터의 급증, 제로 트러스트의 의무화, 랜섬웨어 노출에 대한 이사회 수준의 우려 증가입니다. 기업은 자본 집약적인 On-Premise 백업 하드웨어를 사용 기반 가격 및 탄력적인 확장성을 제공하는 클라우드 배포 구독으로 빠르게 교체하고 있습니다. 소버린 클라우드에 대한 투자, 양자 안전 암호화 시험, 사이버 보험 요구 사항은 제품 로드맵을 재구축하기 위해 수렴하고 있으며, 벤더 통합은 시장 구조를 압축하고 기능 통합을 가속화하고 있습니다.

브라질과 인도에서 GDPR(EU 개인정보보호규정)과 유사한 프레임워크가 전개되어 기업은 스토리지 현지화, 정확한 데이터 매핑 채택, 국경을 넘는 흐름을 관리하는 정책 기반 컨트롤의 구축을 강요받고 있습니다. EU는 2025년 1월에 디지털 운영 탄력성법을 시행하여 금융기관에 거의 실시간으로 인시던트를 보고하도록 의무화했습니다. 미국에서는 새로운 규칙이 외국발 공격자들에게 기밀 데이터의 전송을 제한하고 다국적 기업들에게 복잡성이 높아지고 있습니다. 그 결과 조달팀은 DPAaS 벤더를 선정할 때 RPO/RTO 지표와 함께 소버린 컨트롤을 중시하게 되었습니다. 공급업체는 각국의 규제 당국과 사내 리스크 위원회를 모두 만족시키는 지역별 키 관리, 이중 암호화 옵션, 지역 내 복구 보관소 등에서 대응하고 있습니다.

엣지 도입으로 처리가 센서의 엔드포인트와 지점 근처로 이동하기 때문에 워크로드는 트래픽을 중앙 집중식 데이터 허브로 라우팅하지 않고 대기 시간 목표를 달성할 수 있습니다. 대기업의 40%는 2025년 말까지 미션 크리티컬 용도를 엣지에서 실행할 계획입니다. 이 시프트에는 로컬로 실행하고 비동기식으로 동기화할 수 있는 경량의 정책 기반 백업 에이전트가 필요합니다. 엣지 게이트웨이에 AI 기반 이상 감지 기능을 통합하여 랜섬웨어 침입 시 체류 시간을 단축하는 새로운 제품도 등장하고 있습니다. 의료 시스템은 임상의가 즉시 액세스할 수 있도록 하면서 환자 데이터의 엄격한 현지화 규칙을 준수하기 위해 병원 내에서 이러한 기능을 시험적으로 도입합니다.

변동되는 트래픽 요금 및 API 통화별 가격 설정은 특히 빈번한 복원이 필요한 분석 부하가 높은 쿼리 또는 규제 관련 쿼리의 경우 예산을 증가시킬 수 있습니다. 소규모 클라우드 지역에서 협상력이 제한된 기업은 이 리스크에 가장 노출되어 있습니다. FinOps 팀은 비용 감시가 가능한 대시보드에 투자하고 있지만 스토리지 계층 및 핫 콜드 마이그레이션에 걸친 단편적인 청구는 여전히 예산 과제입니다.

재해 복구 서비스(Disaster-Recovery-as-a-Service) 부문은 2030년까지 연평균 복합 성장률(CAGR)이 29.5%로 성장을 지속할 전망이며, 리더십 팀이 랜섬웨어에 대한 대응을 전략적 지표로 승격시키면서 다른 서비스를 능가하고 있습니다. 기업의 70% 이상이 2026년까지 DRAaS를 SIEM 텔레메트리와 통합하여 위협 점수를 기반으로 자동 페일오버를 실현하려는 의도입니다. 지속적인 데이터 보호 스트림은 복구 지점의 목표를 수초로 줄여 데이터 유출이 컴플라이언스의 벌금과 동일한 금융 및 의료 워크로드에 호소합니다. 스토리지 서비스(Storage-as-a-Service)는 2024년 DPAaS(Data Protection As A Service) 시장 점유율의 43.2%를 차지했지만, 제로 트러스트 아키텍처에 따른 지능적인 계층화와 정책 기반 불변성을 향해 진화하고 있습니다. 컨버지드 플랫폼은 현재 BaaS, STaaS, DRAaS를 통합된 정책 엔진 하에 번들로 제공하여 조달과 거버넌스를 용이하게 합니다.

DRaaS에 대한 관심이 증가하는 반면 스토리지 구독은 여전히 지속되고 있습니다. 오브젝트 스토어의 성장은 비구조화된 데이터 양을 증가시키는 AI 모델의 트레이닝 세트와 비디오 분석을 통해 견조하게 변화하고 있습니다. 이를 위해 공급자는 페타바이트 규모의 중복 제거 및 압축을 추진하고 있습니다. 클라우드 하이퍼스케일러의 풀스택 제공 제품은 현재 자율적인 위협 검사를 통합하고 있으며, 랜섬웨어가 전체 볼륨이 아닌 영향을 받는 블록만을 되풀이한다는 것을 의미합니다. 이러한 기능의 연계는 복구 자동화, 데이터 분류 및 컴플라이언스 매핑이 단일 제어 플레인 내에 존재하는 플랫폼 중심 구매로의 장기적인 움직임을 시사합니다.

하이브리드 모델은 CAGR 31.5%로 가장 빠르게 확대되고 있습니다. 규제 당국은 민감한 데이터 세트를 로컬 프라이빗 클라우드에 유지하면서 규제 대상의 공개 영역에서 버스트 가능한 분석을 가능하게 하는 아키텍처를 지원합니다. 이러한 패턴은 써드파티 서비스에 대한 문서화된 불측사태의 약정을 의무화하는 디지털 오퍼레이션 탄력성법의 대상이 되는 유럽 은행에서 특히 두드러집니다. 정책 자동화는 데이터 분류 라벨을 기반으로 스토리지 대상을 선택하고 대기 시간과 규정 준수를 모두 최적화합니다. 하이브리드 솔루션의 DPAaS(Data Protection As A Service) 시장 내 규모는 기업이 레거시 테이프 아카이브를 클라우드로 연결된 스토리지로 현대화함에 따라 2028년까지 두 배가 될 것으로 예측됩니다.

프라이빗 클라우드의 도입은 43.7%의 점유율을 유지하고 있으며 암호화 키를 관리해야 하는 방위, 유틸리티, 의료기관에 의해 지지를 받고 있습니다. 프라이빗 클라우드 어플라이언스를 제공하는 공급업체는 FIPS Validated HSM, 역할 기반 액세스 및 에어 갭을 통한 구성 관리를 통합해 왔습니다. 퍼블릭 클라우드 접근법은 완전한 주권보다 지역 다양성을 강조하는 디지털 네이티브 기업들 사이에서 여전히 인기가 있습니다. 그러나 AWS European Sovereign Cloud와 같은 소버린 클라우드의 이니셔티브는 그 경계를 모호하게 만듭니다. 이는 현지 법적 관리 하에 퍼블릭 클라우드의 민첩성을 제공하고 규제된 워크로드를 지금까지 도입이 어려웠던 환경으로 끌어들이는 것입니다.

DPaaS(Data Protection As A Service) 시장은 서비스 유형(Storage-As-A-Service, Backup-As-A-Service, Disaster-Recovery-As-A-Service), 배포 모델(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 조직 규모(대기업, 중소기업), 최종 사용자 업계(은행, 금융서비스 및 보험(BFSI), 헬스케어) 시장 예측은 금액(달러)으로 제공됩니다.

북미는 견조한 클라우드 도입과 SaaS에 안전한 컨피규레이션 베이스라인을 적용할 것을 기관에 의무화하는 CISA 구속적 운용지침 25-01 등의 연방지침에 힘입어 37.8%의 매출 점유율을 유지했습니다. 외국발 공격자로부터 미국인의 데이터를 보호하는 법(Protecting Americans' Data from Foreign Adversaries Act)은 기밀성이 높은 개인 데이터의 국경을 넘은 이전을 제한하고 있으며, 국내 보관고와 키 에스크로 수요에 박차를 가하고 있습니다. 기업은 감사인을 위한 자동 인증 보고서를 작성하는 컴플라이언스 매핑 기능을 우선시하고 있습니다.

아시아태평양은 일본, 인도, 한국의 디지털 정부 프로그램이 데이터의 현지화 규칙을 추진하면서 CAGR 31.4%의 가장 빠른 속도로 추이하고 있습니다. 인도의 디지털 개인 데이터 보호법은 중요한 개인 정보의 명확한 현지화를 성문화하고 클라우드 공급자에게 국내 복구 구역을 개시할 것을 요구하고 있습니다. 하이퍼스케일러는 국내 통신 캐리어와 제휴하여 법적인 보관 제약을 존중하면서 해외에서의 백업 서비스를 가능하게 하는 소버린 시설을 설립합니다. 싱가포르와 호주 신흥기업은 안전한 로컬 스토리지와 세계 페일오버 옵션을 결합한 DPaaS를 배포하고 무역과 컴플라이언스의 균형을 맞추는 중견 수출업체에 호소하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정), DORA, 사이버 복원력법, EU 데이터법(2025년 9월 발효) 등 고도의 도입을 진행하고 있습니다. 프랑스 Cloud de Confiance 및 독일 Gaia-X와 같은 국가 프로그램은 투명성과 공급업체의 이식성을 강조하는 표준 기반 인프라에 자금을 투자하고 있습니다. 공급자는 지역 내에서 메타데이터 처리, EU 거주자 전용 운영 직원, 익스포트 가능한 감사 추적을 제공함으로써 차별화를 도모하고 있습니다. 소버린 옵션은 규제 상의 마찰을 줄이고 공공기관의 연결성을 높입니다.

라틴아메리카, 중동, 아프리카의 신흥 시장에서는 소규모이지만 도입이 진행되고 있습니다. 걸프 협력 회의 국가 정부는 경제 다양화와 핀테크 신흥 기업의 유치를 위해 소버린 클라우드 플랫폼에 자금을 제공합니다. 브라질 은행은 미래의 암호화 요구 사항을 예측하여 국경을 넘어서는 복제 링크를 통해 양자 안전 암호화를 시험적으로 도입했습니다. 아프리카 통신 사업자는 빠르게 성장하는 모바일 머니 플랫폼을 보호하기 위해 SaaS 백업을 도입하여 현지 데이터센터의 제한된 용량을 보완하고 있습니다.

The Data Protection As A Service Market size is estimated at USD 21.37 billion in 2025, and is expected to reach USD 62.90 billion by 2030, at a CAGR of 24.10% during the forecast period (2025-2030).

Growth is propelled by a surge in unstructured data, zero-trust mandates, and rising board-level concern over ransomware exposure. Enterprises are rapidly replacing capital-intensive, on-premises backup hardware with cloud-delivered subscriptions that offer usage-based pricing and elastic scale. Sovereign-cloud investments, quantum-safe encryption pilots, and cyber-insurance requirements are converging to reshape product roadmaps, while vendor consolidation is compressing market structure and accelerating feature integration.

The roll-out of GDPR look-alike frameworks from Brazil to India is forcing firms to localize storage, adopt precise data-mapping, and build policy-based controls that govern cross-border flows. The EU Digital Operational Resilience Act took effect in January 2025, mandating near-real-time incident reporting for financial institutions. In the United States, new rules restrict sensitive data transfers to foreign adversaries, adding complexity for multinationals. As a result, procurement teams now rank sovereignty controls alongside RPO/RTO metrics when selecting DPaaS vendors. Providers are responding with region-specific key management, double-encryption options, and in-region recovery vaults that satisfy both national regulators and internal risk committees.

Edge deployments move processing closer to sensor endpoints and branch locations, allowing workloads to meet latency targets without routing traffic back to centralized data hubs. Forty percent of large enterprises plan to run mission-critical applications at the edge by end-2025; that shift necessitates lightweight, policy-driven backup agents capable of executing locally and synchronizing asynchronously. Emerging offerings embed AI-based anomaly detection at edge gateways, reducing dwell time for ransomware incursions. Healthcare systems are piloting these capabilities in hospital campuses to comply with strict patient-data localization rules while ensuring immediate access for clinicians.

Variable traffic fees and per-API call pricing can inflate budgets, especially for analytics-heavy or regulatory inquiries that require frequent restores. Enterprises with limited negotiation leverage in smaller cloud regions feel the pinch most acutely. FinOps teams are investing in cost-observability dashboards, yet fragmented billing across storage tiers and hot-cold transitions remains a budgetary hazard.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The Disaster-Recovery-as-a-Service segment recorded a 29.5% CAGR outlook through 2030, outpacing other offerings as leadership teams elevate ransomware readiness to a strategic metric. More than 70% of enterprises intend to integrate DRaaS with SIEM telemetry by 2026, enabling automated failover based on threat scoring. Continuous data protection streams shrink recovery-point objectives to seconds, appealing to finance and healthcare workloads where data loss equates to compliance fines. Storage-as-a-Service, though still capturing 43.2% of the 2024 data protection as a service market share, is evolving toward intelligent tiering and policy-based immutability that aligns with zero-trust architectures. Converged platforms now bundle BaaS, STaaS, and DRaaS under unified policy engines, easing procurement and governance.

While DRaaS enthusiasm rises, storage subscriptions remain foundational. Object-store growth stays strong due to AI model training sets and video analytics that balloon unstructured data volumes. In response, providers are pushing petabyte-scale deduplication and compression to control the footprint. Full-stack offerings from cloud hyperscalers now integrate autonomous threat scanning, meaning that ransomware reels only the affected blocks rather than entire volumes. Such feature alignment signals a longer-term move toward platform-centric purchasing in which recovery automation, data classification, and compliance mapping exist inside a single control plane.

Hybrid models show the fastest expansion at 31.5% CAGR. Regulators endorse architectures that keep sensitive datasets on local private clouds while allowing burstable analytics in regulated public regions. These patterns are especially evident among European banks subject to the Digital Operational Resilience Act, which mandates documented contingency arrangements for third-party services. Policy automation selects storage targets based on data-classification labels, optimizing both latency and compliance. The data protection as a service market size for hybrid solutions is forecast to double by 2028 as enterprises modernize legacy tape archives into cloud-connected vaults.

Private-cloud deployments retain a 43.7% share, favored by defense, utilities, and healthcare agencies that must assert custody over encryption keys. Vendors supplying private-cloud appliances increasingly embed FIPS-validated HSMs, role-based access, and air-gapped configuration management. Public-cloud approaches remain popular among digital-native firms that value region diversity over full sovereignty. However, sovereign-cloud initiatives, such as the AWS European Sovereign Cloud, blur lines: they deliver public-cloud agility under local legal control, pulling regulated workloads into environments previously deemed off-limits.

Data Protection As A Service Market is Segmented by Service Type (Storage-As-A-Service, Backup-As-A-Service, and Disaster-Recovery-As-A-Service), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Organization Size (Large Enterprises and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America preserves a 37.8% revenue share, anchored by robust cloud adoption and federal directives such as CISA Binding Operational Directive 25-01, which compels agencies to apply secure configuration baselines for SaaS. The Protecting Americans' Data from Foreign Adversaries Act restricts cross-border transfers of sensitive personal data, spurring demand for in-country vaults and key escrow. Enterprises prioritize compliance mapping features that generate automated attestation reports for auditors.

Asia-Pacific posts the fastest trajectory at 31.4% CAGR as digital-government programs in Japan, India, and Korea push data-localization rules. The Indian Digital Personal Data Protection Act codifies explicit localization for critical personal information, pressuring cloud providers to launch domestic recovery zones. Hyperscalers partner with domestic telecom carriers to establish sovereign facilities that allow foreign backup services while respecting legal custody constraints. Start-ups in Singapore and Australia roll out DPaaS offerings that combine secure local storage with global failover options, appealing to mid-market exporters balancing trade and compliance.

Europe remains a sophisticated adopter shaped by GDPR, DORA, the Cyber Resilience Act, and the EU Data Act, effective September 2025. National programs such as France's Cloud de Confiance and Germany's Gaia-X channel funding into federated, standards-based infrastructure that prizes transparency and vendor portability. Providers differentiate by offering in-region metadata processing, EU resident-only operations staff, and exportable audit trails. Sovereign options reduce regulatory friction, driving higher attach rates among public-sector entities.

Emerging markets in Latin America, the Middle East, and Africa register rising adoption from smaller bases. Gulf Cooperation Council governments finance sovereign-cloud platforms to diversify economies and lure fintech start-ups. Brazilian banks pilot quantum-safe encryption on cross-border replication links, anticipating future cryptographic requirements. African telcos deploy SaaS backup to protect rapidly expanding mobile money platforms, offsetting limited local data-center capacity.