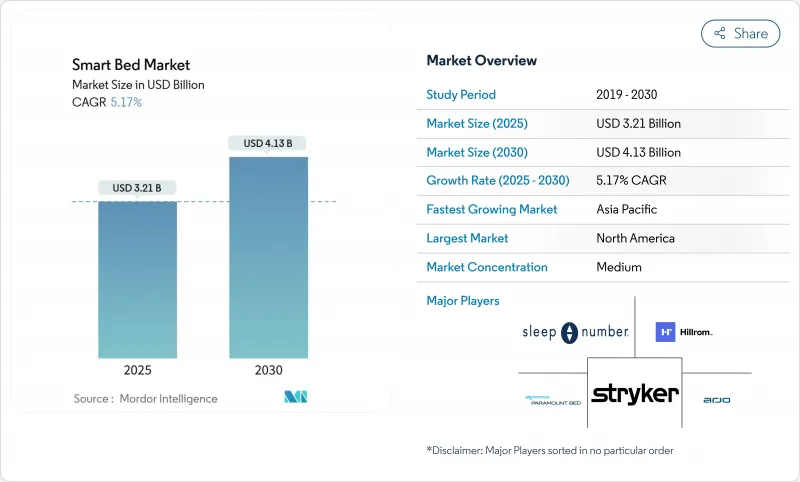

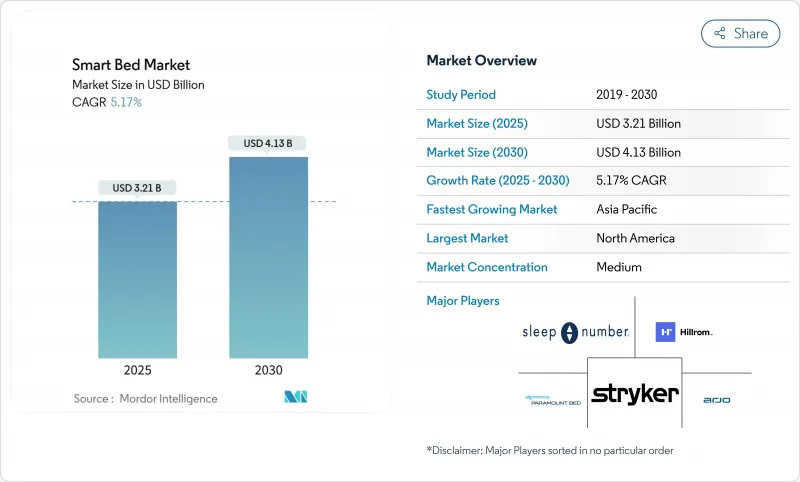

스마트 침대 시장의 2025년 시장 규모는 32억 1,000만 달러로, 2030년에는 41억 3,000만 달러에 이르고, CAGR 5.17%를 나타낼 것으로 예측됩니다.

커넥티드 웰니스에 대한 관심이 높아지고, 헬스케어 환경 전체에 IoT 인프라의 전개, 센서 기술의 급속한 혁신에 의해 스마트 베드는 새로운 것으로부터 헬스케어나 소비자용 제품의 주류로 이행하고 있습니다. 큰 병원 네트워크는 침대를 재입원 감소로 이어지는 길로 간주하고 웰빙에 집중하는 가정은 침대를 일상적인 건강 허브로 간주합니다. 각 제조업체는 애널리틱스 및 개인화된 수면 코칭을 가능하게 하는 소프트웨어 구독을 번들하거나 병원의 전자 의료 기록에 직접 연결하는 통합 키트를 맞춤설정하여 새로운 수익을 얻고 있습니다. 의료 등급의 기존 기업, 가전 브랜드, 스마트 홈 플랫폼 모두가 같은 기회를 노리고 있기 때문에 경쟁의 격렬함이 증가하고 있으며, 제품 사이클의 고속화와 기능 세트의 충실이, 스마트 침대 시장을 커넥티드 헬스 기기의 가장 역동적인 부문의 하나로 하고 있습니다.

스마트 침대는 간병인이 급성기 병동을 떠난 후 환자를 모니터링하는 방법을 재정의합니다. 내장 센서는 심박수, 호흡, 움직임, 수면의 질을 추적하고 그 정보를 ISO/IEEE 11073-10206 상호 운용성 표준에 따라 병원 기록에 직접 스트리밍합니다. 2024년에 실시한 여러 시설에 의한 파일럿 시험에서는 24시간 침대 기반 모니터링이 30일 이내의 재입원을 줄일 수 있는지를 검증하기 위해 설계된 것으로, 연결 침대 코호트에서는 전년에 치료받은 환자에 비해 재입원이 23% 감소했습니다. 설문조사팀은 실시간 경고를 통해 예정된 생체 사인 회진을 기다리는 것이 아니라 문제의 첫 징후로 임상의가 개입할 수 있는지 여부를 결정하는 것을 목표로 했습니다. 같은 해 발표된 병행 연구는 무선 생체 모니터 하드웨어가 리드선을 대체할 수 있어 환자에게 움직임의 자유를 주면서 지속적인 데이터를 케어 팀에 피드백할 수 있음을 보여주었습니다. 이러한 결과를 종합하면 안전성 및 데이터 무결성에 대한 FDA 장비 지침을 충족하면서 재입원 사무처리가 아니라 적극적인 경고가 워크플로우를 추진하는 케어 모델을 제시합니다.

부티크 호텔과 대도시의 고급 호텔에서는 수면을 수익의 테코로 재검토하고 숙박객 각각의 개일 리듬에 맞추어 경도, 표면 온도, 램버 서포트를 자동적으로 미세 조정하는 커넥티드 침대를 도입하고 있습니다. 이 기술을 도입한 호텔은 체인간에 원하는 수면 설정을 저장하는 인앱 체크인을 통해 지원되며 야간 요금이 최대 15% 상승했다고 보고합니다. 도입 곡선이 가장 가파른 것은 부티크 리조트로, 독특한 웰니스 기능이 예약률의 상승이나 만족도의 향상에 신속하게 반영되어, 가격이 아닌 체험이 시장의 프리미엄 엔드를 조타하고 있는 것을 뒷받침하고 있습니다. 클라우드 기반 플릿 대시보드는 운영자가 예측 유지보수를 예약하는 데 도움이 되며 자산 수명을 연장하고 브랜드 일관성을 보호합니다. 짧은 투자 회수 기간은 아시아태평양 리조트 및 유럽 웰니스 리트리트에서의 전개에 박차를 가하고 있어 스마트 침대 시장에, 비용 경쟁보다 체험적 차별화로 번영하는 활기찬 프리미엄 상업 하위 부문을 주고 있습니다.

유행의 여파로 인한 재정적 핍박으로 인해 유럽과 북미의 공공 시스템은 침대 수명을 15년까지 늘려야 합니다. 노후화된 차량에는 최신 센서가 없으며 전자 기록에 연결할 수 없기 때문에 공립 병동과 민간 시설 간의 격차가 확산되고 있습니다. 제조업체 각사는 현재, 후부 부착 센서 매트나 클립 온 게이트웨이를 판매하고 있지만, 이러한 부분적인 수정에서는 기본적인 바이탈 밖에 파악할 수 없고, 소프트웨어 주도의 쾌적성 기능은 생략되어 있습니다. 이러한 2층 구조의 환경은 가장 큰 기관 투자자 부문의 수량 성장을 둔화시키지만, 나중에 완전한 스마트 프레임으로 전환할 수 있는 모듈식 애드온 기술 혁신에도 박차를 가하고 있습니다.

완전 전동 모델은 2024년 판매의 60%를 차지하며, 다축 모터가 자동 압박 방지 루틴과 편안한 환자 이동을 지원하기 위해 스마트 침대 시장을 지원했습니다. 이 부문은 CAGR 4.7%를 나타낼 것으로 예측되며 음성 어시스턴트나 건강 기록 API 등의 커넥티비티층이 추가되어 침대를 케어 플랫폼으로 변모시킵니다. 내장 마이크로컨트롤러는 밀리초 수준의 체압 분산을 가능하게 하고, 내장 RFID 코일이 수면 무호흡 스크리닝에 효과적인 수면 자세 데이터를 획득합니다. 그 결과, 병원에서는 프리미엄 가격을 정당화하는 임상적 유용성이 향상되고, 가정에서는 구체적인 웰빙 효과를 가져옵니다.

반전동식 디자인은 등과 무릎의 관절을 전동으로 움직이지만 높이 조절 크랭크는 수동으로 실시하기 때문에 신흥 시장이나 자금 부족의 간병 시설 등 가격에 민감한 구매자용입니다. 수동 프레임은 송전망이 불안정하거나 규제 규칙에 따라 전동식 가구가 제한되는 경우에 사용됩니다. 이러한 낮은 사양의 카테고리가 진입점이 되는 반면, 혁신은 펌웨어 업그레이드로 지속적인 수익을 제공하는 완전 전기 포트폴리오에 계속 집중하고 있습니다. 그 결과 제조업체는 소프트웨어의 확장성과 모듈식 센서 베이를 선호하고 새로운 출하의 미래를 보장하며 스마트 침대 시장의 완전 디지털 아키텍처로의 꾸준한 전환을 강화하고 있습니다.

북미는 2024년 매출의 42%를 차지했으며, 선진적인 간호 제공 인프라, 추락 예방 기술에 보상하는 지불자 인센티브, 가정용 웰니스 기기에 대한 고액의 재량 지출에 추진되었습니다. 통합 EMR환경은 조달위원회가 간호시간 절약과 입원기간 단축을 정량화할 수 있어 시설에서의 채용을 가속시킵니다. 고소득 가구는 웨어러블 장비와 동기화되는 고급 조정가능한 기반을 채택하여 이 지역의 부문 횡단적인 사용 범위를 확대하고 있습니다. 캐나다는 미국을 반영하지만 규모는 작고 멕시코는 민간 3차 병원과 해안 지역의 리조트 지역에서 기세를 보이고 있습니다.

아시아태평양은 가장 급성장하고 있으며 CAGR 예측은 6.4%를 나타낼 전망입니다. 중국에서는 거주자의 64%가 수면의 질에 우려를 표명하고 있으며 기존 스마트 홈 에코시스템에 맞는 알고리즘 유도형 침구로 방향타를 끊고 있습니다. 브랜드는 소비자 직접 판매 앱을 활용하여 펌웨어 업데이트를 실시하고, 새롭게 특정된 골키퍼 패턴에 대응해, 유저의 리텐션을 높이고 있습니다. 하이테크 선진국인 한국에서는 AI를 활용한 수면 코칭이 급속히 보급되고, 고령화 사회의 일본에서는 야간 화장실에 가는 것을 알리거나, 간병인에게 경고를 발하는 침대 수요가 높아지고 있습니다. 인도는 도시의 프리미엄 소비자가 수입한 무선 모니터링 프레임을 구입하고 호주는 보험 회사가 자금을 제공하는 재택 원격 의료 파일럿을 통해 국민 1인당 도입을 선도하고 있습니다.

유럽은 독일, 프랑스, 영국을 중심으로 견조한 대수를 유지하고 있으며, 각각은 헬스케어의 혁신과 엄격한 데이터 관리 의무의 균형을 맞추고 있습니다. GDPR(EU 개인정보보호규정)은 사용자의 신뢰를 높이지만 클라우드 분석에 의존하는 업그레이드 시장 출시까지의 시간을 늦춥니다. 북유럽 국가들은 가정에 대한 보급률이 가장 높지만, 이는 스마트 홈 기기가 널리 받아들여지고 있으며 수면 건강 개입을 환불하는 국가의 지원 프로그램을 반영합니다. 남유럽에서는 고급 리조트가 커넥티드 침구를 이용하여 객실 카테고리를 차별화하고 있기 때문에 접객 중심의 성장을 볼 수 있습니다. 그러나 공공 부문의 예산 상한은 병원의 갱신 주기를 늦추기 때문에 제조업체 각사는 의료 품질의 향상을 유지하면서 레거시 자산을 확장하는 후부 센서 키트를 추진하게 됩니다.

The smart bed market is valued at USD 3.21 billion in 2025 and is forecast to reach USD 4.13 billion by 2030, expanding to a 5.17% CAGR.

Heightened interest in connected wellness, the rollout of IoT infrastructure across healthcare settings, and rapid innovation in sensor technology are moving smart beds from novelty status to mainstream healthcare and consumer products. Large hospital networks see the beds as a pathway to lower readmissions, while wellness-focused households view them as an everyday health hub. Manufacturers are capturing new revenue by bundling software subscriptions that unlock analytics and personalized sleep coaching, and by tailoring integration kits that connect directly to hospital electronic medical records. Competitive intensity is rising as medical-grade incumbents, consumer electronics brands, and smart-home platforms all target the same opportunity, prompting faster product cycles and richer feature sets that make the smart bed market one of the most dynamic segments of connected health equipment.

Smart beds are redefining how caregivers keep tabs on patients once they leave the acute ward. Built-in sensors track heart rate, breathing, movement, and sleep quality, then stream that information straight into hospital records under the ISO/IEEE 11073-10206 interoperability standard . A 2024 multi-facility pilot-designed to test whether round-the-clock, bed-based monitoring could cut 30-day returns-found that the connected-bed cohort recorded a 23% drop in readmissions compared with matched patients treated the previous year. Researchers aimed to determine whether real-time alerts would let clinicians intervene at the first sign of trouble rather than waiting for scheduled vital-sign rounds. Parallel work published the same year showed that wireless biomonitoring hardware can replace tethered leads, giving patients more freedom of movement while still feeding continuous data back to the care team . Taken together, these results point to a care model where proactive alerts-not readmission paperwork-drive the workflow, all while meeting FDA device guidelines for safety and data integrity.

Boutique hotels and marquee city properties are re-imagining sleep as a revenue lever, integrating connected beds that automatically fine-tune firmness, surface temperature, and lumbar support to each guest's circadian rhythm. Properties report nightly rate uplifts of up to 15% after introducing the technology, supported by in-app check-in that stores preferred sleep settings across chains. The adoption curve is steepest in boutique resorts, where unique wellness features translate quickly into higher booking rates and stronger satisfaction scores, confirming that experience, not price, is steering the premium end of the market . Cloud-based fleet dashboards also help operators schedule predictive maintenance, extending asset life and protecting brand consistency. Short payback periods are fueling rollouts across Asia-Pacific resort destinations and European wellness retreats, giving the smart bed market a vibrant premium-commercial subsegment that thrives on experiential differentiation rather than cost competition.

Fiscal pressures stemming from pandemic aftershocks compel European and North American public systems to stretch bed lifespans up to 15 years. Aging fleets lack modern sensors and cannot connect to electronic records, widening the gap between public wards and privately funded facilities. Manufacturers now market retrofit sensor mats and clip-on gateways, but these partial fixes capture only basic vitals and omit software-driven comfort features. The resulting two-tier environment slows volume growth in the largest institutional buyer segment, although it also spurs innovation in modular add-ons that can later be migrated to full smart frames.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fully electric models controlled 60% of 2024 revenue and anchor the smart bed market because their multi-axis motors support automated anti-pressure-injury routines and effortless patient mobilization. This segment is forecast to expand to a 4.7% CAGR, adding connectivity layers such as voice assistants and health-record APIs that transform beds into care platforms. Integrated micro-controllers now enable millisecond-level pressure redistribution, and embedded RFID coils capture sleep posture data validated for sleep-apnea screening. The result is enhanced clinical utility that justifies premium pricing in hospitals and delivers tangible wellness benefits in homes.

Semi-electric designs offer electric back and knee articulation but retain manual height cranks, positioning them for price-sensitive buyers in emerging markets or cash-strapped long-term care facilities. Manual frames persist where grid power is unreliable or regulatory rules restrict electrified furniture. While these lower-spec categories provide entry points, innovation continues to cluster inside fully electric portfolios where firmware upgrades unlock recurring revenue. Consequently, manufacturers prioritize software scalability and modular sensor bays that future-proof new shipments, reinforcing the smart bed market's steady migration toward fully digital architectures.

The Smart Bed Market Report is Segmented by Product (Manual Beds, Semi-Electric Beds, and Fully Electric Beds), End User (Residential and Commercial), Distribution Channel (B2C/Retail, B2B/Projects), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America commanded 42% of 2024 revenue, propelled by advanced care-delivery infrastructure, payer incentives that reward fall-prevention technology, and high discretionary spending on at-home wellness devices. Integrated EMR environments accelerate institutional adoption because procurement committees can quantify nursing-hour savings and shorter lengths of stay. High-income households embrace premium adjustable bases that sync with wearables, expanding the region's cross-segment usage footprint. Canada mirrors the United States but on a smaller scale, and Mexico shows momentum in private tertiary hospitals and coastal resort corridors.

Asia-Pacific is the fastest-growing territory, posting a 6.4% CAGR forecast that reflects rising urban incomes and the ubiquity of mobile commerce. In China, 64% of residents expressed sleep-quality concerns, steering them toward algorithm-guided bedding that slots into existing smart-home ecosystems. Brands leverage direct-to-consumer apps to roll out firmware updates, addressing newly identified snoring patterns and boosting user retention. South Korea's tech-forward culture fuels rapid uptake of AI-driven sleep coaching, while Japan's aging society spurs demand for beds that flag nocturnal bathroom trips and trigger caregiver alerts. India edges forward as premium urban consumers purchase imported wireless monitoring frames, and Australia leads per-capita adoption through insurer-funded home tele-health pilots.

Europe maintains solid volume anchored in Germany, France, and the United Kingdom, each balancing healthcare innovation with strict data-governance mandates. GDPR builds trust among users but slows time-to-market for upgrades that rely on cloud analytics. Nordic countries register the highest household penetration, reflecting broad acceptance of smart-home devices and state-backed programs that reimburse sleep-health interventions. Southern Europe shows hospitality-led growth as upscale resorts use connected bedding to differentiate room categories. Public-sector budget caps, however, delay hospital refresh cycles, prompting manufacturers to push retrofit sensor kits that extend legacy assets while preserving care-quality gains.