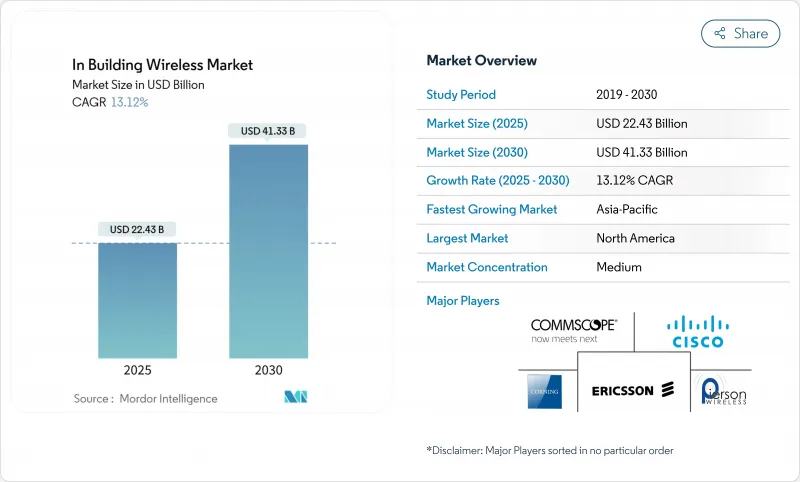

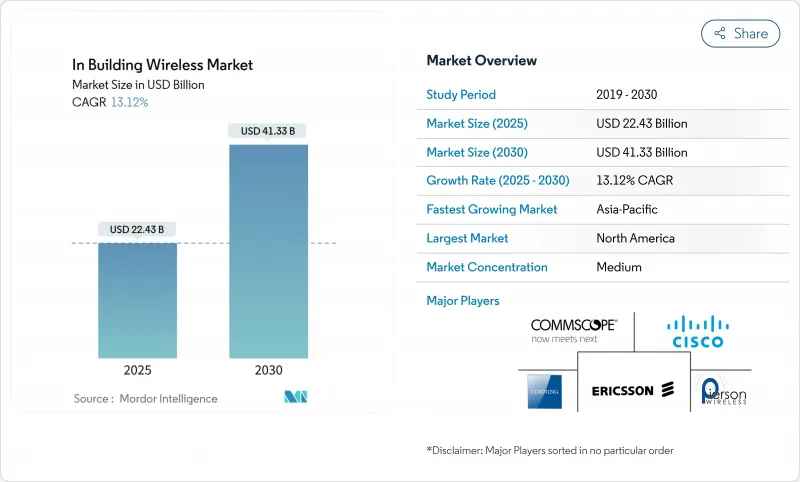

실내 무선 시장 규모는 2025년에 224억 3,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 13.12%로, 2030년에는 413억 3,000만 달러에 달할 것으로 예상됩니다.

상시 이용 가능한 실내 연결에 대한 지속적인 수요, 5G 대응 빌딩으로의 전환, 스마트 시설의 의무화 증가가 이 기세를 뒷받침하고 있습니다. 기업은 현재 실내 커버리지를 핵심 인프라로 취급하고 프라이빗 5G와 차세대 Wi-Fi를 페어링하여 용도 가동 시간을 보장하는 셀룰러 퍼스트 아키텍처에 투자하고 있습니다. 공급망의 인플레이션으로 도입 비용이 상승하고 있지만, 비용 압력은 라이프 사이클 비용을 줄이는 중립 호스트 설계와 AI 기반 최적화에 의해 부분적으로 상쇄됩니다. 장비 제조업체가 라디오, 전송 및 클라우드 관리 레이어를 다루는 엔드 투 엔드 솔루션 포트폴리오를 추구하면서 벤더 통합이 실내 무선 시장을 재구성하고 있습니다.

현재 모든 모바일 트래픽의 약 80%가 건물 내에서 발생하고 있으며 비디오, AR 트레이닝, 고밀도 IoT 워크로드가 급증할 때마다 기존 Wi-Fi를 압도하고 있습니다. Tractor Supply와 같은 소매 체인은 Wi-Fi가 실시간 재고 및 고객 관리 용도를 지원하지 못했기 때문에 2,000개 이상의 매장에서 5G를 채택했습니다. 헬스케어에서는 한 어린이 병원이 900대의 트라이 라디오 AP를 설치하여 원격 의료 및 영상 진단 트래픽을 환자의 방해 없이 보호했습니다. 비디오 협업 및 에지 애널리틱스 워크로드 증가는 수요 곡선을 강화하고 실내 무선 시장의 수익 전망을 강화합니다.

규제 당국은 실내 전용의 주파수대를 확보해, 기업의 설계를 옥외에서 실내에의 오버레이로부터 프라이빗 셀룰러로 첫날부터 변화시키려고 하고 있습니다. 미국에서는 CBRS 경매를 통해 기업 및 회장에서의 전개를 목적으로 하는 3.5GHz대의 면허에 46억 달러를 할당했고, Tier1 캐리어 1사만으로 18억 9,000만 달러를 지출했습니다. 유럽에서는 6GHz대의 480-500MHz가 인가되어 스타디움, 공항, 대학 등에서 중요한 320MHz 폭의 채널이 가능하게 되었습니다. 중국 모바일은 대규모 공장 자동화를 가속화하기 위해 300개 도시에서 5G-Advanced 배포에 4억 1,600만 달러를 기록했습니다. 이러한 할당은 장기적인 주파수 대역의 확실성을 확보하고, 실내 무선 시장 전체의 신뢰와 설비 투자에 대한 헌신을 높입니다.

기업은 비즈니스 트래픽을 보다 광범위한 셀룰러 생태계에 노출하는 데 신중한 태도를 무너뜨리지 않습니다. GDPR(EU 개인정보보호규정) 대응으로 유럽에서는 위치 정보 추적 기능의 감시가 강화되어 스마트 오피스 프로젝트의 조달 사이클이 장기화. 의료 서비스 제공업체는 환자 데이터가 동일한 공기 인터페이스를 통해 이동하기 때문에 새로운 무선을 승인하기 전에 보호된 관리 프레임과 고급 암호화를 의무화합니다. 미국에서는 안전하지 않은 장비에 대한 "립 앤 리플레이스"규칙이 있으며, 교환에 예상치 못한 비용이 들지만, 결과적으로 실내 무선 시장의 보안 체제를 강화하게 됩니다.

분산 안테나 시스템은 2024년 매출의 38%를 차지하며, 경기장, 공항, 클래스 A 사무실에 깊은 침투를 통해 실내 무선 시장을 지원했습니다. 한편, 프라이빗 5G 스몰 셀은 CAGR 13.89%로 진전하고 있어 기업이 소유·관리할 수 있는 민첩한 셀룰러 네트워크에의 축족을 나타내고 있습니다. 광섬유 및 동축 케이블의 가격 상승으로 인티그레이터는 케이블 배선을 최소화하고 소프트웨어의 원격 업그레이드를 용이하게 하는 액티브 DAS 및 스몰셀 아키텍처를 선호합니다.

안테나 기술 혁신은 현재 Wi-Fi 및 셀룰러 커버리지를 하나의 폼 팩터로 결합하여 지붕 공간 요구 사항을 줄이는 멀티 밴드, 멀티 오퍼레이터 설계를 선호합니다. 스몰셀 클러스터가 RF 노이즈의 영향을 받지 않고 강력한 업링크를 제공하기 때문에 중계기의 사용이 감소하고 있습니다. 암페놀이 21억 달러로 콤스코프의 모빌리티 자산을 인수한 것으로 대표되는 벤더의 통합은 케이블, 커넥터, 무선 구성 요소를 묶어 조달을 간소화합니다. 중립 호스트 수요가 증가함에 따라 공공 및 개인 슬라이스를 동시에 전송할 수 있는 단일 백본 인프라는 실내 무선 시장 전체의 자본 배분 패턴을 재구성할 것으로 보입니다.

4G/LTE는 성숙한 디바이스 에코시스템과 음성 및 데이터의 입증된 안정성을 지원하며 2024년에는 65%의 점유율을 유지했습니다. 그러나 5G NR은 10ms 이하의 확정적인 지연을 필요로 하는 산업 자동화 프로젝트에 견인되어 CAGR14.67%를 나타낼 전망입니다. Wi-Fi 6E도 확대되고 있지만, Wi-Fi 7은 320MHz 채널, 멀티링크 동작, 4K-QAM을 도입하여 기업에 초고 처리량에 대한 비셀룰러 경로를 제공합니다.

병원, 스마트 공장, 고등 교육 캠퍼스에서는 5G와 Wi-Fi 7을 융합한 하이브리드 전개가 레퍼런스 아키텍처로서 등장하고 있습니다. 제조 공장에서 모바일 로봇과 안전하고 중요한 원격 측정을 위해 5G를 사용하는 반면, Wi-Fi는 태블릿과 노트북의 대량 데이터 오프로드를 처리합니다. 중국의 5G-Advanced 배포는 이 기술이 실내 광대역에 적합하다는 것을 증명하고 액티브 DAS 및 스몰셀 벤더 부품 수요를 부추기고 있습니다. 민간 면허가 새로 부여될 때마다 실내 무선 시장은 사업자 주도에서 기업 주도 네트워크로의 전환을 심화시키고 있습니다.

실내 무선 시장 보고서는 구성 요소 유형(안테나, 분산 안테나 시스템, 케이블, 리피터, 스몰셀), 기술(4G/LTE, 5G NR, Wi-Fi 6/6E, Wi-Fi 7), 주파수대(1GHz 미만, 1-6GHz, 6GHz 이상), 최종 사용자 산업(상업, 주택, 산업, 공공 안전·정부), 지역

북미는 CBRS 주파수대의 자유화와 FirstNet의 80억 달러의 공공안전투자를 통해 1,000개의 새로운 셀사이트에 자금을 공급해 2024년 실내 무선 시장을 34%의 수익 점유율로 선도했습니다. 미국 기업은 통신 사업자와의 관계를 통합하고 미래의 사설 네트워크에 대한 야망을 실현하기 위해 중립 호스트 아키텍처를 채용. 여러 공급업체가 Wi-Fi 7을 발표하고 새로 고침 사이클을 가속화하는 반면 캐나다와 멕시코는 자동차와 항공우주의 클러스터를 활용하여 공장 내 개인 셀룰러 도입을 정당화합니다.

아시아태평양은 2030년까지 14.60%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 중국은 이미 440만 5G 기지국을 보유하고 있으며, 제조 및 물류의 디지털화에 따라 예측기간 내에 450만을 넘을 예정입니다. 일본의 면허제도는 스마트 공장에서 서브 6G와 mm파 하이브리드를 지원하고 한국은 반도체 공장의 캠퍼스 네트워크에 국가 인센티브를 투입하고 있습니다. 인도의 전자 제조업은 수입 비용을 줄이고 도입 리드 타임을 단축하는 안테나의 현지화 제휴에 의해 지원되고 있습니다.

유럽에서는 데이터 프라이버시 및 건축물의 배기가스에 관한 규제 강화의 영향을 받아 꾸준히 보급이 진행되고 있습니다. 6GHz대 할당으로 고밀도 회장에서 Wi-Fi 용량이 확대되고 프랑스 도시에서는 시영 카메라 백홀용으로 프라이빗 5G의 비용 우위성이 입증되었습니다. 독일, 영국, 프랑스 기업이 채용을 이끌고 중동의 제조업체는 Industry 4.0을 지원하기 위해 개인 5G를 시험적으로 도입했습니다. 엄격한 GDPR(EU 개인정보보호규정) 컴플라이언스 요구 사항은 On-Premise 코어 네트워크와 보안 장치 ID 프레임워크에 대한 구매자를 뒷받침하고 실내 무선 시장에서 보안 우선 접근 방식을 형성하고 있습니다.

The In Building Wireless Market size is estimated at USD 22.43 billion in 2025, and is expected to reach USD 41.33 billion by 2030, at a CAGR of 13.12% during the forecast period (2025-2030).

Sustained demand for always-available indoor connectivity, the transition to 5G-ready buildings, and rising smart-facility mandates are driving this momentum. Enterprises now treat indoor coverage as core infrastructure, investing in cellular-first architectures that pair private 5G with next-generation Wi-Fi to guarantee application uptime. Supply-chain inflation has nudged deployment costs higher, yet cost pressures are partially offset by neutral-host designs and AI-based optimisation that lower life-cycle expenses. Vendor consolidation is reshaping the In-Building Wireless market as equipment makers pursue end-to-end solution portfolios capable of spanning radio, transport, and cloud management layers.

Roughly 80% of all mobile traffic now originates inside buildings, overwhelming legacy Wi-Fi whenever video, AR training, or high-density IoT workloads spike. Retail chains such as Tractor Supply adopted 5G across more than 2,000 outlets after Wi-Fi could not support real-time inventory and customer-engagement applications. In healthcare, a single children's hospital installed 900 tri-radio APs to safeguard tele-medicine and imaging traffic without patient disruption, underscoring the capacity gap that indoor 5G plus Wi-Fi 6E is filling. Growing video collaboration and edge analytics workloads will intensify the demand curve, reinforcing the revenue outlook for the In-Building Wireless market.

Regulators are carving out dedicated indoor spectrum, shifting enterprise design from outdoor-to-indoor overlay to private cellular from day one. In the United States, the CBRS auction channelled USD 4.6 billion into 3.5 GHz licences aimed at enterprise and venue deployments, with one Tier-1 carrier alone spending USD 1.89 billion. Europe authorised 480-500 MHz in the 6 GHz band, enabling 320 MHz-wide channels critical for stadiums, airports, and universities. China Mobile earmarked USD 416 million for 5G-Advanced rollouts across 300 cities to accelerate factory automation at scale. Such allocations ensure long-term spectrum certainty, lifting confidence and capex commitment across the In-Building Wireless market.

Enterprises remain cautious about exposing operational traffic to broader cellular ecosystems. GDPR compliance elevates scrutiny of location-tracking functions in Europe, prolonging procurement cycles for smart-office projects. Healthcare providers mandate Protected Management Frames and advanced encryption before approving new radios because patient data moves over the same air interface. The US "rip-and-replace" rules for insecure equipment add unexpected swap-out costs but ultimately harden the security posture of the In-Building Wireless market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Distributed Antenna Systems held 38% of 2024 revenue, anchoring the In-Building Wireless market through deep penetration in stadiums, airports, and Class-A offices. Private-5G small cells, however, are advancing at a 13.89% CAGR, signaling a pivot toward agile cellular networks that enterprises can own and manage. Rising fibre and coax prices push integrators to favour active DAS or small-cell architectures that minimise cabling runs and facilitate remote software upgrades.

Antenna innovation now prioritises multi-band, multi-operator designs that collapse Wi-Fi and cellular coverage into one form factor, trimming roof-space requirements. Repeater use is declining as small-cell clusters deliver stronger uplinks without RF noise penalties. Vendor consolidation, illustrated by Amphenol's USD 2.1 billion acquisition of CommScope's mobility assets, bundles cabling, connectors, and radio components to streamline procurement. As neutral-host demand grows, single backbone infrastructures capable of carrying public and private slices simultaneously will reshape capital-allocation patterns across the In-Building Wireless market.

4G/LTE retained 65% share in 2024, underpinned by a mature device ecosystem and proven stability for voice and data. Yet 5G NR is expanding at a 14.67% CAGR, driven by industrial automation projects that need deterministic latency below 10 ms. Wi-Fi 6E is also scaling, but Wi-Fi 7 introduces 320 MHz channels, multi-link operation, and 4K-QAM, giving enterprises a non-cellular path to ultra-high throughput.

Hybrid deployments blending 5G and Wi-Fi 7 are emerging as the reference architecture in hospitals, smart factories, and higher-education campuses. Manufacturing plants use 5G for mobile robotics and safety-critical telemetry, while Wi-Fi handles bulk data offload for tablets and laptops. China's 5G-Advanced roll-out validates the technology's readiness for indoor broadband, fuelling component demand from active DAS and small-cell vendors. With each additional private licence granted, the In-Building Wireless market deepens its shift from operator-led to enterprise-controlled networks.

The in Building Wireless Market Report is Segmented by Component Type (Antenna, Distributed Antenna Systems, Cables, Repeaters, and Small Cells), Technology (4G/LTE, 5G NR, Wi-Fi 6/6E, and Wi-Fi 7), Frequency Band (Less Than 1 GHz, 1 - 6 GHz, and More Than 6 GHz), End-User Industry (Commercial, Residential, Industrial, and Public-Safety and Government), and Geography.

North America led the In-Building Wireless market with 34% revenue share in 2024, aided by CBRS spectrum liberalisation and FirstNet's USD 8 billion public-safety investment that funded 1,000 new cell sites. Enterprises in the United States adopt neutral-host architectures to consolidate carrier relationships and future-proof private-network ambitions. Wi-Fi 7 launches from multiple vendors accelerate refresh cycles, while Canada and Mexico leverage their automotive and aerospace clusters to justify private cellular rollouts inside plants.

Asia-Pacific is expanding at a 14.60% CAGR to 2030. China already hosts 4.4 million 5G base stations and plans to exceed 4.5 million within the forecast horizon as it digitalises manufacturing and logistics. Japan's licence regime supports sub-6 and mmWave hybrids in smart factories, and South Korea channels state incentives into campus networks at semiconductor fabs. India's electronic-manufacturing drive is supported by antenna localisation partnerships that trim import costs and shorten deployment lead times.

Europe shows steady uptake influenced by regulatory stringency around data privacy and building emissions. The 6 GHz allocation enlarges Wi-Fi capacity for dense venues, and French cities demonstrate the cost advantage of private 5G for municipal camera backhaul. German, British, and French enterprises lead adoption, while Central-Eastern manufacturers pilot private 5G to support Industry 4.0. Strict GDPR compliance requirements nudge buyers toward on-premises core networks and secure device-identity frameworks, shaping a security-first approach within the In-Building Wireless market.