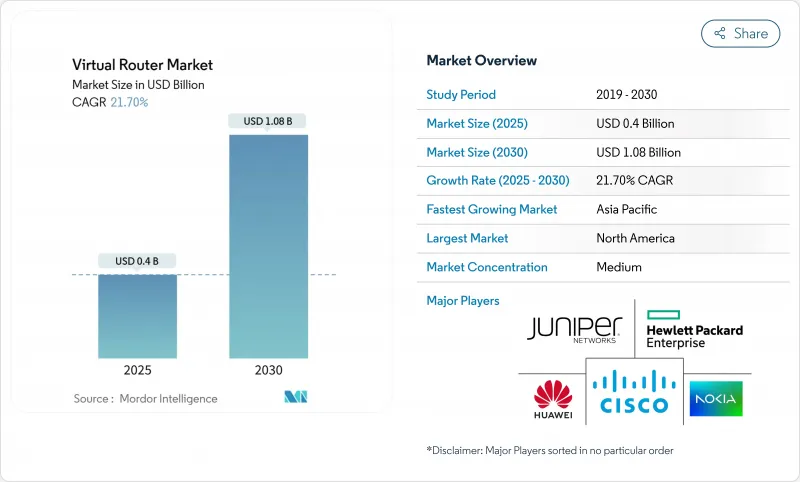

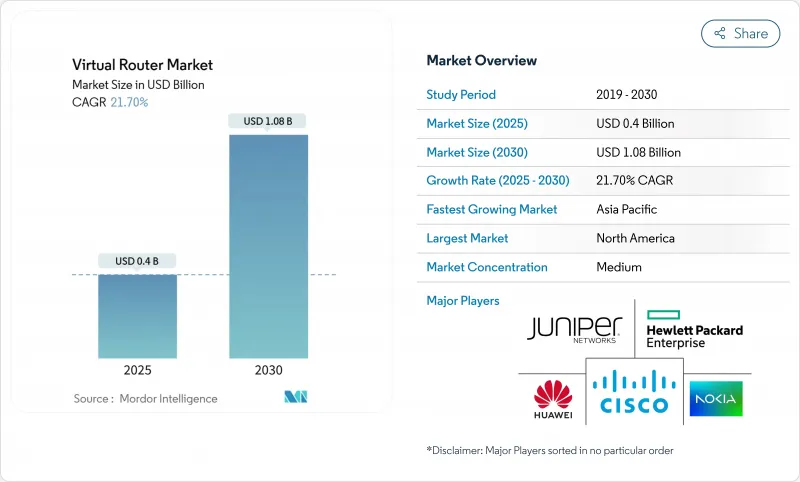

가상 라우터 시장 규모는 2025년에 4억 달러, 예측 기간(2025-2030년)의 CAGR은 21.70%를 나타내고, 2030년에는 10억 8,000만 달러에 달할 것으로 예측됩니다.

이 성장은 클라우드 네이티브 애플리케이션의 급증, 사설 5G의 상용 배포, 네트워크 민첩성을 높이면서 자본 지출을 줄이려는 움직임을 반영합니다. 기업이 소프트웨어 기반 라우팅을 선호하는 이유는 신속하게 확장하고, 오케스트레이션 도구와 통합할 수 있으며, 서비스 속도를 지원하여 제품의 신속한 배포와 운영 비용을 절감할 수 있기 때문입니다. 오픈소스 라우팅 스택이 많은 하이퍼스케일 데이터센터에서 활용되고 있는 반면, 클라우드 제공업체는 가상 라우팅 기능을 Infrastructure-as-a-Service에 직접 통합하여 진입 장벽을 낮추고 있습니다. HPE와 Juniper의 합병과 같은 대규모 합병에 대한 규제 상황의 조사는 규모와 포트폴리오의 충실도가 승패를 결정하게 되는 성숙한 상황을 보여줍니다.

서비스 제공업체와 기업은 인프라를 통합하고 운영 비용을 줄이기 위해 라우팅 워크로드를 소프트웨어로 마이그레이션합니다. 네트워크 기능이 몇 주가 아닌 몇 분 만에 시작되므로 스위치가 서비스 배포를 가속화합니다. 이탈리아 EOLO와 같은 운영자는 MANO가 배포한 가상 라우터에서 수천 개의 기지국 링크를 확장하여 이 모델이 전국적으로 작동한다는 것을 증명합니다. SDN 컨트롤러는 공급자가 대기 시간 및 대역폭 프로파일을 통해 분리해야 하는 5G 서비스에 네트워크 슬라이싱을 도입할 수 있도록 합니다. 그 결과 기업은 오케스트레이션 플랫폼에 투자를 쏟아 부어 소프트웨어 엔지니어링 팀의 인력을 늘리고 네트워크 운영을 민첩한 소프트웨어 파이프라인으로 전환하고 있습니다.

하이브리드 워크, 화상 회의 및 클라우드 워크로드는 트래픽을 데이터센터로 라우팅하는 전통적인 WAN 아키텍처에 스트레스를 주어 지연과 비용을 증가시킵니다. 중앙 정책 엔진에 의해 제어되는 가상 라우터는 트래픽을 클라우드 애플리케이션으로 직접 안내하고 원격 직원에게 일관된 사용자 경험을 제공합니다. 아시아태평양에서는 스마트 공장이 로봇 엔지니어링 및 IoT 센서용 저지연 링크에 의존하기 때문에 제조업체는 생산 이동 중에 재프로비저닝 가능한 소프트웨어 정의 라우팅을 도입하고 있습니다. 이러한 배포는 가상 라우터 시장이 물리적 트랙 롤 없이 동적 재구성을 지원하고 디지털 변환 프로그램의 속도와 일치하는 방식을 돋보이게 합니다.

멀티 테넌트 호스팅에서는 가상 라우터가 컴퓨팅 레이어와 하이퍼바이저를 공유하므로 공격 대상이 증가합니다. 콩코르디아 대학의 조사팀은 테넌트 분리를 우회할 수 있는 교차 레이어 공격을 확인했습니다. 이에 따라 ETSI는 NFV 보안 프레임워크를 업데이트하여 보다 강력한 능력 어설션과 암호화된 관리 채널을 통합했습니다. 금융 서비스와 정부 기관은 추가 침입 테스트와 감사 로깅을 요구하며, 이는 롤아웃을 지연시키지만 궁극적으로 플랫폼의 보안을 강화합니다.

2024년 가상 라우터 시장 수익의 60.3%를 창출했으며 솔루션 제품에 의한 것으로, 소프트웨어 라이선스와 가상 어플라이언스가 SD-WAN과 NFV의 기능을 요구하는 기업에 있어서 여전히 구매의 중심임을 확인했습니다. 이러한 이점은 라우팅 코드의 높은 가치, 경력 등급 규모의 필요성 및 이러한 라이선스가 네트워크 근대화 프로젝트에서 수행하는 중요한 역할에 의해 지원됩니다. 그러나 서비스는 성장 엔진이며 기업이 설계, 마이그레이션 및 관리 운영 전문 지식을 구매함에 따라 2030년까지 연평균 복합 성장률(CAGR)은 24.5%로 상승합니다. TIC 3.0의 의무화를 추진하는 많은 연방 정부 기관은 Software-Defined Routing으로 전환하는 동안 규정 준수를 보장하기 위해 통합업체에 의존하고 있습니다.

기업은 내부에 NFV 인력이 없기 때문에 서비스 제공업체는 자문 및 운영 서비스를 패키징하여 성공을 보장합니다. Managed Services는 가동 시간과 성능에 대한 서비스 수준 계약을 점점 더 통합하여 운영 위험을 고객으로부터 끌어들이고 있습니다. 이 패턴은 공급업체가 기술 체크리스트 대신 라이프사이클 서비스를 차별화하는 전략적 축족을 보여주며 가상 라우터 시장의 컨설팅 영업 활동을 강화하고 있습니다.

클라우드 기반 배포는 2024년 가상 라우터 시장 규모의 68.7%를 차지했으며 CAGR도 가장 빠른 25.01%를 기록했습니다. 기업은 하이퍼스케일 클라우드가 제공하는 즉각적인 가용성, 종량 과금의 경제성, 내장형 고가용성을 높이 평가합니다. Microsoft Virtual WAN Hub 라우팅 정책은 소프트웨어 라우팅이 외부 어플라이언스가 아닌 네이티브 클라우드 기능임을 나타냅니다. On-Premise의 도입은 로컬 데이터 처리를 필요로 하는 엄격한 규제 영역에서는 여전히 흔하지만, 보안 프레임워크가 성숙함에 따라 성장은 클라우드 모델에 뒤처져 있습니다.

제어 플레인은 클라우드에 배치되고 데이터 플레인은 대기 시간 이유로 On-Premise에 배치하는 하이브리드 패턴이 나타납니다. 공급업체는 추가 요금 없이 사이트를 가로질러 인스턴스를 이동할 수 있는 라이선싱으로 대응하여 채택을 강화하고 있습니다. 대역폭 집약적인 AI 워크로드가 급증하는 동안 클라우드 버스트는 여전히 주요 추진력이며 클라우드 호스팅 라우팅은 새로운 사이트의 기본값으로 자리 잡고 있습니다.

가상 라우터 시장은 구성 요소(솔루션 및 서비스), 배포 유형(클라우드 기반 및 On-Premise), 최종 사용자(서비스 제공업체, 엔터프라이즈 등), 용도(SD-WAN 및 WAN 에지, VCPE/에지 라우팅, VPN 및 네트워크 보안 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년 가상 라우터 시장 매출의 38.1%를 차지해 클라우드 채택과 SD-WAN의 조기 전개가 뒷받침되었습니다. AT&T와 같은 통신 사업자는 핵심 트래픽을 화이트 박스 라우팅으로 전환하고 소프트웨어 라우팅이 캐리어 등급이라는 명확한 신호를 보냅니다. 미국 전역의 기업이 가상 라우터를 제로 트러스트 아키텍처에 통합하고 캐나다 서비스 제공업체가 가상 라우터를 도입하여 지역 광대역을 확장하고 있습니다. 연방 정부 기관은 TIC 3.0 준수를 추진하고 지출 기세를 유지하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 23.8%로 가장 빠르게 성장하고 있으며, 일본, 한국, 인도에서 국가 지원의 5G 구축에 의해 지원되고 있습니다. 제조 및 광업에서 민간 5G 네트워크는 자율 기계를 제어하기 위해 국부적 인 라우팅이 필요하며 에지 대응 가상 라우터를위한 비옥한 토양을 생산합니다. GSMA는 이 지역의 사설 5G 투자가 급증할 것으로 예상하고 있으며 디지털 변환이 이러한 확대를 촉진할 것이라고 강조하고 있습니다.

유럽에서는 데이터 주권법이 소프트웨어 정의 상호 연결을 필요로 하는 국내 클라우드 지역을 뒷받침하고 있으며 안정적인 성장을 유지하고 있습니다. 통신사는 가격 규제 내에서 비용 절감을 위해 NFV를 도입했으며 EU의 Gaia-X 이니셔티브는 가상 라우팅을 따라 개방형 디지털 인프라를 추진하고 있습니다. 중동 및 아프리카는 스마트 시티 프로젝트에 투자하고 세계 벤더에게 공공 안전망의 에지 라우팅을 시험적으로 도입하게 합니다. 라틴아메리카에서는 핀테크 용도를 위한 신뢰할 수 있는 클라우드 연결을 요구하는 금융 허브를 중심으로 완만한 진전을 볼 수 있습니다.

The Virtual Router Market size is estimated at USD 0.4 billion in 2025, and is expected to reach USD 1.08 billion by 2030, at a CAGR of 21.70% during the forecast period (2025-2030).

Growth reflects the surge of cloud-native applications, the commercial rollout of private 5G, and the drive to trim capital outlays while boosting network agility. Enterprises prefer software-based routing because it scales rapidly, integrates with orchestration tools, and supports service velocity, enabling faster product rollouts and lower operating expenses. Competitive dynamics also favor the technology: open-source routing stacks now power many hyperscale data centers, while cloud providers embed virtual routing functions directly into infrastructure-as-a-service offerings, flattening barriers to entry. Regulatory scrutiny of large mergers, such as the contested HPE-Juniper deal, signals a maturing landscape where scale and portfolio depth increasingly decide winners.

Service providers and enterprises are shifting routing workloads onto software to consolidate infrastructure and cut operating expenses, achieving up to 60% savings when NFV replaces fixed hardware. The switch accelerates service rollouts because network functions spin up in minutes rather than weeks. Operators such as EOLO in Italy scaled thousands of base-station links with MANO-deployed virtual routers, proving the model works at a nationwide scale. SDN controllers also let providers introduce network slicing for 5G services that need isolation by latency or bandwidth profiles. As a result, companies pour investment into orchestration platforms and staff up software engineering teams, transforming network operations into agile software pipelines.

Hybrid work, video meetings, and cloud workloads stress legacy WAN architectures that route traffic back to a data center, adding latency and cost. Virtual routers, controlled by central policy engines, steer traffic directly to cloud applications, delivering a consistent user experience for remote staff. In Asia-Pacific, smart factories depend on low-latency links for robotics and IoT sensors, prompting manufacturers to deploy software-defined routing that can be re-provisioned during production shifts. These deployments highlight how the virtual router market supports dynamic reconfiguration without physical truck rolls, matching the speed of digital transformation programs.

Multi-tenant hosting increases attack surfaces because virtual routers share compute layers and hypervisors. Researchers at Concordia University identified cross-layer attacks that can bypass tenant isolation. In response, ETSI updated its NFV security framework to include stronger capability assertions and encrypted management channels. Financial services and government agencies demand additional penetration testing and audit logging, which slows rollouts but ultimately strengthens platform security.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solution offerings generated 60.3% of virtual router market revenue in 2024, confirming that software licenses and virtual appliances remain the core purchase for enterprises seeking SD-WAN and NFV capabilities. This dominance is underpinned by the high value of routing code, the need for carrier-grade scale, and the critical role these licenses play in network modernization projects. Services, however, are the growth engine, rising at 24.5% CAGR through 2030 as organizations purchase design, migration, and managed operations expertise. Many federal agencies pursuing TIC 3.0 mandates rely on integrators to ensure compliance while migrating to software-defined routing.

Enterprises lack in-house NFV talent, so service providers package advisory and run-operate services to guarantee success. Managed offerings increasingly embed service-level agreements for uptime and performance, transferring operational risk away from customers. The pattern indicates a strategic pivot, in which vendors differentiate on lifecycle services instead of technical checklists, reinforcing the virtual router market's consultative sales motion.

Cloud-based deployment captured 68.7% of the virtual router market size in 2024 and also posted the fastest 25.01% CAGR. Enterprises value instant availability, pay-as-you-grow economics, and built-in high availability offered by hyperscale clouds. Microsoft's Virtual WAN Hub routing policies illustrate how software routing becomes a native cloud function rather than an external appliance. On-premise deployments remain common in highly regulated sectors requiring local data processing, but their growth lags cloud models as security frameworks mature.

Hybrid patterns emerge in which control planes reside in the cloud while data planes stay on-premises for latency reasons. Vendors respond with licensing that moves instances across sites without additional fees, reinforcing adoption. As bandwidth-intensive AI workloads proliferate, cloud bursting remains a major driver, positioning cloud-hosted routing as the default for new sites.

Virtual Router Market is Segmented by Component (Solution and Service), Deployment Type (Cloud-Based and On-Premise), End-User (Service Provider, Enterprise, and More), Application (SD-WAN and WAN Edge, VCPE/Edge Routing, VPN and Network Security, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated the largest slice of the virtual router market revenue at 38.1% in 2024, boosted by cloud adoption and early SD-WAN rollouts. Telecom operators such as AT&T migrate core traffic to white-box routing, sending a clear signal that software routing is carrier-grade. Enterprises across the United States integrate virtual routers into zero-trust architectures, while Canadian service providers deploy virtual routers to extend broadband in rural regions. Federal agencies' push for TIC 3.0 compliance maintains spending momentum.

Asia-Pacific is the fastest mover at a 23.8% CAGR to 2030, supported by state-backed 5G build-outs in Japan, South Korea, and India. Private 5G networks in manufacturing and mining require localized routing to control autonomous machines, creating fertile ground for edge-ready virtual routers. The GSMA expects private 5G investment in the region to rise sharply, highlighting how digital transformation fuels this expansion.

Europe maintains steady growth as data-sovereignty laws encourage in-country cloud regions that need software-defined interconnects. Telecom operators deploy NFV to cut costs amid price regulation, and the EU's Gaia-X initiative promotes open digital infrastructure aligned with virtual routing. The Middle East and Africa invest in smart-city projects, inviting global vendors to pilot edge routing for public safety nets. Latin America experiences moderate progress, with adoption centered on financial hubs that demand reliable cloud connectivity for fintech applications.