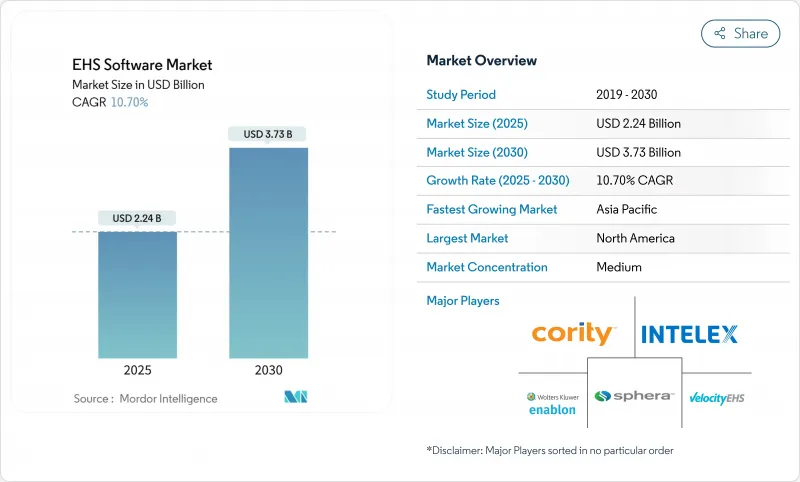

환경 보건 안전(EHS) 소프트웨어 시장의 2025년 시장 규모는 22억 4,000만 달러로 예상되며, 2030년에는 37억 3,000만 달러에 이르고, CAGR 10.7%를 나타낼 것으로 예측됩니다.

지속적인 규제 강화, 급속한 ESG 공식화, AI를 활용한 안전 분석으로의 전환이 이 확대를 지원하고 있습니다. 유럽에서는 CSRD(Corporate Sustainability Reporting Directive)가 지연되어 자동화된 컴플라이언스 워크플로에 대한 수요가 증가하고 있습니다. 운영 레벨에서 기업은 총 소유 비용을 줄이기 위해 SaaS 아키텍처를 선호합니다. 클라우드 배포는 이미 활성 배포의 62%를 차지하고 있으며 60%를 넘는 점유율을 통해 배포 전문 지식이 채택에 여전히 중요함이 나타났습니다. 대기업은 크로스보더 리스크에 대처하기 위해 플랫폼의 폭을 활용하고 있지만, 구독 가격에 의해 선행 투자 장벽이 제거되기 때문에 중소기업이 가장 급속히 이행하고 있습니다.

유럽 연합(EU)의 CSRD는 정보 공개의 범위와 빈도를 대폭 확대하고 있으며, 다국적 기업은 여러 법역의 보고 워크플로를 자동화해야 합니다. 미국에서는 뉴욕주 온실가스 보고 의무 등 컴플라이언스 위반에 대한 배상책임이 늘어나고 있습니다. 따라서 기업은 EHS 소프트웨어 시장 솔루션을 선제적인 법적 안전 가드로 취급합니다. 일본의 사이버 보안 전략은 공급망을 보호하기 위해 소프트웨어 BOM을 요구하고 있으며 통합 리스크 플랫폼에 대한 수요를 높이고 있습니다. 그 결과, 구조화된 데이터는 폭발적으로 증가하여 수작업에 의한 처리 능력을 넘어서고 있습니다.

ESG 공개의 의무화는 투자자 주도의 기대에서 법적 의무로 확대되었습니다. EU의 탄소 국경 조정 메커니즘을 통해 수입업체는 임베디드 배출량 추적을 의무화하고 세계 공급업체는 환경 데이터 취득을 제도화해야 합니다. 영국의 중소기업에서 ESG를 의식하고 있는 기업은 불과 19%에 불과하지만 새로운 규제가 정착됨에 따라, 화이트 스페이스에서의 채용의 가능성이 밝혀지고 있습니다. 케냐의 녹색금융분류법은 기후 변화에 대응한 프로젝트에 대출처를 유도하고 정보공개의 틀을 제도화하고 있습니다. 따라서 업계 관계자는 환경 보건 안전 소프트웨어 시장을 감사에 대응한 ESG 분석을 일상 업무에 통합하여 컴플라이언스를 실현하기 위한 확장성이 있는 루트로 간주하고 있습니다.

이탈리아의 소규모 제조업체는 디지털 안전 도입의 주요 억제요인으로 구매 가격, 시스템 전환의 복잡성 및 직원 교육을 꼽았습니다. 중소기업의 40%가 환경 데이터를 수집하고 있지만 성능 지표에 통합하는 기업은 단 18%입니다. 공급업체는 패키징된 온보딩 서비스와 템플릿화된 구성을 지원하지만 예산 제약이 여전히 전환을 늦추고 EHS 소프트웨어 시장의 단기 성장을 억제하고 있습니다.

2024년 EHS 소프트웨어 시장 점유율의 60%는 서비스였습니다. 규제 해석, 데이터 마이그레이션 및 사용자 교육이 프로젝트의 성공을 좌우합니다. ERA 엔바이로멘탈이 정한 도입 라이프사이클(평가, 탠덤 전개, 검증)은 컨설턴트의 재능이 필수적인 이유를 보여줍니다. 예측 기간 동안 AI와 ESG 모듈이 많은 기업들이 아웃소싱하는 복잡성을 추가하기 때문에 서비스와 관련된 EHS 소프트웨어 시장의 규모는 꾸준히 확대됩니다.

소프트웨어 판매는 클라우드 네이티브 제품군 및 모바일 확장 기능으로의 전환이 진행됨에 따라 CAGR 10.7%로 성장할 전망입니다. 공급업체는 구성 가능한 ESG 템플릿 및 AI 기반 리스크 엔진을 통합하여 설치 시간을 단축하고 정착도를 높입니다. 결과적으로 장기 마진 확대는 플랫폼 라이센서에게 유리하지만 단기 규모 확장은 기업 배포를 가속화하는 서비스 파트너에 따라 달라집니다.

클라우드 솔루션은 2024년 EHS 소프트웨어 시장 규모의 62%를 차지하였습니다. 데이터 중앙 집중식 관리, 탄력적인 스토리지, 즉각적인 패치 적용으로 오랜 보안 문제가 해결됩니다. 일본 기업은 디지털 전환의 세 번째 단계인 데이터 분석을 진행하고 있으며, 클라우드 인프라스트럭처가 얼마나 효율화를 지원하고 있는지를 부각하고 있습니다.

On-Premise 배포는 대기 시간, 주권 또는 맞춤형 워크플로가 로컬 제어를 필요로 하는 경우에 지속되지만, 성장은 클라우드로 인해 6% 둔화되었습니다. 업계별로는 네이티브 데스크톱 에디션의 폐지가 벤더 간에 진행되고 있으며, 규제가 엄격한 업종에서는 하이브리드 전략이 장려되고 있습니다. 다국적 기업이 서버 시설을 간소화하는 동안 EHS 소프트웨어 시장은 비용과 규모를 일치시키는 이용 기반 가격 설정에 더욱 기울어지고 있습니다.

EHS 소프트웨어 시장은 도입 형태별(클라우드, On-Premise), 컴포넌트별(소프트웨어, 서비스), 최종 사용자 업종별(석유 및 가스, 에너지 및 유틸리티, 기타), 솔루션 유형별(사고 및 안전 관리, 감사 및 검사 등), 조직 규모별(대기업, 기타), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년에 EHS 소프트웨어 시장 규모의 37.5%를 유지하였으며, 성숙한 OSHA 컴플라이언스 문화와 주 교통기관에 의한 조기 AI 도입이 성장을 지원하고 있습니다. UC San Diego Health와 같은 건강 관리 네트워크는 환자 결과를 개선하기 위해 AI에 2,200만 달러를 투자하고 있으며, 디지털 안전 도구에 대한 광범위한 경영진의 헌신을 보여줍니다. 사이버 위생에 관한 연방 정부의 지침이 클라우드 플랫폼에 대한 신뢰를 더욱 가속화하고 있습니다.

아시아태평양은 성장 엔진이며 2030년까지의 CAGR은 10.1%로 예상됩니다. 일본의 디지털 사회 우선 프로그램과 1조 5,400억엔(107억 달러)의 분기 소프트웨어 투자는 생산성 향상에 관한 민간과 정부 간 협력의 모범 사례입니다. 베트남과 인도의 지역 규제 당국은 화학물질과 기후에 관한 프레임워크를 조화시키고 있으며, EHS 소프트웨어 시장의 대응가능한 기반이 확대되고 있습니다.

유럽에서는 CSRD 기한이 다가오는 가운데 신중한 성장을 볼 수 있습니다. 기업은 감사팀을 동원하여 지속가능성 지표를 재무제표에 통합하여 보고 모듈의 지속적인 수요를 창출하고 있습니다. EU의 탄소 경계 조정 메커니즘은 간접적으로 무역 상대국에서 채택을 촉진하고 환경 보건 안전 소프트웨어 산업의 저변을 확대합니다.

The environmental health safety software market is valued at USD 2.24 billion in 2025 and is forecast to reach USD 3.73 billion by 2030, advancing at a 10.7% CAGR.

Persistent regulatory tightening, rapid ESG formalization and the shift toward AI-enabled safety analytics collectively anchor this expansion. European delays in the Corporate Sustainability Reporting Directive (CSRD) are generating pent-up demand for automated compliance workflows, while New York's mandatory greenhouse-gas disclosures preview similar obligations in other jurisdictions. At an operational level, enterprises favor software-as-a-service architectures to reduce total cost of ownership; cloud deployments already account for 62% of active installations, and services commanding 60% illustrate that implementation expertise remains critical for adoption.Large enterprises leverage platform breadth to address cross-border risk, yet small and mid-sized firms are the fastest movers because subscription pricing removes upfront capital barriers.

The European Union's CSRD markedly widens disclosure scope and frequency, compelling multinationals to automate multi-jurisdictional reporting workflows. Parallel action in the United States-such as New York's greenhouse-gas reporting requirement-signals rising liability for non-compliance. Businesses therefore treat environmental health safety software market solutions as a pre-emptive legal safeguard. Asian regulators are converging; Japan's cybersecurity strategy now requires Software Bills of Materials to protect supply chains, elevating demand for integrated risk platforms . The cumulative result is an unprecedented volume of structured data that exceeds manual processing capacity, turning automation into necessity rather than choice.

Mandatory ESG disclosures have expanded from investor-led expectations to statutory obligations. The EU's Carbon Border Adjustment Mechanism forces importers to track embedded emissions, compelling global suppliers to institutionalize environmental data capture. Only 19% of UK SMEs have any ESG awareness, revealing white-space adoption potential as new penalties take hold. Emerging economies are aligning; Kenya's Green Finance Taxonomy now directs lenders toward climate-aligned projects, institutionalizing disclosure frameworks. Industry practitioners therefore view the environmental health safety software market as a scalable route to compliance, embedding audit-ready ESG analytics into day-to-day operations.

Small manufacturers in Italy cite purchase price, system migration complexity and workforce training as principal inhibitors to digital safety adoption. Similar feedback is recorded across, economies, where 40% of SMEs collect environmental data but only 18% integrate it into performance metrics . Vendors respond with packaged onboarding services and templated configurations, yet budget constraints still delay conversions and trim near-term growth in the environmental health safety software market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Services held 60% of environmental health safety software market share in 2024 . Organizations acknowledge that platform acquisition addresses only a fraction of compliance complexity; regulatory interpretation, data migration and user training determine project success. The implementation lifecycle set out by ERA Environmental-assessment, tandem deployment and validation-illustrates why consultancy talent remains integral. Over the forecast period, the environmental health safety software market size linked to Services will expand steadily as AI and ESG modules add intricacy that many firms outsource.

Software revenue grows at an aligned 10.7% CAGR as buyers progress toward cloud-native suites and mobile extensions. Vendors embed configurable ESG templates and AI-based risk engines, compressing setup time and increasing stickiness. Consequently, long-term margin expansion favors platform licensors, yet near-term scale depends on service partners to accelerate enterprise roll-outs.

Cloud solutions commanded 62% of environmental health safety software market size in 2024. Centralized data management, elastic storage and instant patching outweigh long-standing security concerns. Japanese corporates have progressed to the third stage of digital transformation-data analytics underscoring how cloud infrastructure underpins efficiency gains .

On-premise installations persist where latency, sovereignty or bespoke workflows require localized control, but growth lags cloud by six percentage points. Vendors increasingly sunset native desktop editions, encouraging hybrid strategies in heavily regulated verticals. As multinationals rationalize server estates, the environmental health safety software market tilts further toward usage-based pricing that aligns cost with scale.

EHS Software Market is Segmented by Deployment Mode (Cloud, On-Premise), by Component (Software, Services) by End-User Vertical (Oil and Gas, Energy and Utilities, and More), by Solution Type (Incident and Safety Management, Audit and Inspection and More), by Organization Size (Large Enterprises and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retains 37.5% of environmental health safety software market size in 2024, underpinned by mature OSHA compliance culture and early AI adoption by state transportation agencies. Healthcare networks such as UC San Diego Health invest USD 22 million in AI to elevate patient outcomes, demonstrating broad management commitment to digital safety tools . Federal guidance on cyber hygiene further accelerates trust in cloud platforms

Asia-Pacific is the growth engine, poised for 10.1% CAGR through 2030. Japan's Digital Society priority program and JPY 1.54 trillion (USD 10.7 billion) quarterly software investments exemplify government-private collaboration on productivity gains. Regional regulators-from Vietnam to India-are rolling out harmonized chemical and climate frameworks, expanding the environmental health safety software market addressable base.

Europe shows measured growth as CSRD deadlines loom. Corporates mobilize audit teams to integrate sustainability metrics with financial statements, creating recurring demand for reporting modules . The EU Carbon Border Adjustment Mechanism indirectly pulls adoption in trading partners, broadening the environmental health safety software industry footprint.