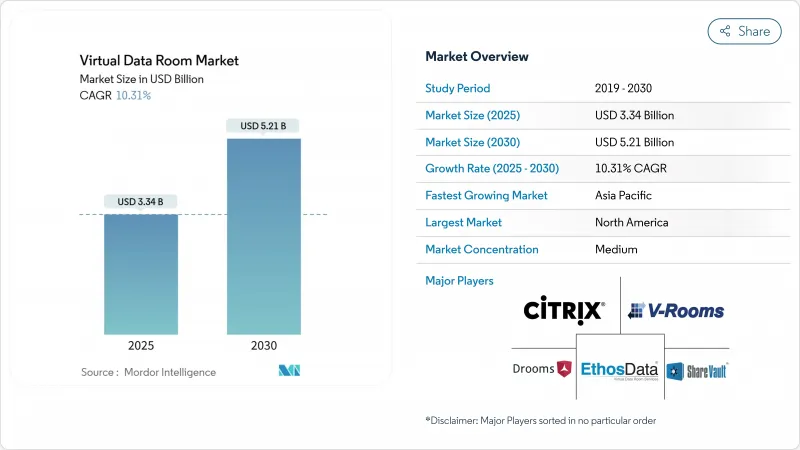

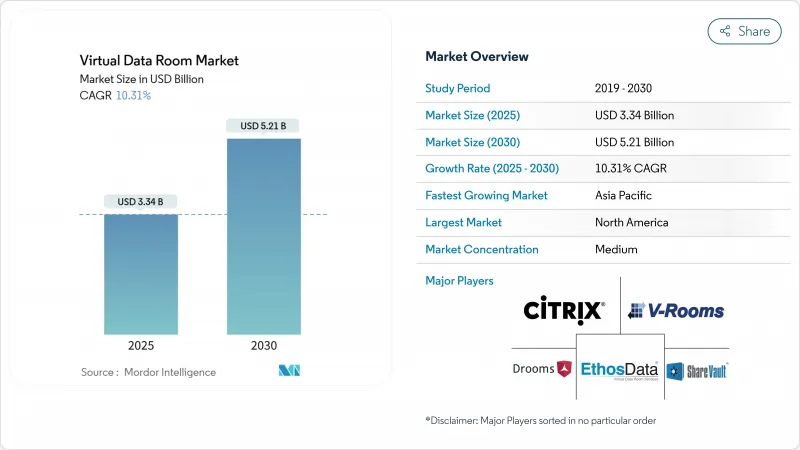

가상 데이터룸 시장 규모는 2025년 33억 4,000만 달러로 추정되고, 2030년 52억 1,000만 달러에 이를 것으로 예측되며, CAGR 10.31%로 성장할 전망입니다.

규제 강화에 대응하고 국경을 넘는 거래를 합리화하기 위해 기업이 기밀 문서의 디지털화를 가속화함에 따라 수요가 확대되고 있습니다. 거래는 대규모화되고 복잡해지고 있으며, 기업은 실사 및 합병 후의 통합에 안전한 AI 대응 플랫폼의 도입을 추진하고 있습니다. 중국의 네트워크 데이터 보안 관리 규제와 EU 데이터 법은 공급업체에게 스토리지 현지화와 섬세한 감사 추적을 통합하고 있으며 EMEA와 아시아태평양 모두에서 시장 확대를 강화하고 있습니다. 구독 기반 모델이 월400-1,000달러로 떨어졌으며 과거 비용 장벽이 제거되었습니다. 생명 과학 문서의 eCTD 뷰어와 같은 업계 특화된 기능은 CAGR 15.2%에서 가장 급성장하는 최종 사용자 업종인 헬스케어와 바이오테크놀러지에 더욱 기세를 주고 있습니다.

크로스보더 M&A의 거래액은 2024년에 5% 증가했지만 거래 건수는 감소하고 있으며, 독점금지법, 외국투자법, 데이터 및 프라이버시법 등 중복되는 법규제를 충족해야 하는 고액 거래로의 시프트가 부각되고 있습니다. 아랍에미리트(UAE)의 새로운 합병 규제 기준과 독일 FDI 필터의 엄격화는 구매자가 직면한 승인 미로를 이야기하고 있습니다. 인도의 디지털 개인 데이터 보호법은 명시적인 동의와 국가별 처리 조항을 요구하며 정보 흐름을 더욱 복잡하게 만듭니다. 공급업체는 데이터 주권 토글 및 실시간 규제 체크리스트를 통합하여 거래 팀이 법률별로 문서 위치, 사용자 액세스 및 보관 기간을 매핑할 수 있도록 합니다.

아시아태평양의 금융 기관은 비용 절감 및 컴플라이언스의 현대화를 위해 클라우드 마이그레이션을 가속화하고 있지만, 93%는 감사 요구에 부응하기가 어렵다고 응답하고 있으며, 로그를 불변할 수 있는 보안 이사회 포털 투자에 박차를 가하고 있습니다. 중국의 데이터 보안 관리 방식에서는 은행이 정보를 분류하고 모든 액세스 이벤트를 문서화해야 합니다. 나스닥의 자회사 거버넌스에 대한 특허는 규제 당국의 검토를 간소화하는 다중 엔티티의 데이터 계층화 추진을 보여줍니다.

EU의 GDPR(EU 개인정보보호규정)과 미국의 CLOUD법 간의 갈등으로 인해 다국적 기업은 스토리지를 구분하거나 강제 조치의 위험을 맡아야 하며, 공급자는 독일, 일본, 호주에 지역 데이터센터를 개설할 수밖에 없습니다. 중국의 Trusted Data Space 청사진은 마찬가지로 외국으로의 전송을 제한하고 인프라 이중화를 위한 설비 투자를 늘리고 있습니다. 독일 중소기업은 또한 NIS-2와 DORA 사이버 보안 규정을 충족해야 하며 공급업체 선택에 영향을 미치는 규정 준수 오버헤드를 추가하고 있습니다.

2024년 매출의 68%는 소프트웨어가 차지하였고, 가상 데이터룸 시장의 핵심임을 뒷받침합니다. 그러나 규제 컨설팅, AI 분석 및 통합 지원을 요구하는 고객이 증가함에 따라 서비스 부문의 CAGR은 13.9%로 빠르게 확대되고 있습니다. 대규모 고객은 워크플로우 설계 프로젝트에 플랫폼 라이선스를 번들하는 경향이 강해지고 있으며, SS&C의 2024년 매출이 48억 4,000만 달러로 증가한 것을 반영하고 있습니다. 영국의 65억 달러 G-Cloud 14와 같은 정부 입찰도 매니지드 서비스를 지정했으며, 순수한 소프트웨어 딜리버리에서 성과 기반 계약으로의 전환을 검증하고 있습니다.

거래가 프라이버시 시스템에 걸친 경우 프리미엄 서비스에 대한 수요가 증가하고 공급업체는 데이터 잔여 규칙, 보존 일정 및 AI 주도 재편집 모델을 설정하는 전문 팀을 배치하게 됩니다. 그 결과 도입 컨설팅, 워크플로우 자동화, 온콜 컴플라이언스 자문는 2030년까지 시장 지출 증가분의 30% 이상을 차지할 것으로 예측됩니다. 따라서 서비스 흐름은 코어 라이선싱에서 가격 압력에 대한 헤지 역할을 하며 기존 기업에 대한 수익의 다양성을 강화합니다.

클라우드 전개는 2024년 수익의 83%를 차지하였고, CAGR 14.6%로 가장 높은 성장 속도를 보여줍니다. 이는 하이퍼스케일 인프라가 이제 은행 수준의 관리를 충족할 수 있는 시장 합의를 보여줍니다. 기가바이트당 요금은 월 60-77달러이며 여전히 헤비 데이터 사용자에게 영향을 미치고 있지만 월 400-1,000달러의 정액 옵션은 중견 구매자의 전환을 촉구하고 있습니다. 주권 조항에 따라 일부 고객은 온프레미스에 민감한 아카이브를 남기고 분석 컴퓨팅을 클라우드로 마이그레이션하는 하이브리드 설정으로 조타합니다.

공급자는 규제 당국이 클라우드를 동등하거나 그 이상의 관리 환경으로 인정하도록 멀티 테넌트 암호화 및 고객 관리 키에 투자합니다. 퍼블릭 클라우드 리전이 전 세계적으로 구축됨으로써 대기 시간을 줄이면서 거주 규정을 충족하는 근접성이 생겨 지리적으로 분산된 거래 팀에 대한 도입이 가속화됩니다. 기술적 신뢰가 높아짐에 따라 기존 온프레미스 설치는 2030년까지 가상 데이터룸 시장의 10% 이하로 줄어들 것으로 예측됩니다.

북미는 충실한 자본 시장, 활발한 프라이빗 주식 활동, 명확한 정보 공시법에 힘입어 2024년 매출의 41%를 차지했습니다. 이 지역의 가상 데이터룸 시장 규모는 에너지, 헬스케어, 기술 분야의 리피터가 매년 여러 사건의 파이프라인을 실행함으로써 지원되고 있습니다. SS&C의 2024년 매출이 48억 4,000만 달러로 증가한 것은 이 수요를 뒷받침합니다.

유럽에서는 팬데믹 후 M&A 회복이 가속화되고 있으며 2025년에는 거래량이 10% 증가할 것으로 예측됩니다. EU 데이터 방법은 API가 풍부한 플랫폼과 지역 내 스토리지 노드가 있는 공급업체에게 유리한 상호 운용 의무를 추가합니다. 독일에서는 대일 직접 투자 감시가 강화되고 중견기업의 사모 펀드가 회복되고 있기 때문에 VDR을 이용한 실시간 질의응답과 재편집이 클로징 타임라인을 단축하는 이용 사례가 탄생합니다.

아시아태평양의 CAGR은 14.4%로 가장 높습니다. 중국의 금융기술 개발계획과 데이터보안규제가 국내 호스팅을 강제하고 세계 프로바이더가 합작투자와 소블린 클라우드의 설립을 촉구하고 있습니다. 일본의 리갈텍이 주도하는 전자기기 공급망 서비스는 업계 특유의 컴플라이언스에 대응하는 현지화된 혁신을 강조하고 있습니다. 인도의 새로운 데이터 프라이버시법은 하이테크와 제약의 크로스보더 거래에서의 채용을 촉진하여 2030년까지 성장 엔진으로서 APAC의 역할을 확고히 합니다.

The virtual data room market size is valued at USD 3.34 billion in 2025 and is forecast to reach USD 5.21 billion by 2030, registering a 10.31% CAGR.

Demand is expanding as enterprises accelerate the digitization of sensitive documents to meet tightening regulatory mandates and to streamline cross-border transactions. Deals are becoming larger and more complex, pushing corporates to adopt secure, AI-enabled platforms for due diligence and post-merger integration. China's Network Data Security Management Regulations and the EU Data Act are compelling providers to localize storage and embed granular audit trails, reinforcing market expansion in both EMEA and Asia-Pacific. Large enterprises still generate most revenue, yet SMEs are the fastest-growing buyers because subscription-based models have fallen to USD 400-1,000 per month, removing historical cost barriers. Industry-specific functionality-such as eCTD viewers for life-sciences dossiers-adds further momentum in healthcare and biotech, the fastest-growing end-user vertical at 15.2% CAGR.

Cross-border deal values rose 5% in 2024 even as volumes slipped, highlighting the shift toward high-stakes transactions that must satisfy overlapping antitrust, foreign investment, and data-privacy laws. New merger-control thresholds in the UAE and stricter FDI filters in Germany illustrate the maze of approvals buyers confront. India's Digital Personal Data Protection Act requires explicit consent and country-specific processing clauses, further complicating information flows. Vendors are embedding data-sovereignty toggles and real-time regulatory checklists so deal teams can map document location, user access, and retention periods by jurisdiction.

Financial institutions in Asia-Pacific are accelerating cloud migration to cut costs and modernize compliance, yet 93% cite difficulty meeting audit demands, fueling investment in secure board portals with immutable logs. China's Data Security Management Measures oblige banks to classify information and document every access event, a mandate now hard-wired into enterprise-grade VDRs. Nasdaq's patent for subsidiary governance showcases the push for multi-entity data hierarchies that streamline regulator reviews.

Conflicts between the EU's GDPR and the US CLOUD Act force multinationals to compartmentalize storage or risk enforcement action, driving providers to open regional data centers in Germany, Japan, and Australia. China's Trusted Data Space blueprint similarly restricts outbound transfers, raising capex for infrastructure duplication. German SMEs must also meet NIS-2 and DORA cybersecurity controls, adding compliance overhead that influences provider selection.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software anchored 68% of revenue in 2024, underscoring its status as the backbone of the virtual data room market. The services component, however, is scaling faster at 13.9% CAGR as clients seek regulatory consulting, AI analytics, and integration support. Large accounts increasingly bundle platform licenses with workflow-design projects, mirroring SS&C's revenue uplift to USD 4.84 billion in 2024. Government tenders such as the UK's USD 6.5 billion G-Cloud 14 are also specifying managed services, validating a shift from pure software delivery to outcome-based engagements.

Demand for premium services rises when transactions span privacy regimes, prompting vendors to position specialized teams that configure data-residency rules, retention schedules, and AI-driven redaction models. As a result, implementation consulting, workflow automation, and on-call compliance advisory are expected to command over 30% of incremental market spend by 2030. The services stream therefore acts as a hedge against price pressure in core licensing, reinforcing revenue diversity for established players.

Cloud delivery captured 83% of 2024 revenue and exhibits the highest growth pace at 14.6% CAGR, signalling market consensus that hyperscale infrastructure can now satisfy bank-grade controls. Per-gigabyte fees-ranging from USD 60-77 per month-still influence heavy-data users, but flat-rate options at USD 400-1,000 monthly encourage midsize buyers to migrate. Sovereignty clauses are steering some clients to hybrid setups where sensitive archives stay on-premise while analytics compute bursts into the cloud.

Providers invest in multi-tenant encryption and customer-managed keys so that regulators accept cloud as an equivalent or superior control environment. The global build-out of public-cloud regions creates proximity that slices latency while satisfying residency statutes, accelerating adoption in geographically dispersed deal teams. As technological confidence mounts, legacy on-premise installations are expected to shrink below 10% of the virtual data room market by 2030.

The Virtual Data Room Market is Segmented by Component (Software, Services), Deployment Mode (Cloud-Based, On-Premise), Organization Size (SMEs, Large Enterprises), by Business Function (Legal and Compliance, Financial Management, Intellectual-Property Management, and More), End-User Industry (BFSI, IT and Telecom, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated 41% of 2024 revenue, supported by deep capital markets, robust private equity activity, and well-defined disclosure laws. The virtual data room market size for the region is buoyed by repeat buyers in energy, healthcare, and technology sectors that execute multi-deal pipelines annually. SS&C's rise to USD 4.84 billion revenue in 2024 underscores this demand.

Europe is gaining momentum as M&A recoveries accelerate post-pandemic, with expected 10% volume growth in 2025. The EU Data Act adds interoperability obligations that favor vendors with API-rich platforms and in-region storage nodes. Germany's heightened FDI scrutiny and mid-cap private equity rebound create use cases where VDR-enabled real-time Q&A and redaction speed closing timelines.

Asia-Pacific posts the highest CAGR at 14.4%. China's Financial Technology Development Plan and data-security regulations compel domestic hosting, prompting global providers to establish joint ventures and sovereign clouds. Japan's LegalTech-led services for electronics supply chains highlight localized innovation that addresses industry-specific compliance. India's new data-privacy law drives adoption in tech and pharma cross-border deals, cementing APAC's role as a growth engine through 2030.