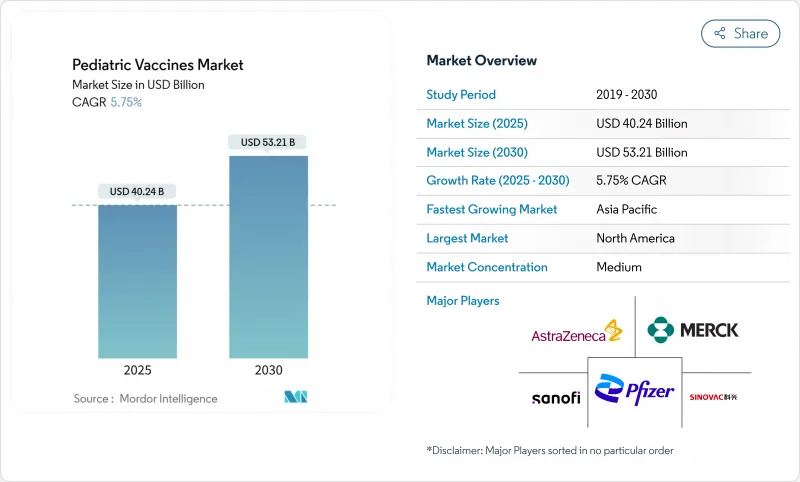

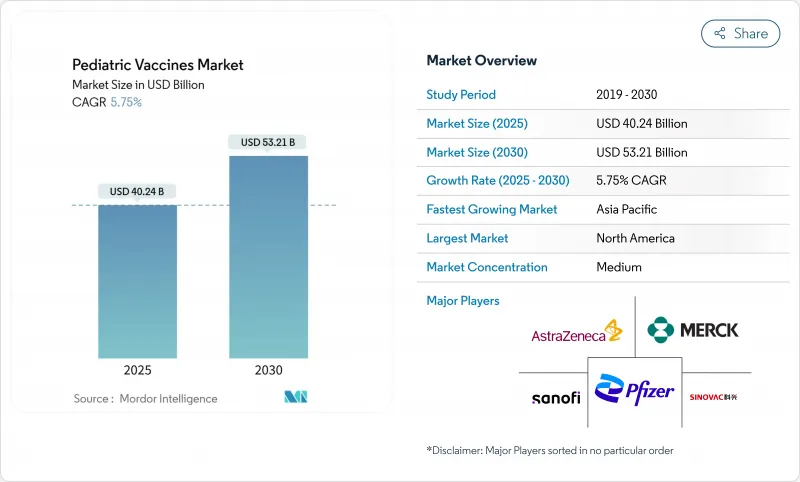

소아용 백신 시장의 2025년 시장 규모는 402억 4,000만 달러로 추정되고, 2030년에는 532억 1,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 5.75%로 견조하게 추이할 전망입니다.

강력한 정부 자금, 다가 제형에 대한 선호도 증가, mRNA 및 기타 차세대 플랫폼의 급속한 스케일 업이 이러한 성장의 기세를 지원합니다. 미국의 'Vaccines for Children Program'과 선진적인 COVID-19 예방약에 대한 50억 달러의 투자 'Project NextGen' 등으로 대표되는 공적 예방접종 예산의 확대는 계속 생산량을 뒷받침하며 기술 혁신에 박차를 가하고 있습니다. 동시에 디지털 공급망 자동화 및 블록체인 기반 추적성 솔루션은 세계 백신 유통에 여전히 영향을 미치는 1/3 폐기율을 억제하고 연간 300억 달러의 가치를 보호하는 것을 목표로 하고 있습니다. 또한 임산부에 대한 RSV 예방 접종이 일상적으로 이루어지게 되고, 제조업체가 보다 고활성의 결합제나 재조합 후보 백신을 상업 규모로 하면서 시장 기회가 확대되고 있습니다.

홍역의 유행은 면역 격차의 확대를 부각하고 있으며, 베트남에서는 2025년에 8만 1,691건의 의혹 사례가 기록되어 2020년 이후 최고가 되었습니다. 사하라 이남 아프리카의 일부에서는 백일해와 수두가 마찬가지로 급증하고 긴급 캐치업 캠페인을 촉구하며, 단기 조달 급증과 정기 접종 강화를 위한 장기적인 노력이 진행되고 있습니다. 마찬가지로 소아의 인플루엔자 사망률도 여전히 정책상의 급소가 되고 있으며, 각국 기관은 계절성 백신 접종의 메시지를 강화하고 면역원성이 높은 애주번트 제제나 세포 기반 제제에 중점을 두게 되어 있습니다. 이러한 역학적 압력은 콜드체인 업그레이드 및 개별 접종 완료를 추적하고 실시간으로 탈락 플래그를 설정하는 POS 디지털 등록에 대한 투자를 자극합니다. 이러한 시책은 총체로서 편리성을 중시한 배합제에 대한 수요를 확대하고 신규 항원의 조기 승인을 촉구하는 것입니다.

Project NextGen은 소아과에서 평가할 수 있는 점막 백신과 범 코로나 바이러스 후보에 50억 달러를 투입하여 변혁적 예방법에 대한 연방 정부의 장기적인 헌신을 보여줍니다. 이와 병행하여, Gavi의 2026-2030년 전략은 최소 90억 달러의 새로운 기증자 서약을 요구하고 현지 생산을 위한 아프리카 백신 제조 가속기에 12억 달러를 할당합니다. 액세스 측면에서 미국 '어린이를 위한 백신 프로그램'이 확실히 자기 부담을 없애고, 기준선량을 안정시키며, 제조업체를 수요 쇼크로부터 지키고 있습니다. 이러한 다층 자금 조달의 틀은 기술 혁신의 위험을 줄이고, 투자 회수 기간을 단축하며, 소아의 미충족 요구를 목표로 하는 다양한 후기 단계의 파이프라인을 유지하는 데 도움이 됩니다.

CDC는 현재 2세까지 36회, 18세까지 70회 이상의 예방접종을 권장하고 있으며, 전문가에 의한 분석에 따르면, 어린이 1명당 공적기관이 약 1,452달러, 민간 기업이 2,012달러의 비용을 부담하고 있습니다. 최근 Gavi의 지원으로 이행한 중소득국은 정가가 국가의 구매력을 상회하고 기증자의 지원도 축소하고 있기 때문에 가장 압박감을 느끼고 있습니다. 혼합 백신은 지출을 어느 정도 완화하지만, mRNA와 같은 새로운 플랫폼은 고급 바이오프로세스와 유통에 소요되는 비용 때문에 여전히 가격이 비쌉니다. 따라서 조달기관은 예산 범위를 벗어나지 않고 커버율을 유지하기 위해 성과 기반 계약과 풀링된 사전구매 계약을 시험적으로 도입하고 있습니다.

다가 제형은 2024년 소아용 백신 시장 매출의 62.43%를 차지하였고, 여러 항원을 1회 주사로 투여함으로써 의료 시스템의 효율성이 분명히 향상됨을 보여줍니다. 이 부문은 물류의 단순화, 클리닉의 진찰 횟수 감소, 간병인의 수용 태세 개선 등의 이점이 있으며, 이들 모두가 투여 누출률을 저하시켜 집단 면역 지속에 기여합니다.

1가 제품 수요는 계속 견고하고 단항원 부스터, 신속한 아웃브레이크 대책, 면역 결핍아에 대한 예방 접종 등 틈새 용도가 출현하고 있기 때문에, 2030년까지 연평균 복합 성장률(CAGR)은 6.66%로 성장할 전망입니다. 매사추세츠 공과대학(MIT)의 시간 방출 미립자 기술과 같은 혁신적인 기술은 별도의 용량을 단일 주사로 패키징함으로써 단일 항원 접근법과 다항원 접근법의 경계를 모호하게 할 것을 약속합니다. 국가의 스케줄이 임산부 RSV와 수막염균 예방 확대 등으로 확대되는 가운데 소아용 백신 시장은 편리성을 중시한 다가 백신의 섭취와 특정 역학적 갭에 대처하는 표적을 좁힌 1가 백신의 개입의 균형을 유지할 것으로 보입니다.

결합형 백신은 20년에 걸친 캡슐화 세균에 대한 임상 실적과 거의 모든 초년도 스케줄에 통합에 지지되어 2024년 매출에서 36.24%의 리드를 유지했습니다. 그럼에도 불구하고 세계적인 수요의 급증에 대응하기 위해 제조업체가 고수율 발현 시스템과 확장 가능한 바이오리액터를 활용하고 있기 때문에 재조합 기술은 CAGR 6.59%로 가장 급속히 진보하고 있습니다.

재조합 후보 약물의 소아용 백신 시장 규모는 사노피의 PCV21과 같은 고활성 구조물이 3단계를 넘어 입찰 주기에 들어갈 때 크게 확대될 것으로 예측됩니다. 동시에, 다가 mRNA-DTP 프로토타입은 백일해 면역 저하를 해결하기 위해 재조합 및 핵산 플랫폼이 어떻게 협력할 수 있는지를 보여줍니다. 이 수렴은 포트폴리오의 갱신 속도를 가속화하고 기존에는 한 줌의 기존 기업이 지배하고 있던 복잡한 항원 시장에 중견 제조업체가 비용 효율적인 루트로 진입할 수 있게 되었습니다.

북미는 2024년 세계 매출의 39.12%를 차지했으며, GSK의 5-in-1 수막염균 예방주사와 머크의 VAXNEUVANCE 소아 적응 등 견고한 상환제도, 엄격한 취학의무, FDA 승인의 지속에 뒷받침되고 있습니다. 그럼에도 불구하고 이 지역은 보험적용 기준을 위협하는 예방 접종에 어려움을 겪고 있으며, 새로운 디지털 리마인더 캠페인과 약사가 관리하는 프로그램을 통해 예방 접종의 진료율을 높게 유지하려고 합니다. 북미의 소아용 백신 시장 규모는 다병원성 후보 약물을 개발하는 국내 제조업체의 기술적 위험을 줄이는 Project NextGen의 자금 지원에 의해 더욱 유지되고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 6.78%로 가장 높을 것으로 예측됩니다. 원동력이 되는 것은 대규모 출생 코호트, 가처분 소득 증가, 2023년까지 부스터 접종률이 83%에 달한 인도의 폐렴구균 결합형 폐렴구균의 확대 성공과 같은 국가적 전개 등입니다. 베트남이나 인근 국가에서는 홍역이 급증하고 백신의 긴급 비축이나 신속한 입찰에 박차가 걸려 있습니다. APEC과 같은 지역ㅍ기관은 COVID-19의 혼란에 접종을 보류한 2,300만 명의 어린이들에게 백신 접종을 목표로 하는 10년 계획을 채택하고 있으며, 급성장 경제권에서 소아용 백신 시장의 지속적인 기세를 보여줍니다.

유럽은 유럽 위원회의 중앙 집중화된 제조 및 판매 승인 프로세스를 통해 조화로운 액세스를 가속화하고 상당한 점유율을 유지하고 있습니다. 최근 승인된 화이자의 PREVENAR 20은 유아와 청소년을 대상으로 폐렴구균의 혈청형을 지금까지 가장 폭넓게 커버하고, 회원국 전체에서 결합형 폐렴구균의 섭취를 확고하게 하고 있습니다. 그러나 일부 국가에서는 예산의 상한이 있기 때문에 가치 기반 조달이 중요하며, 상환에 대한 심의는 실제 유효성 데이터와 관련성이 높아지고 있습니다.

중동, 아프리카 및 남미에서는 다양한 상황을 볼 수 있습니다. 아프리카 연합(AU)의 일부 회원국은 Gavi의 공동 자금을 활용하고 African Vaccine Manufacturing Accelerator(아프리카 백신 제조 가속기) 하에서 자국에서 제조 체제를 구축하고, 페루와 이웃 시장은 팬데믹 중에 잃어버린 소아기의 정기적인 접종 회복을 위해 노력하고 있습니다. 전체적으로 자금과 인프라는 불균질하기 때문에 성장률은 세계 평균을 밑돌겠지만, 기증자의 목표를 좁힌 이니셔티브, 기술이전 협정, 콜드체인의 현대화로 이들 지역 전체에서 소아용 백신 시장은 점차 개선되고 있습니다.

The pediatric vaccines market is valued at USD 40.24 billion in 2025 and is forecast to reach USD 53.21 billion by 2030, advancing at a steady 5.75% CAGR over the period.

Strong governmental funding, a growing preference for multivalent formulations and the rapid scale-up of mRNA and other next-generation platforms are sustaining this growth momentum. Expanded public immunization budgets, exemplified by the United States Vaccines for Children Program and the USD 5 billion Project NextGen investment in advanced COVID-19 prophylaxis, continue to underpin volumes and spur innovation. At the same time, digital supply-chain automation and blockchain-based traceability solutions aim to curb the one-in-three wastage rate that still affects global vaccine distribution, thereby protecting up to USD 30 billion in value annually. Market opportunities are also widening as maternal RSV immunization enters routine use, and as manufacturers bring higher-valent conjugates and recombinant candidates to commercial scale.

Measles outbreaks underscore widening immunity gaps, with Vietnam recording 81,691 suspected cases in 2025, the highest since 2020 . Similar spikes in pertussis and varicella across parts of Sub-Saharan Africa are prompting emergency catch-up campaigns, driving short-term procurement surges and longer-run commitments to reinforce routine schedules. Influenza mortality among children likewise remains a policy flashpoint, leading national agencies to intensify seasonal vaccination messaging and pivot toward highly immunogenic adjuvanted or cell-based formulations. These epidemiological pressures are stimulating investment in cold-chain upgrades as well as point-of-care digital registries that track individual dose completion and flag drop-outs in real time. Collectively, such measures expand demand for convenience-oriented combination products and encourage accelerated approvals for novel antigens.

Project NextGen channels USD 5 billion into mucosal and pan-coronavirus candidates poised for pediatric evaluation, signalling long-term federal commitment to transformative prophylaxis. In parallel, Gavi's 2026-2030 strategy seeks at least USD 9 billion in new donor pledges and allocates USD 1.2 billion to the African Vaccine Manufacturing Accelerator to localize production. At the access end, the United States Vaccines for Children Program reliably removes out-of-pocket costs, stabilizing baseline volumes and insulating manufacturers from demand shocks. Such multi-tiered funding frameworks de-risk innovation, shorten payback horizons and help sustain a diversified late-stage pipeline targeting unmet pediatric needs.

The CDC now recommends 36 doses before age 2 and more than 70 by age 18, translating into public-sector costs of roughly USD 1,452 and private-sector outlays of USD 2,012 per child according to peer-reviewed analyses. Middle-income economies that recently transitioned out of Gavi support feel the squeeze most acutely, as list prices outpace national purchasing power yet donor assistance winds down. Combination vaccines mitigate some expenditure, but newer platforms such as mRNA still carry premium price tags owing to sophisticated bioprocessing and distribution overheads. Consequently, procurement agencies are piloting outcome-based contracts and pooled advance purchase agreements to preserve coverage levels without breaching budget ceilings.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Multivalent formulations captured 62.43% of pediatric vaccines market revenue in 2024, illustrating the clear efficiency gains health systems achieve when several antigens are delivered in one injection. The segment benefits from simplified logistics, reduced clinic visits and improved caregiver acceptance, all of which lower missed-dose rates and contribute to sustained herd immunity.

Demand for monovalent products remains resilient, growing at a 6.66% CAGR through 2030 as niche applications emerge for single-antigen boosters, rapid outbreak control and immunisation of immunocompromised children. Innovations such as MIT's time-release microparticle technology promise to blur the line between single and multi-antigen approaches by packaging separate doses into one shot. As national schedules widen to include maternal RSV and expanded meningococcal protection, the pediatric vaccines market will continue to balance convenience-driven multivalent uptake against targeted monovalent interventions that address specific epidemiological gaps.

Conjugate vaccines maintained a 36.24% revenue lead in 2024, buoyed by two decades of clinical performance against encapsulated bacteria and their inclusion in nearly all first-year schedules. This dominance is unlikely to diminish soon; nevertheless, recombinant technologies are advancing the fastest at 6.59% CAGR as manufacturers exploit high-yield expression systems and scalable bioreactors to meet surging global demand.

The pediatric vaccines market size for recombinant candidates is forecast to expand materially once higher-valent constructs like Sanofi's PCV21 move beyond Phase 3 and enter tender cycles. Concurrently, multivalent mRNA-DTP prototypes illustrate how recombinant and nucleic-acid platforms can cooperate to address waning pertussis immunity. This convergence accelerates portfolio refresh rates and provides mid-tier manufacturers with a cost-effective route into complex antigen markets traditionally controlled by a handful of incumbents.

The Pediatric Vaccines Market is Segmented by Vaccine Valence (Monovalent and Multivalent), Technology Platform (Live Attenuated, Inactivated, Toxoid, and More), Indication (DTP (Diphtheria-Tetanus-Pertussis), Pneumococcal Disease, and More), Distribution Channel (Public and Private), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

North America controlled 39.12% of global revenue in 2024, buoyed by robust reimbursement systems, stringent school-entry mandates and a continuous stream of FDA approvals such as GSK's 5-in-1 meningococcal shot and Merck's VAXNEUVANCE pediatric indication. The region nonetheless grapples with pockets of hesitancy that threaten coverage thresholds, prompting new digital reminder campaigns and pharmacist-administered programs to keep uptake high. The pediatric vaccines market size in North America is further sustained by Project NextGen funding that lowers technological risk for domestic manufacturers developing multi-pathogen candidates.

Asia-Pacific is forecast to post the highest 6.78% CAGR through 2030. Drivers include large birth cohorts, rising disposable incomes and national rollouts such as India's successful pneumococcal conjugate expansion, which reached 83% booster coverage by 2023. Yet infrastructure gaps and disease resurgence remain pressing challenges; measles surges in Vietnam and neighbouring nations have spurred emergency vaccine stockpiles and fast-track tendering. Regional bodies like APEC have adopted a decade-long plan aiming to vaccinate 23 million children who missed doses during COVID-19 disruptions, signalling persistent momentum for the pediatric vaccines market in fast-growing economies.

Europe retains a sizable share, underpinned by the European Commission's centralised marketing authorisation process that speeds harmonised access. Recent approval of Pfizer's PREVENAR 20 offers the broadest pneumococcal serotype coverage yet for infants and adolescents, cementing conjugate uptake across member states. However, budget ceilings in several economies sharpen the focus on value-based procurement, and reimbursement deliberations are increasingly linked to real-world effectiveness data.

The Middle East & Africa and South America present mixed pictures. Several African Union members leverage Gavi co-financing to build indigenous manufacturing under the African Vaccine Manufacturing Accelerator, while Peru and neighbouring markets work to restore routine childhood coverage lost during the pandemic. Overall, heterogeneous funding and infrastructure will keep growth below the global average, yet targeted donor initiatives, technology transfer agreements and cold-chain modernisation point to gradual improvements in the pediatric vaccines market across these regions.