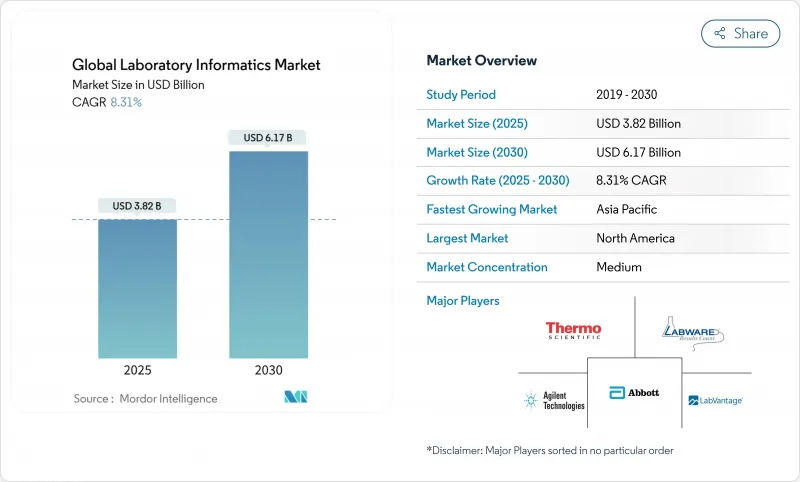

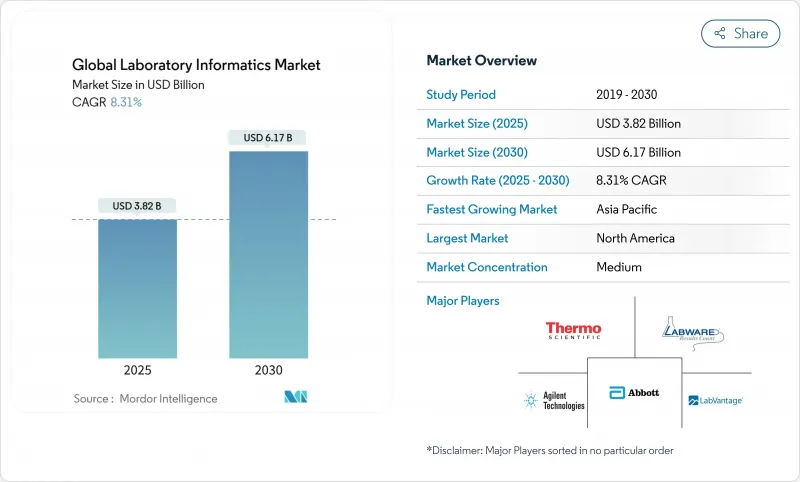

실험실 정보학 시장의 2024년 시장 규모는 38억 2,000만 달러로 평가되었고, 2030년에는 61억 7,000만 달러에 이르고, 2025-2030년의 CAGR은 8.31%를 나타낼 전망입니다.

성장을 뒷받침하는 것은 클라우드 배포로 전환하는 실험실, 의약품 아웃소싱 속도 증가, 강력한 멀티오믹스 데이터 관리가 필요한 정밀의료 바이오뱅크의 확장입니다. 클라우드 배포는 이미 최대의 수익 풀을 지배하고 있으며, 제약 연구 개발에서는 원격 액세스 워크플로가 표준이 되어 리드를 넓히고 있습니다. 규제 당국에 의한 데이터 통합의 의무화로 인해 레거시 랩 정보 관리 시스템(LIMS)에서 설계 컴플라이언스를 통합한 최신 플랫폼으로의 교체가 가속화되고 있습니다. 동시에 인공지능 모듈은 인포매틱스 스위트에 통합되어 있으며, 특히 종양학이나 희소질환 연구에 있어서 분석주기를 단축하고 예측적 통찰을 표면화하게 되었습니다.

레거시 LIMS는 오늘날의 감사 추적, CoC, 전자 서명 요구 사항을 충족할 수 없기 때문에 미국과 캐나다 제약 회사 및 임상 실험실에서 리플레이스 프로젝트의 물결이 밀려오고 있습니다. 미국 식품의약국은 애보트의 STARLIMS를 검사시설 전체에 채택하여 컴플라이언스 워크플로우를 자동화하는 플랫폼에 대한 규제 당국의 기호를 나타내고 있습니다. 전염병 보고서가 수동 로그에서 주 감시 네트워크와 통합된 의무화된 전자 검사 보고서로 이동함에 따라 병원도 이를 추종하고 있습니다. 사실상, 업그레이드 주기는 세분화된 감사 추적, 검증된 장비 인터페이스, 21 CFR Part 11 지원을 갖춘 시스템에 대한 공급업체 선택을 강화하고, 검사 정보학 시장을 더 높은 연간 유지보수 수익과 더 긴 다년간 지원 계약으로 밀어 올리고 있습니다.

중국, 인도, 동남아시아의 연구개발 수탁기관은 초기 단계의 의약품 개발에 보다 큰 점유율을 획득하고 있으며, 이 지역의 CRO 수익은 2025년에 460억 달러로 상승합니다. 스폰서는 외부 위탁된 분석을 실시간으로 시각화할 것을 요구하고 있으며, CRO는 고객 포털에 데이터를 스트리밍하는 클라우드 기반 LIMS를 도입해야 합니다. LabVantage는 이 요구에 대응하기 위해 2020년부터 2023년 사이에 아시아와 남미에 있어서의 프로페셔널 서비스의 거점을 80% 확대했습니다. 클라우드 호스팅은 On-Premise 데이터센터의 자본 지출을 피할 수 있기 때문에 소규모 생명 공학 기업은 CRO 파트너와의 제휴를 신속하게 수행할 수 있어 실험실 정보학 시장의 지속적인 2자리 성장에 기여합니다.

라틴아메리카의 많은 실험실은 수십 년에 걸쳐 얻은 이기종 혼합 벤치 탑 장비에 의존하며, 각각 자체 파일 형식과 오래된 펌웨어를 실행합니다. Science 잡지의 2024년 시약 협력 네트워크의 보도에서 강조된 바와 같이, 현지 시약 공급업체의 부족과 소모품 수입 비용의 상승은 과제를 더욱 복잡하게 만듭니다. 실험실이 시약을 현지에서 생산하도록 지도하는 노력은 소모품 비용을 줄이는 것, 핵심 통합 문제를 해결하는 것이 아닙니다. 결과적으로, LIMS의 새로운 배치는 커스텀 드라이버 개발과 인터페이스 검증을 포함해야 하며, 프로젝트 예산은 증가하고, 일정은 장기화되고, 이 지역의 실험실 정보학 시장의 확대 속도를 약화시킵니다.

북미는 2024년 매출의 43.0%를 차지하며 엄격한 규제감독과 높은 연구개발 집약도를 반영하고 있습니다. 미국 질병관리예방센터는 COVID-19 긴급사태 이전에 전자검사보고 인프라를 통합하여 공중위생연구소에 신속한 데이터 교환 선두를 두었습니다. 이 지역에 본사를 두고 있는 제약 대기업은 AI를 활용한 데이터 분석을 위한 디지털 변혁 예산을 일상적으로 계상하여 정보과학 플랫폼의 안정적인 갱신 사이클을 확보하고 있습니다. 유행성 대책과 항균제 내성 감시를 위한 연방 보조금이 수요를 더욱 자극하고, 연구소 정보 시장에서 북미의 리드는 유지되고 있습니다.

아시아태평양의 CAGR은 9.0%를 나타내고 세계에서 가장 빠릅니다. 중국과 인도에서는 국내 CRO가 세계 스폰서에 서비스를 제공하기 위해 용량을 확대하고 있기 때문에 설치 수가 압도적으로 많습니다. 각국 정부는 실험실 자동화와 직원 교육에 보조금을 제공하는 국가 품질 인프라 프로그램을 개발하고 도입 일정을 단축하고 있습니다. LabVantage의 현지 도입 팀 강화 결정은 수출 주도의 서비스 모델에서 지역 내 지원 체제로 전환하는 신호이며, 고객에게 언어와 시간대의 마찰을 줄이는 움직임입니다. 많은 새로운 실험실에서는 굳어진 레거시 시스템이 존재하지 않기 때문에 클라우드 도입으로의 직접적인 도약이 가능하며, 아시아태평양 전역의 실험실 정보학 시장의 성장세를 확대하고 있습니다.

유럽에서는 고급 정밀의료에 대한 노력과 엄격한 데이터 보호 시스템이 양립하고 있습니다. 암 이미지 바이오뱅크와 멀티오믹스 리포지토리는 개인 식별 정보를 보호하면서 이미지, 유전체 및 임상 데이터를 원활하게 통합하는 플랫폼을 필요로 합니다. GDPR(EU 개인정보보호규정) 준수는 암호화, 토큰화 및 국경을 넘는 데이터 전송 관리에 대한 공급업체 투자를 촉진합니다. 규제로 인한 오버헤드로 단기 예산은 깎아지며, 국가 의료 서비스 및 시장 세분화 자금원은 디지털 인프라 업그레이드에 보조금을 충당하고 있으며 실험실 정보학 시장 규모의 유럽 부문에 서비스를 제공하는 공급업체의 중기 파이프라인을 보장하고 있습니다.

The laboratory informatics market is valued at USD 3.82 billion in 2024 and is projected to reach USD 6.17 billion by 2030, advancing at an 8.31% CAGR over 2025-2030.

Growth is underpinned by laboratories shifting to cloud deployment, the rising pace of outsourced drug discovery, and the expansion of precision-medicine biobanks that demand robust multi-omics data management. Cloud delivery already controls the largest revenue pool and is widening its lead because remote-access workflows have become standard in pharmaceutical R&D. Data-integrity mandates from regulators accelerate the replacement of legacy Laboratory Information Management Systems (LIMS) with modern platforms that embed compliance by design. Simultaneously, artificial-intelligence modules are being folded into informatics suites to shorten analysis cycles and surface predictive insights, especially in oncology and rare-disease research.

Legacy LIMS cannot satisfy today's audit-trail, chain-of-custody, and electronic-signature requirements, propelling a wave of rip-and-replace projects across pharmaceutical and clinical laboratories in the United States and Canada. The U.S. Food and Drug Administration adopted Abbott's STARLIMS across its testing sites, illustrating the regulatory preference for platforms that automate compliance workflows. Hospitals are following suit as infectious-disease reporting moves from manual logs to mandated electronic laboratory reporting that integrates with state surveillance networks. In practical terms, the upgrade cycle tightens vendor selection to systems with granular audit trails, validated instrument interfaces, and support for 21 CFR Part 11, pushing the laboratory informatics market toward higher annual maintenance revenue and longer multi-year support contracts.

Contract Research Organizations in China, India, and South-East Asia are winning a larger slice of early-stage drug development, lifting regional CRO revenue toward USD 46 billion in 2025. Sponsors demand real-time visibility into outsourced assays, forcing CROs to install cloud-architected LIMS that stream data to client portals. LabVantage expanded its professional-services footprint in Asia and South America by 80% between 2020-2023 to meet this need. Because cloud hosting sidesteps the capital outlay of on-premise data centers, smaller biotech firms can onboard CRO partners faster, contributing to sustained double-digit segment growth within the laboratory informatics market.

Many Latin American laboratories rely on heterogeneous benchtop instruments acquired over decades, each running proprietary file formats and outdated firmware. The scarcity of local reagent suppliers and the elevated cost of importing consumables compound the challenge, as highlighted in Science's 2024 coverage of the Reagent Collaboration Network. Although initiatives that teach labs to manufacture reagents locally reduce consumable costs, they do not solve the core integration problem. Consequently, new LIMS rollouts must include custom driver development and interface validation, raising project budgets and elongating timelines, which tempers the expansion pace of the laboratory informatics market in the region.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

North America contributed 43.0% of 2024 revenue, reflecting the confluence of stringent regulatory oversight and high R&D intensity. The U.S. Centers for Disease Control and Prevention embedded electronic-laboratory-reporting infrastructure long before the COVID-19 emergency, giving public-health labs a head start in rapid data exchange. Pharmaceutical majors based in the region routinely earmark digital-transformation budgets for AI-enabled data analytics, ensuring steady refresh cycles for informatics platforms. Federal grants for pandemic preparedness and antimicrobial-resistance surveillance further fuel demand, maintaining North America's lead within the laboratory informatics market.

Asia Pacific is advancing at a 9.0% CAGR, the fastest worldwide. China and India dominate installation counts as domestic CROs scale capacity to service global sponsors. Governments are deploying national quality-infrastructure programs that subsidize laboratory automation and staff training, compressing adoption timelines. LabVantage's decision to bolster its local implementation teams signals a pivot from export-led service models to in-region support structures, a move that lowers language and time-zone friction for clients. The absence of entrenched legacy systems in many new labs allows direct leapfrogging to cloud deployment, magnifying the growth momentum of the laboratory informatics market across Asia Pacific.

Europe balances advanced precision-medicine initiatives with strict data-protection regimes. Cancer-image biobanks and multi-omics repositories mandate platforms that seamlessly integrate imaging, genomic, and clinical data while safeguarding personal identifiers. Compliance with GDPR drives vendor investment in encryption, tokenization, and cross-border data-transfer controls. Although the regulatory overhead trims short-term budgets, national health services and Horizon funding streams are earmarking grants for digital-infrastructure upgrades, ensuring a solid mid-term pipeline for vendors servicing the European segment of the laboratory informatics market size.