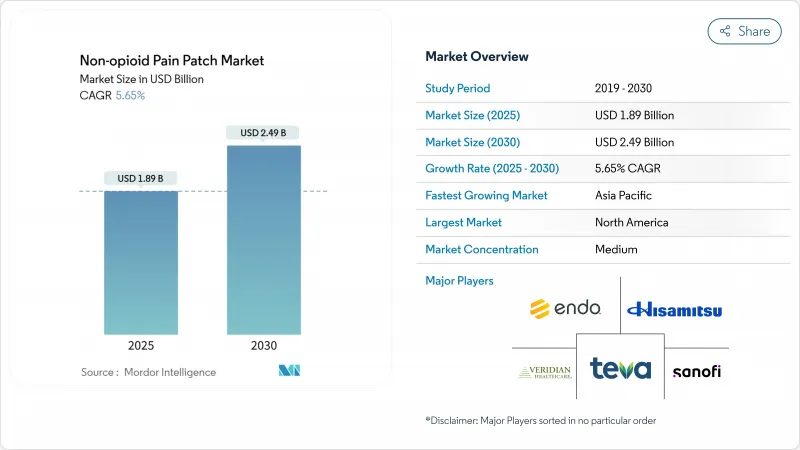

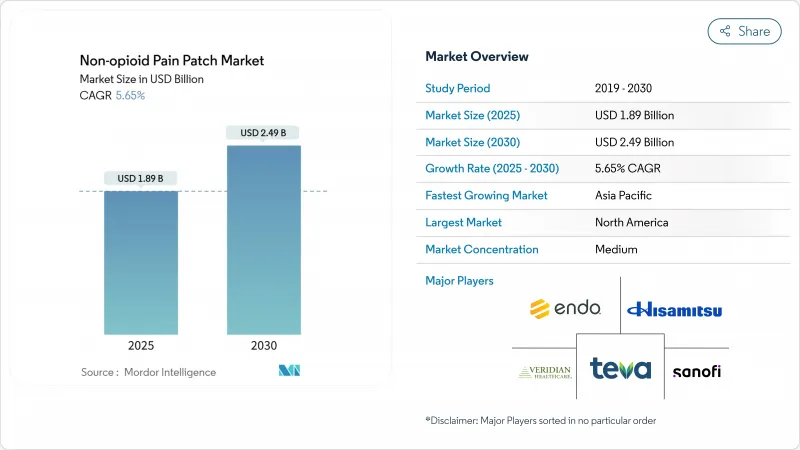

비오피오이드 진통 패치 시장 규모는 2025년에 18억 9,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 5.65%로 성장할 전망이며, 2030년에는 24억 9,000만 달러에 달할 것으로 예측됩니다.

성장의 배경은 세계적인 오피오이드 처방에서 벗어나고, 경피 전달에서 꾸준한 기술 혁신, 국소 진통제에 대한 상환 확대가 있습니다. 새로운 마이크로니들 강화 시스템은 약물전달의 효율성을 높이는 한편, 대형 매트릭스 포맷은 기존 브랜드의 비용 우위를 유지하고 있습니다. 온라인 약국은 Paysent Journey를 재구성하고, 제조업체가 환자와 직접적인 관계를 구축하며, 가격 투명성을 높입니다. 통합은 계속되고 있습니다. : 글루넨탈은 아포텍스와 Qutenza의 라이선싱 계약을 체결하고 캐나다 전개의 폭을 넓히는 한편, 에노콘메디컬 등 중소기업은 안전성을 중시하는 사용자에게 어필하는 천연 성분 패치로 87%의 임상효과를 기록했습니다.

15억 명 이상이 만성적인 통증을 갖고 생활하고 있으며, 고령화 사회가 신경장애성 질환을 최전선으로 밀어 올리고 있습니다. 당뇨병만으로도 2045년까지 7억 8,300만 명의 성인이 이환될 것으로 예측되고 있으며, 당뇨병성 말초신경장애 환자 수가 증가하고 있습니다. 미국에서는 통제되지 않은 통증으로 인한 생산성 손실이 매년 3,000억 달러를 초과합니다. 따라서 지불자와 임상의는 환자의 활동을 유지하고 전신 약물에 대한 의존도를 줄이는 국소적이고 위험이 낮은 치료를 선호합니다.

4세대 패치는 현재 강인한 피부 외층을 우회하고 진통제를 제어된 방식으로 방출하는 마이크로 바늘을 내장하고 있습니다. 다공성 코팅이 적용된 폴리머 기반 마이크로니들 어레이는 금속보다 3배 더 높은 하중을 제공하여 진통 지속 시간을 연장합니다. 이러한 장점은 친수성 약물의 이전 한계를 해결하고 적용 빈도를 줄여 환자의 어드레싱을 향상시킵니다.

많은 신흥 국가에서 브랜드 패치 가격은 제네릭 이부프로펜 정제의 5배에서 10배나 됩니다. 보험이 적용되는 범위가 제한되어 있기 때문에 환자는 가장 저렴하고 즉각적인 진통제를 선택할 것입니다. 인도의 의약품 제조업체는 2030년까지 300개가 넘는 제품의 특허가 끊어지기 때문에 제네릭 패치를 출시함으로써 이 갭을 메우고 싶지만, 눈앞의 가격적인 장애물은 여전히 높습니다.

2024년 비오피오이드 진통 패치 시장 규모에서는 리도카인 제형이 35.23%로 가장 큰 점유율을 차지했으며, 수십년에 걸친 임상 사용과 광범위한 제3자 지불에 지원되고 있습니다. 강력한 안전성과 최소한의 전신 흡수로 리도카인은 대상 포진 후 신경통에 가장 많이 걸린 노인층에게 인기가 있습니다. 글루넨탈사와 사이렉스사는 박리하지 않고 운동이나 샤워를 가능하게 하는 보다 얇고 고밀착성의 시스템을 제공함으로써 수용의 폭을 넓혔습니다.

캡사이신 패치는 고농도 제제가 당뇨병성 신경병증나 화학요법에 의한 통증을 몇 개월에 걸쳐 완화하기 때문에 CAGR이 6.97%로 패치 유형 중에서 가장 급속히 확대되었습니다. 캅사이신과 표준 치료를 비교한 2025년 연구에서는 노인 환자가 통계적으로 유의한 통증 점수 감소를 달성했습니다. 디클로페낙과 케토프로펜은 근골격계의 상해 관리에 틈새 역할을 담당하고 있으며, 에노콘의 천연 성분 패치는 화학 약품을 사용하지 않는 치료를 요구하는 사람들을 위해 작지만 눈에 보이는 프론티어를 창출하고 있습니다.

매트릭스 구조는 2024년 비오피오이드 진통 패치 시장 점유율의 48.41%를 차지했습니다. 제조업체가 이 형식을 선호하는 이유는 합리적인 제조 비용으로 광범위한 API를 지원할 수 있기 때문입니다. 병원은 12-24시간에 걸쳐 안정된 혈장 농도가 얻어지는 것을 평가했습니다.

마이크로니들 강화 패치는 가바펜틴과 같은 친수성 분자의 투과를 개선하는 마이크로 채널을 여는 능력을 활용하여 CAGR 7.12%의 고성장을 이룹니다. 2024년 카본마스터 마이크로니들의 프로토타입은 초기 금속 유닛에 비해 전달 효율을 3배로 높였습니다. 저장 시스템은 장시간의 만성 치료에도 대응하고, 약물 접착 시트는 초박형 디자인으로 미용 매력을 보장합니다. 스마트 pH 반응성 마이크로니들 어레이는 국소 염증 수준에 맞게 복용량을 조정하는 다음 파도를 상징합니다.

북미는 2024년 매출의 39.45%를 차지했지만, 이는 오피오이드 중독의 위험에 대한 인식의 확산과 국소 진통제에 대한 지불자의 적용 범위를 반영하고 있습니다. 2025년 NOPAIN법은 비오피오이드 수술 후 옵션에 자금을 제공하여 캡사이신 및 리도카인 시스템의 병원에서의 사용을 촉진합니다. 미국 FDA에 의한 신규 비오피오이드 치료법의 승인도 FDA의 임상의에 대한 신뢰감을 높이고 있습니다.

아시아태평양의 2030년까지 CAGR은 7.87%로 가장 빠를 전망입니다. 일본의 초고령화 사회에서는 대상포진 후 신경통의 이환율이 높고, 상환위원회는 장기적인 완화를 목적으로 한 캡사이신 8% 패치로의 상환을 인정하고 있습니다. 중국과 인도의 성장은 가격 협상에 달려 있으며, 국내 계약업체들은 저가의 제네릭 의약품을 준비하고 있기 때문에 세계 특허가 만료되면 액세스가 확대될 수 있습니다.

유럽은 강력한 만성 통증 관리 프레임 워크를 통해 견고한 점유율을 유지하고 있지만, EMA가 피부 감작성 시험을 추가해야 하기 때문에 성장이 둔화되고 있습니다. 독일, 영국, 프랑스는 전자 처방전을 장려하고 디지털 약국의 도입을 촉진하고 있습니다. 라틴아메리카와 중동은 1급 도시에서 민간 보험 회사가 브랜드 패치를 상환함으로써 완만한 성장을 보이고 있습니다. 습도가 높은 ASEAN의 기후는 습기가 많으면 보존 기간이 짧아지기 때문에 호일 라미네이트된 백이나 건조제 라이너가 필요하고 공급망의 과제가 되고 있습니다.

The Non-opioid Pain Patch Market size is estimated at USD 1.89 billion in 2025, and is expected to reach USD 2.49 billion by 2030, at a CAGR of 5.65% during the forecast period (2025-2030).

Growth is rooted in the global shift away from opioid prescribing, steady innovation in transdermal delivery, and widening reimbursement for topical analgesics. New microneedle-enhanced systems are raising drug-delivery efficiency while large matrix formats preserve cost advantages for established brands. Online pharmacies are reshaping purchase journeys, letting manufacturers build direct bonds with patients and sharpen pricing transparency. Consolidation continues: Grunenthal's Qutenza licensing deal with Apotex broadened reach in Canada, while smaller firms such as Enokon Medical posted 87% clinical efficacy with natural-ingredient patches that appeal to safety-conscious users.

More than 1.5 billion people live with chronic pain, and aging societies push neuropathic conditions to the forefront. Diabetes alone is set to affect 783 million adults by 2045, swelling the pool of patients with diabetic peripheral neuropathy. Productivity losses tied to unmanaged pain top USD 300 billion each year in the United States. Payers and clinicians therefore favor localized, low-risk treatments that keep patients active and reduce reliance on systemic drugs.

Fourth-generation patches now integrate microneedles that bypass the tough outer skin layer and release analgesics in a controlled manner. Polymer-based microneedle arrays with porous coatings deliver three-times higher loads than metal designs and extend pain-relief duration. Such gains address prior limits for hydrophilic drugs and cut application frequency, raising patient adherence.

In many emerging countries a branded patch costs five-to-ten times more than generic ibuprofen tablets. Limited insurance coverage prompts patients to opt for the cheapest immediate relief. India's drug-makers hope to bridge this gap by launching generic patches as patents expire on over 300 products by 2030, yet near-term affordability hurdles stay in place.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Lidocaine products held the largest slice of the non-opioid pain patch market size at 35.23% in 2024, supported by decades of clinical use and broad third-party payment. Strong safety and minimal systemic absorption make lidocaine popular in elderly populations, which are most affected by post-herpetic neuralgia. Grunenthal and Scilex broadened acceptance by delivering thinner, high-adhesion systems that permit exercise and showering without detachment.

Capsaicin patches expand at a 6.97% CAGR, the fastest among patch types, because high-concentration formulations produce multi-month relief from diabetic neuropathy and chemotherapy-induced pain. Older patients achieved statistically significant pain score reductions in a 2025 study that compared capsaicin to standard care. Diclofenac and ketoprofen hold niche roles in musculoskeletal injury management, while natural-ingredient patches from Enokon create a small but visible frontier for chemical-free therapy seekers.

Matrix construction accounted for 48.41% of the non-opioid pain patch market share in 2024. Manufacturers prefer the format because it supports a wide range of APIs at reasonable production cost. Hospitals value the steady plasma levels delivered over 12-24 hours.

Microneedle-enhanced patches post the highest growth at 7.12% CAGR, capitalizing on their ability to open microchannels that improve permeation of hydrophilic molecules like gabapentin. A 2024 carbon-master microneedle prototype raised delivery efficiency threefold compared with earlier metal units. Reservoir systems stay relevant in long-wear chronic treatment, and drug-in-adhesive sheets secure cosmetic appeal with ultra-thin designs. Smart pH-responsive microneedle arrays represent the next wave, adjusting dose to local inflammation levels.

The Non-Opioid Pain Patch Market Report is Segmented by Patch Type (Lidocaine Patches, Diclofenac Patches, Capsaicin Patches, and More), Technology (Matrix Patches, Reservoir Patches and More), Indication (Pain Type) (Neuropathic Pain, and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 39.45% of 2024 revenue, reflecting widespread awareness of opioid addiction risks and generous payer coverage for topical analgesics. The 2025 NOPAIN Act funds non-opioid postoperative options, driving hospital uptake of capsaicin and lidocaine systems. U.S. FDA approvals of novel non-opioid treatments also boost clinician confidence FDA.

Asia Pacific posts the fastest regional CAGR at 7.87% through 2030. Japan's super-aged society faces high rates of post-herpetic neuralgia, and reimbursement committees increasingly reimburse capsaicin 8% patches for long-term relief. In China and India growth hinges on price negotiation; domestic contract manufacturers prepare low-price generics that could widen access once global patents expire.

Europe holds a solid share with strong chronic-pain management frameworks but slower growth because the EMA demands extra skin-sensitization tests. Germany, the United Kingdom, and France incentivize e-prescriptions, easing digital pharmacy adoption. Latin America and the Middle East show moderate growth when private insurers reimburse branded patches in tier-one cities. Humid ASEAN climates challenge supply chains because high moisture shortens shelf life, prompting foil-laminated sachets and desiccant liners.