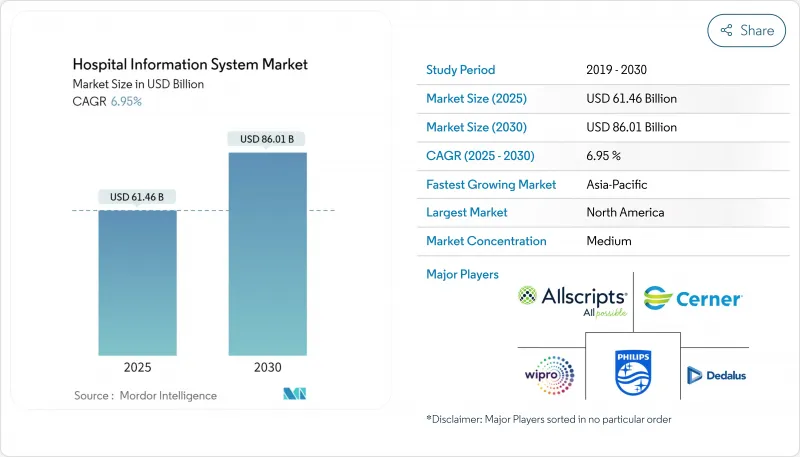

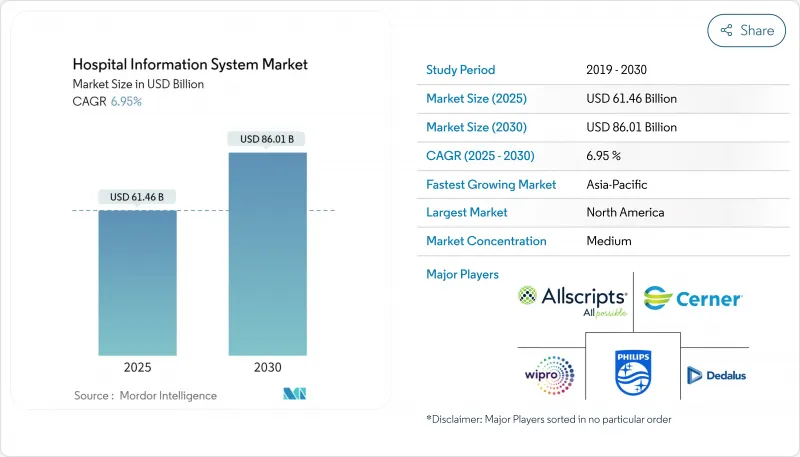

병원 정보 시스템 시장의 2025년 시장 규모는 614억 6,000만 달러로 추정되고, 2030년에는 860억 1,000만 달러에 이를 것으로 예측되며, CAGR 6.95%로 성장할 전망입니다.

통합 디지털 플랫폼은 더 이상 옵션이 아니며, 기본이 되는 인프라라는 컨센서스 증가가 조달 과제를 재구성하고 있습니다. 구매자는 현재 평생 총 소유 비용, 측정 가능한 임상 결과, 모듈형 클라우드 업그레이드에 대한 공급업체 지원에 중점을 둡니다. 이러한 우선사항에 따라 의사결정은 사일로화한 부문에서 재무와 임상 감독을 융합시킨 기업 차원의 디지털 운영위원회로 밀어 올리고 있습니다. 공급업체는 애널리틱스, 사이버 보안 및 관리 서비스를 번들로 제공하며, 1회 소프트웨어 벤더가 아니라 여러 해에 걸친 '디지털 현대화' 프로그램의 파트너로 자리매김하기 때문에 경쟁이 치열해지고 있습니다.

병원은 현재 머신러닝 모델을 통합하여 패혈증 플래그, 항생제 최적화, 퇴원 준비 예측을 거의 실시간으로 실시했습니다. Epic 로드맵에는 100개 이상의 AI 기능이 게재되어 있으며 분석이 핵심 플랫폼에 깊게 짜여져 있는 방법을 보여줍니다. Duke Health는 GE Healthcare Command Center 소프트웨어를 도입한 후 침대 할당 간격을 줄여 눈에 보이는 처리량을 향상시켰습니다. 이사회는 점점 더 모델의 설명 가능성을 요구하고 있으며, 거버넌스 팀은 데이터 사이언스자와 협력하여 지역 관리 경로를 반영하는 알고리즘을 교정하고 있습니다. 이러한 실천이 주류가 됨에 따라 AI 기능은 파일럿에서 기본 요건으로 이동하여 병원 정보 시스템 시장에서의 대응 가능한 지출을 확대하고 있습니다.

걸프 협력 회의 회원국과 동남아시아 국가에서는 건설과 병행하여 디지털 플랫폼의 예산이 계상되어 새로운 3차 의료 센터가 레거시 아키텍처를 뛰어넘을 수 있게 되어 있습니다. 아랍에미리트(UAE)의 프로젝트는 EHR, 이미지 아카이브, 커맨드 센터 분석에 엄청난 자금을 할당받았으며, 물리적 능력과 보조를 바탕으로 디지털 성숙도가 높아지고 있습니다. 다국어 인터페이스를 제공하는 공급업체는 선행자 이익을 얻습니다. 이러한 역학은 수익 풀을 급성장하는 인프라가 풍부한 지역을 향해 아시아태평양이 가장 급성장하고 있는 시장으로서의 역할을 강화하고 있습니다.

종합적인 EHR 전개에는 하드웨어, 데이터 마이그레이션, 워크플로 재설계, 수년간의 유지보수 등을 포함하면 수억 달러의 비용이 소요됩니다. 노스웰 헬스 이사회는 중복 검사 감소와 집단 헬스케어 개선을 통해 투자 회수 가능성을 제시한 후 12억 달러의 이니셔티브를 승인했습니다. 소규모 병원에서는 이러한 자본 지출을 흡수하는 균형 시트가 없기 때문에 구독 가격과 공유 서비스 모델로의 전환이 진행되고 있습니다. 이를 통해 관리 서비스 컨세션부터 관민 파트너십에 이르기까지 혁신적인 자금 조달 메커니즘이 지지를 받고 있습니다. 공급업체는 고객이 전체 라이프사이클에 걸쳐 가치를 판단한다는 사실을 인식하고 계약 내에서 최적화 서비스를 번들하여 대응합니다. 이러한 경제학의 진화로 병원 정보 시스템 업계는 단순한 소프트웨어 설치가 아니라 측정 가능한 개선에 보답하는 성과 기반 가격 체계로 전환하고 있습니다.

병원 정보 시스템 시장은 서비스가 최대 점유율을 차지하고 2024년 매출의 46%를 차지한 반면, 소프트웨어 컴포넌트는 2025-2030년 8%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되고 있습니다. 복잡한 데이터 변환 프로젝트 및 다중 사이트 롤아웃은 특히 여러 레거시 플랫폼을 통합하는 의료 시스템 간에 컨설팅 서비스와 관리 서비스에 대한 수요를 계속 추진하고 있습니다. 한편, AI 대응 모듈의 인기가 높아지고 있으며, 특히 의사 결정 지원과 앰비언트 문서를 위한 소프트웨어 라이선스의 성장이 가속화되고 있습니다. Epic이 Mayo Clinic 및 Abridge와 제휴하여 간호 워크플로우를 위한 제네레이티브 AI를 시험적으로 도입한 것은 공급업체가 서비스 랩 어라운드를 심화시키고 Time-to-Value를 가속화하고 있음을 상징합니다. 재현성이 뛰어난 클라우드 네이티브 템플릿이 맞춤형 코딩을 대체함으로써 구현 타임라인이 단축되었음이 눈에 띄는 결과로 나타납니다. 서비스 계약을 측정 가능한 임상적 및 재무적 목표에 맞추는 공급자는 보다 빨리 이익을 실현하는 경향이 있으며, 병원 정보 시스템 업계에서 전문 서비스의 전략적 역할이 강화되고 있습니다.

2024년 병원 정보 시스템 시장 규모는 온프레미스형이 55%의 점유율을 차지해 최대였으며, 클라우드 기반 모델은 2030년까지 연평균 복합 성장률(CAGR) 9%로 확대될 것으로 예측되고 있습니다. CTO(최고기술 책임자)는 클라우드의 주요 동기로 확장성과 비즈니스 연속성을 꼽고 있지만 대기 시간과 주권상의 이유로 핵심 EHR 데이터베이스를 로컬 서버에 두고 있는 기업도 여전히 많습니다. 첨단 기업은 하이브리드 아키텍처를 채택하고 애널리틱스 샌드박스를 클라우드에서 호스팅하는 반면 거래량이 많은 모듈은 전용 데이터센터에서 관리하고 있습니다. 퍼블릭 클라우드를 신속하게 채택한 Epic의 성공 스토리는 운영의 탄력성을 입증하지만, 비용 효율성은 여전히 인스턴스의 엄격한 라이트 사이징에 따라 달라집니다. 현실적인 의미는 프로젝트 로드맵에서 네트워크 대역폭 계획과 ID 액세스 관리가 애플리케이션 로직만큼 중요하다는 것입니다. 결과적으로 전개 형태를 결정하려면 탄력성, 비용, 데이터 상주 및 혁신 목표의 균형을 고려한 학제적인 검토가 필요합니다.

북미는 2024년에 42%의 병원 정보 시스템 시장 점유율을 기록했는데, 이는 EHR 도입의 의무화와 예산 규모의 크기에 뒷받침된 것입니다. 체인지 헬스케어 사이버 사건 이후 미국 병원은 공급업체의 위험 평가를 강화하고 실시간 위협 인텔리전스 조항을 계약에 통합했습니다. BMC Digital Health의 리뷰에 따르면 미국 시스템의 84%가 AI 예측 모델을 도입했지만 거버넌스 팀은 여전히 자원 부족입니다. 따라서 공급자는 모델 검증을 위한 관리형 서비스를 추구하고 서비스가 풍부한 병원 정보 시스템 시장을 육성하고 있습니다.

아시아태평양은 의료비 증가와 클라우드 퍼스트 정책에 힘입어 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 9.5%가 될 전망입니다. 인도의 연방 의료 예산은 2024년 2자리 증가했으며, 태국에서는 AI 트리어지 엔진과 연동된 원격 의료용 키오스크를 시험적으로 도입하고 있습니다. 싱가포르의 스마트 워드 이니셔티브는 IoT 지원 바이탈 사인 추적에 중점을 두고 상호 운용성에 대한 기대를 높이고 있습니다. 언어 현지화를 제공하는 공급업체는 특히 개인정보보호법의 보급에 따라 두각을 나타냅니다. 오래된 인프라를 뛰어넘어 병원은 지역 광대역 업그레이드에 맞는 클라우드 EHR 플랫폼을 채택하여 병원 정보 시스템 시장에서 아시아태평양의 역할을 강화하고 있습니다.

유럽, 중동 및 아프리카는 디지털 성숙도 스펙트럼을 보여줍니다. 독일의 Krankenhauszukunftsgesetz(KHZG) 기금은 병원에 대한 디지털 투약 관리 인증을 의무화하고 있으며 공급업체는 생태계 서비스 확대에 박차를 가하고 있습니다. GCC 국가에서는 공립병원의 4분의 3 이상이 이미 EHR을 도입하고 있으며, 사우디아라비아의 '비전 2030'에 의한 원격 진료의 목표가 이를 뒷받침하고 있습니다. 데이터 교환 표준에 관한 규제의 수렴은 다자간의 구현을 용이하게 하고, 유럽에서 걸프 메가 프로젝트로의 인재 유입은 스킬 믹스의 진화를 가속시킵니다. 전반적으로 이 지역은 이질적이지만 병원 정보 시스템 시장에 전략적으로 중요한 무대가 되고 있습니다.

The hospital information system market is valued at USD 61.46 billion in 2025 and is forecast to reach USD 86.01 billion by 2030, registering a 6.95% CAGR.

A growing consensus that integrated digital platforms are no longer optional but foundational infrastructure is reshaping procurement agendas. Buyers now focus on lifetime total cost of ownership, measurable clinical outcomes and vendor support for modular cloud upgrades. These priorities have pushed decision-making from siloed departments to enterprise-level digital steering committees that blend financial and clinical oversight. Competition is intensifying as suppliers bundle analytics, cybersecurity and managed services, positioning themselves as partners in multi-year "digital modernisation" programmes rather than one-time software vendors.

Hospitals now embed machine-learning models to flag sepsis, optimise antibiotics and predict discharge readiness in near real time. Epic lists more than 100 AI features on its roadmap, signalling how deeply analytics is being woven into core platforms . Duke Health shortened bed-assignment intervals after implementing GE HealthCare's Command Center Software, demonstrating tangible throughput gains . Boards increasingly demand model-explainability statements, and governance teams work with data scientists to calibrate algorithms that reflect local care pathways. As these practices become mainstream, AI functionality is shifting from pilots to default requirements, enlarging addressable spend in the hospital information system market.

Gulf Cooperation Council states and multiple Southeast Asian countries now budget digital platforms alongside construction, allowing new tertiary centres to leapfrog legacy architectures. Projects in the United Arab Emirates allocate substantial funds to EHR, imaging archives and command-centre analytics, ensuring that digital maturity grows in lockstep with physical capacity . Vendors providing multilingual interfaces gain first-mover advantage. These dynamics redirect revenue pools toward fast-growing, infrastructure-rich regions, reinforcing Asia-Pacific's role as the quickest-expanding hospital information system market.

Comprehensive EHR deployments can cost hundreds of millions of USD when hardware, data migration, workflow redesign and multi-year maintenance are included. Northwell Health's board approved a USD 1.2 billion initiative after leadership demonstrated a credible payback horizon through reduced duplicative testing and improved population-health management. Smaller hospitals lack the balance sheets to absorb such capital outlays, pushing them toward subscription pricing or shared-services models. Innovative financing mechanisms-ranging from managed-service concessions to public-private partnerships-are therefore gaining traction. Vendors respond by bundling optimisation services within contracts, recognising that clients judge value over the full life cycle. This evolving economics is nudging the Hospital Information System industry toward outcome-based pricing structures that reward measurable improvements rather than mere software installation.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Services accounted for the largest Hospital Information System market share, representing 46% of 2024 revenue, while the software component is forecast to record an 8% CAGR between 2025 and 2030. Complex data-conversion projects and multi-site rollouts continue to drive demand for consultative and managed services, particularly among health systems consolidating multiple legacy platforms. Meanwhile, the rising popularity of AI-enabled modules is fuelling software licence growth, especially for decision-support and ambient documentation. Epic's partnership with Mayo Clinic and Abridge to pilot generative AI for nursing workflows typifies how vendors are deepening service wrap-arounds to accelerate time-to-value. An observable consequence is that implementation timelines are shortening as repeatable, cloud-native templates replace bespoke coding. Providers that align service engagements to measurable clinical and financial objectives tend to realise faster benefit realisation, reinforcing the strategic role of professional services in the Hospital Information System industry.

On-premise deployments retained the largest hospital information system market size in 2024, with an estimated 55% share, yet cloud-based models are projected to expand at close to a 9 % CAGR through 2030. Chief technology officers cite scalability and business-continuity features as primary cloud motivators, but many still keep core EHR databases on local servers for latency and sovereignty reasons. Progressive organisations adopt hybrid architectures, hosting analytics sandboxes in the cloud while maintaining high-transaction modules in dedicated data centres. Epic's success stories from early public-cloud adopters demonstrate operational elasticity, though cost efficiencies remain contingent on rigorous instance-rightsizing. A practical implication is that network-bandwidth planning and identity-access management become as critical as application logic in project roadmaps. Consequently, mode-of-delivery decisions now involve multidisciplinary reviews that balance resilience, cost, data-residency and innovation goals.

The Hospital Information System Market Report Segments the Industry Into Mode of Delivery (Cloud-Based, On-Premise, and More), Type (Clinical Information Systems, Administrative Information Systems, and More), by Component (Software, Services, and Hardware), by End User (Multi-Specialty Hospitals, Specialty Hospitals, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America recorded a 42% hospital information system market share in 2024, buoyed by mandated EHR adoption and sizeable budgets. After the Change Healthcare cyber incident, US hospitals tightened vendor risk assessments and embedded real-time threat-intelligence clauses in contracts. A BMC Digital Health review noted that 84% of US systems deploy AI predictive models, though governance teams remain under-resourced. Providers therefore seek managed services for model validation, fostering a service-rich hospital information system market.

Asia-Pacific is poised for the fastest 9.5% CAGR to 2030, fuelled by rising health expenditure and cloud-first policies. India's federal health budget increased double digits in 2024, and Thailand's ministry pilots tele-medicine kiosks interfacing with AI triage engines. Singapore's smart-ward initiatives emphasise IoT-enabled vital-sign tracking, raising interoperability expectations. Vendors offering language localisation gain headroom, especially as personal-data-protection acts proliferate. Leapfrogging older infrastructure, hospitals adopt cloud EHR platforms that align with regional broadband upgrades, fortifying Asia-Pacific's role in the hospital information system market.

Europe, the Middle East and Africa present a spectrum of digital maturity. Germany's Krankenhauszukunftsgesetz (KHZG) fund compels hospitals to certify digital-medication management, spurring suppliers to expand ecosystem services. GCC nations report more than three-quarters of public hospitals already on EHRs, amplified by Saudi Arabia's Vision 2030 tele-consultation targets. Regulatory convergence on data-interchange standards eases multi-national implementations, while talent flows from Europe to Gulf megaprojects accelerate skill-mix evolution. Collectively, the region remains a heterogeneous but strategically important theatre for the hospital information system market.