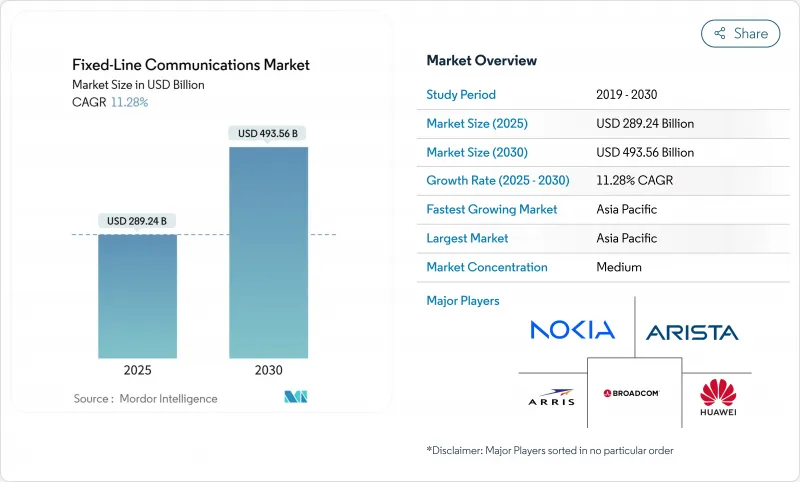

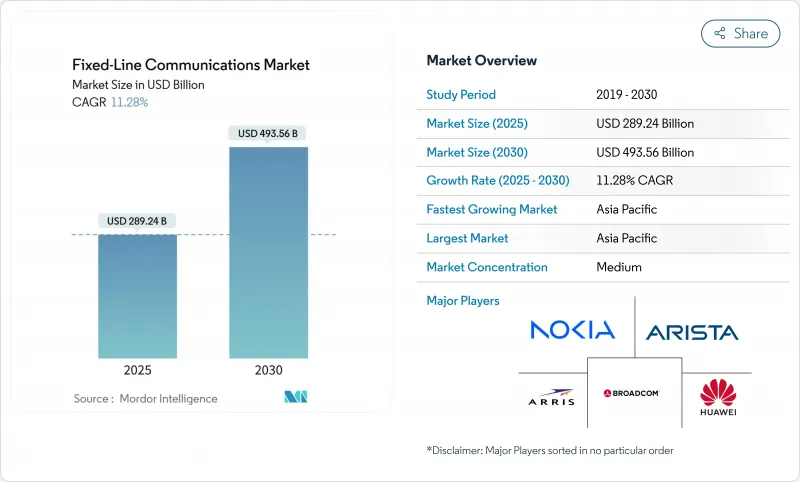

고정 통신 시장 규모는 2025년에 2,892억 4,000만 달러에 이르고, 2030년에는 4,935억 6,000만 달러에 달할 것으로 예상되며, 기간 중 11.28%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

지속적인 성장은 고정 통신 시장이 클라우드 컴퓨팅, 인공지능 워크로드, 5G 백홀 요구사항을 어떻게 지원하고 있는지를 반영하며, 기본 디지털 인프라로서의 역할을 확고히 하고 있습니다. 유럽 연합(EU), 미국, 아시아태평양의 여러 정부가 채택한 신메트릭 기가비트 타겟은 광섬유 배치를 가속화하고 있으며, 데이터 주권에 관한 규칙은 지연에 민감한 트래픽을 국내 네트워크에 유지하도록 촉구하고 있습니다. 급속한 하이퍼스케일 데이터센터 건설은 레거시 백본에 부담을 주고 운영자를 800G 및 테라비트 광 업그레이드로 향하게 하여 장비 수요를 높이고 있습니다. 이와 병행하여 개방형 표준 이니셔티브와 Software-Defined Networking은 경쟁 우위를 하드웨어 기능에서 프로그래머블 플랫폼으로 이동시켜 저지연 서비스 수준의 헌신에 대응할 수 있는 새로운 공급업체에게 기회를 제공합니다. 도로사용허가의 합리화를 요구하는 규제압력이 높아짐에 따라 고정 통신 시장이 대응가능한 수요를 어느 정도의 속도로 획득할 수 있는지는 최종사용자의 의욕이 아니라 도입속도가 좌우하는 것을 시사합니다.

AT&T가 2026년까지 3,000만 가구에 FTTH를 부설하겠다는 공약을 내세우고 있는 것처럼 기존의 통신사업자는 구리선의 단계적인 업그레이드에서 전반적인 파이버 교환으로 이동하고 있습니다. 인프라펀드에 지원된 과제적인 알토넷은 교외의 서비스가 충분하지 않은 지역을 개척해, 자신들의 기반을 지키려고 약기되고 있는 레거시 사업자에게, 보다 신속한 대응을 다가가고 있습니다. 미국의 BEAD와 같은 보조금 제도는 수십억의 자금을 농촌 건설에 돌려 깊은 섬유에 유리한 비용 방정식을 더 기울입니다. 보다 빠른 개발 기술(마이크로 트렌치, 커넥티드 드롭)과 덕트 재사용을 결합하여 가구당 설비 투자액을 줄이고 중밀도 지역에서도 매력적인 내부 수익률을 유지할 수 있습니다. 장기적으로 유비쿼터스 파이버 플랫폼을 구축함으로써 캐리어는 엣지 컴퓨팅 호스팅과 사설 5G 서비스를 업셀 할 수 있습니다.

지방의 주택 1동을 통과시키는 데는 1,000달러 이상의 비용이 들 수 있고, 이와바와 산간부에서는 그 금액이 급격히 상승합니다. 규모의 경제성이 없는 소규모 통신 사업자는 상당히 높은 자금 조달 비용을 부담하게 되며, 그 채무 약관은 종종 느린 롤아웃 일정을 지시합니다. 작업자가 전기 기둥에 섬유를 설치해야 하는 경우, 준비 작업 및 설치 요금을 둘러싼 법적 분쟁으로 인해 몇 달의 지연이 발생합니다. 공인 광섬유 연결업체의 임금 인플레이션도 문제를 복잡하게 하고 있어 이전에는 모바일 네트워크 엔지니어만이 받고 있던 계약 보너스를 지급하고 있는 시장도 있습니다. 정부 보조금은 건설비의 일부를 부담해 줍니다만, 벤더나 기술의 제한에 의해 프로젝트의 총 비용은 한층 더 상승해, 투자자의 일반적인 투자 회수 기간을 넘어 버립니다.

광섬유 케이블은 2024년 매출의 28.3%를 차지하며 고정 통신 시장의 볼륨 백본으로 자리잡았습니다. 800G의 코히런트 전송에 대한 수요 증가는 사업자가 외부 플랜트 업그레이드를 가속화하는 것을 뒷받침하고, 관련 광회선 단말기와 패시브 스플리터는 CAGR 13.9%로 액세스 기기에 대한 지출을 증가시킵니다. 트랜스미터 벤더는 캐리어가 기존의 100G 옵틱을 비트당 전력 소비를 절반으로 줄이는 플러그 케이블로 교체하여 네트워크 전체의 효율성을 높이는 이점이 있습니다. 스위칭 장비의 수익은 소프트웨어 정의 컨트롤 플레인이 중앙 오피스 내 고성능 리프 스파인 패브릭을 필요로 하기 때문에 함께 확장됩니다.

일반 가정이 Wi-Fi 7 라우터나 메쉬 노드를 채용하는 가운데, 고객 가내 기기는 계속해서 멀티기가비트의 파도를 탄다. 공급업체는 현재 관리형 Wi-Fi 애널리틱스를 번들로 제공하고 캐리어가 가정 내 성능을 원격으로 문제 해결할 수 있도록 하고 있으며, 트랙의 출동 횟수를 줄이고 있습니다. 반면 2024년에는 고정 무선 CPE 출하량이 DOCSIS 모뎀을 넘어서고 광섬유 고정 통신 시장 규모가 여전히 우세하다는 사실에도 불구하고 무선 대안이 특정 배포 시나리오를 포착할 수 있음을 보여주었습니다.

고정 광대역 데이터 서비스는 2024년 총 매출의 68.9%를 차지했으며, 분 단위 과금에서 대역폭 수익화로 돌이킬 수 없게 축발을 옮기는 것으로 확인되었습니다. IPTV 및 기타 부가가치 플랫폼이 CAGR 12.4%로 이어지지만, 이는 캐리어가 광섬유에 대한 투자를 컨텐츠 및 클라우드 게임의 경상 수익으로 변환하는 방법을 반영합니다. 엔터프라이즈가 클라우드 PBX 서비스로 전환하고 일반 가정이 모바일에만 의존하는 동안 기존의 고정 음성은 줄어들고 있습니다.

연결성을 사이버 보안 및 엣지 컴퓨팅 오케스트레이션과 융합시킨 관리 서비스 번들은 특히 사내에 IT 팀이 없는 중견기업에서 지지되고 있습니다. 네트워크상의 AI 엔진에 의해 강화된 동영상 분석은 초타겟팅 광고를 가능하게 하며 추가 설비 투자 없이 금리를 증가시킵니다.

고정 통신 시장 보고서는 제품 유형(전송 장치, 교환 장치 등), 서비스 유형(고정 음성, 고정 광대역 데이터 등), 기술(디지털 가입자선, 동축(Docsis) 등), 최종 사용자(주택, 중소기업, 대기업 등), 지역별로 분류됩니다.

아시아태평양은 2024년 매출의 38.7%를 차지했고 CAGR 11.42%를 나타내 최대 고정 통신 시장으로 자리매김할 것으로 예측됩니다. 중국에서는 10G 도시 네트워크가 의무화되어 전국적인 광섬유 배치가 추진되는 반면 인도에서는 Digital Bharat 프로그램이 관민 합작 사업을 유발하여 연간 50만 km 이상의 경로가 추가됩니다. 일본과 한국의 사업자는 몰입형 미디어와 산업 자동화를 지원하기 위해 25G와 50G의 PON으로 업그레이드합니다.

북미에서는 BEAD 프로그램을 활용하여 지방의 격차를 해소합니다. Tier 1 경력이 도시에서의 건설을 가속해, 위성 광대역 기업와 경쟁해 장기 가입자를 확보합니다. 베라이존의 고정 무선 가입자 증가는 대체 리스크를 부각하고 있지만, 섬유 부설 수는 전주 설치 개혁에 의해 허가 대기 행렬이 단축되었기 때문에 분기 기준으로 과거 최고를 기록하고 있습니다. 캐나다의 오픈 액세스 규칙은 기존 사업자에게 광섬유 루프 도매를 강제하고 네트워크 소유자의 경제성을 손상시키지 않고 취득률을 자극하는 소매 경쟁을 촉진합니다.

유럽의 기가비트 인프라법은 홈 파기 승인을 간소화하고 '디그완스' 조정을 실시하여 토목 공사비를 2자리 줄여줍니다. 프랑스와 스페인에서는 FTTH의 보급률이 75%를 넘어 유비쿼터스 기가비트 서비스를 사용할 수 있게 된 후 수요의 탄력성이 증명되었습니다. 독일의 늦은 시작은 민간 자본이 출자하는 알토넷의 뒷받침을 받고 가속화, 영국의 프로젝트 기가비트 경매는 도달 곤란한 코무라까지 커버리지를 확대하고 있습니다.

The fixed-line communications market size reaches USD 289.24 billion in 2025 and is forecast to touch USD 493.56 billion by 2030, advancing at an 11.28% CAGR over the period.

Sustained growth reflects how the fixed-line communications market underpins cloud computing, artificial intelligence workloads, and 5G back-haul requirements, cementing its role as foundational digital infrastructure. Symmetric gigabit targets adopted by the European Union, the United States, and multiple Asia-Pacific governments continue to accelerate fiber roll-outs, while data-sovereignty rules spur enterprises to keep latency-sensitive traffic on national networks. Rapid hyperscale data-center construction strains legacy backbones, pushing operators toward 800 G and terabit optical upgrades that lift equipment demand. In parallel, open-standards initiatives and software-defined networking shift competitive advantage from hardware features toward programmable platforms, creating opportunities for new vendors that can match low-latency service-level commitments. Mounting regulatory pressure to streamline right-of-way permits suggests that deployment speed, not end-user appetite, will determine how fast the fixed-line communications market captures its addressable demand.

Incumbent telcos have shifted from incremental copper upgrades to full-scale fiber replacement, as seen in AT&T's pledge to pass 30 million premises with FTTH by 2026. Challenger altnets, backed by infrastructure funds, pick off pockets of under-served suburbs, forcing faster reactions from legacy operators eager to defend their base. Subsidy frameworks such as BEAD in the United States redirect billions toward rural builds, further tilting the cost equation in favor of deep fiber. The combination of faster deployment techniques (micro-trenching, connectorized drops) and duct re-use lowers capex per home, keeping internal rates of return attractive even in mid-density territories. Longer term, establishing a ubiquitous fiber platform positions carriers to upsell edge-compute hosting and private 5G services.

Passing a single rural premise can cost more than USD 1,000, a figure that climbs sharply in rocky or mountainous terrain. Smaller carriers without scale economics shoulder significantly higher financing costs, and their debt covenants often dictate slower roll-out schedules. Where crews must attach fiber to utility poles, make-ready work and legal disputes over attachment fees add months of delay. Wage inflation for certified fiber splicers compounds the problem, with some markets offering signing bonuses that previously only mobile-network engineers received. Although government grants defray part of the build expense, restrictions on permissible vendors or technology can push total project cost back up, stretching payback periods beyond typical investor horizons.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fiber-optic cables generated 28.3% of revenue in 2024, cementing their position as the volume backbone of the fixed-line communications market. Intensifying demand for 800 G coherent transmission pushes operators to accelerate outside-plant upgrades, while associated optical line terminals and passive splitters lift access-equipment spend at a 13.9% CAGR. Transmission-equipment vendors benefit as carriers swap legacy 100 G optics for pluggables that halve power per bit, enhancing total network efficiency. Switching gear revenue expands in tandem because software-defined control planes require high-performance leaf-spine fabrics inside central offices.

Customer-premises equipment continues to ride the multi-gigabit wave as households adopt Wi-Fi 7 routers and mesh nodes. Vendors now bundle managed Wi-Fi analytics that let carriers troubleshoot in-home performance remotely, reducing truck rolls. Meanwhile, fixed-wireless CPE shipments overtook DOCSIS modems in 2024, showing that wireless substitution can capture specific deployment scenarios even as the fixed-line communications market size for fiber remains dominant.

Fixed broadband data services accounted for 68.9% of total 2024 revenue, confirming the irreversible pivot from minutes-based billing to bandwidth monetization. IPTV and other value-added platforms follow with a 12.4% CAGR, reflecting how carriers translate sunk fiber investments into recurring content and cloud-gaming revenue. Traditional fixed voice continues its secular slide as enterprises migrate to cloud PBX offerings and households rely exclusively on mobile.

Managed service bundles that merge connectivity with cybersecurity and edge-compute orchestration gain favor, especially among mid-sized enterprises lacking in-house IT teams. Enhanced video analytics powered by on-network AI engines enable ultra-targeted advertising, adding incremental margins without additional capex.

The Fixed-Line Communication Market Report is Segmented by Product Type (Transmission Equipment, Switching Equipment, and More), Service Type (Fixed Voice, Fixed Broadband Data, and More), Technology (Digital Subscriber Line, Coaxial (Docsis), and More), End User (Residential, Small and Medium Enterprises, Large Enterprises, and More), and Geography.

Asia Pacific retained 38.7% of 2024 revenue and is projected to expand at an 11.42% CAGR, cementing its position as the largest fixed-line communications market. China's mandate for 10 G city networks drives nationwide fiber deployment, while India's Digital Bharat program triggers public-private joint ventures that add more than 0.5 million route-kilometers annually. Japanese and Korean operators upgrade to 25 G and 50 G PON to support immersive media and industrial automation.

North America leverages the BEAD program to close rural gaps. Tier-1 carriers accelerate urban builds, racing satellite broadband players to lock in long-term subscribers. Verizon's fixed-wireless subscriber gains highlight substitution risk, yet fiber build counts hit new quarterly highs as pole-attachment reforms shorten permitting queues. Canadian open-access rules compel incumbents to wholesale fiber loops, fostering retail competition that stimulates take-rates without eroding network-owner economics.

Europe's Gigabit Infrastructure Act streamlines trenching approvals and enforces "dig-once" coordination, cutting civil-works costs by double digits. France and Spain now post FTTH take-up rates above 75%, proving demand elasticity once ubiquitous gigabit service is available. Germany's late start accelerates on the back of private-equity-funded altnets, while the United Kingdom's Project Gigabit auctions extend coverage to hard-to-reach hamlets.