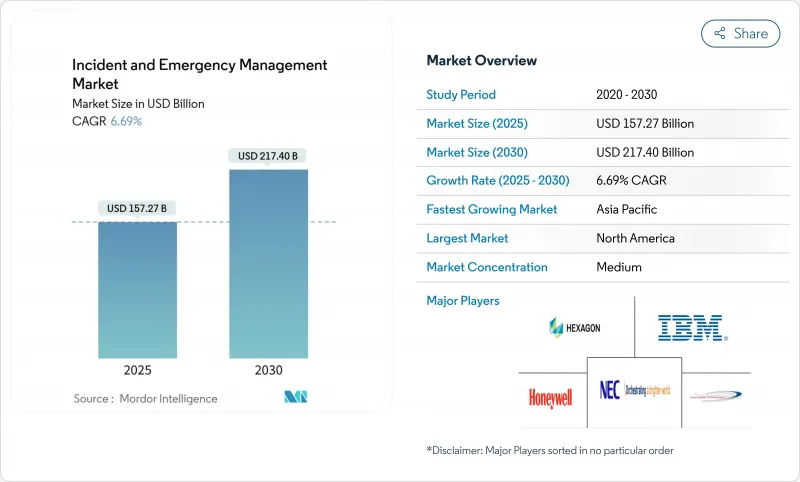

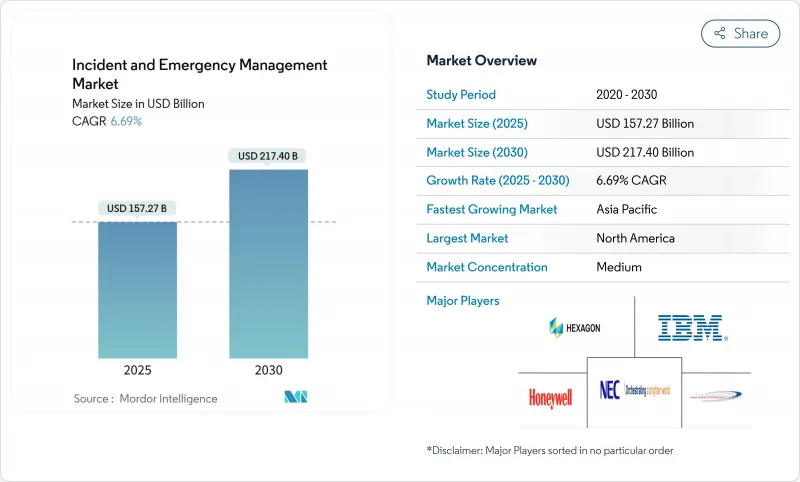

사고 및 비상 관리 시장 규모는 2025년에 1,572억 7,000만 달러로 평가되었고 2030년에 2,174억 달러로 성장할 전망입니다.

이러한 추세는 공공 및 민간 부문 모두에서 비상 대비 예산의 급속한 제도화와 함께, 보다 포괄적이고 기술 기반의 대응 역량을 요구하는 기상 관련 재해의 증가를 반영합니다. 북미는 정교한 연방 자금 지원 프로그램 덕분에 광범위한 우위를 유지하고 있는 반면, 아시아는 정부가 조기 경보 및 대량 알림 인프라를 업그레이드함에 따라 가장 빠른 성장세를 보이고 있습니다. 수요는 지리공간 분석, 클라우드 네이티브 아키텍처, AI 기반 의사 결정 지원이 융합된 통합 플랫폼으로 전환되며, 이로 인해 감지부터 현장 대응까지의 시간이 단축됩니다. 심화되는 사이버-물리적 위협과 교통·공공 안전 제어 시스템의 스마트시티 인프라로의 이전이 단기 성장 촉진 요인으로 작용합니다.

자연 재해로 인한 경제적 손실은 2024년 3,200억 달러에 달했으며, 북미가 약 60%를 차지하고 아시아태평양 지역에서 79건의 수문기상 사건이 발생하여 대비 태세 격차를 부각시켰습니다. 손실률 상승으로 정부와 기업은 다중 위험 조기 경보 네트워크, 클라우드 기반 사고 대시보드, 위성 기반 상황 인식 피드를 도입하고 있습니다. 세계은행 산하 GFDRR(글로벌 재해 위험 감소 기금)과 같은 개발 금융 기관들은 역량 강화 보조금을 지원하며, 다년간의 조달 파이프라인을 구축해 사건 및 비상 관리 시장을 강화하고 있습니다.

통신 사업자와 공공 기관은 이제 인증된 셀 브로드캐스트 및 다중 모드 경보 지원을 법적으로 의무화되어, 대량 알림 시스템 구축이 가속화되고 있습니다. FEMA의 IPAWS 기준은 미국에서 광범위한 카운티 수준의 도입을 촉진했으며, EU의 전자통신법은 2025년까지 대륙 전체 경보 도달을 의무화했습니다. 프랑스의 차세대 임무중요 광대역 네트워크는 주파수 이주가 어떻게 더 풍부한 미디어(위치 기반 텍스트, 이미지, 짧은 동영상)를 가능케 하여 위기 시 대중의 대응력을 높이는지 보여줍니다.

많은 유럽 공공안전 기관은 여전히 독점 프로토콜로 작동하는 협대역 P25 또는 TETRA 무전기에 의존하고 있어, 광대역 셀룰러 또는 위성 링크로의 원활한 로밍을 방해합니다. SAFECOM 보조금 지침은 주정부에 표준 기반 브리징 기술 채택을 촉구하지만, 자금 조달 및 조달 주기로 인해 통합 솔루션의 도입이 지연되고 있습니다. 이로 인한 파편화된 시스템은 국경 간 협력을 지연시키고, 사건 및 비상 관리 시장의 단기 성장을 다소 저해합니다.

솔루션은 2024년 사고 및 비상 관리 시장의 55%를 차지했으며, 이는 단일 창에서 경보, 자원 배분, 사후 보고를 통합 관리하는 엔드투엔드 플랫폼에 대한 구매자 선호도를 입증합니다. AI 엔진과 클라우드 탄력성에 대한 신속한 업그레이드는 지속적인 지갑 점유율 확장을 뒷받침합니다. 벤더들은 CAD, GIS, EOC 모듈과 연동되는 오픈 API 생태계를 강조하여 지역 기관의 가치 실현 시간을 단축하고 있습니다. 예측 기간 동안 보험 위험 점수 산정 도구와의 긴밀한 통합은 플랫폼 수익을 더욱 공고히 할 것입니다.

시뮬레이션 및 훈련 부문은 절대적 매출 규모는 작지만, 기관들이 시나리오 기반 대비 정책을 제도화함에 따라 연평균 7.8% 성장률을 보이고 있습니다. 조지 메이슨 대학의 AI 강화형 'Go-Repair'와 같은 게임화 모듈은 몰입형 학습이 이탈률을 낮추고 역량을 향상시켜 훈련 예산을 증대시키는 방식을 보여줍니다. 이 부문의 확장은 선순환 구조를 형성합니다. 강화된 대비 지표는 주정부의 복원력 보조금 수혜 자격을 부여하여 플랫폼 솔루션에 대한 상류 수요를 강화합니다.

비상/대량 알림 부문은 규제 의무화로 업그레이드 주기가 고정되면서 2024년 매출의 28%를 계속 차지할 전망입니다. 그러나 감시 및 보안 모니터링 부문은 AI 기반 영상 분석과 물체 탐지 기술이 출동 시간을 단축시키며 8.5% CAGR로 가장 빠르게 성장하는 틈새 시장입니다. 영상 피드가 이제 911 센터에 직접 통합되어 상황 인식 명확성과 대응자 안전성을 증대시키는 지속적인 정보 루프를 생성합니다. 전망 기간 동안, 지방자치단체의 ‘비전 제로(Vision Zero)’ 프로그램이 예상대로 가속화될 경우 이 하위 부문에 연계된 사고 및 비상 관리 시장 규모는 350억 달러를 초과할 수 있습니다.

교통 및 사고 관리는 도시 이동성 투자에 힘입어 성장하는 반면, CBRNE/유해물질 탐지 분야는 인체 노출을 최소화하는 무인 항공 시스템을 통해 센서 배치를 확대하고 있습니다. 재해 복구 및 백업 솔루션은 2차적인 사업 중단 비용을 완화하는 데 중요한 역할을 수행합니다.

사고 및 비상 관리 시장은 구성 요소별(솔루션, 서비스, 기타), 솔루션 유형별(비상/대량 알림, 기타), 서비스 유형별(전문 서비스, 컨설팅 및 권고 등), 통신 시스템별(최초 대응자 통신, 비상용 무전기 등), 시뮬레이션 모듈별(교통 시뮬레이션 소프트웨어, 기타), 최종 사용자별(정부, BFSI 등), 지역별로 세분화됩니다.

북미는 FEMA 보조금, 민간 부문 사이버 투자, 광범위한 FirstNet 보급에 힘입어 2024년 매출의 42%를 차지합니다. 미국 카운티들은 상호운용성 프로토콜을 채택하고 있으며, 캐나다의 DFAA 프레임워크는 재정적 안전장치와 현대화 약속을 결합하여 공급업체, 시스템 통합업체, 학계로 구성된 성숙한 생태계를 조성하고 있습니다. TIM(실시간 정보 관리)을 위한 유선 드론 시범 배치는 실질적인 증거를 제공하여 지방자치단체 예산 갱신을 뒷받침합니다.

아시아는 초거대 도시들의 태풍 및 지진 위험 노출로 인해 7.3%의 연평균 성장률(CAGR)을 기록하고 있습니다. 중국은 지휘 센터에 도시 전체 HD 카메라 그리드를 중첩 적용하고, 일본의 J-ALERT 시스템은 실시간 위험 정보를 대중에게 전달합니다. 인도는 사이클론 후 구호 통로 분류를 위해 AI 기반 지리공간 플랫폼을 활용하여 비상 운영 센터에 대한 기업 지출을 증가시킵니다. ADB의 재난 위험 관리 실행 계획을 통한 다자간 자금 조달은 ASEAN 시장의 조달을 촉진합니다.

유럽은 EECC(유럽 전기통신 규정) 준수 시한이 다가옴에 따라 꾸준한 교체 주기를 유지하고 있습니다. BroadWay와 같은 프로젝트는 응급 대응 요원을 위한 국경 간 로밍을 시범 운영하며, 솔루션 제공업체들이 보안 SIM 인증 및 서비스 품질 계층을 내장하도록 유도하고 있습니다. 한편 중동과 아프리카에서는 인도주의 구호 기관과 국가 안보 기관들이 복합적인 가뭄 및 분쟁 위험에 대응하기 위해 조기 경보 분석을 표준화함에 따라 점진적인 도입이 이루어지고 있습니다.

The incident and emergency management market size is valued at USD 157.27 billion in 2025 and is forecast to reach USD 217.40 billion by 2030, reflecting a steady 6.69% CAGR over the period.

This trajectory mirrors the rapid institutionalisation of emergency-preparedness budgets in both the public and private sectors, coupled with rising weather-driven disasters that command more comprehensive, technology-enabled response capabilities. North America maintains a broad lead on account of sophisticated federal funding programmes, while Asia registers the fastest expansion as governments upgrade early-warning and mass-notification infrastructures. Demand pivots toward integrated platforms that fuse geospatial analytics, cloud-native architectures, and AI-driven decision support, shortening the time between detection and coordinated field action. Intensifying cyber-physical threats and the migration of traffic and public-safety controls into smart-city fabrics round out the near-term growth catalysts.

Economic losses from natural catastrophes reached USD 320 billion in 2024, with North America absorbing roughly 60% and Asia Pacific recording 79 hydro-meteorological events, spotlighting preparedness gaps. Rising loss ratios push governments and enterprises to procure multi-hazard early-warning networks, cloud-based incident dashboards, and satellite-enabled situational-awareness feeds. Development lenders such as the World Bank-hosted GFDRR underwrite capacity-building grants, anchoring multi-year procurement pipelines that fortify the incident and emergency management market.

Legislation now obliges telecom operators and public agencies to support authenticated cell-broadcast and multimodal warnings, accelerating mass-notification deployments. FEMA's IPAWS benchmarks spurred heavy county-level adoption in the United States, while the EU's Electronic Communications Code has set a 2025 deadline for continent-wide alerting reach. France's upcoming mission-critical broadband network illustrates how spectrum migration unlocks richer media-location-pinpointed texts, images, and short videos-that heighten public responsiveness during crises.

Many European public-safety agencies still depend on narrowband P25 or TETRA radios that operate on proprietary protocols, hampering seamless roaming onto broadband cellular or satellite links. SAFECOM grant guidance presses states to adopt standards-based bridging technologies, yet funding and procurement cycles slow roll-out of converged solution. The resulting patchwork delays cross-border coordination and marginally dampens the incident and emergency management market's near-term growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions generated 55% of the incident and emergency management market in 2024, a testament to buyer preference for end-to-end platforms that orchestrate alerting, resource allocation, and after-action reporting in a single pane of glass. Rapid upgrades to AI engines and cloud elasticity underpin continued wallet share expansion. Vendors accentuate open-API ecosystems that plug into CAD, GIS, and EOC modules, improving time-to-value for regional agencies. Over the forecast horizon, tighter integration with insurance-risk scoring tools will further entrench platform revenues.

Simulation & Training, though smaller in absolute revenue, is scaling at 7.8% CAGR as agencies institutionalise scenario-based preparedness policies. Gamified modules such as George Mason University's AI-augmented "Go-Repair" illustrate how immersive learning cuts attrition and raises competence, thereby elevating training budgets. This segment's expansion feeds a virtuous cycle: stronger preparedness metrics qualify states for resilience grants, reinforcing upstream demand for platform solutions.

Emergency/Mass Notification continues to anchor 28% of 2024 revenue as regulated mandates lock in upgrade cycles. However, Surveillance & Security Monitoring is the fastest-moving niche at 8.5% CAGR, propelled by AI-driven video analytics and object detection that shorten dispatch times. Video feeds now integrate directly into 911 centres, producing a continuous intelligence loop that amplifies situational clarity and responder safety. Over the outlook period, the incident and emergency management market size attached to this sub-segment could exceed USD 35 billion if municipal vision-zero programmes accelerate as projected.

Traffic & Incident Management rides urban-mobility investments, whereas CBRNE/HazMat Detection broadens sensor deployment via unmanned aerial systems that minimise human exposure. Disaster Recovery & Backup solutions play a crucial role, mitigating secondary business-interruption costs.

The Incident and Emergency Management Market is Segmented by Component (Solutions, Services, and More), Solution Type (Emergency/Mass Notification, and More), Service Type (Professional Services, Consulting and Advisory, and More), Communication System (First-Responder Communication, Emergency Radios, and More), Simulation Module (Traffic Simulation Software, and More), End-User (Government, BFSI, and More), and Geography.

North America anchors 42% of 2024 revenue, sustained by FEMA grants, private-sector cyber-investment, and wide FirstNet penetration. US counties align on interoperable protocols, and Canada's DFAA framework pairs fiscal backstops with modernisation commitments, cultivating a mature ecosystem of suppliers, systems integrators, and academia. Pilot deployments of tethered drones for TIM lend tangible proof points that reinforce municipal budget renewals.

Asia delivers a 7.3% CAGR, spurred by megacities' exposure to typhoons and seismic risk. China overlays city-wide HD camera grids onto command centres, and Japan's J-ALERT system extends real-time hazard feeds to the public. India leverages AI-driven geospatial platforms to triage relief corridors after cyclones, elevating enterprise spending on emergency operations centres. Multilateral funding via ADB's Disaster Risk Management Action Plan catalyses procurement in ASEAN markets.

Europe sustains steady replacement cycles as the EECC compliance clock counts down. Projects such as BroadWay pilot cross-border roaming for first responders, driving solution providers to embed secure SIM credentialing and quality of service tiers. Meanwhile, the Middle East and Africa witness incremental adoption as humanitarian-relief agencies and national security bodies standardise on early-warning analytics to counter compound drought and conflict risks.