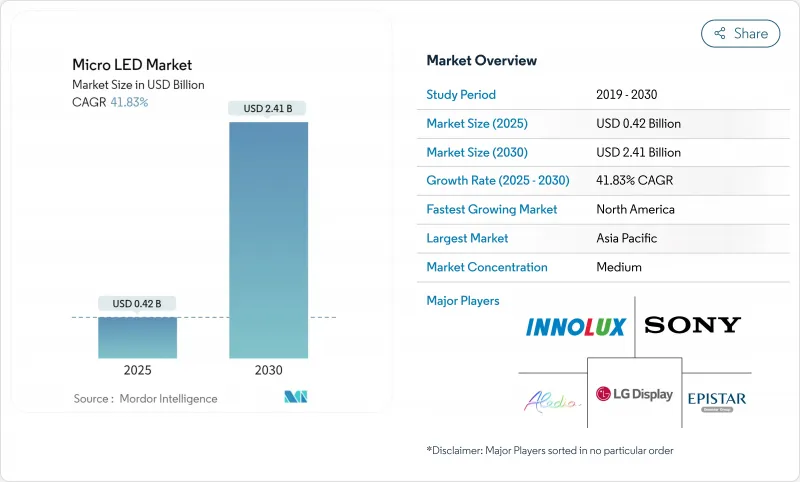

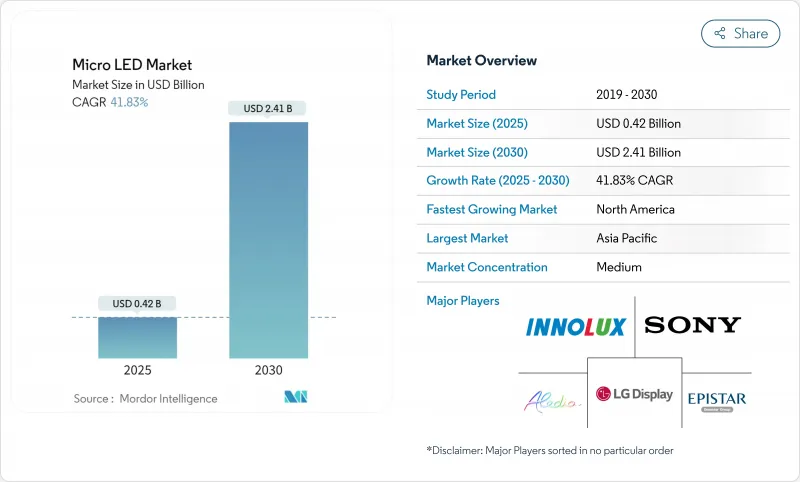

마이크로 LED 시장은 2025년에 4억 2,000만 달러로 평가되었고 2030년에 24억 1,000만 달러에 이를 것으로 예측되며, CAGR은 41.83%를 나타낼 전망입니다.

상업적 성공은 LCD 및 OLED 디스플레이를 능가하는 높은 밝기, 낮은 전력 소모, 입증된 긴 수명이라는 기술적 장점에 달려 있습니다. 제조사들은 대량 생산 수율을 꾸준히 높이고 있으며, 대만과 한국의 자본 집약적 파일럿 라인은 웨어러블 기기, 대형 간판, 자동차 콕핏용 기술 확장을 추진 중입니다. 아시아태평양 지역은 성숙한 반도체 생태계와 지원적인 산업 정책을 바탕으로 제조 리더십을 장악하고 있으며, 북미는 국방 및 AR/VR 프로그램을 위한 투자를 가속화하고 있습니다. 가격은 여전히 높은 수준이지만, 전력, 열, 또는 햇빛 가독성에 심각한 제약이 있는 최종 사용자들이 먼저 움직이고 있어 프리미엄 포지셔닝을 강화하고 마이크로 LED 시장의 장기적 경쟁력을 부각시키고 있습니다.

애플의 LuxVue 인수 이후 30억 달러 투자와 삼성의 병행 R&D 프로그램은 단기 일정 변경에도 장기적 의지를 시사합니다. 드라이버 IC 및 전사 장비 공급업체의 설계 수주 증가로 2인치 미만 패널로의 공급망 전환이 가시화되고 있습니다. 고휘도, 엄격한 전력 예산, 실외 가독성 요구가 스마트워치 디스플레이의 45% 연평균 복합 성장률(CAGR) 전망을 뒷받침합니다. 전문 장비 업체들은 고처리량 픽앤플레이스 시스템을 상용화하며 플래그십 브랜드를 넘어 파일럿 생산의 대중화를 돕고 있습니다. 이러한 역학은 두 시장 선도 기업의 전략적 로드맵이 마이크로 LED 시장 전반의 자본 배분을 어떻게 형성하는지 보여줍니다.

두바이의 럭셔리 쇼핑몰과 서울의 플래그십 매장은 디지털 콘텐츠와 실제 매장 외관을 융합하는 베젤리스 투명 마이크로 LED 외벽을 설치 중입니다. 4,000니트 실외 밝기를 구현한 Tianma의 PID 프로토타입은 LCD 대비 성능 우위를 입증합니다. 모듈식 아키텍처는 맞춤형 치수 구현을 단순화해 소매 통합업체의 설치 주기를 단축합니다. 에너지 효율성은 24시간 운영 시 총소유비용(TCO)을 절감합니다. 이러한 특성들은 디지털 사이니지가 보유한 38%의 응용 분야 선두 위치를 공고히 하며 마이크로 LED 시장 내 새로운 수익 창출의 기반을 마련합니다.

대형 기판에 수백만 개의 미세 발광체를 배치하는 정확도는 여전히 60% 미만으로, 불량률을 증가시키고 라인 가동률을 저하시킵니다. 장비 제조사들은 99.99% 배치 정확도 달성을 위해 레이저 유도 전이 및 전자기 픽업 방식을 시험 중이며, VueReal의 MicroSolid Printing은 7μm 미만 피치 구현 능력을 보여주고 있습니다. 이러한 솔루션이 성숙되기 전까지는 생산 비용이 OLED 대비 높은 수준을 유지하여 마이크로 LED 시장의 대중 시장 TV 및 스마트폰 분야에서의 단기적 보급이 제한될 전망입니다.

디지털 사이니지는 2024년 매출의 38%를 차지하며, 마이크로 LED가 고영향력·주간 가독성 비디오 월에 적합함을 입증했습니다. 럭셔리 리테일 체인은 매끄러운 캔버스를 형성하는 모듈형 타일을 도입하는 반면, 교통 허브는 중요 정보 게시판에 마이크로 LED의 낮은 고장률을 선호합니다. 이 부문의 안정적인 주문 흐름은 초기 생산 능력 활용도를 뒷받침하며 마이크로 LED 시장을 강화합니다.

반면 스마트워치 출하량은 소비자 가전 출시 주기에 따라 확대됩니다. 배터리 제약이 있는 웨어러블 기기는 1와트 미만 디스플레이를 요구하며, 3,000니트 피크 밝기는 실외 사용성을 확장합니다. 해당 부문의 45% 예상 연평균 성장률(CAGR)은 핵심 물량 성장 동력으로 자리매김하게 합니다. 근접 시야 AR 모듈도 픽셀 밀도가 4,000 PPI를 초과하며 진전되어, 더 넓은 채택의 기반을 마련하고 소형 패널 부문의 마이크로 LED 시장 규모 장기적 확장을 뒷받침하고 있습니다.

소비자 가전제품은 프리미엄 TV, 시계, 스마트폰이 이 기술의 높은 명암비와 긴 수명을 수용하며 2024년 수요의 72.1%를 차지했습니다. 삼성의 플래그십 TV 라인인 '더 월(The Wall)'은 대형 스크린 쇼케이스 설치의 중심축 역할을 하며 프리미엄 가격 책정을 정당화합니다. 이 부문의 폭넓은 적용 범위는 백플레인, 드라이버 IC, 검사 장비 전반에 걸친 부품 수요를 안정화시켜 마이크로 LED 시장에서 핵심적 위치를 공고히 합니다.

유럽의 엄격한 햇빛 가독성 규정 강화로 자동차 수요는 연평균 47% 성장률로 증가할 전망입니다. HUD 프로토타입은 편광 윈드스크린을 통한 가독성을 보장하는 10,000니트 이상의 밝기를 달성했습니다. 확장된 온도 내성과 진동 저항성도 AEC-Q 표준을 충족합니다. 더 많은 자동차 제조사들이 첨단 운전자 디스플레이를 통합함에 따라, 마이크로 LED의 콕핏 전자기기 시장 규모는 확대될 전망이며, 이는 소비자 가전 beyond을 넘어 수익원을 다각화할 것입니다.

50인치 이상의 패널은 2024년 매출의 55.6%를 차지했습니다. 고급 주거 및 기업 로비에서는 설치 유연성과 타의 추종을 불허하는 최고 휘도가 프리미엄 가격을 정당화하는 110인치부터 220인치 어셈블리를 채택하고 있습니다. 고급 호텔 시설은 베젤 없는 표면을 활용해 몰입형 경험을 창출하며 마이크로 LED 시장 내 점유율 우위를 공고히 하고 있습니다.

10인치 미만 패널은 제조 기술 혁신으로 다이당 비용이 감소함에 따라 2030년까지 연평균 49% 성장할 전망입니다. 1인치 미만 마이크로 디스플레이는 VR 헤드셋용으로 6,500 PPI에 도달했으며, 차량용 스마트 계기판은 소형 고해상도 형식을 요구합니다. 첨단 전사 인쇄 기술의 도입으로 학습 곡선이 가속화되면서, 소형 패널의 물량이 향후 10년 동안 마이크로 LED 시장 점유율 역학을 점차 재편할 것임을 시사합니다.

아시아태평양 지역은 2024년 매출의 46.9%를 차지했으며, 이는 대만의 백엔드 공정 역량과 한국의 깊은 디스플레이 노하우에 힘입은 결과입니다. BOE의 HC SemiTek 인수와 Sanan의 20억 달러 규모 팹 건설 계획은 지속적인 자본 유입을 강조합니다. GaN 웨이퍼 수출 환급을 포함한 정부의 지원 정책은 지역적 비용 우위를 유지하고 마이크로 LED 시장에서의 리더십을 공고히 합니다.

북미는 2030년까지 연평균 43% 성장률로 가장 빠르게 성장 중입니다. CHIPS 법안의 연방 인센티브가 신규 질화갈륨 생산라인을 촉진하는 한편, 국방 및 AR/VR 프로그램이 구매 계약을 확보합니다. 애플의 다중 사이트 R&D 기반과 메타의 헤드셋 야망이 생태계 활동을 집중시켜 강력한 설계 반복을 주도하고 더 높은 기판 수요를 뒷받침합니다.

유럽은 자동차 및 산업용 분야에서 특화된 역할을 구축 중입니다. 햇빛 가독성 규제로 HUD 통합이 가속화되며, 현지 1차 공급업체들은 안정적인 다이 공급 확보를 위해 아시아 LED 제조사와 협력합니다. 동시에 EU의 클린룸 개조 지원금은 신생 웨이퍼 공급 기반을 육성하여 아시아 집중화에 대한 전략적 헤지 기능을 제공합니다. 중동·아프리카 지역은 GCC 쇼핑몰의 프리미엄 소매 간판으로 도입이 시작되는 반면, 라틴아메리카는 스포츠 인프라 투자와 연계된 대형 전시장 디스플레이를 시범 운영 중입니다.

The Micro LED market stood at USD 0.42 billion in 2025 and is forecast to reach USD 2.41 billion by 2030, advancing at a 41.83% CAGR.

Commercial traction hinges on the technology's high brightness, low power draw, and proven longevity that outperforms LCD and OLED displays. Manufacturers are steadily lifting mass-transfer yields, and capital-intensive pilot lines in Taiwan and South Korea are scaling the technology for wearables, large-format signage, and automotive cockpits. Asia Pacific commands manufacturing leadership on the back of mature semiconductor ecosystems and supportive industrial policies, while North America is accelerating investment for defense and AR/VR programs. Pricing remains elevated, yet end-users with severe power, thermal, or sunlight-readability constraints are moving first, reinforcing premium positioning and underscoring the long-run competitiveness of the Micro LED market.

Apple's USD 3 billion outlay since acquiring LuxVue and Samsung's parallel R&D programs signal long-term commitment despite near-term schedule shifts. Rising design wins for driver ICs and transfer equipment suppliers indicate a supply-chain pivot toward sub-2-inch panels. High brightness, stringent power budgets, and demand for outdoor readability underpin a projected 45% CAGR for smartwatch displays. Specialized tool vendors are commercializing high-throughput pick-and-place systems, helping democratize pilot production beyond flagship brands. This dynamic underlines how strategic roadmaps from two market leaders shape broader capital allocation across the Micro LED market.

Luxury malls in Dubai and flagships in Seoul are installing bezel-less, transparent Micro LED facades that merge digital content with physical storefronts. Tianma's PID prototypes, engineered for 4,000-nit outdoor brightness, illustrate performance headroom over LCD alternatives. Modular architectures simplify custom dimensions, trimming installation cycles for retail integrators. Energy efficiency also reduces total cost of ownership for 24/7 operation. These attributes safeguard the 38% application lead held by digital signage and set the stage for new revenue pools inside the Micro LED market.

Placement accuracy for millions of micro-emitters on large substrates remains below 60%, inflating scrap rates and depressing line utilization. Equipment makers are trialing laser-induced transfer and electromagnetic pick-up to reach 99.99% placement accuracy, while VueReal's MicroSolid Printing demonstrates sub-7 µm pitch capability. Until these solutions mature, output costs will stay above OLED equivalents, limiting near-term penetration in mass-market televisions and smartphones inside the Micro LED market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Digital signage delivered 38% of 2024 revenue, validating Micro LED's suitability for high-impact, day-light-readable video walls. Luxury retail chains deploy modular tiles that form seamless canvases, while transportation hubs favor Micro LED's low failure rates for critical information boards. The segment's stable order flow underpins early capacity utilization, reinforcing the Micro LED market.

Smartwatch shipments, in contrast, scale with consumer electronics release cycles. Battery-limited wearables demand sub-1-watt displays, and 3,000-nit peak brightness extends outdoor usability. The segment's 45% forecast CAGR positions it as a pivotal volume driver. Near-eye AR modules are also progressing as pixel densities exceed 4,000 PPI, setting the stage for broader adoption and supporting the long-run expansion of the Micro LED market size at the small-panel end.

Consumer electronics captured 72.1% of 2024 demand as premium TVs, watches, and smartphones embraced the technology's high contrast and longevity. Samsung's flagship television line, The Wall, anchors large-screen showcase deployments and validates premium pricing. The segment's breadth stabilizes component demand across backplanes, driver ICs, and inspection tools, cementing its central role in the Micro LED market.

Automotive demand is rising at a projected 47% CAGR amid stricter European sun-readability mandates. HUD prototypes achieve over 10,000 nits, ensuring legibility through polarized windscreens. Extended temperature tolerance and vibration resistance also meet AEC-Q standards. As more carmakers integrate advanced driver displays, the Micro LED market size for cockpit electronics is set to widen, diversifying revenue beyond consumer gadgets.

Panels larger than 50 inches held 55.6% of 2024 revenue. Luxury residential and corporate lobbies adopt 110-inch to 220-inch assemblies where installation flexibility and unrivaled peak luminance justify premium prices. High-end hospitality venues leverage bezel-free surfaces to create immersive experiences, reinforcing share dominance within the Micro LED market.

Panels below 10 inches will grow 49% CAGR to 2030 as manufacturing breakthroughs lower cost per die. Sub-1-inch micro-displays now reach 6,500 PPI for VR headsets, and smart-instrument clusters in vehicles demand compact, high-resolution formats. Adoption of advanced transfer printing hastens the learning curve, signaling that small-panel volumes will increasingly reshape Micro LED market share dynamics later in the decade.

The Micro LED Market Report is Segmented by Application (Smartwatch, and More), End-Use Industry (Automotive, and More), Panel Size (Less Than 10 Inch, and More), Pixel Pitch (Fine Pitch, and More), Technology (Color) (RGB, and More), Component (Epitaxial Wafers, and More), Manufacturing Process (Mass Transfer, and More), Offering (Display Modules, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific held 46.9% of 2024 revenue, powered by Taiwan's role in back-end processing and South Korea's deep display know-how. BOE's acquisition of HC SemiTek and Sanan's USD 2 billion fab plan underscore continued capital inflows. Government facilitation, including export rebates on GaN wafers, sustains regional cost advantages and solidifies leadership in the Micro LED market.

North America is growing fastest at 43% CAGR to 2030. Federal incentives under the CHIPS Act spur new gallium-nitride lines, while defense and AR/VR programs lock in offtake agreements. Apple's multi-site R&D footprint and Meta's headset ambitions concentrate ecosystem activity, driving robust design iterations and supporting higher substrate demand.

Europe carves out a specialty role in automotive and industrial deployments. Sun-readability mandates accelerate HUD integration, and local tier-1 suppliers collaborate with Asian LED makers to secure stable die flow. Parallel EU subsidies for clean-room retrofits nurture a nascent wafer supply base, providing strategic hedges against Asian concentration. Adoption in Middle East and Africa begins with premium retail signage in GCC malls, whereas Latin America pilots large-venue displays tied to sports infrastructure investments.