실험실용 여과 시장 규모는 2025년에 47억 달러로 추정되며 예측 기간(2025-2030년)의 CAGR은 8.02%로, 2030년에는 69억 1,000만 달러에 달할 것으로 예상됩니다.

바이오 의약품 생산량 증가, 단일 사용 프로세스 기술의 급속한 채택, 첨단 연구 워크플로우에서 순도 요건 증가가 이 확대를 지원하고 있습니다. 정밀 등급 정밀 여과는 계속 루틴의 정화 단계를 지원하는 반면, 획기적인 나노 여과 플랫폼은 세포 및 유전자 치료 파이프라인에서 분자 수준 분리에 사용되고 있습니다. 연구개발 수탁제조기관(CRDMO)으로의 아웃소싱이 활발해지고, 유연한 여과 어셈블리에 대한 접근이 확대되고, 지속가능성에 대한 대처가 PFAS 프리막으로의 변화를 가속화하고 있습니다. 경쟁사와의 차별화는 현재 바이러스 보존 성능, 자동화 대응, 디지털 호환성을 중심으로 전개되고 있으며, 실험실용 여과 시장 전체에서 제품 업그레이드와 플랫폼 통합이 꾸준히 진행되고 있습니다.

생물학적 제형의 파이프라인은 단일클론항체, 재조합 단백질, 백신, 세포 기반 요법에서 빠르게 확대되고 있습니다. 하류의 정제에서는 생체분자의 완전성을 손상시키지 않고 보다 높은 역가에 대응하는 무균·바이러스 유지 필터가 요구되게 되어 있습니다. 2024년 10월에 출시된 아사히카세이 메디컬의 플라노바 FG1 필터는 바이러스 클리어런스 성능을 유지하면서 항체 처리의 체적 처리량을 7배로 향상시켰습니다. 가방 일체형 단일 사용 카트리지에 대한 왕성한 수요는 제조업체가 신속한 제품 교환이 가능한 유연한 공장을 건설함에 따라 실험실용 여과 시장을 더욱 밀어 올립니다.

높은 처리량 시퀀싱와 멀티플렉스 단백질체학는 샘플 양을 밀리리터에서 마이크로리터로 응축시켰습니다. 차세대 시퀀싱(NGS) 라이브러리 준비 및 바이오마커 검증 분석에서는 96-웰 및 384-웰 플레이트에 해당하는 여과 장치가 표준이 되었습니다. Cytiva사의 Whatman Mini-UniPrep G2 시린지리스 필터는 단백질 침전, 미립자 제거, 오토샘플러 바이알 통합을 한 단계로 수행하여 초고속 액체 크로마토그래피(UHPLC)의 고정밀 요구를 충족하면서 플라스틱 사용량과 작업 시간을 절감합니다. 자동화에 적합한 형식으로 실험실용 여과 시장은 디지털화된 워크웨이 유전체학 플랫폼에 지속적으로 도입할 수 있습니다.

재정적인 압력에 노출된 실험실에서는 비싼 멸균 등급의 멤브레인을 재사용하려는 경우가 많으며 소모품 비용은 최대 50%까지 줄어들지 만 오염 및 검증 위험은 증가합니다. 이 부담은 소규모 학술 연구소 및 필터 무결성 테스트 인프라가 부족한 자원의 제한된 지역에서 심각합니다.

정밀여과의 실험실용 여과 시장 규모는 2024년 세계 매출의 40.2%에 달하여 미생물 제거 및 샘플 정화 작업에서의 편재성을 뒷받침했있습니다. 그러나 나노여과는 실험실이 바이러스 제거, 염 선택적 분리, 치료 등급 완충제 제조를 위한 분자 수준의 차단을 채택하기 때문에 2030년까지 매년 9.6%의 속도로 증가하는 경향이 있습니다. DuPont의 FilmTec LiNE-XD 요소는 이러한 변화를 보여주며 배터리 재료 품질 관리에 중요한 다가 이온을 제외하면서 높은 리튬 투과율을 달성합니다.

한외여과와 역삼투는 각각 단백질 농축과 초순수 제조의 기초가 되고 있습니다. 산화 그래핀 채널과 고분자 골격을 결합한 하이브리드 멤브레인은 분야를 가로지르는 획기적인 다음 웨이브를 가리킵니다. 이러한 혁신은 전통적인 경계를 모호하게 하기 때문에 벤더는 바이오 치료제, 반도체 세정, 환경 시험 등과 관련된 성능 지표를 명확하게 보여줄 필요가 있습니다.

북미는 2024년 실험실용 여과 시장의 36.4%를 차지했는데, 이는 선진적인 의약품 연구개발, 생명공학 집적지, 엄격한 품질규제 때문입니다. 보스턴의 켄달 스퀘어, 샌프란시스코 베이 지역, 샌디에고는 모두 높은 처리량의 생물 제제 탐색 파이프라인을 구축하여 멸균 등급의 배지, 깊이 필터 및 일회용 캡슐의 정기적인 주문을 보장합니다. 캐나다의 생물 제제 생산 능력 확장 프로그램과 멕시코의 비용 경쟁력 있는 충진 마감 시설이 이 지역의 생산량을 더욱 향상시키고 있습니다.

아시아태평양은 가장 역동적인 무대이며 2030년까지 연평균 복합 성장률(CAGR)은 10.7%를 나타낼 전망입니다. 중국 지방의 생명과학공원은 mRNA 백신과 유전자 편집 세포요법을 지원하기 위해 그린필드 공장에 일회용 여과 트레인을 장비하고 있습니다. 싱가포르의 바이오메디컬 사이언스 이니셔티브와 한국의 의약품 자극책은 자동화 대응의 여과 장치에 대한 현지 수요를 강화하고, 일본은 초고정밀도 멤브레인 등급으로 프리미엄 부문을 유지합니다. 인도의 제네릭 의약품 제조업체는 PIC/S 하모나이제이션 가이드라인에 준거를 유지하는 비용 효율적인 미디어를 중시하여 벌크 의약품의 여과 처리 능력을 강화하고 있습니다.

유럽은 세계의 실험실용 여과 시장에서 큰 비중을 유지하고 있습니다. 독일 엔지니어링의 전통은 첨단 멤브레인 모듈의 꾸준한 채용을 촉진하고 영국의 세포 치료 제조 생태계는 바이러스 벡터 정제에 최적화된 특수 필터 설계를 뒷받침하고 있습니다. 프랑스, 스위스, 북유럽 국가들은 강력한 분석 시험 분야에서 이 지역의 발자취를 넓히고 있습니다. 남미에서는 브라질이 백신 충전 마감 라인에 대한 투자의 중심이 되고 있으며, 중동 및 아프리카에서는 국가 예방 접종 프로그램과 수질 프로그램과 관련된 투자가 증가하고 있습니다.

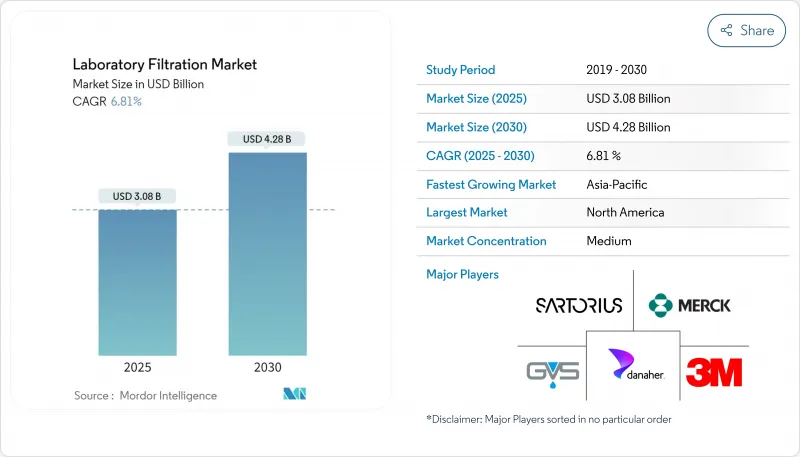

The Laboratory Filtration Market size is estimated at USD 4.70 billion in 2025, and is expected to reach USD 6.91 billion by 2030, at a CAGR of 8.02% during the forecast period (2025-2030).

Rising biopharmaceutical production volumes, rapid adoption of single-use process technologies, and escalating purity requirements in advanced research workflows underpin this expansion. Precision-grade microfiltration continues to anchor routine clarification steps, while breakthrough nanofiltration platforms are gaining traction for molecular-level separations in cell and gene therapy pipelines. Heightened outsourcing to contract research and development manufacturing organizations (CRDMOs) is widening access to flexible filtration assemblies, and sustainability initiatives are accelerating the shift toward PFAS-free membranes. Competitive differentiation now revolves around virus-retentive performance, automation readiness, and digital compatibility, encouraging a steady wave of product upgrades and platform integrations across the laboratory filtration market.

Biologics pipelines are scaling quickly in monoclonal antibodies, recombinant proteins, vaccines, and cell-based therapies. Downstream purification now demands sterile, virus-retentive filters that handle higher titers without compromising biomolecule integrity. Asahi Kasei Medical's Planova FG1 filter, released in October 2024, demonstrates a seven-fold increase in volumetric throughput for antibody processing while preserving virus clearance performance. Strong demand for single-use bag-integrated cartridges further propels the laboratory filtration market as manufacturers build flexible plants capable of rapid product changeovers.

High-throughput sequencing and multiplexed proteomics have condensed sample volumes from milliliters to microliters. Filtration devices compatible with 96- and 384-well plates are now standard in next-generation sequencing (NGS) library preparation and biomarker validation assays. Cytiva's Whatman Mini-UniPrep G2 syringeless filters combine protein precipitation, particulate removal, and autosampler vial integration in one step, cutting plastic use and hands-on time while meeting the precision needs of ultrahigh-performance liquid chromatography (UHPLC). Automation-friendly formats position the laboratory filtration market for sustained uptake in digital, walk-away genomics platforms.

Laboratories under fiscal pressure often attempt to recycle expensive sterilizing-grade membranes, reducing consumable spend by up to 50% but amplifying contamination and validation risks. The burden is acute in small academic labs and resource-limited geographies, where filter integrity testing infrastructure may be lacking.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The laboratory filtration market size for microfiltration amounted to 40.2% of global revenue in 2024, underscoring its ubiquity in microorganism removal and sample clarification tasks. Nanofiltration, however, is on pace to compound at 9.6% annually to 2030 as laboratories adopt molecular-level cutoffs for virus clearance, salt-selective separations, and therapeutic-grade buffer production. The FilmTec LiNE-XD element from DuPont illustrates this shift, achieving high lithium passage while excluding multivalent ions critical to battery-material quality control.

Ultrafiltration and reverse osmosis remain cornerstones for protein concentration and ultrapure water generation respectively. Hybrid membranes combining graphene oxide channels with polymer backbones point toward the next wave of cross-disciplinary breakthroughs. Such innovations blur legacy boundaries, compelling vendors to articulate performance metrics in terms relevant to biotherapeutics, semiconductor rinsing, and environmental testing alike.

The Laboratory Filtration Market Report is Segmented by Technology (Microfiltration, Ultrafiltration, Reverse Osmosis, and More), Product (Filtration Media, Filtration Assemblies, and Filtration Accessories), End User (Pharmaceutical and Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America generated the largest share 36.4% of the laboratory filtration market in 2024 owing to its advanced pharmaceutical R&D, dense biotech clusters, and strict quality regulations. Boston's Kendall Square, the San Francisco Bay Area, and San Diego collectively orchestrate high-throughput biologics discovery pipelines, securing recurring orders for sterilizing-grade media, depth filters, and disposable capsules. Canada's biologics capacity expansion programs and Mexico's cost-competitive fill-finish facilities further elevate regional unit volumes.

Asia-Pacific is the most dynamic arena, advancing at a 10.7% CAGR through 2030. China's provincial life-science parks are outfitting greenfield plants with single-use filtration trains to support mRNA vaccines and gene-edited cell therapies. Singapore's Biomedical Sciences Initiative and South Korea's pharmaceutical stimulus packages intensify local demand for automation-ready filtration units, while Japan sustains premium segments with ultra-high precision membrane grades. India's generics producers reinforce bulk-drug filtration throughput, emphasizing cost-efficient media that maintain compliance with PIC/S harmonization guidelines.

Europe maintains significant weight in the global laboratory filtration market. Germany's engineering heritage fosters steady adoption of advanced membrane modules, and the United Kingdom's cell therapy manufacturing ecosystem drives specialty filter designs optimized for viral vector purification. France, Switzerland, and the Nordic countries extend the region's footprint with strong analytical testing sectors. In South America, Brazil anchors investment in vaccine fill-finish lines, whereas the Middle East & Africa are witnessing incremental gains tied to national immunization and water-quality programs.