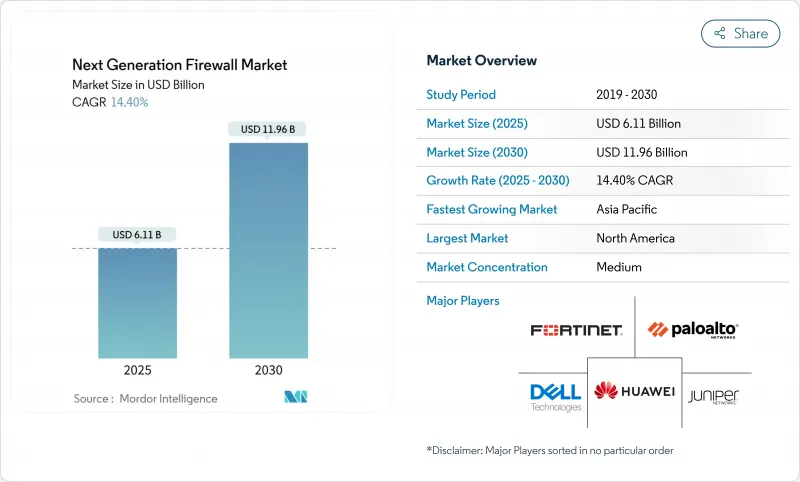

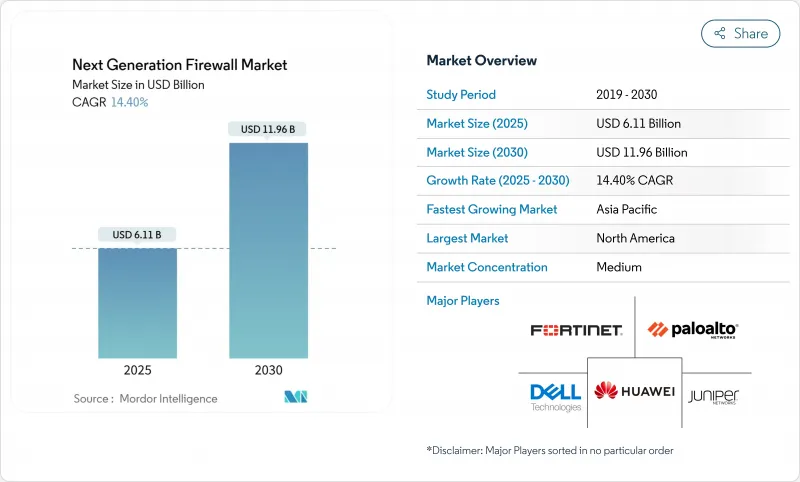

차세대 방화벽 시장의 2025년 시장 규모는 61억 1,000만 달러로, CAGR 14.4%를 나타내 2030년에는 119억 6,000만 달러에 이를 것으로 예상됩니다.

제로 트러스트 아키텍처로의 마이그레이션, 보다 광범위한 클라우드 워크로드 분산 및 오감지를 최대 71%까지 줄이는 임베디드 AI 위협 분석은 채택 확대로 인한 것입니다. 하드웨어 어플라이언스는 여전히 주류이지만 기업이 하이브리드 환경을 위한 소프트웨어 정의 보안을 추구하는 동안 가상 및 클라우드 네이티브 배포가 급속히 확대되고 있습니다. 북미의 매출 점유율은 36%로 톱이지만, 아시아태평양은 각국 정부가 주권 클라우드의 의무화나 지역의 데이터 거주에 관한 법률을 정비하고 있기 때문에 가장 급속하게 확대하고 있습니다. 수요가 집중되고 있는 것은 IT-텔레콤(공유 46%)과 BFSI로, 컴플라이언스 규제의 엄격화와 가치가 높은 디지털 자산에 의해 금융기관은 실시간 위협 대책에 주력하고 있습니다. ASIC 수준의 성능, AI 주도 감지, 통합 정책 관리를 결합할 수 있는 공급업체는 차세대 방화벽 시장에서 새로운 비즈니스 기회를 포착하는 데 이상적입니다.

현재 엔터프라이즈 워크로드의 68%가 퍼블릭, 프라이빗 또는 하이브리드 클라우드에서 실행되고 있으며 기존 방화벽에서는 검사할 수 없는 동서 트래픽이 노출되어 있습니다. 용도를 의식적으로 검사하는 클라우드 네이티브 NGFW는 경계 전용 컨트롤과 비교하여 위협의 평균 감지 시간을 63% 단축하고 보안 인시던트를 47% 줄입니다. 기업의 72%가 2025년에 클라우드 예산을 늘리고 NGFW가 분산 아키텍처의 컨트롤 플레인으로 확고한 지위를 구축하는 동안, 마이크로서비스 전체의 깊은 가시성으로 보안 팀은 통일된 정책을 유지할 수 있습니다.

하이브리드 워크가 항상화됨에 따라 원격 액세스 엔드포인트가 급증하고 현재 42%의 장치가 관리되지 않습니다. 제로 트러스트 네트워크 액세스를 포함한 NGFW는 모든 연결을 검증하고 SonicWALL 클라우드 보안 에지 예약 건수를 전년 대비 54% 증가시켰습니다. 신원 인식 정책은 자격 증명의 무단 사용을 방지하고 2023년 이후 이러한 공격이 37% 증가하고 있음을 해결하며 기업은 기업 네트워크와 홈 네트워크 사이를 이동하는 직원을 보호할 수 있습니다.

고성능 SSL/TLS 디코딩을 통해 공급업체는 맞춤형 실리콘을 요구합니다. 포티넷의 SP5 프로세서는 전력 소비를 크게 줄이면서 방화벽 처리량을 7배 향상시켰지만, 연구 개발 비용이 부족하기 때문에 엔트리 수준의 가격은 높아지고 있으며, 중소기업의 43%는 비용을 가장 큰 장벽으로 삼고 있습니다. ASIC은 에너지 효율을 향상시키지만(FortiGate 70G는 Gbps당 필요한 와트 수가 타사 제품보다 62배 적음) 예산에 제약이 있는 구매자에게 초기 투자는 여전히 큰 부담이 되고 있습니다.

대기업은 2024년 매출의 70%를 차지하고 있어 윤택한 예산으로 암호화된 트래픽을 지연 없이 검사하는 다중 기가비트 어플라이언스를 도입할 수 있었습니다. 대기업은 계속해서 온-어플라이언스 ASIC 가속과 중앙 집중식 정책 오케스트레이션의 조합을 선호합니다. 한편, 중소기업은 자본 장애물을 낮추는 소비 기반의 구독과 매니지드 서비스에 힘입어 2030년까지의 CAGR이 16.3%를 나타낼 것으로 예측했습니다. 유연한 라이선싱 및 턴키 관리를 통해 리소스가 제한된 팀은 복잡성을 아웃소싱하면서 엔터프라이즈급 컨트롤을 얻을 수 있습니다. 그 결과 차세대 방화벽 시장은 세계 다국적 기업을 위한 타협 없는 처리량과 중소기업을 위한 간소화된 서비스 주도 제공이라는 두 가지 다른 가치 제안을 받았습니다.

규제 의무도 지출 패턴을 형성합니다. 대기업은 엄격한 감사 추적에 직면하고 데이터센터, 지점, 자회사에 걸쳐 섬세한 관리를 입증해야합니다. 한편, 중소기업은 SD-WAN, IPS, 제로 트러스트 액세스를 단일 스택으로 통합하고 "도구 난립"을 피하는 통합 플랫폼에 끌려갑니다. 종량제 가상 방화벽의 가용성이 확대됨에 따라 차세대 방화벽 시장은 특히 자본 집약이 우려되는 신흥 경제 국가에서 신규 채용자가 이용하기 쉬운 상황이 계속될 것으로 예측됩니다.

하드웨어 어플라이언스는 On-Premise 데이터센터 내에서 안정적인 성능 특성을 반영하여 2024년에는 55%의 점유율을 유지했습니다. FortiGate 700G와 같은 ASIC을 탑재한 플래그쉽 제품은 업계 평균보다 7배 뛰어난 전력 효율로 164Gbps의 방화벽 처리량을 실현하고 광대역폭의 사업자가 확정적인 대기 시간을 실현하는 물리 디바이스를 계속 선호하는 이유를 명확하게 보여줍니다. 반면에 가상 및 클라우드 기반 제품의 수익 비율은 탄력적인 워크로드 및 인프라스트럭처 애즈 코드의 경제성으로 가속화되고 CAGR 15.4%로 증가하고 있습니다.

클라우드 호스팅 NGFW는 여러 테넌트에 걸친 위협을 상관시키는 중앙 집중식 AI 분석에서 강점을 이끌어냅니다. 버서 네트웍스는 독립 기관의 보안 테스트에서 99.90%의 점수를 받았으며 하드웨어의 기존 기업과 동등하다는 것을 보여줍니다. 엔터프라이즈가 툴체인을 간소화함에 따라 방화벽 기능을 전반적인 SASE 또는 SSE 프레임워크에 통합하는 경우가 늘어나고 가상 제품의 연결 속도가 높아지고 있습니다. 이러한 이중 진화로 차세대 방화벽 시장은 성능에 제약이 있는 데이터센터의 요구와 민첩한 DevOps 파이프라인을 모두 수용할 수 있게 되었습니다.

북미는 2024년 36%의 점유율을 획득해 1위를 유지했습니다. 제로 트러스트 프레임워크의 조기 도입, NIST 가이드라인 등의 컴플라이언스 촉진요인, 유력 벤더의 존재가 높은 지출 심도를 유지하고 있습니다. 미국 금융 서비스 및 의료 기관은 암호화된 트래픽에 대한 상세한 검사와 마이크로세그먼테이션을 선호하고 있으며, 고급 어플라이언스에 대한 수요를 강화하고 있습니다. 중요 인프라를 현대화하는 연방 정부 프로그램은 조달을 더욱 활발하게 만듭니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 16.2%를 나타낼 것으로 예측됩니다. 일본, 인도, 싱가포르의 주권 클라우드 정책과 디지털 서비스 경제의 급성장으로 클라우드 네이티브 방어의 전개가 가속화되고 있습니다. Palo Alto Networks가 최근 Prisma Access Browser를 각 지역의 데이터센터로 확장한 것은 안전한 원격 액세스를 허용하면서 거주 규칙을 충족하기 위한 공급업체의 노력을 보여줍니다. 관리 보안 서비스의 상승은 기술 부족에도 대응하고 있으며, 기업은 대규모 사내 팀이 없는 엔터프라이즈급 NGFW 기능을 도입할 수 있습니다.

GDPR(EU 개인정보보호규정)과 NIS2 지침은 견고한 트래픽 검사와 데이터 처리를 위한 안전 가드를 요구하기 때문에 유럽은 대규모 대응 가능한 기반을 형성하고 있습니다. 곧 시행되는 EU의 AI법은 보안 제품에 대한 책임있는 AI의 통합에 새로운 중점을 두고 벤더가 위협 감지 엔진을 어떻게 배치하는지에 영향을 미칩니다. 수요는 에너지, 수송, 금융시장의 유틸리티과 같은 중요한 인프라 사업자들 사이에서 두드러집니다.

중동 및 아프리카에서는 5G, 스마트시티프로젝트, 전자정부 플랫폼 등의 디지털 변혁이 진행되고 있어 견조한 성장을 보이고 있습니다. 사우디아라비아와 아랍에미리트(UAE)에서는 사이버 보안에 대한 GDP의 배분이 견조하기 때문에 경쟁 입찰이 활발해지고 있으며, 구매자는 포스트 양자암호에 대한 대응과 유연한 소비 모델을 요구하고 있습니다. 차세대 방화벽 시장 규모는 작지만, 이러한 지역은 차세대 방화벽 시장에 다양성을 가져오고 시스템 통합자에게 채널 기회를 제공합니다.

The next generation firewall market is valued at USD 6.11 billion in 2025 and is forecast to climb to USD 11.96 billion by 2030, reflecting a 14.4% CAGR.

Heightened adoption stems from the move to zero-trust architectures, wider cloud workload distribution, and embedded AI-threat analytics that cut false positives by up to 71%. Hardware appliances still dominate, yet virtual and cloud-native deployments are scaling quickly as enterprises pursue software-defined security for hybrid environments. North America leads with a 36% revenue share, while Asia-Pacific is expanding the fastest as governments roll out sovereign-cloud mandates and regional data-residency laws. Demand is concentrated in IT-Telecom (46% share) and BFSI, where stricter compliance regimes and high-value digital assets push institutions toward real-time threat prevention. Vendors able to combine ASIC-level performance, AI-driven detection, and unified policy management are best placed to capture emerging opportunities in the next generation firewall market.

Sixty-eight percent of enterprise workloads now run in public, private, or hybrid clouds, exposing east-west traffic that legacy firewalls cannot inspect. Cloud-native NGFWs equipped with application-aware inspection shorten average threat detection time by 63% and cut security incidents by 47% compared with perimeter-only controls. Deep visibility across microservices lets security teams retain uniform policies as 72% of enterprises boost cloud budgets in 2025, firmly positioning NGFWs as the control plane for distributed architectures.

Remote access endpoints grew sharply when hybrid work became permanent, with 42% of devices now unmanaged. NGFWs that embed zero-trust network access validate every connection and have driven a 54% year-on-year booking increase for SonicWall's Cloud Secure Edge. Identity-aware policies prevent credential abuse, addressing the 37% rise in such attacks since 2023, and equip firms to secure staff who move between corporate and home networks.

High-performance SSL/TLS decryption drives vendors toward custom silicon. Fortinet's SP5 processor gives 7X higher firewall throughput while consuming far less power, yet the research and development outlay keeps entry-level pricing elevated, with 43% of small businesses citing cost as the chief barrier. Although ASICs improve energy efficiency-FortiGate 70G needs 62X fewer watts per Gbps than rivals-the upfront spend remains daunting for budget-constrained buyers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Large enterprises contributed 70% of 2024 revenue as their sizable budgets allowed deployment of multi-gigabit appliances inspecting encrypted traffic without latency. They continue to favor on-appliance ASIC acceleration paired with centralized policy orchestration. In contrast, SMEs are forecast to post a 16.3% CAGR to 2030, propelled by consumption-based subscriptions and managed services that lower capital hurdles. Flexible licensing and turnkey management let resource-limited teams gain enterprise-grade controls while outsourcing complexity. As a result, the next generation firewall market captures two distinct value propositions: uncompromising throughput for global multinationals and simplified, service-led offerings for smaller firms.

Regulatory obligations also shape spending patterns. Larger organizations confront stringent audit trails and must demonstrate granular control across data centers, branches, and subsidiaries. Smaller companies, meanwhile, gravitate toward consolidated platforms that integrate SD-WAN, IPS, and zero-trust access in a single stack, avoiding "tool sprawl." The widening availability of pay-as-you-go virtual firewalls is expected to keep the next generation firewall market accessible to new adopters, especially across developing economies where capital intensity is a concern.

Hardware appliances retained 55% share in 2024, reflecting trusted performance characteristics within on-premises data centers. ASIC-laden flagships such as the FortiGate 700G deliver 164 Gbps firewall throughput at 7X better power efficiency than the industry mean, underscoring why high-bandwidth operators continue to prefer physical devices for deterministic latency. Meanwhile, the portion of revenue from virtual and cloud-based offerings is rising at a 15.4% CAGR, accelerated by elastic workloads and the economics of infrastructure-as-code.

Cloud-hosted NGFWs draw strength from centralized AI analytics that correlate threats across multiple tenants. Versa Networks scored 99.90% in independent security tests, signaling parity with hardware incumbents. As enterprises rationalize toolchains, they increasingly embed firewall functions within holistic SASE or SSE frameworks, boosting attach rates for virtual products. This dual-track evolution ensures the next generation firewall market addresses both performance-bound data-center needs and agile DevOps pipelines.

Next Generation Firewall Market Report is Segmented by Enterprise Size (SMEs and Large Enterprises), Solution Type (Hardware Appliance and Virtual / Cloud-Based), Deployment Mode (On-Premises, Public Cloud, and More), End-User Industry (Banking, Financial Services and Insurance (BFSI), Information Technology (IT) and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America maintained first place with a 36% share in 2024. Early adoption of zero-trust frameworks, compliance drivers such as the NIST guidelines, and the presence of leading vendors sustain high spending depths. Financial services and healthcare institutions in the United States prioritize deep inspection of encrypted traffic and micro-segmentation, reinforcing demand for high-end appliances. Federal programs that modernize critical infrastructure further amplify procurement.

Asia-Pacific is projected to grow at 16.2% CAGR through 2030. Sovereign-cloud policies in Japan, India, and Singapore, together with a surging digital-services economy, accelerate rollouts of cloud-native defenses. Palo Alto Networks' recent expansion of Prisma Access Browser to regional data centers underlines vendor efforts to meet residency rules while enabling secure remote access. The climb in managed security services also addresses skills shortages, allowing enterprises to deploy enterprise-grade NGFW capabilities without large in-house teams.

Europe forms a sizable addressable base as GDPR and the NIS2 Directive require robust traffic inspection and data-handling safeguards. The forthcoming EU AI Act places new emphasis on responsible AI integration within security products, influencing how vendors position threat-detection engines. Demand is notable among critical infrastructure operators in energy, transport, and financial market utilities.

The Middle East and Africa are registering solid growth as national digital-transformation agendas roll out 5G, smart-city projects, and e-government platforms. Robust GDP allocation to cybersecurity in Saudi Arabia and the United Arab Emirates stimulates competitive tenders, with buyers looking for post-quantum cryptography readiness and flexible consumption models. Although starting from a smaller base, these regions add diversity to the next generation firewall market and open channel opportunities for system integrators.