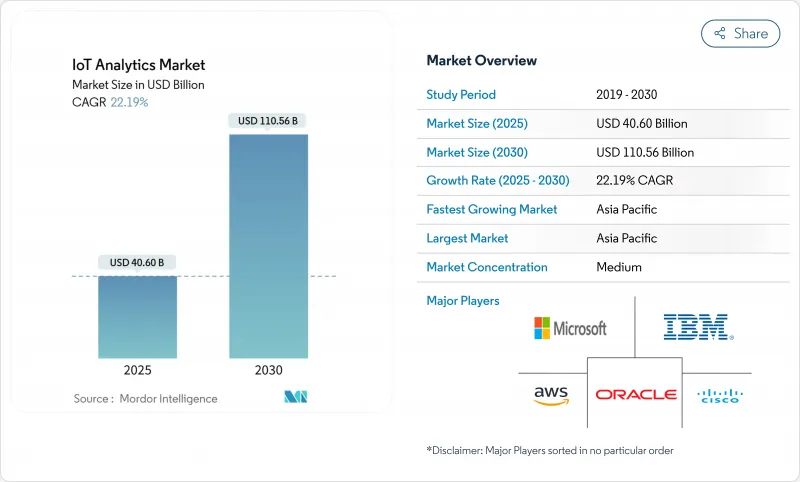

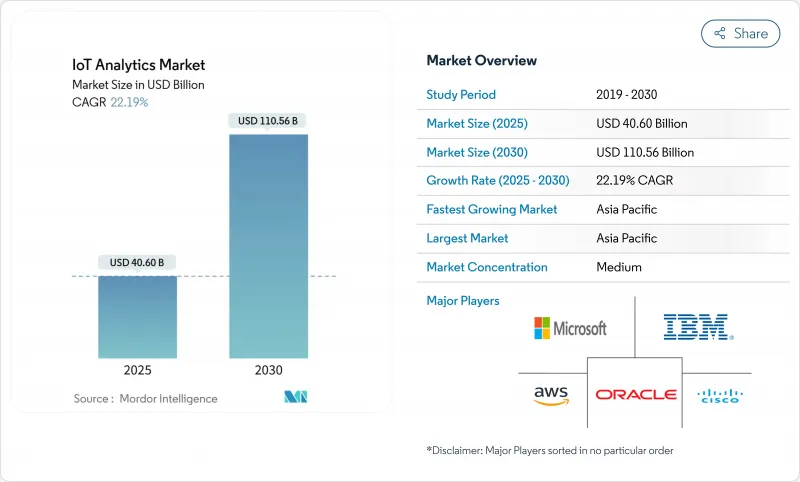

IoT 애널리틱스 시장 규모는 2025년 406억 달러로 추정되고, 2030년 1,105억 6,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 22.2%로 성장할 전망입니다.

장치의 급속한 보급, 엣지와 AI의 융합, 기업의 디지털 변혁 프로그램이 이 확대를 지원하고 있습니다. 기업은 분석 워크로드를 연결된 자산에 접근하여 대기 시간 및 대역폭 비용을 줄이면서 운영 의사 결정을 개선합니다. 자산 집약형 부문에서의 예지보전의 성공 사례와 지속적인 퍼포먼스 감시를 요구하는 지속가능성의 의무화에 의해 수요가 강화되고 있습니다. 클라우드 하이퍼스케일러, 전문 공급업체 및 엣지 플랫폼 제공업체는 생태계의 이점을 보장하기 위해 파트너십과 인수를 활용하여 경쟁이 치열해지고 있습니다.

커넥티드 디바이스의 수는 급격히 증가하고 있으며, 세계 IoT 엔드포인트는 2025년까지 연간 175제타바이트 이상의 데이터를 생성할 것으로 예측됩니다. 플랜트 레벨 센서 어레이는 이미 매일 테라바이트의 데이터를 출력하고 있으며, 기업은 클라우드 백홀 지연을 피하기 위해 엣지에 분석 엔진을 도입할 필요가 있습니다. 이 엣지 퍼스트 모델을 채용하는 제조업체는 클라우드만의 셋업과 비교해, 운영 효율이 30% 향상된 것을 기록하고 있습니다. 데이터 급증은 구조화된 원격 측정, 비정형 비디오 및 로그 파일에 이르기 때문에 다양한 페이로드를 동시에 처리할 수 있는 멀티모달 분석 프레임워크에 대한 투자가 필요합니다.

Microsoft Azure IoT Operations와 같은 확장 가능한 종량 과금 서비스를 통해 기업은 인프라 투자를 최대 60% 절감하면서 매일 수십억 개의 메시지를 캡처할 수 있습니다. 제로 트러스트 아키텍처와 임베디드 위협 분석은 보안 우려를 완화하고 제조 및 물류에서 풀 클라우드 배포를 가속화합니다. 까다로운 산업에서는 클라우드와 로컬 프로세싱의 융합이 진행되고 있지만 공급자가 컴플라이언스 툴킷을 확장하고 있기 때문에 마이그레이션 기세는 여전히 강합니다.

GDPR(EU 개인정보보호규정)은 엄격한 동의, 최소화 및 현지화 규칙을 부과하며 규정 준수 위반은 세계 판매의 4%에 해당합니다. 각 국가의 법률이 다르기 때문에 기업은 여러 지역의 데이터스토어를 유지해야 하며 프로젝트 예산이 최대 25%까지 증가합니다. 국경을 넘는 실시간 분석은 주권 관련 규정을 충족하기 위해 정책을 의식한 라우팅을 통합해야 하며 기업 전개를 지연시킵니다.

솔루션이 계속 우세하며 2024년 매출의 68.7%를 차지했습니다. IoT 애널리틱스에서는 솔루션 시장 규모가 꾸준히 확대될 것으로 예상되지만 기업이 관리하는 전문 지식을 추구하고 있기 때문에 서비스 카테고리의 CAGR은 24.0%로 빠르게 확대될 것으로 예측됩니다. 전문 서비스는 프로토콜 매핑, 엣지 스택 튜닝, 멀티클라우드 통합에 대한 수요가 높습니다.

인력 부족 및 아키텍처의 복잡화로 인해 외부 파트너는 매력적인 존재가 되었습니다. 매니지드 서비스 계약은 종종 소프트웨어, 인프라 및 성과 기반 SLA를 번들로 제공하고 위험을 공급자에게 전가합니다. 보안 애널리틱스의 하위 부문은 연결된 장치와 관련된 공격 대상의 확장으로 인해 호조입니다.

2024년 온프레미스 설치 점유율은 65.4%로, 이는 제어, 지연 및 규제 요구를 반영합니다. 그러나 클라우드 인스턴스는 하이퍼스케일러가 인제스트 파이프라인과 서버리스 분석 엔진을 결합하여 CAGR 24.1%로 성장하고 있습니다. 하이브리드 디자인은 시간에 중요한 워크로드를 엣지 노드로 라우팅하는 반면 배치 AI용으로 집계된 데이터를 클라우드로 전송합니다.

Microsoft와 아마존은 컴포저블 제품으로 선도하고 있으며, 기업은 디지털 트윈과 대규모 모델 교육을 몇 분 안에 시작할 수 있습니다. 공급망 불안정성 및 에너지 가격 변동은 탄력적인 컴퓨팅의 필요성을 강조하고 클라우드 사용을 더욱 촉진하고 있습니다.

IoT 애널리틱스 시장 보고서는 컴포넌트별(솔루션 및 서비스), 전개별(온프레미스 및 클라우드), 조직 규모별(대기업 및 중소기업(SME)), 용도별(예지보전, 자산 성능 관리, 에너지 관리 등), 최종 사용자 산업별(제조, 에너지 및 유틸리티, 운송 및 물류, 소매 및 전자상거래 등), 지역별로 분류됩니다.

아시아태평양은 2024년 매출의 35.6%를 차지했으며, '메이드 인 차이나 2025'와 인도의 스마트 시티 미션 등 정부 프로그램의 혜택을 누리고 있습니다. 이 지역의 CAGR은 23.2%로, 산업의 디지털화, 5G의 전개, 엣지 AI의 시험적 도입의 규모를 뒷받침하고 있습니다. 중국 공장에서는 비전 기반의 품질 관리가 도입되고 인도의 지자체에서는 폐기물 및 교통 관리에 센서 네트워크가 활용되고 있습니다.

북미는 성숙한 클라우드 인프라와 조기 AI 도입으로 약간의 차이로 이어집니다. 벤처 기업의 자금 조달과 대학의 연구 파이프라인이 뒷받침되고, 기업은 스트리밍 분석을 디지털 운영 센터와 통합하고 있습니다. 이 지역은 자율적 인 이동성과 정밀 농업 프로젝트의 테스트 베드입니다.

유럽에서는 ESG 컴플라이언스를 기반으로 한 실시간 배출 모니터링이 견고한 성장을 보입니다. 유럽의 그린 딜 구상은 전력회사나 제조업체를 데이터 주도의 효율화로 향하게 합니다. 라틴아메리카와 중동의 신흥 시장은 통신사업자가 NB-IoT와 5G의 커버리지를 확대하여 물류, 석유, 공공안전에 있어 그린필드 전개를 가능하게 함으로써 기세를 늘리고 있습니다.

The IoT analytics market size is USD 40.60 billion in 2025 and is forecast to reach USD 110.56 billion in 2030, registering a 22.2% CAGR over the period.

Rapid device proliferation, edge-AI convergence, and enterprise digital-transformation programs underpin this expansion. Enterprises are moving analytic workloads closer to connected assets, reducing latency and bandwidth costs while improving operational decisions. Demand is reinforced by predictive-maintenance success stories in asset-intensive sectors and by sustainability mandates that call for continuous performance monitoring. Competitive intensity is strengthening as cloud hyperscalers, specialist vendors, and edge-platform providers leverage partnerships and acquisitions to secure ecosystem advantages.

Connected-device counts are rising sharply, with global IoT endpoints expected to produce more than 175 zettabytes of data annually by 2025. Plant-level sensor arrays already emit terabytes each day, forcing enterprises to deploy analytics engines at the edge to avoid cloud-backhaul delays. Manufacturers adopting this edge-first model record 30% higher operational efficiency versus cloud-only setups. The data surge spans structured telemetry, unstructured video, and log files, prompting investment in multimodal analytic frameworks that can handle diverse payloads concurrently.

Scalable, pay-as-you-go services such as Microsoft Azure IoT Operations allow firms to ingest billions of daily messages while cutting infrastructure outlays by up to 60%. Zero-trust architectures and built-in threat analytics lessen security concerns, accelerating full-cloud adoption in manufacturing and logistics. Highly regulated verticals continue to blend cloud and local processing, but migration momentum remains strong as providers extend compliance toolkits.

GDPR imposes stringent consent, minimization, and localization rules; non-compliance can cost 4% of global turnover. Divergent national laws force firms to maintain multiple regional data stores, inflating project budgets by up to 25%. Real-time analytics crossing borders must incorporate policy-aware routing to satisfy sovereignty mandates, slowing enterprise rollouts.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions continued to dominate, accounting for 68.7% revenue in 2024. The IoT analytics market size for solutions is forecast to increase steadily, yet the services category is set to expand faster at 24.0% CAGR as firms seek managed expertise. Professional services are in high demand for protocol mapping, edge-stack tuning, and multi-cloud integration.

The talent shortfall and rising architectural complexity make external partners attractive. Managed-service contracts often bundle software, infrastructure, and outcome-based SLAs, shifting risk to providers. Security-analytics sub-segments are buoyed by expanding attack surfaces tied to connected devices.

On-premise installations held 65.4% share in 2024, reflecting control, latency, and regulatory needs. Yet cloud instances are growing at 24.1% CAGR as hyperscalers couple ingestion pipelines with serverless analytic engines. Hybrid designs route time-critical workloads to edge nodes while sending aggregated data to the cloud for batch AI.

Microsoft and Amazon lead with composable offerings, enabling enterprises to spin up digital twins and large-scale model training within minutes. Supply-chain volatility and energy-price swings underline the need for elastic compute, further pushing cloud uptake.

The IoT Analytics Market Report is Segmented by Component (Solutions and Services), Deployment (On-Premise and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), Application (Predictive Maintenance, Asset Performance Management, Energy Management, and More), End-User Industry (Manufacturing, Energy and Utilities, Transportation and Logistics, Retail and E-Commerce, and More), and Geography.

Asia-Pacific delivered 35.6% of 2024 revenue, benefiting from government programs such as "Made in China 2025" and India's Smart Cities Mission. Regional CAGR of 23.2% underscores the scale of industrial digitization, 5G rollout, and edge-AI pilots. Chinese factories deploy vision-based quality control, while Indian municipalities apply sensor networks to manage waste and traffic.

North America follows closely, with mature cloud infrastructure and early AI adoption. Enterprises integrate streaming analytics with digital-operations centers, aided by robust venture funding and university research pipelines. The region remains a test-bed for autonomous-mobility and precision-agriculture projects.

Europe posts steady growth as ESG compliance drives real-time emissions monitoring. Initiatives under the European Green Deal push utilities and manufacturers toward data-driven efficiency. Emerging markets in Latin America and the Middle East gain momentum as telecom operators extend NB-IoT and 5G coverage, enabling greenfield deployments in logistics, oil, and public safety.