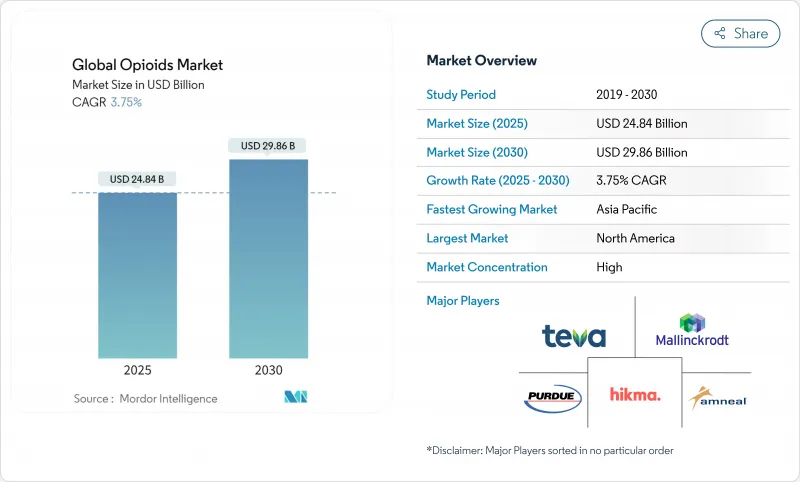

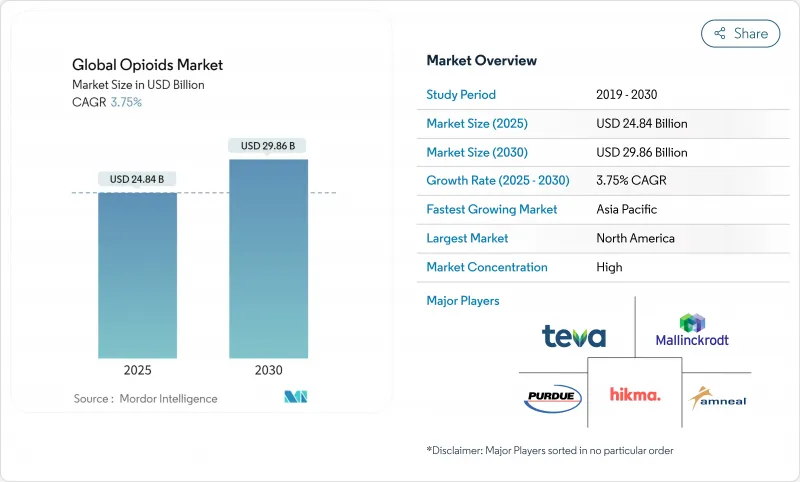

오피오이드 시장은 2025년에 248억 4,000만 달러로 평가되었고, 2030년에 298억 6,000만 달러에 이를 것으로 예측되며, CAGR은 3.75%를 나타낼 전망입니다.

오피오이드 시장의 꾸준한 확대는 강력한 진통제에 대한 지속적인 임상적 필요성과 불법 유통 및 오남용을 억제하기 위한 엄격한 글로벌 통제 사이의 신중한 균형을 반영합니다. 수요는 수술, 종양학 및 중증 만성 통증 분야에서 견인되고 있으나, 생산 할당량 축소, 강화된 처방 모니터링, 대체 요법의 증가하는 가용성으로 인해 성장은 제한되고 있습니다. 전 세계적으로 병원이 여전히 오피오이드 소비의 대부분을 차지하고 있으나, 주사용 모르핀, 하이드로모르폰 및 펜타닐의 부족으로 인해 의료 제공자들은 공급을 배분하고 다중 모드 요법을 채택해야 하는 상황입니다. 제품 혁신은 남용 방지 제형과 수제트리진(NaV1.8 억제제로 2025년 FDA 승인 획득)과 같은 최초의 비오피오이드 진통제로 전환되고 있으며, 이는 첨단 통증 치료 옵션의 다양화 추세를 보여줍니다. 한편, 정확한 오피오이드 투여량을 안내하는 디지털 치료제는 평균 처방량을 감소시키고 데이터 기반 관리 프로그램에 대한 보험사 선호도를 강화하고 있습니다.

인구 고령화, 비만, 좌식 생활 방식은 골관절염 및 척추 질환 발생률을 높여 오피오이드 시장 내 수요를 유지하고 있습니다. 5천만 명 이상의 미국 성인이 만성 통증을 겪고 있으며, 비약물적 치료가 실패할 경우 오피오이드는 돌발성 통증 완화에 여전히 필수적입니다. 정교한 치료 경로는 이제 오피오이드와 보조 물리치료 및 인지 지원을 병행하지만, 처방집 제한과 단계적 치료 의무화로 인해 치료 시작 시기가 지연되고 있습니다. 부작용 최소화 압박으로 시판 후 감시가 강화되며, 변조 방지 포장 및 비정상 처방을 경고하는 분석 대시보드에 대한 투자가 촉진되고 있습니다. 그 결과, 실제 안전성 혜택을 입증할 수 있는 제조사들은 오피오이드 시장 전반에서 우대적 보험급여와 높은 처방약 등급 배정을 유지하고 있습니다.

임상 의사들은 혈장 농도 안정화와 야간 돌발 통증 감소를 위해 1일 1회 또는 2회 복용 서방형 정제를 점점 더 선택하고 있습니다. FDA의 진화하는 ADF(약물 방출 장치) 승인 경로는 분쇄 및 주사 남용을 방지하는 미세구체 기술을 적용한 엑스탐자 ER(Xtampza ER)과 같은 제품의 승인을 가속화했습니다. 서방형 제품은 프리미엄 가격을 형성하여 처방량 정체에도 불구하고 단위 매출을 끌어올리고 있습니다. 그러나 복잡한 제조 공정과 엄격한 남용 시뮬레이션 연구는 신규 진입을 제한하고 자본 요건을 높여 오피오이드 시장 내 기존 업체들의 경쟁적 위치를 강화하고 있습니다.

미국 39개 주와 점점 더 많은 유럽 관할 구역에서 시행 중인 의료용 마리화나 법안은 대체 효과를 발생시켜 메디케이드 환자 대상 스케줄 III 오피오이드 처방을 거의 30% 감소시켰습니다. 무작위 대조 시험에 따르면, 특히 저효능 요법의 경우 대마초를 오피오이드와 병용할 때 모르핀 밀리그램 환산량이 39.3% 감소하는 것으로 보고되었습니다. 그럼에도 대마초는 복잡한 수술에 필요한 고효능 오피오이드를 완전히 대체하지 못하므로, 그 영향은 전문 병원보다 일차 진료에서 더 두드러집니다. 이러한 추세는 전체 처방량 증가를 억제하지만, 제조사들이 오피오이드 시장의 고난도 틈새 시장을 공략하도록 장려합니다.

옥시코돈은 2024년 오피오이드 시장 점유율 32.17%를 차지했으며, 이는 급성 및 만성 적응증의 광범위한 스펙트럼을 커버하는 즉시 방출형 및 지속 방출형 제형에 대한 의사의 지속적인 선호도를 반영합니다. 생체이용률 프로파일, 예측 가능한 대사 과정, 수십 년간의 임상 경험은 DEA 할당량 삭감 및 제조 중단으로 공급이 주기적으로 제한되더라도 높은 처방전 침투율을 유지하는 데 기여합니다. 알보젠(Alvogen), 암닐(Amneal), 캠버(Camber) 등 다수 공급업체가 공급 부족을 보고함에 따라 병원 구매팀은 조달 네트워크를 확대하고 치료 연속성을 유지하기 위해 노력하고 있습니다. 4.16% 점유율을 차지하는 메타돈은 여전히 오피오이드 대체 치료의 핵심으로, 긴 혈장 반감기로 인해 금단 위험이 낮아 치료 프로그램 내에서 매일 관찰 투여가 가능합니다.

모르핀과 하이드로코돈의 변동성은 지속되고 있습니다. 하이드로코돈 생산 할당량이 2015년 이후 73% 감소했으며, 모르핀은 제조 캠페인 지연 시 부족 현상이 발생하기 때문입니다. 메페리딘은 신경독성 대사산물 우려로 사용이 계속 감소하는 반면, 옥시모르폰 같은 틈새 약제는 지속적인 공급 공백에 직면해 있습니다. 억제책 강화와 공급망 관리 강화가 결합되면서 오피오이드 시장 내 경쟁 계층이 재편되고 있습니다.

강력 작용제는 2024년 오피오이드 시장 점유율 50.71%를 차지하며 중증 수술 후 종양학 및 외상 치료에서의 역할을 공고히 했습니다. 완전한 μ-수용체 활성화로 타의 추종을 불허하는 효능을 제공하지만, 위험 완화를 위해 지속적인 산소 포화도 모니터링과 가속화된 감량 프로토콜이 필요합니다. 부분 작용제, 특히 4.51% 점유율을 기록한 부프레노르핀은 사전 대면 진료 없이 전자 처방이 허용되는 원격의료 규정 완화로 계속해서 시장 점유율을 확대하고 있습니다. 이러한 유연성은 치료 프로그램 참여율을 높이고 전문 제조사들의 수익을 안정화시킵니다.

오피오이드 산업은 중추신경계 침투를 최소화하여 호흡억제를 줄이면서도 진통 효과를 유지하는 말초 선택적 분자 개발에 연구개발(R&D)을 집중하고 있습니다. 날록손과 같은 길항제는 응급의료 서비스 전반에서 여전히 필수적인 보조제로 활용되며, 작용성과 내포체 편향성을 결합한 새로운 이중작용 분자들이 2상 임상시험에 진입 중입니다. 규제 감독이 강화됨에 따라 수용체 결합 선택성은 오피오이드 시장에서 차별화 전략과 가치 창출을 점차 결정짓는 요소가 될 것입니다.

북미는 2024년에도 42.91%라는 압도적인 오피오이드 시장 점유율을 유지했으며, 이는 선진적인 수술 역량, 포괄적인 보험 적용 범위, 그리고 고강도 치료를 위한 강력 작용제에 대한 지속적인 의존에 기반을 두고 있습니다. DEA 생산 할당량 감소(2015년 이후 옥시코돈 68%, 하이드로코돈 73%)로 공급이 위축되었지만 수요는 꺾이지 않아, 조사 대상 통증 환자의 90%가 접근성 어려움을 보고했습니다. 미국 의료 네트워크는 처방 관리 강화로 대응하여 수술 후 신규 처방 시작을 3.5% 감소시키고 정제 수를 41.8% 줄였으나, ADF 제품이 처방 목록 점유율을 확대하며 가격-혼합 효과 상승으로 해당 지역 오피오이드 시장 규모는 여전히 증가했습니다. 캐나다의 중앙 집중식 모니터링 시스템은 불법 유통을 낮게 유지하는 반면, 멕시코는 완제 의약품의 경유지 역할과 국내 수요 사이에서 균형을 맞추고 있습니다.

유럽은 두 번째로 큰 지역 시장을 형성하며, 강력한 제조 역량과 견고한 통증 관리 인프라를 바탕으로 합니다. 독일, 프랑스, 영국은 ADF 조달을 우선시하는 반면, 이탈리아와 스페인은 돌발성 통증 발작 시에만 오피오이드를 사용하는 다중 모드 요법에 점점 더 의존하고 있습니다. 유럽 마약 및 약물 중독 모니터링 센터는 니타제네스 같은 합성 오피오이드 위협에 대한 대응 프로토콜을 조정하며 국가 처방 지침 수립에 기여합니다. 브렉시트 관련 관세 검사는 절차적 마찰을 초래했으나, 상호인정협정의 지속으로 영국 해협을 가로지르는 안정적인 의약품 유통이 유지되며 전체 오피오이드 시장 성장은 훼손되지 않았습니다.

아시아태평양 지역은 2024년 오피오이드 시장 점유율 5.43%로 가장 빠르게 성장하는 지역이며, 2030년까지 연평균 5.9% 성장률을 기록할 것으로 전망됩니다. 일본의 초고령화 인구 구조는 경피 및 경구 서방형 제제에 대한 꾸준한 수요를 창출하는 반면, 호주는 의사 쇼핑(의사 쇼핑)을 억제하기 위해 실시간 처방 모니터링 시스템을 개선 중입니다. 중국이 2024년 7월 덱스트로메토르판을 제2류 향정신성 의약품으로 재분류한 것은 통제 물질 규제의 전반적 강화 추세를 반영하지만, 암 및 외상 센터의 중증 통증 프로토콜은 유지됩니다. 인도는 제조국이자 소비국이라는 이중적 위치 덕분에 수출 확대의 혜택을 누릴 수 있으나, 국내 당국은 환자 접근성과 불법 유출 위험 사이의 균형을 맞추기 위해 고심 중입니다. 인도네시아, 태국, 베트남의 수술 역량 증가는 지역 내 수요를 더욱 끌어올려 오피오이드 시장의 장기적 성장 전망을 공동으로 강화하고 있습니다.

The opioids market generated USD 24.84 billion in revenue in 2025 and is forecast to reach USD 29.86 billion by 2030, advancing at a 3.75% CAGR.

The steady expansion of the opioids market reflects a careful equilibrium between persistent clinical need for potent analgesics and strict global controls aimed at curbing diversion and misuse. Demand is anchored in surgical, oncology, and severe chronic pain settings, yet growth is tempered by production-quota cuts, heightened prescription monitoring, and the rising availability of substitute therapies. Hospitals worldwide continue to account for the bulk of opioid consumption, although shortages of injectable morphine, hydromorphone, and fentanyl force providers to ration supply and adopt multimodal regimens. Product innovation is pivoting toward abuse-deterrent formulations and toward first-in-class non-opioid analgesics such as suzetrigine, a NaV1.8 inhibitor that secured FDA approval in 2025, illustrating a parallel trend toward diversification of advanced pain option. Meanwhile, digital therapeutics that guide precise opioid dosing are lowering average prescription sizes and reinforcing payers' preference for data-driven stewardship programs.

Population aging, obesity, and sedentary lifestyles are elevating rates of osteoarthritis and back disorders, sustaining demand within the opioids market. More than 50 million U.S. adults live with chronic pain, and opioids remain critical for breakthrough pain when non-pharmacological measures fail. Sophisticated care pathways now pair opioids with adjunctive physiotherapy and cognitive support, yet formulary restrictions and step-therapy mandates prolong time to therapy initiation. Pressure to minimize adverse events is intensifying post-marketing surveillance, spurring investment in tamper-resistant packaging and analytic dashboards that flag aberrant prescribing. As a result, manufacturers that can demonstrate real-world safety benefits are securing preferential reimbursement and sustaining high formulary tier placement across the opioids market.

Clinicians increasingly choose once- or twice-daily extended-release tablets to stabilize plasma concentrations and reduce nocturnal breakthrough pain. The FDA's evolving ADF pathway has accelerated approvals such as Xtampza ER, which employs microsphere technology to thwart crushing and injection abuse. Extended-release products command premium pricing, lifting unit revenues despite flat prescription volumes. Complex manufacturing processes and rigorous abuse-simulation studies, however, restrict new entrants and create elevated capital requirements, reinforcing the competitive positions of incumbents within the opioids market.

Medical-marijuana legislation in 39 U.S. states and a growing number of European jurisdictions is producing substitution effects, cutting Schedule III opioid prescriptions among Medicaid patients by nearly 30%. Randomized trials report 39.3% reductions in morphine-milligram equivalents when cannabis is combined with opioids, especially for low-potency regimens. Nevertheless, cannabis does not fully replace high-potency opioids required for complex surgery, so its impact is more pronounced in primary care than in specialty hospitals. The trend restrains overall volume growth yet encourages manufacturers to target high-acuity niches in the opioids market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Oxycodone secured 32.17% opioids market share in 2024, reflecting sustained physician preference for both immediate-release and extended-release formats that cover a wide spectrum of acute and chronic indications. Its bioavailability profile, predictable metabolism, and decades of clinical experience reinforce high formulary penetration even as DEA quota cuts and manufacturing outages periodically constrain supply. Multiple suppliers-Alvogen, Amneal, Camber-have reported shortages, prompting hospital purchasing teams to widen sourcing networks and preserve continuity of care. Methadone, with 4.16% share, remains a cornerstone of opioid-substitution treatment; long plasma half-life lowers withdrawal risk, supporting daily observed dosing within treatment programs.

Volatility persists for morphine and hydrocodone because hydrocodone production quotas have fallen 73% since 2015, and morphine shortages arise when manufacturing campaigns are delayed. Meperidine's use continues to erode due to neurotoxic metabolite concerns, while niche agents such as oxymorphone face sustained supply gaps. The emphasis on deterrence, combined with supply-chain diligence, is reshaping competitive tiers within the opioids market.

Strong agonists captured 50.71% opioids market share in 2024, underpinning their role in severe postoperative oncology and trauma care. Their full μ-receptor activation delivers unmatched potency, although risk mitigation requires continuous oxygen saturation monitoring and accelerated tapering protocols. Partial agonists, notably buprenorphine at 4.51% share, continue to expand under relaxation of telemedicine rules permitting e-prescribing without prior in-person visits . This flexibility boosts treatment-program enrollment and stabilizes revenue for specialized manufacturers.

The opioids industry is channeling R&D toward peripheral-selective molecules that minimize central nervous system penetration, thereby maintaining analgesia with reduced respiratory depression. Antagonists such as naloxone remain vital adjuncts across emergency medical services, and novel dual-action molecules that combine agonism with endocytic bias are entering Phase II trials. As regulatory scrutiny tightens, receptor-binding selectivity will increasingly define differentiation strategies and value capture in the opioids market.

The Opioids Market Report Segments the Industry Into by Product Type (Codeine, Fentanyl, Meperidine, and More), by Receptor Binding (Strong Agonist, Mild To Moderate Agonist, and More), by Route of Administration (Oral, Parenteral, and More), by Application (Pain Management, Cold and Cough, and More), by Distribution Channel (Hospital, and More) and by Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America sustained a commanding 42.91% opioids market share in 2024, anchored by advanced surgical capacity, comprehensive insurance coverage, and continued reliance on potent analgesics for high-acuity care. DEA production-quota reductions-68% for oxycodone and 73% for hydrocodone since 2015-tightened supply but did not derail demand, prompting 90% of surveyed pain patients to report access difficulties. U.S. health networks responded with prescription stewardship that cut new postoperative starts by 3.5% and trimmed tablet counts by 41.8%, yet the opioids market size for the region still rose on price-mix uplift as ADF products captured greater formulary share. Canada's centralized monitoring system keeps diversion low, while Mexico balances domestic need with its role as a transit corridor for finished pharmaceuticals.

Europe forms the second-largest regional pool, supported by deep manufacturing capabilities and robust pain-care infrastructure. Germany, France, and the U.K. prioritize ADF procurement, while Italy and Spain increasingly rely on multimodal regimens that reserve opioids for breakthrough episodes. The European Monitoring Centre for Drugs and Drug Addiction coordinates response protocols for synthetic opioid threats such as nitazenes, informing national prescribing guidelines . Brexit-linked customs checks introduced procedural frictions, yet continued mutual-recognition agreements uphold stable medicine flow across the Channel, keeping overall opioids market growth intact.

Asia-Pacific, with 5.43% opioids market share in 2024, is the fastest-advancing geography and is projected to post 5.9% CAGR through 2030. Japan's super-aged demographic drives steady demand for transdermal and oral controlled-release formulations, while Australia refines its real-time prescription-monitoring system to curb doctor shopping. China's reclassification of dextromethorphan to Category II Psychotropic Drugs in July 2024 underscores a broader tightening of controlled-substance rules, though severe-pain protocols remain intact for oncology and trauma centers. India's dual role as manufacturer and consumer positions it to benefit from export expansion even as domestic authorities grapple with balancing patient access against diversion risks. Growing surgical capacity across Indonesia, Thailand, and Vietnam further elevates regional volume, collectively reinforcing long-term growth prospects for the opioids market.