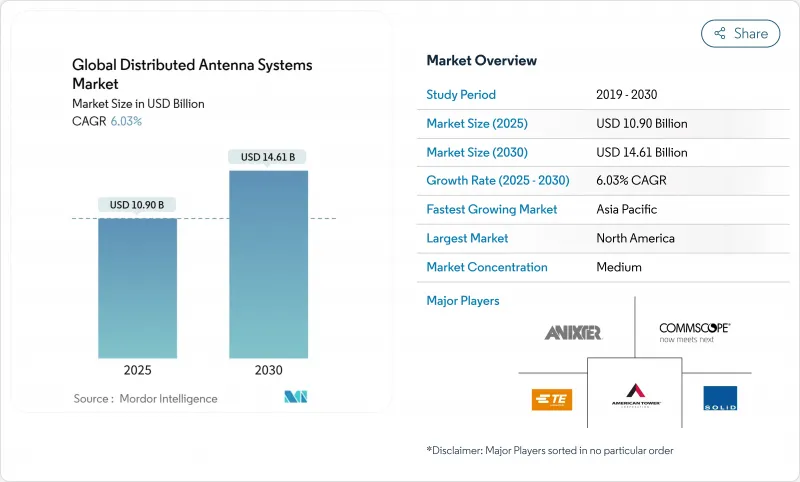

세계의 분산 안테나 시스템 시장 규모는 2025년에 109억 달러, 2030년에는 146억 1,000만 달러에 이르고, 예측 기간(2025-2030년)의 CAGR은 6.03%를 나타낼 전망입니다.

분산 안테나 시스템 시장 규모는 2025년에 109억 달러, 2030년에는 146억 1,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR은 6.03%를 나타낼 전망입니다. 5G의 고밀도화로 실내 커버리지 갭이 드러나는 반면, 중립 호스트의 비즈니스 모델은 회장 소유자의 자본 부담을 줄여 수요가 가속화되고 있습니다. 패시브 아키텍처는 계속해서 비용에 중점을 둔 배치를 지배하고 있으며, 공공 안전 무선의 커버리지에 관한 규제의 의무화에 의해 경기 변동시에도 지출 사이클은 회복력을 유지하고 있습니다. 인공지능 기반의 자체 최적화 네트워크는 운영 비용을 줄이기 시작했으며, 디지털 DAS 설계는 에너지 소비를 줄이고 기업의 지속가능성 목표를 높이고 있습니다.

모바일 데이터 사용 패턴은 트래픽의 80% 이상이 실내에서 발생하는 것으로 확인되었지만 대용량 5G 셀을 구동하는 동일한 미드밴드 및 mm 파 신호가 건물 내에서 빠르게 감쇠합니다. Verizon과 같은 통신 사업자는 서비스 품질을 유지하기 위해 고정 무선 서비스와 mm 파 DAS 배포를 결합합니다. 회장의 소유자는 현재 부동산 평가와 실내 연결 보증을 연결하고 있으며 비용에 민감한 상업용 부동산 분야에서도 투자 결정을 내리고 있습니다.

국제소방법을 모델로 한 건축기준에서는 시설 전체에서 95%, 계단 붐비는 등 중요한 존에서는 99%의 신호 커버리지가 의무화되어 있어 공공안전DAS에 대한 비재량적인 수요가 탄생하고 있습니다. 전국 방화협회(National Fire Protection Association)의 규칙에 따라 연례 재인증은 수익원에 정기적인 서비스 계층을 추가합니다. 공공 안전 DAS는 병원과 교통 허브에도 의무화되어 옵션 편의 시설이 아닌 기본 건물 인프라가되고 있습니다.

4개 이상의 모바일 네트워크 사업자를 만족시켜야 하는 배치는 설계, 신호원, 주파수 클리어런스에 대해 관계자가 조정하는 동안 6-12개월간 정체될 가능성이 있습니다. 디지털 DAS 플랫폼은 소프트웨어 정의의 유연성을 제공함으로써 이러한 부담을 줄일 수 있지만, 엔드 투 엔드 솔루션을 중재하는 중립 호스트 통합자는 부동산 소유자를 대신하여 복잡성을 흡수하여 롤아웃을 가속화합니다.

2024년 분산 안테나 시스템 시장 점유율은 패시브 아키텍처가 63%를 차지하고 설치 비용이 낮고 유지보수의 간편성을 우선시하는 중규모 장소의 소유자에게 호소하고 있습니다. 이 시스템은 동축 케이블과 스플리터를 통해 RF를 라우팅하므로 대규모 액티브 전자 제품이 필요 없으므로 필요한 전력을 줄일 수 있습니다. 파이버 백홀과 패시브 디스트리뷰션을 결합한 하이브리드 DAS는 호스피탈리티 시설과 아카데믹 캠퍼스에서 성능과 예산 제약의 균형을 맞추기 위해 CAGR 9.06%를 보일 것으로 예측됩니다. 액티브 DAS는 종합적인 커버리지와 대용량이 비용 우려를 뛰어넘는 대규모 경기장과 공항에서 그 역할을 유지하는 반면 디지털 DAS는 향후 멀티 오퍼레이터를 지원하는 소프트웨어 정의의 유연성과 지지를 모으고 있습니다.

수렴하는 기술 로드맵은 카테고리 간의 역사적인 경계를 모호하게 만듭니다. Corning의 Everon 5G Enterprise Radio Access Network는 스몰셀 라디오와 DAS 헤드 엔드를 통합하여 기존 시스템에 비해 설치 시간을 75%, 소유 비용을 50% 절감합니다. 공급업체는 에너지 절약과 모듈식 확장성을 강조하고 있으며 차세대 플랫폼은 구매자를 고정된 토폴로지에 고정하지 않고도 성능과 지속가능성 요구 사항을 모두 충족하는 것으로 자리잡고 있습니다.

2024년 분산 안테나 시스템 시장 점유율은 북미가 39%로 선두에 올랐습니다. 국제 소방법(International Fire Code)과 미국 화재 협회(National Fire Protection Association)의 표준에 내장된 요구사항은 거시경제 주기에 관계없이 강제적인 수요를 발생시킵니다. 미국의 통신 사업자는 매크로의 고밀도화를 보완하기 위해 mm파의 스몰셀과 DAS에 크게 기여하고 있으며, 부동산 소유자는 커버리지를 향상시키면서 초기 비용을 억제할 수 있는 중립 호스트 플랫폼을 점점 선호하고 있습니다.

유럽에서는 건축 기준법의 개정과 지속가능성 목표에 대응하기 위해 오래된 오피스 빌딩의 개수가 진행되고 있으며, 꾸준한 갱신 수요를 볼 수 있습니다. 영국과 독일에서는 여러 사업자의 협상이 복잡해진 초기 사례가 있어 도입 스케줄이 장기화하는 경우가 많지만, 승인을 합리화할 수 있는 통합자에게는 비옥한 토양이 되고 있습니다. 한편 프랑스와 스페인에서는 정부가 뒷받침하는 광대역 정책을 통해 디지털 인프라에 보조금을 돌려주고 교통요소와 헬스케어 캠퍼스에서 관민 DAS 파트너십의 길을 열고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 9.37%로 가장 급성장하고 있는 지역으로, 중국의 진행 중인 도시화, 일본의 고밀도 교통 시스템, 인도의 고급 상업 부동산에 대한 캐치업 투자가 뒷받침하고 있습니다. 중국의 배치는 DAS와 IoT 센서의 백본을 융합시키는 스마트 시티 프로젝트와 일치하며, 일본의 사업자는 대규모 스포츠 행사를 앞두고 지하철역과 복합 상업시설에서의 원활한 연결을 우선하고 있습니다. 일본의 로컬 5G 및 인도 전용 LTE 라이선스와 같은 스펙트럼 공유 메커니즘은 지역 전체에서 비용 최적화된 실내 커버리지 모델로의 광범위한 이동을 반영하여 중립 호스트 실험을 위한 규제 활주로를 제공합니다.

The Global Distributed Antenna Systems Market size is estimated at USD 10.90 billion in 2025, and is expected to reach USD 14.61 billion by 2030, at a CAGR of 6.03% during the forecast period (2025-2030).

The distributed antenna systems market size stands at USD 10.90 billion in 2025 and is forecast to reach USD 14.61 billion by 2030, reflecting a 6.03% CAGR over the period. Demand is accelerating as 5G densification exposes indoor coverage gaps, while neutral-host business models ease capital burdens for venue owners. Passive architecture continues to dominate cost-sensitive deployments, and regulatory mandates for public-safety radio coverage keep the spending cycle resilient during economic swings. Artificial-intelligence-based self-optimizing networks are beginning to trim operating costs, and digital DAS designs are tempering energy draw, aligning deployments with rising corporate sustainability goals.

Mobile data-use patterns confirm that more than 80% of traffic originates indoors, yet the same mid-band and millimeter-wave signals powering high-capacity 5G cells attenuate quickly inside buildings. These physics trigger urgent demand for in-building infrastructure, leading carriers such as Verizon to pair fixed-wireless offerings with millimeter-wave DAS rollouts to sustain service quality. Venue owners now link property valuations to guaranteed indoor connectivity, compelling investment decisions even in cost-sensitive commercial real-estate segments.

Building codes modeled on the International Fire Code require 95% signal coverage throughout facilities and 99% in critical zones such as stairwells, creating non-discretionary demand for public-safety DAS. Annual recertification under National Fire Protection Association rules adds a recurring-services layer to revenue streams. As mandates spread to hospitals and transit hubs, public-safety DAS is becoming baseline building infrastructure rather than an optional amenity.

Deployments that must satisfy four or more mobile network operators can stall for 6-12 months while parties align on design, signal sources, and frequency clearance. Digital DAS platforms lighten this burden by offering software-defined flexibility, but neutral-host integrators who broker end-to-end solutions frequently expedite rollouts by absorbing the complexity on behalf of property owners.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Passive architectures captured a 63% distributed antenna systems market share in 2024, appealing to owners of mid-sized venues who prioritize low installation cost and simple maintenance. These systems route RF over coaxial cables and splitters, eliminating the need for extensive active electronics and thereby shrinking power requirements. Hybrid DAS, combining fiber backhaul and passive distribution, is forecast to grow at a 9.06% CAGR as it balances performance and budget constraints in hospitality properties and academic campuses. Active DAS retains its role in large stadiums and airports where blanket coverage and high capacity override cost concerns, while digital DAS gains traction for its software-defined flexibility that future-proofs multi-operator support.

Converging technology roadmaps blur historical boundaries among categories. Corning's Everon 5G Enterprise Radio Access Network integrates small-cell radios with DAS head-ends, trimming installation time 75% and ownership costs 50% compared with earlier systems. Vendors increasingly highlight energy savings and modular scalability, positioning next-generation platforms to satisfy both performance and sustainability requirements without locking buyers into fixed topologies.

Global Distributed Antenna Systems Market Report is Segmented by Type (Active, Passive, and More), End-User (Manufacturing, Healthcare, Government and Public Safety, Transportation and Logistics, Sports and Entertainment Venues, and More), Application (Enterprise DAS, Public Safety DAS, Neutral-Host / Multi-Operator DAS), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America led with a 39% distributed antenna systems market share in 2024, propelled by strict public-safety codes and rapid 5G rollouts. Requirements embedded in the International Fire Code and National Fire Protection Association standards create mandatory demand regardless of macroeconomic cycles. Carriers in the United States lean heavily on millimeter-wave small cells and DAS to complement macro densification, and property owners increasingly prefer neutral-host platforms that cap upfront costs while enhancing coverage.

Europe exhibits steady replacement demand as older office stock undergoes retrofit to meet revised building codes and sustainability targets. Both the United Kingdom and Germany extend early examples of multi-operator negotiation complexity, often lengthening deployment timelines but providing fertile ground for integrators able to streamline approvals. Meanwhile, government-backed broadband agendas in France and Spain channel grants toward digital infrastructure, carving a path for public-private DAS partnerships in transport hubs and healthcare campuses.

Asia-Pacific is the fastest-growing region at a 9.37% CAGR through 2030, buoyed by China's ongoing urbanization, Japan's high-density transit systems, and India's catch-up investments in premium commercial real estate. Chinese deployments align with smart-city projects that merge DAS with IoT sensor backbones, while Japanese operators prioritize seamless connectivity in metro stations and commercial complexes ahead of large sporting events. Spectrum-sharing mechanisms such as Japan's local 5G and India's private LTE licenses provide the regulatory runway for neutral-host experiments, reflecting a broader shift toward cost-optimized indoor coverage models across the region.