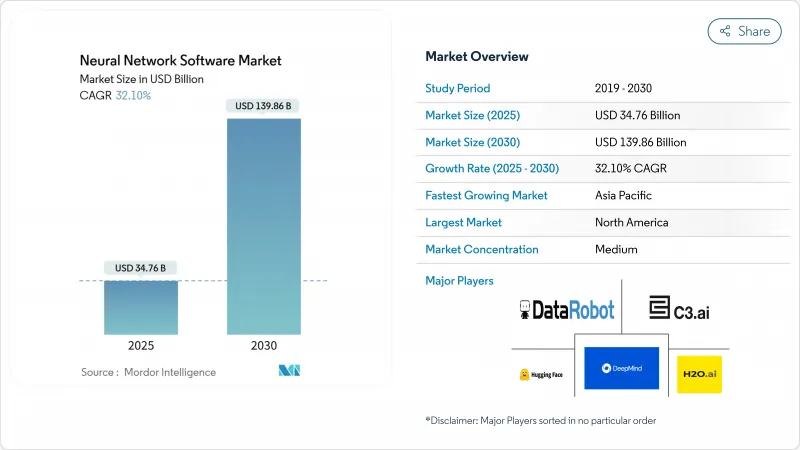

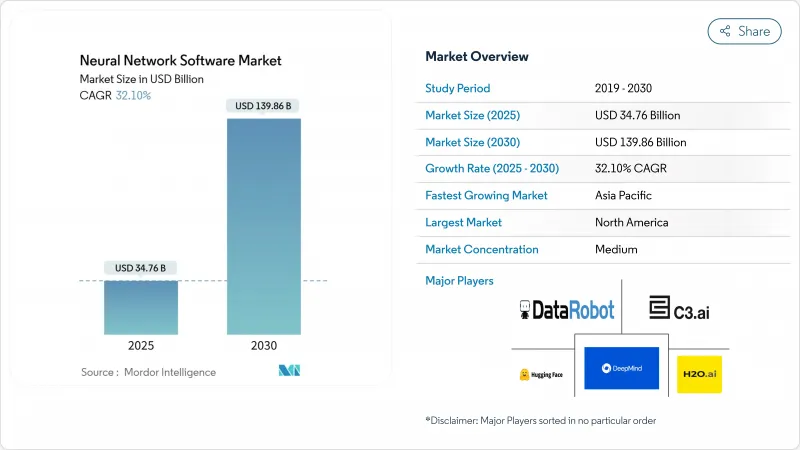

신경망 소프트웨어 시장 규모는 2025년에 347억 6,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 32.10%로 성장할 전망이며, 2030년에는 1,398억 6,000만 달러에 달할 것으로 예측됩니다.

소블린 AI 프로그램, 기반 모델 에코시스템, 채용 장벽을 낮추는 클라우드 플랫폼에 힘입어 기업이 개념 실증에서 본격적인 롤아웃으로 전환함에 따라 확대가 가속화되고 있습니다. OpenAI의 수익은 2024년 12월 55억 달러에서 2025년 6월 100억 달러로 급증하여 대규모 신경망 배포에 대한 상업 수요 증가를 보여줍니다. 중국, 일본, 인도, 한국이 대규모 언어 모델을 지역화하고 AI 클라우드를 구축하고 있기 때문에 아시아태평양이 가장 급성장하고 있습니다. 컴포넌트 동향에서 소프트웨어 툴은 대부분의 점유율을 유지하지만 기업이 통합 및 최적화 전문 지식을 요구하기 때문에 서비스 확대가 가속화되고 있습니다. 클라우드 하이퍼스케일러, 기업 소프트웨어 벤더, AI 전문 기업은 모델의 효율성, 거버넌스, 수직 솔루션으로 차별화를 추구하려고 경쟁하고 있으며, 경쟁은 격화의 길을 따라가고 있습니다.

중견기업이 자본 장벽을 없애는 매니지드 플랫폼을 채택함으로써 기업의 생성형 AI 지출은 2025년 30% 증가합니다. 레드햇이 신경 매직을 인수함에 따라 최적화된 추론 라이브러리가 하이브리드 클라우드 제품군에 추가되어 프라이빗 클러스터 내에서 효율적인 전개가 가능해졌습니다. Rackspace의 AI Anywhere 서비스는 사전 구축된 모델을 예측 가능한 구독 가격으로 패키징하여 사내 전문 지식이 없는 기업에서도 복잡한 신경망 아키텍처를 실현할 수 있도록 합니다. Google의 Gemini 제품군은 표준 클라우드 콘솔에 텍스트에서 이미지 및 비디오로 생성 API를 통합하여 개발자가 맞춤형 인프라 없이 멀티모달 추론을 테스트할 수 있게 함으로써 민주화를 확대하고 있습니다. 이러한 플랫폼의 움직임으로 가치 실현까지의 시간이 단축되고 신경망 소프트웨어 시장이 새로운 기업 채용자들 사이에서 확대됩니다.

신경망의 고장 예측 정확도가 94%에 이르면서, 제조업은 리액티브 유지 관리에서 프로액티브 유지 관리로 시프트하고 있습니다. BMW의 레겐스부르크 공장에서는 기존 부품 데이터를 분석하여 연간 500분 이상의 조립 중단을 방지하고 산업계에서 ROI의 높이를 확인하고 있습니다. 제너럴 모터스는 IoT 센서와 AI 구동 스케줄링 엔진을 연계하여 예기치 않은 다운타임을 15% 절감하고 연간 2,000만 달러를 절약했습니다. 금융기관에서는 하이브리드형 딥러닝 모델이 부정결제의 98.7%를 검출하는 등 유사한 효과를 얻을 수 있습니다. 이러한 명확한 경제적 이익은 소프트웨어의 조달주기를 가속화하고 공급업체의 신속한 도입 지원에 대한 기대를 높입니다.

AI를 채용하고 있는 기업 중 MLOps 전임의 엔지니어를 고용하고 있는 것은 불과 28%에 불과하고, 유럽 고용자의 75%는 2024년에 AI의 역할을 채우는 데 고생하고 있으며, 스킬 갭의 강건함을 부각하고 있습니다. 테크 대기업은 현재 재기능을 가속화하기 위한 공인 커리큘럼을 제공하고 있지만 커리큘럼은 급속한 프레임워크 변화에 대응할 수 없습니다. 모델을 운영하기에 충분한 실무자가 없으면 도입 기간이 장기화되고 서비스 수익이 증가하기 때문에 수요가 증가하더라도 단기적인 신경망 소프트웨어 시장의 이익에는 한계가 있습니다.

소프트웨어 프레임워크, 라이브러리 및 AutoML 제품군은 2024년 매출의 54.4%를 차지했으며, 신경망 소프트웨어 시장의 구조적 백본 역할을 명확히 했습니다. TensorFlow, PyTorch, JAX 등의 핵심 개발 키트는 여전히 필수적이지만 실험 사이클을 단축하는 턴키 모듈에 대한 수요가 증가하고 있습니다. 전문 컨설팅 및 관리 운영을 포함한 서비스는 기업이 통합, 튜닝 및 수명 주기 관리를 아웃소싱함에 따라 CAGR 35.4%로 증가하고 있습니다.

매니지드 서비스는 클라우드 제공업체가 AI 전문가를 구독 패키지에 통합하여 제품화까지의 시간을 단축함으로써 2024년 신경망 소프트웨어 시장 규모의 35.4%에 해당하는 증가분을 획득했습니다. 전문 서비스 팀은 의료 이미지 컴플라이언스와 같은 분야 특유의 요구에 부응하여 서비스 점유율을 더욱 높였습니다. 예측 기간 동안 공급업체의 차별화는 라이선싱뿐만 아니라 영역의 깊이와 결과 기반 가격 설정에 따라 달라질 것입니다.

2024년 신경망 소프트웨어 시장 점유율에서는 퍼블릭 클라우드가 61.3%를 차지했습니다. 기업은 주문형 GPU 클러스터를 활용하여 선행 투자를 피할 수 있습니다. 그러나 주권, 대기 시간, 규제 요건으로 인해 2030년까지 연평균 복합 성장률(CAGR)이 34.8%로 예측되는 하이브리드 도입으로 성장이 시프트하고 있습니다.

하이브리드 아키텍처에서 데이터는 온프레미스 또는 프라이빗 클라우드에 배치되며 모델 교육은 확장 가능한 공용 환경에서 수행됩니다. 금융 서비스 및 헬스케어 사업자는 클라우드의 규모를 활용하면서 기밀 데이터를 보호하기 위해 이 토폴로지를 채택하고 있습니다. 컨피던셜 컴퓨팅 및 페더레이티드 학습의 사용이 확대되면 하이브리드 수요가 더욱 높아지고 공급업체의 리소스 계획이 재구성될 것으로 보입니다.

신경망 소프트웨어 시장은 컴포넌트별(소프트웨어 툴, 플랫폼, 서비스), 전개 모드별(클라우드, 온프레미스, 하이브리드), 유형별(데이터 마이닝 및 아카이브, 분석 소프트웨어 등), 용도별(부정 감지, 하드웨어 진단, 재무 예측, 기타), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 헬스케어, 기타), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 확립된 벤처캐피탈 에코시스템, 첨단 클라우드 인프라, 인재풀이 밀집되어 있기 때문에 2024년 매출은 38.06%였습니다. OpenAI의 연간 경상 수익이 두 배로 100억 달러에 이르는 것은 상업적 성숙을 돋보이게 하는 반면 하이퍼스케일러는 매니지드 AI 포트폴리오를 지속적으로 확대하고 있습니다. 캐나다는 몬트리올과 토론토의 아카데믹 클러스터를 활용하고 있지만, 아시아에 대한 칩 제조 의존이 소블린 컴퓨팅의 야심을 제한하고 있습니다. 멕시코는 니어 쇼어링을 활용하여 물류와 자동차 생산에 신경망 솔루션을 통합하여 지역 공급망을 강화하고 있습니다.

아시아태평양은 CAGR 35.7%로 성장했고, 중국, 일본, 인도, 한국이 국가적 AI 클라우드를 도입함으로써, 신경망 소프트웨어 시장 규모는 2030년까지 3,000억 달러로 뛰어오를 것으로 예측되고 있습니다. 중국은 44개의 중요한 연구개발 분야 중 37개를 이끌고 있으며, 국가 재정을 산업 AI 업그레이드에 충실히 하고 있습니다. 일본은 OpenAI의 인도 태평양 지역 최초의 오피스를 개설하고, 언어적 뉘앙스와 데이터 거주법을 존중하는 엔터프라이즈 GPT 솔루션에 대한 현지 수요를 확인하고 있습니다. 인도는 정부의 샌드박스를 통해 신생 기업을 육성하고 호주와 싱가포르는 안전과 거버넌스 연구에 투자하여 다양한 지역 기회를 창출하고 있습니다.

유럽은 소블린 AI 프로젝트를 통해 기술적 자율성을 추구하고 있습니다. 엔비디아는 유럽의 데이터센터 파트너에게 3,000개의 엑사플롭스를 넘는 블랙웰 클러스터를 공급하여 규제된 AI 워크로드를 위한 대륙 척추를 형성하고 있습니다. 독일의 산업용 AI 클라우드와 프랑스의 통신 사업자 주도의 모델 호스팅 허브가 두께를 늘리고 있습니다. 그러나 인력 부족은 여전히 지속되고 있으며, 고용주의 75%가 AI 직무를 맡지 못하고 임금 인플레이션과 국경을 넘어 이주를 촉구하고 있습니다. 엄격한 GDPR(EU 개인정보보호규정)과 다가올 AI 법의 요구 사항은 거버넌스 도구를 제공하는 공급업체에게 유리하며 조달 우선 순위를 형성합니다.

The Neural Network Software Market size is estimated at USD 34.76 billion in 2025, and is expected to reach USD 139.86 billion by 2030, at a CAGR of 32.10% during the forecast period (2025-2030).

Expansion is accelerating as enterprises move from proofs of concept to full-scale rollouts, supported by sovereign-AI programs, foundation-model ecosystems, and cloud platforms that lower adoption barriers. OpenAI's revenue jump from USD 5.5 billion in December 2024 to USD 10 billion in June 2025, illustrating rising commercial demand for large-scale neural network deployments. Asia-Pacific is the fastest-growing geography because China, Japan, India, and South Korea are localizing large language models and building national AI clouds. Component trends show software tools retaining the majority share, yet services are expanding faster as enterprises seek integration and optimization expertise. Competition continues to intensify, with cloud hyperscalers, enterprise software vendors, and specialist AI firms racing to differentiate on model efficiency, governance, and vertical solutions.

Enterprise generative-AI spending is rising 30% in 2025 as mid-market firms adopt managed platforms that remove capital barriers. Red Hat's purchase of Neural Magic adds optimized inference libraries to its hybrid cloud suite, enabling efficient deployments within private clusters. Rackspace's AI Anywhere service packages pre-built models with predictable subscription pricing, making complex neural network architectures attainable for firms lacking in-house expertise. Google's Gemini family extends democratization by embedding text-to-image and video generation APIs inside standard cloud consoles, letting developers test multimodal inference without bespoke infrastructure. These platform moves reduce time-to-value and expand the neural network software market across new corporate adopters.

Manufacturers are shifting from reactive to proactive maintenance as neural networks reach 94% accuracy in fault prediction. BMW's Regensburg plant prevents over 500 minutes of annual assembly disruption by analyzing existing component data, confirming strong ROI in industrial contexts. General Motors cut unexpected downtime by 15% and saved USD 20 million yearly after linking IoT sensors with AI-driven scheduling engines. Financial institutions see parallel benefits, with hybrid deep-learning models catching 98.7% of fraudulent payments. Such clear economic gains accelerate software procurement cycles and raise expectations for rapid deployment support from vendors.

Only 28% of AI adopters employ dedicated MLOps engineers, and 75% of European employers struggled to fill AI roles in 2024, spotlighting a persistent skills gap. Tech giants now deliver certification curricula to accelerate reskilling, yet curricula cannot match rapid framework changes. Without sufficient practitioners to operationalize models, deployment timelines lengthen and service revenues climb, capping short-term neural network software market gains even as demand grows.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software frameworks, libraries, and AutoML suites delivered 54.4% of 2024 revenue, underscoring their role as the structural backbone of the neural network software market. Core development kits such as TensorFlow, PyTorch, and JAX remain essential, yet buyers increasingly demand turnkey modules that shorten experimentation cycles. Services, including professional consulting and managed operations, are rising at 35.4% CAGR as firms outsource integration, tuning, and lifecycle management.

Managed services captured incremental gains equal to 35.4% of the neural network software market size in 2024 as cloud providers embedded AI specialists within subscription packages to accelerate time-to-production. Professional service teams respond to sector-specific needs-e.g., healthcare imaging compliance-further boosting service share. Over the forecast window, vendor differentiation will hinge on domain depth and outcome-based pricing rather than licensing alone.

Public cloud retained 61.3% of the neural network software market share in 2024 because hyperscalers offer elastic compute for training and inference. Enterprises leverage GPU clusters on demand, avoiding up-front capital outlays. Yet sovereignty, latency, and regulatory requirements are shifting growth toward hybrid deployments, forecast at 34.8% CAGR to 2030.

Hybrid architectures let data reside on-premise or in private clouds while model training happens in scalable public environments. Financial services and healthcare operators adopt this topology to protect sensitive data while exploiting cloud scale. The growing use of confidential computing and federated learning will amplify hybrid demand, reshaping resource planning for vendors.

Neural Network Software Market is Segmented by Component (Software Tools, Platform, and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Type (Data Mining and Archiving, Analytical Software, and More), Application (Fraud Detection, Hardware Diagnostics, Financial Forecasting, and More), End-User Vertical (BFSI, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America held 38.06% revenue in 2024 due to an established venture-capital ecosystem, advanced cloud infrastructure, and dense talent pools. OpenAI doubling annual recurring revenue to USD 10 billion highlights commercial maturity, while hyperscalers continually widen managed-AI portfolios. Canada leverages academic clusters in Montreal and Toronto, yet chip fabrication dependence on Asia limits sovereign compute ambitions. Mexico leverages nearshoring to integrate neural network solutions in logistics and automotive production, strengthening regional supply chains.

Asia-Pacific is forecast to grow at 35.7% CAGR, with the neural network software market size jumping to USD 300 billion by 2030 as China, Japan, India, and South Korea implement national AI clouds. China leads 37 of 44 critical R&D disciplines, channelling state financing toward industrial AI upgrades. Japan hosts OpenAI's first Indo-Pacific office, confirming local demand for enterprise GPT solutions that respect linguistic nuance and data-residency laws. India nurtures start-ups through government sandboxes, while Australia and Singapore invest in safety and governance research, creating diversified regional opportunities.

Europe pursues technological autonomy through sovereign-AI projects. NVIDIA is supplying over 3,000 exaflops of Blackwell clusters to European data-center partners, forming a continental spine for regulated AI workloads. Germany's industrial AI cloud and France's telco-led model-hosting hubs add depth. However, talent shortages persist, with 75% of employers unable to staff AI roles, driving wage inflation and cross-border migration. Strict GDPR and forthcoming AI-Act requirements favor vendors offering governance tooling, shaping procurement priorities.