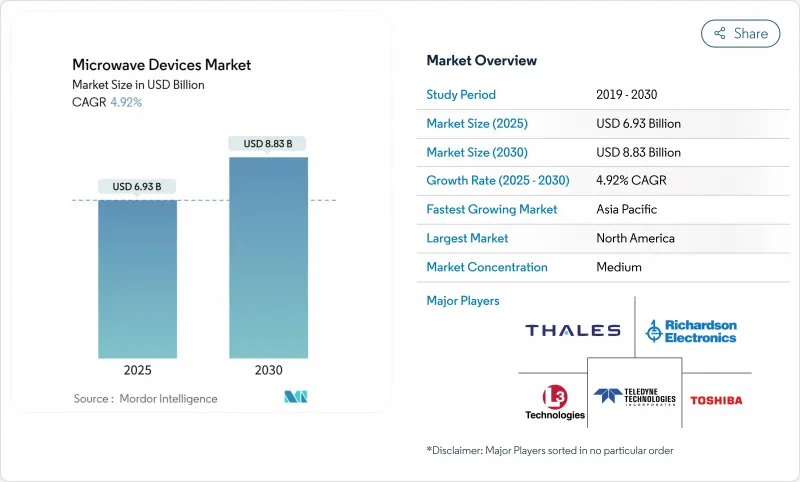

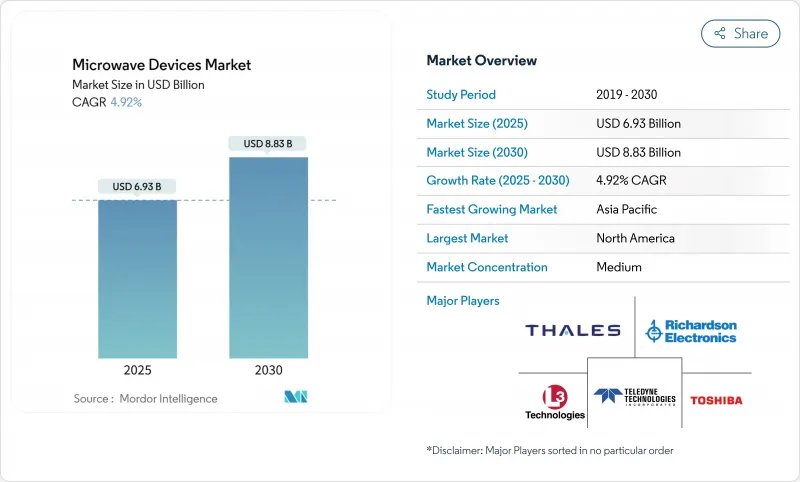

마이크로파 장치 시장은 2025년에 69억 3,000만 달러로 평가되었고, CAGR은 4.92%를 나타낼 것으로 예측되며 2030년에는 88억 3,000만 달러에 달할 전망입니다.

수익은 방위산업, 위성통신, 5G 백홀, 신흥 의료 치료 분야에 걸쳐 성숙하면서도 지속적인 수요 구조를 반영합니다. 질화갈륨(GaN) 전력 소자는 기존 갈륨비소 솔루션을 지속적으로 대체하며, 전력 밀도와 효율을 향상시키는 동시에 시스템 설치 공간과 냉각 부하를 줄이고 있습니다. 미국 국방부와 계약 중인 지향성 에너지 무기 시제품을 중심으로 한 지속적인 국방 현대화 프로그램은 고출력 주문에 대한 견고한 기반을 마련합니다. E-밴드 및 V-밴드에서 5G 고정 무선 액세스의 병행 출시로 대량 생산 핸드셋 물량이 감소하는 상황에서도 상업적 모멘텀이 유지됩니다. 의료용 마이크로파 절제 플랫폼은 병원에게 무선 주파수 대안보다 더 빠른 시술과 더 깊은 병변 침투를 제공하며 다양한 수요 구조를 완성합니다.

현대 군대 네트워크는 방해에 강한 링크와 다중 대역 유연성을 요구합니다. 최근 미군이 L3Harris와 체결한 6천만 달러 규모의 계약을 바탕으로 모듈형 VSAT 단말기를 배치한 사례는 고속 데이터 전송과 신속한 배치를 결합한 소형 시스템으로의 전환을 보여줍니다. GaN 증폭기는 현재 요구되는 전력 수준과 대역폭을 가능하게 하여 진공관 퇴출을 가속화하고 있습니다. 중국이 기가와트급 고출력 마이크로파(HPM) 무기에 병행 투자하면서 기술 경쟁이 가속화되어 방위 조달 파이프라인이 활발히 유지되고 있습니다.

고정 무선 백홀은 광섬유 비용이 여전히 부담스러운 지역에서 기가비트급 처리량을 제공합니다. FCC의 90억 달러 규모 '미국 농촌 지역 5G 기금'은 E-밴드 및 V-밴드 링크에 대한 단기 수요를 주도합니다. 위성은 또 다른 수요를 창출합니다. 스페이스X의 E-밴드 고체 전력 증폭기 1,970만 달러 규모 주문은 고주파 마이크로웨이브 페이로드의 상용화 규모를 입증합니다. 광대역 갭 소자의 높은 R&D 비용

GaN 및 SiC용 에피택셜 반응기는 수천만 달러에 달해 진입 장벽이 높습니다. 주요 공급업체들은 매출의 15-20%를 공정 최적화에 투자하는데, 이는 신규 진입자가 극복하기 어려운 장벽입니다.

2024년 마이크로파 장치 시장의 62%를 차지한 액티브 소자는 2030년까지 연평균 7.57% 성장률을 기록할 전망입니다. 크기, 무게 및 신뢰성 측면의 장점으로 인해 진공 전자 소자에서 GaN 고체 전력 증폭기로의 전환이 가속화되고 있습니다. 액티브 소자 마이크로파 장치 시장 규모는 2030년까지 53억 달러에 도달할 전망입니다. 통합 트렌드는 빔 포밍 및 이득 제어 로직을 증폭기 다이 내부에 통합하여 소프트웨어 정의 무선 플랫폼을 가능하게 합니다. 진공관 제품은 여전히 초고출력 레이더에 사용되나, 방위 프로그램이 고체 모듈을 표준화함에 따라 점유율이 감소 중입니다.

2차 효과는 패시브 소자 부문으로 확산되며, 기능이 칩 내로 이동함에 따라 개별 필터 및 커플러는 가격 압박에 직면하고 있습니다. 의료용 절제 플랫폼은 밀리초 단위 전력 변조를 위해 액티브 솔루션을 선호하여 해당 부문의 장기 성장 궤도를 강화하고 있습니다. 제품 파이프라인은 신흥 5G 매크로 무선 아키텍처와 부합하는 24V 및 28V GaN 소자에 대한 수요 증가를 보여줍니다.

마이크로파 장치 시장 보고서는 장치 유형(활성 (고체, 진공 전자), 패시브 (필터, 커플러 등)), 주파수 대역(L 및 S, C 및 X, 기타), 용도(우주 및 통신, 방위 (레이더, EW, DEW), 의료 (절제술, 영상) 등), 지역별로 분류됩니다.

북미는 2024년 38% 점유율을 유지했으며, 이는 90억 달러 규모의 연방 5G 보조금과 강력한 미국 국방 예산에 기반합니다. 마이크로파 장치 시장은 지향성 에너지 무기 프로그램과 농촌 지역 광대역 구축 사업의 지속적인 혜택을 받고 있습니다. 수출 허가 준수 요건은 비용 부담을 초래하지만, 기존 주요 기업들은 공급 차질을 완화하는 현지 조달 전략을 유지하고 있습니다.

아시아태평양 지역은 2030년까지 7.24%의 최고 연평균 성장률(CAGR)을 기록할 전망입니다. 중국은 채굴 갈륨의 98%를 장악하여 국내 팹에 비용 우위를 제공하면서 외국 통합업체들은 가격 변동성에 노출됩니다. 지역 정부들은 300mm 파워 반도체 팹에 자금을 지원하며, 인도의 신규 설계사들은 RF 프런트엔드 혁신을 위한 인재 풀을 확대합니다. 한국과 일본은 첨단 테스트 및 패키징 역량을 공급하며 자급자족형 가치 사슬을 강화합니다.

유럽은 주권 방위 수요와 상업 통신 확장을 균형 있게 추진합니다. EU 정책 인센티브는 GaN 에피택시 및 패키징 역량의 현지화를 목표로 합니다. 대서양 횡단 파트너십을 통해 유럽의 RF 설계는 북미 팹에서 파일럿 생산된 후 대량 생산을 국내 라인으로 환원하여 지정학적 위험을 완화합니다. 지속가능성 지침은 네트워크 사업자들이 신규 5G 및 차세대 6G 노드에서 에너지 효율적인 GaN 플랫폼으로 전환하도록 추가로 촉진합니다.

The microwave devices market reached a value of USD 6.93 billion in 2025 and is forecast to climb to USD 8.83 billion by 2030, reflecting a 4.92% CAGR.

Gains track a mature yet durable demand profile spanning defense, satellite communications, 5G back-haul, and emerging medical therapies. Gallium nitride (GaN) power devices continue to displace legacy gallium arsenide solutions, improving power density and efficiency while trimming system footprint and cooling loads. Ongoing defense modernization programs, highlighted by directed-energy weapon prototypes now on contract with the U.S. Department of Defense, underpin a robust baseline of high-power orders. Parallel roll-outs of 5G fixed-wireless access in the E- and V-bands sustain commercial momentum even as mass-tier handset volumes soften. Medical microwave ablation platforms round out a diversified demand stack, offering hospitals faster procedures and deeper lesion penetration than radiofrequency alternatives.

Modern armed-forces networks require jam-resilient links and multi-band versatility. Recent U.S. Army fielding of modular VSAT terminals, backed by a USD 60 million contract with L3Harris, illustrates the shift toward compact systems that merge high data rates with quick deployment. GaN amplifiers enable the power levels and bandwidth now specified, speeding the retirement of vacuum tubes. Parallel Chinese investment in gigawatt-class high-power microwave (HPM) weapons fuels a technology race that keeps defense procurement pipelines active.

Fixed-wireless backhaul offers gigabit-class throughput where fiber costs remain prohibitive. The FCC's USD 9 billion 5G Fund for Rural America anchors near-term demand for E- and V-band links. Satellites add another pull: a USD 19.7 million order from SpaceX for E-band solid-state power amplifiers affirms commercial scale for high-frequency microwave payloads.

Epitaxial reactors for GaN and SiC run into the tens of millions of dollars, creating high entry barriers. Leading suppliers devote 15-20% of turnover to process optimization, a hurdle few new entrants can clear.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Active devices accounted for 62% of the microwave devices market in 2024 and advanced at a 7.57% CAGR to 2030. Size, weight, and reliability advantages are accelerating the swap from vacuum electron devices to GaN solid-state power amplifiers. The Microwave devices market size for active devices is on track to reach USD 5.3 billion by 2030. Integration trends fold beam-forming and gain-control logic into the amplifier die, enabling software-defined radio platforms. Vacuum tube products still serve ultra-high-power radar, but cede volume share as defense programs standardize on solid-state modules.

Second-level effects cascade into the passive segment, where discrete filters and couplers face pricing pressure as functions move on-chip. Medical ablation platforms prefer active solutions for millisecond-scale power modulation, reinforcing the segment's long-term growth trajectory. Product pipelines show rising demand for 24 V and 28 V GaN devices that align with emerging 5G macro radio architectures.

The Microwave Devices Market Report is Segmented by Device Type (Active [Solid-State, Vacuum Electron] and Passive [Filters, Couplers, Etc. ]), Frequency Band (L and S, C and X, and More), Application (Space and Communication, Defense [Radar, EW, DEW], , Medical [Ablation, Imaging] and More), and Geography.

North America retained a 38% stake in 2024, anchored by USD 9 billion in federal 5G subsidies and strong U.S. defense budgets. The microwave devices market continues to benefit from directed-energy weapon programs and rural broadband build-outs. Export-license compliance introduces cost friction, but established primes sustain local sourcing strategies that cushion supply disruptions.

Asia Pacific delivers the highest 7.24% CAGR to 2030. China controls 98% of mined gallium, giving domestic fabs cost leverage while exposing foreign integrators to price volatility. Regional governments fund 300 mm power-semiconductor fabs, and India's newly opened design houses add talent depth for RF front-end innovation. South Korea and Japan supply advanced test and packaging capacity, reinforcing a self-contained value chain.

Europe balances sovereign defense needs with commercial telecom expansion. EU policy incentives aim to localize GaN epitaxy and packaging capacity. Cross-Atlantic partnerships send European RF designs to North American fabs for pilot runs, then bring volume back to domestic lines, mitigating geopolitical risk. Sustainability directives further nudge network operators toward energy-efficient GaN platforms in new 5G and future 6G nodes.