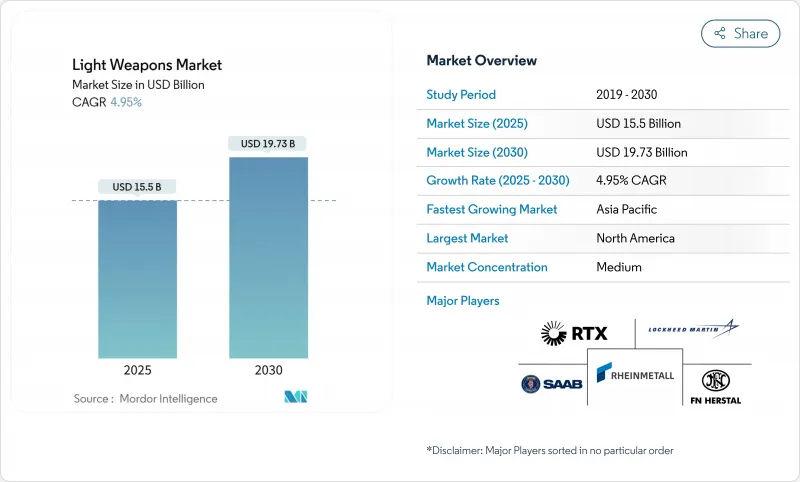

경무기 시장 규모는 2025년 155억 달러로 평가되었고, 2030년 197억 3,000만 달러에 이를 것으로 예측되며, CAGR은 4.95%를 나타낼 전망입니다.

이러한 꾸준한 성장은 지정학적 위험 증가에 대응한 국방 예산 확장에서 비롯되었으며, 2024년 전 세계 군사 지출은 9.4% 증가한 2조 7,180억 달러를 기록했습니다. 조달 우선순위는 휴대용 정밀 시스템에 집중되는 한편, 해군 근접 방어 프로그램과 폴리머 복합 탄약은 병행되는 현대화 흐름을 보여줍니다. 기술 융합(특히 AI 기반 사격 통제 모듈)은 군대가 기존 장비를 전면 교체하는 것보다 낮은 비용으로 업그레이드할 수 있게 합니다. 공급업체 간 경쟁은 여전히 완만합니다. 기존 계약업체들은 규모와 규정 준수 전문성을 통해 입지를 지키고 있지만, 틈새 혁신 기업들은 소프트웨어 중심 차별화를 활용하고 있습니다. 원자재 가격 변동성과 강화되는 무기 수출 규정이 성장을 억제하지만, 지역적 분쟁 고조로 인한 수요 증가를 상쇄하지는 못합니다.

2024년 유럽 군사 지출은 NATO 국가들이 러시아의 우크라이나 침공에 대응하며 17% 증가한 6,930억 달러를 기록했습니다. 폴란드는 2025년까지 국방비를 GDP의 4.7%로 증액할 예정이며, 독일의 1,000억 유로(1,090억 달러) 규모 특별 기금은 장기적 의지를 강조합니다. 유럽연합(EU)의 ‘유럽 재무장(ReArm Europe)’ 제안은 8,000억 유로(8,700억 달러)를 동원하는 것을 목표로 하며, 여기에는 공동 조달 대출 1,500억 유로(1,630억 달러)가 포함됩니다. 이 계획은 독일의 라인메탈과 체결한 85억 유로(92억 달러) 규모의 탄약 계약과 같은 상당한 보병 무기 주문으로 이어져 경무기 시장의 수요를 강화하고 있습니다.

우크라이나 전장 경험은 휴대용 미사일이 중무장 부대를 무력화하는 방식을 보여주며, 지역 행위자들이 유사한 자산을 비축하도록 촉진하고 있습니다. 유럽의 무기 수입은 2014-2018년 대비 2019-2023년에 두 배로 증가했습니다. 대만의 스위치블레이드 300 로이팅 무기(3억 6,020만 달러 규모) 구매는 아시아태평양 지역의 도입 확대를 부각시킵니다. 미 육군 1,300만 달러 프로그램으로 배치된 SMASH 2000L 같은 스마트 소총 조준경은 대(對)드론 대응을 보여줍니다. 이처럼 비대칭 교리는 경무기 시장에서 다목적 및 소형 제품의 수요를 유지합니다.

미국 상무부는 2024년 5월 총기 수출 규정을 강화하여 다수 상업 거래에 대해 원칙적으로 불허 입장을 취했습니다. 워싱턴의 개정된 재래식 무기 이전 정책은 인권 침해 가능성을 높이는 수출을 차단합니다. 현재 113개국이 가입한 무기거래조약(ATT)은 사전 위험 평가를 의무화합니다. 영국의 2024년 수출 통제 개정안은 신기술 분야를 추가로 포함시켰다. 규정 준수 부담과 허가 불확실성은 중소 수출업체의 경무기 시장 진입을 저해합니다.

MANPADS(휴대용 지대공 미사일)는 2024년 매출의 33.35%를 차지하며 경무기 시장 규모에서 가장 높은 비중을 기록했는데, 이는 대만 및 동유럽 동맹국들의 스팅어급 미사일 광범위한 조달을 반영한 결과입니다. 유인 드론이 대체 위협으로 부상하고 있으나, 확립된 물류망과 즉각적인 가용성으로 수요는 탄력성을 유지하고 있습니다. 중기관총과 박격포는 수명 연장 계약을 통해 틈새 시장을 유지하는 반면, 대드론 소총은 신생이지만 중요한 카테고리를 형성하고 있습니다.

수류탄 및 수류탄 발사기는 8.91%의 가장 빠른 연평균 성장률(CAGR) 전망을 기록했습니다. 콜트 CZ가 도입한 Mk 47과 같은 프로그래밍 가능한 공중 폭발탄 및 정밀 발사기는 유도형 서브탄약으로의 가치 이동을 보여줍니다. 도시전 교리와 치안 요구사항은 군민 겸용 판매를 뒷받침합니다. 이러한 추세들은 경무기 시장 내 제품 구성 다각화를 보장합니다.

유도탄은 2024년 매출의 55.51%를 차지했으며, 7.40%의 CAGR로 다른 기술을 앞지를 전망으로, 경무기 시장 점유율 계층 구조 내에서의 비중을 강조합니다. 빔 라이딩 레이저 모델과 적외선 발사 후 방치 미사일은 조작자의 노출을 줄이고 부수적 피해 기준을 충족시키며, 탈레스의 경량 다목적 미사일 시험에서 입증되었습니다.

비유도 시스템은 가격 경쟁력과 전자전(EW) 방해에 대한 내구성으로 인해 여전히 사용됩니다. 예산 제약이 있는 군대는 공급 안정성을 보장하기 위해 저렴한 탄약을 비축합니다. 전자전 위협이 확대됨에 따라 스마트 무기와 비유도 무기를 병행 보유하는 이중 재고 전략은 유연성을 제공하며, 경무기 산업 내에서 비유도 제품의 안정적인 틈새 시장을 확보합니다.

2024년 북미 지역은 38.70%의 매출 점유율로 시장을 주도했으며, 이는 미국의 9,970억 달러 국방 예산에 기반합니다. 강력한 국내 주문은 규모의 경제를 뒷받침하는 한편, 대외 군사 판매(FMS)는 동맹국 함대로의 진출을 확대합니다. 록히드 마틴의 미사일 및 화력 통제 부문 매출은 2025년 1분기 미결 주문 가시성 개선에 힘입어 13% 증가한 33억 7천만 달러를 기록했습니다.

아시아태평양 지역 경무기 시장은 2030년까지 연평균 7.65% 성장률(CAGR)을 기록하며 가장 빠른 지역 성장률을 보일 전망입니다. 인도는 2024-2029 회계연도 동안 국방 자본 지출이 연평균 20% 증가함에 따라 계약의 65%를 차지하는 현지 조달 의무를 유지하고 있습니다. 필리핀은 ‘리호라이즌 3’ 계획에 350억 달러를 배정했으며, 일본의 21% 예산 증액은 1952년 이후 최대 규모다. 중국 관련 안보 불안 고조로 다국적 재무장이 촉진되며 공급업체에 방대한 수주 파이프라인이 형성되고 있습니다.

유럽의 군사비 지출이 전년 대비 17% 증가한 6,930억 달러로 급증하며 가장 즉각적인 조달 급증을 초래하고 있습니다. 독일의 1000억 유로(1090억 달러) 기금, 폴란드의 GDP 대비 4.7% 목표, EU의 재군비(ReArm) 제안은 보병 무기의 광범위한 다년간 현대화를 뒷받침합니다. 영국-독일 합동 장거리 타격 미사일 같은 공동 프로그램은 유럽 내 산업적 결속력을 보여주며 지역 경무기 시장을 활성화합니다.

The light weapons market size was valued at USD 15.50 billion in 2025 and is forecasted to reach USD 19.73 billion by 2030, translating into a 4.95% CAGR.

This steady advance stems from defense-budget expansion in response to heightened geopolitical risk, with global military expenditure rising 9.4% to USD 2.718 trillion in 2024. Procurement priorities concentrate on man-portable precision systems, while naval close-in programs and polymer-composite ammunition illustrate parallel modernization currents. Technology convergence-especially AI-enabled fire-control modules-allows armed forces to upgrade legacy inventories at a lower cost than wholesale fleet replacement. Vendor competition remains moderate: established contractors guard incumbency through scale and compliance expertise, yet niche innovators exploit software-centric differentiation. Raw-material price volatility and tightening arms-export rules temper growth but outweigh the demand pull created by escalating regional flashpoints.

European military outlays climbed 17% to USD 693 billion in 2024 as NATO states reacted to Russia's invasion of Ukraine. Poland will raise defense spending to 4.7% of GDP by 2025, while Germany's EUR 100 billion (USD 109 billion) special fund underlines long-term commitment. The European Union's ReArm Europe proposal aims to mobilize EUR 800 billion (USD 870 billion), which includes EUR 150 billion (USD 163 billion) in joint-procurement loans. This initiative has led to significant infantry weapon orders, such as Germany's EUR 8.5 billion (USD 9.2 billion) ammunition contract with Rheinmetall, strengthening the demand in the light weapons market.

Ukraine's battlefield experience shows how man-portable missiles blunt heavier forces, prompting regional actors to stockpile similar assets; European arms imports doubled in 2019-2023 versus 2014-2018. Taiwan's purchase of Switchblade 300 loitering munitions worth USD 360.2 million highlights Asia-Pacific uptake. Smart-rifle scopes such as the SMASH 2000L, fielded under a USD 13 million US Army program, illustrate counter-drone. Asymmetric doctrine thus sustains multi-role, low-footprint products within the light weapons market.

The US Commerce Department imposed tighter firearms-export rules in May 2024, presuming denial for many commercial deals. Washington's revised Conventional Arms Transfer policy blocks shipments likely to enable rights abuses. The Arms Trade Treaty, now at 113 parties, mandates prior risk assessments.The UK's 2024 Export Control amendment added emerging-tech coverage. Compliance overhead and license uncertainty curb smaller exporters' access to the light weapons market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

MANPADS generated 33.35% of 2024 revenue, the highest individual slice of the light weapons market size, reflecting broad procurement of Stinger-class missiles by Taiwan and Eastern European allies. Although loitering drones threaten substitution, established logistics chains and immediate availability keep demand resilient. Heavy machine guns and mortars retain niche relevance through service-life extension contracts, while counter-drone rifles form a fledgling but important category.

Grenades and grenade launchers delivered the fastest 8.91% CAGR outlook. Programmable air-burst rounds and precision launchers, such as the Mk 47 acquired by Colt CZ, illustrate value migration toward guided sub-munitions. Urban warfare doctrines and policing requirements underpin dual-use sales. Together, these trends ensure product-mix diversification inside the light weapons market.

Guided munitions commanded 55.51% revenue in 2024 and will outpace other technologies at 7.40% CAGR, underlining their mass in the light weapons market share hierarchy. Beam-riding laser models and IR fire-and-forget missiles reduce operator exposure and meet collateral-damage thresholds, as evidenced by Thales' Lightweight Multi-role Missile trials.

Unguided systems persist due to their price advantage and resilience against jamming. Budget-constrained forces stockpile inexpensive rounds to ensure supply sufficiency. As electronic warfare (EW) threats expand, dual inventories-smart and dumb-provide hedge flexibility, securing a stable niche for unguided products within the light weapons industry.

The Light Weapons Market Report is Segmented by Type (Heavy Machine Guns (HMGs), Grenades and Grenade Launchers, Mortars, and More), Technology (Guided and Unguided), Platform (Land-Based, Airborne, and Naval), End-User (Army, Special Forces, and More), Material (Steel and Specialty Alloys, Polymer Composites, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led the market with 38.70% revenue in 2024, anchored by the United States' USD 997 billion defense budget. Robust domestic orders underpin economies of scale, while Foreign Military Sales extend reach into allied fleets. Lockheed Martin's Missiles and Fire Control sales climbed 13% to USD 3.37 billion in Q1 2025 as backlog visibility improved.

Asia-Pacific's light weapons market size is projected to grow at a 7.65% CAGR through 2030, the fastest regional rate. India's 20% compound defense-capital growth through FY24-FY29 sustains local sourcing mandates covering 65% of contracts. The Philippines earmarked USD 35 billion under Re-Horizon 3, while Japan's 21% budget hike marks the largest since 1952. Rising China-related security anxiety fuels multi-country rearmament, giving suppliers an expansive pipeline.

Europe's surge in military spending-up 17% year-on-year to USD 693 billion-creates the most immediate procurement spike. Germany's EUR 100 billion (USD 109 billion) fund, Poland's 4.7% of GDP target, and the EU's ReArm proposal underpin a broad, multi-year refresh of infantry weapons. Joint programs such as the UK-Germany deep-strike missile demonstrate intra-European industrial cohesion, boosting the regional light weapons market.