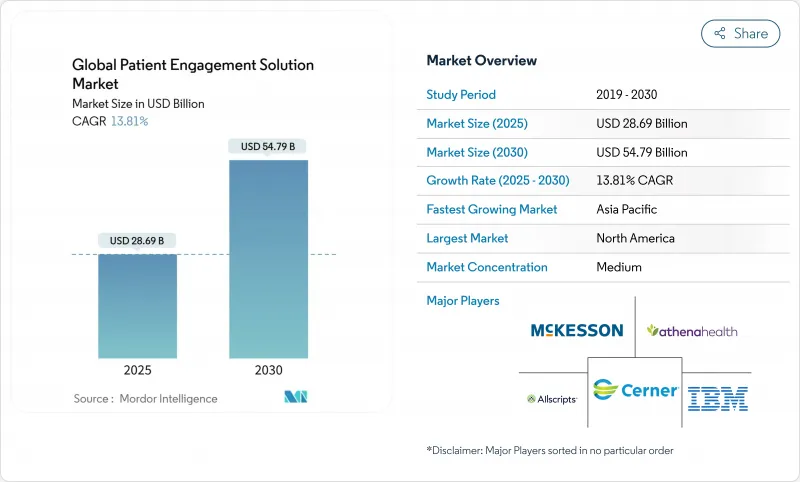

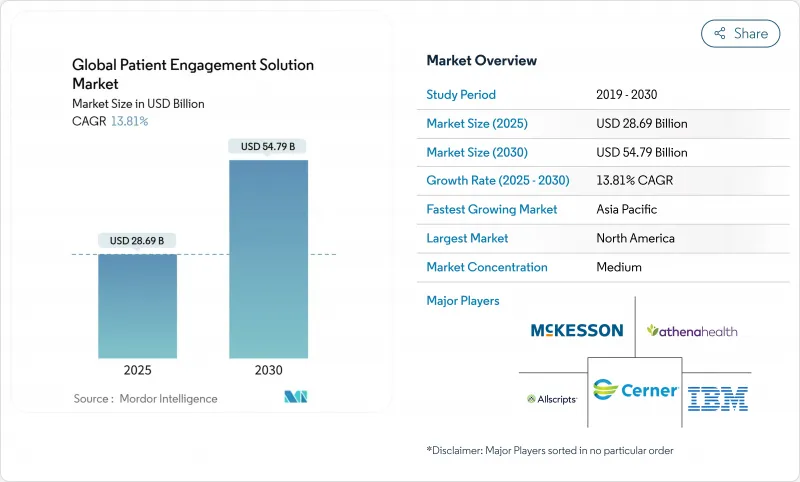

세계의 환자 참여 솔루션 시장 규모는 2025년에 286억 9,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 13.81%로 성장할 전망이며, 2030년에는 547억 9,000만 달러에 이를 것으로 예측됩니다.

성장을 뒷받침하는 것은 헬스케어 부문이 가치 기반 케어로 축족을 옮기고 있는 것, AI를 활용한 참여 플랫폼이 급속히 성숙하고 있는 것, 커넥티드 환자는 치료 계획에 충실하다는 근거가 높아지고 있다는 것입니다. 북미는 계속 페이스를 잡고 있지만, 아시아태평양의 디지털 헬스에 대한 기세, 스마트폰에 대한 폭넓은 접근, 유리한 정책 전환으로 이 지역은 크게 성장하고 있습니다. 클라우드 구축, 옴니채널화, EHR 상호 운용성 강화로 턴키형 엔터프라이즈급 솔루션을 제공할 수 있는 벤더의 경쟁 우위성이 확고해지고 있습니다. 견고한 수요 신호에도 불구하고 데이터 보안 준수 및 인적 자원 부족의 지속은 역풍이 되어, 당면한 도입이 억제될 수 있습니다.

병원에서는 대화형 인공지능, 예측 분석, 자동 방어를 프런트 오피스 및 임상 워크플로에 통합합니다. 조사 대상이 된 의료 시스템의 82%가 2년 이내에 AI 기반 참여 도구의 도입을 계획하고 있습니다. 조기에 도입된 의료기관에서는 대기 시간 단축, 케어의 부드러운 이행, 임상의 만족도 향상이 보고되고 있으며, 그 주된 이유는 가상 어시스턴트가 차트에 사전에 입력하여 일상적인 문의를 처리하기 때문입니다. Philips에 따르면 85%의 경영진이 현재 제너레이션 AI 참여 프로젝트에 구체적인 예산을 할당하고 있습니다. 알고리즘이 성숙함에 따라 병원은 예약 준수율 향상과 노쇼 감소를 목격하고 환자의 충성도를 강화하는 동시에 측정 가능한 수익 증가를 창출하고 있습니다.

스마트폰 중심의 케어 경로를 통해 환자는 실시간으로 의료 데이터, 채팅봇 및 행동 너지에 액세스할 수 있어 대규모 의료 시스템 전반에 걸쳐 포털에 대한 로그인률이 증가하고 있습니다. 아시아태평양은 모바일 헬스 다운로드 수를 선도하고 있지만 북미 공급자는 사용자 1인당 세션 시간을 가장 오래 기록하고 있습니다. 의료 기관은 비디오 방문, 보안 메시징 및 원격 생체 캡처를 단일 앱으로 통합하여 소비자를 위한 하이테크 경험을 반영하는 옴니 채널을 구축합니다. 이 접근 방식은 콜센터에 대한 문의를 줄이고 후속 스케줄링을 가속화하며 비용 절감과 관리 연속성을 향상시킵니다.

헬스케어 조직은 환자 참여 강화 및 엄격한 데이터 보호 요구 사항의 균형을 유지해야 하므로 데이터 보안 문제가 시장 성장의 주요 억제요인이 되었습니다. 2009년부터 2022년까지 5,000건 이상의 의료 데이터 침해가 보고되었으며, 의료 산업은 사용자 친화적인 참여 솔루션을 유지하면서 견고한 보안 프레임워크를 구축해야 합니다. 미국의 HIPAA 및 유럽 GDPR(EU 개인정보보호규정)과 같은 규제의 도입은 특히 IT 자원이 제한된 소규모 의료 제공업체에게 채택을 지연시킬 수 있는 컴플라이언스 과제를 낳고 있습니다. 이러한 과제를 해결하기 위해 HITRUST Common Security Framework(CSF)와 같은 프레임워크를 채용하는 의료기관이 늘어나고 있지만, 도입에는 기술과 전문지식 모두에 엄청난 투자가 필요합니다. 사용자 경험을 손상시키지 않는 안전한 인증 메커니즘이 특히 어려움을 겪고 있으며, 복잡한 보안 조치는 환자의 참여율을 낮추고 가치있는 솔루션의 효과를 제한할 수 있습니다.

2024년 환자 참여 솔루션 시장에서 소프트웨어는 56.31%에서 가장 큰 점유율을 차지했으며, 헬스케어 조직 전체의 디지털 전환 이니셔티브의 핵심 역할을 하고 있습니다. 이러한 이점은 기존의 의료 IT 인프라와 원활하게 통합할 수 있는 소프트웨어의 능력으로 인해 의미 있는 환자와의 교류에 필요한 기능을 제공합니다. 환자 포털, 모바일 애플리케이션 및 원격 의료 플랫폼은 가장 널리 사용되는 소프트웨어 솔루션으로 예약 스케줄링에서 보안 메시징, 의료 기록에 대한 액세스까지 다양한 기능을 제공합니다. 서비스 분야는 현재 규모가 작은 것으로, 2025-2030년 CAGR 16.09%로 가장 급속히 성장할 것으로 전망됩니다. 이는 의료기관이 기술 투자를 최대한 활용하기 위한 도입 지원, 교육 및 지속적인 유지보수의 중요성을 인식하기 때문입니다. 키오스크 단말기, 태블릿 단말기 및 웨어러블 단말기와 같은 하드웨어 구성 요소는 특히 환자와 직접 상호 작용해야 하는 임상 현장에서 생태계 전체에서 보조적이지만 필수적인 역할을 합니다.

헬스케어 리더의 85%가 임상의의 생산성 및 환자 참여도를 높이기 위해 일반 인공지능에 투자하는 것처럼 소프트웨어 상황이 급속히 진화하고 있으며 인공지능 통합이 결정적인 동향으로 떠오르고 있습니다. 상호 운용성은 중요한 초점이 되고, 의료 조직은 통합된 환자 경험을 창출하기 위해 서로 다른 시스템 간에 데이터를 원활하게 교환할 수 있는 솔루션을 선호합니다. 클라우드 기반 소프트웨어 제공 모델로의 전환은 확장성, 접근성, IT 오버헤드 감소 등의 이점을 배경으로 가속화되었습니다. 서비스 제공업체는 기본적인 구현에 그치지 않고 전략적 컨설팅, 워크플로우 최적화, 지속적인 개선 프로그램 등 의료 기관이 환자 참여에 대한 투자로부터 최대한의 가치를 끌어낼 수 있는 서비스 제공을 확대하고 있습니다. 컴포넌트 에코시스템은 의료 제공 모델의 변화에 따라 계속 진화하고 있으며, 기존의 임상 환경 이외의 케어 제공을 지원하는 솔루션이 점점 더 중요해지고 있습니다.

웹 및 클라우드 기반 솔루션은 2024년에 총 70.31%의 점유율을 차지했으며, 시장을 독점했습니다. 이것은 레거시 온프레미스 시스템에서 결정적인 전환을 반영합니다. 특히 클라우드 기반 솔루션은 2025-2030년 CAGR 18.94%로 폭발적인 성장을 전망하고 있습니다. 이는 의료기관이 확장성, 접근성, IT 부담 감소 등의 이점을 인식하고 있기 때문입니다. 클라우드 구축은 온프레미스 시스템보다 77% 저렴하며 유지보수 비용도 대폭 절감할 수 있기 때문에 클라우드 도입의 경제적 이점은 큽니다. 온프레미스 솔루션은 주로 특정 보안 요구 사항과 연결 제한이 있는 환경에서 관련성을 유지하지만 클라우드의 보안 기능이 성숙하고 연결 인프라가 개선됨에 따라 시장 점유율은 계속 감소하고 있습니다.

클라우드 기반 제공 모델로의 전환은 실시간 데이터 분석, 원활한 멀티 디바이스 경험, 진화하는 헬스케어의 필요에 대응하는 신속한 기능 업데이트 등 이전에는 비실용적이었던 새로운 기능을 가능하게 합니다. 헬스케어 조직은 보안, 컴플라이언스 및 접근성 요구사항의 균형을 맞추기 위해 클라우드와 온프레미스 요소를 결합한 하이브리드 방식을 채택하는 경향이 커지고 있습니다. 클라우드 솔루션의 비용 구조는 일반적으로 '사용자 1인당 월별' 모델을 따르며 대규모 선행 투자를 위한 자금이 없는 소규모 의료 조직에 특히 매력적입니다. 이전에는 클라우드 배포가 제한된 보안 문제는 고급 암호화, 다중 요소 인증 및 컴플라이언스 인증을 통해 해결되고 있으며, 많은 클라우드 제공업체는 기존 온프레미스 배포의 보안 기능을 능가합니다. 클라우드 기반 솔루션의 유연성은 헬스케어가 혼란될 때 특히 가치를 발휘하며, 환자의 요구와 케어 제공 모델의 변화에 따라 새로운 참여 기능을 신속하게 배포할 수 있습니다.

북미는 2024년에 42.15%의 점유율을 획득하여 환자 참여 솔루션 시장에서 지배적인 지위를 유지했습니다. 이것은 첨단 헬스케어 인프라, 유리한 상환 정책, 디지털 건강 기술의 조기 도입이 배경에 있습니다. 이 지역의 리더십은 미닝 풀 사용 요구 사항 및 가치 기반 관리 프로그램과 같은 환자 참여 이니셔티브에 대한 규제 당국의 강력한 지원으로 강화되었습니다. 헬스케어 정보관리 시스템 협회(HIMSS)의 종합적인 조사에 따르면 미국의 의료기관의 61%가 전략계획에서 환자 체험과 참여에 대한 노력을 우선하고 있으며, 72%가 2026년까지 디지털 환자 참여 기술에 대한 투자를 늘릴 예정임을 보여주었습니다. 이 지역에서는 AI를 활용한 참여 솔루션의 통합이 특별히 진행되고 있으며, 자동 예약 스케줄링부터 개인화된 건강 추천 및 가상 어시스턴트에 이르기까지 다양한 애플리케이션이 제공됩니다. 캐나다와 멕시코도 비슷한 도입 궤도를 따르고 있지만, 의료 시스템의 구조와 자금 조달 메커니즘의 차이로 인해 속도가 다소 느립니다.

아시아태평양은 2025-2030년 CAGR 17.77%로 성장이 예측되어 가장 급성장하고 있는 지역 시장입니다. 이는 급속히 확대되는 헬스케어 인프라, 스마트폰의 보급률 향상, 헬스케어에 대한 기대가 높은 중류계급의 인구 증가에 추진되고 있습니다. 중국은 디지털 헬스 인프라와 환자 중심의 케어 이니셔티브에 대한 대규모 투자로 지역 성장을 이끌고 있으며, 인도는 정부의 디지털 헬스 프로그램과 급성장하는 원격 의료 부문에 견인되어 도입이 가속화되고 있습니다. 고령화가 진행되는 일본에서는 고령 환자의 원격 모니터링과 만성 질환 관리와 같은 솔루션이 점점 중시되고 있으며, 독자적인 대처 과제 및 기회가 탄생하고 있습니다. 호주와 한국은 AI와 IoT와 같은 첨단 기술을 환자 참여 플랫폼에 통합하는 최전선에 있으며, 보다 개인화된 프로액티브 케어 체험을 창출하고 있습니다. 이 지역의 성장을 더욱 뒷받침하는 것은 의료비 증가와 도시 지역과 농촌 지역 모두에서 의료 접근성 개선에 대한 강한 관심입니다.

유럽은 큰 시장 점유율을 차지하고 있으며 독일, 영국, 프랑스 등의 국가들이 환자 참여 솔루션의 도입을 주도하고 있습니다. 이 지역의 엄격한 데이터 보호 규정, 특히 GDPR(EU 개인정보보호규정)은 향상된 개인 정보 보호 기능과 투명한 데이터 거버넌스 관행을 갖춘 참여 플랫폼 개발을 형성합니다. 중동 및 아프리카은 현재 시장 점유율이 작고, 특히 걸프 협력 회의(GCC) 국가에서는 도입이 확대되고 있으며, 의료 근대화 이니셔티브가 환자 참여 기술에 대한 투자를 촉진하고 있습니다. 남미는 유망한 성장 잠재력을 보여주고 있으며, 의료 제공업체가 디지털 참여 솔루션을 통해 액세스 과제를 해결하려고 하기 때문에 브라질이 이 지역의 채용을 선도하고 있습니다. 환자 참여 시장의 세계 특성은 점점 더 분명해지고 있으며, 솔루션은 지리적 경계를 넘어서는 핵심 기능을 유지하면서 지역 특유의 의료 문제를 해결하기 위해 적응되고 있습니다.

The Global Patient Engagement Solution Market size is estimated at USD 28.69 billion in 2025, and is expected to reach USD 54.79 billion by 2030, at a CAGR of 13.81% during the forecast period (2025-2030).

Growth is propelled by the healthcare sector's pivot toward value-based care, the rapid maturation of AI-enabled engagement platforms, and mounting evidence that connected patients are more adherent to treatment plans. North America continues to set the pace, but Asia-Pacific's digital-health momentum, broad smartphone access, and favorable policy shifts position the region for outsized gains. Cloud deployment, omni-channel engagement, and tighter EHR interoperability are solidifying competitive advantages for vendors that can offer turnkey, enterprise-grade solutions. Despite strong demand signals, data-security compliance and persistent talent shortages present headwinds that could temper adoption in the near term.

Hospitals are embedding conversational AI, predictive analytics, and automated triage into front-office and clinical workflows. Eighty-two percent of health systems surveyed plan to implement AI-enabled engagement tools within two years. Early adopters report shorter wait times, smoother care transitions, and higher clinician satisfaction, largely because virtual assistants pre-populate charts and handle routine queries. Philips found that 85% of executives now allocate specific budgets for generative-AI engagement projects.As algorithms mature, hospitals see improved appointment adherence and a decline in no-shows, producing measurable revenue uplift while strengthening patient loyalty.

Smartphone-centric care pathways give patients real-time access to their medical data, chatbots, and behavioral nudges, which has helped lift portal log-in rates across large health systems. Asia-Pacific leads mobile-health downloads, yet North American providers record the highest per-user session length. Health organizations are layering video visits, secure messaging, and remote vitals capture into single apps, building an omni-channel presence that mirrors consumer-tech experiences. The approach reduces inbound call-center volume and accelerates follow-up scheduling, delivering cost savings and better care continuity.

Data security concerns represent a significant restraint on market growth, as healthcare organizations must balance enhanced patient engagement with stringent data protection requirements. With over 5,000 reported healthcare data breaches from 2009 to 2022, the industry faces mounting pressure to implement robust security frameworks while maintaining user-friendly engagement solutions. The implementation of regulations like HIPAA in the US and GDPR in Europe creates compliance challenges that can slow adoption, particularly for smaller healthcare providers with limited IT resources. Healthcare organizations are increasingly turning to frameworks like the HITRUST Common Security Framework (CSF) to address these challenges, but implementation requires significant investment in both technology and expertise. The need for secure authentication mechanisms that don't compromise user experience presents a particular challenge, as cumbersome security measures can reduce patient engagement rates and limit the effectiveness of otherwise valuable solutions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software commands the largest share of the Patient Engagement Solution Market at 56.31% in 2024, serving as the cornerstone of digital transformation initiatives across healthcare organizations. This dominance stems from software's ability to integrate seamlessly with existing healthcare IT infrastructure while providing the functionality necessary for meaningful patient interactions. Patient portals, mobile applications, and telehealth platforms represent the most widely adopted software solutions, with features ranging from appointment scheduling to secure messaging and access to medical records. The services segment, while currently smaller, is experiencing the fastest growth at a CAGR of 16.09% for 2025-2030, as healthcare organizations increasingly recognize the importance of implementation support, training, and ongoing maintenance to maximize their technology investments. Hardware components, including kiosks, tablets, and wearable devices, play a supporting but essential role in the overall ecosystem, particularly in clinical settings where direct patient interaction is required.

The software landscape is evolving rapidly with AI integration emerging as a defining trend, as 85% of healthcare leaders invest in generative AI to enhance clinician productivity and patient engagement. Interoperability has become a critical focus area, with healthcare organizations prioritizing solutions that can exchange data seamlessly across disparate systems to create a unified patient experience. The shift toward cloud-based software delivery models is accelerating, driven by advantages in scalability, accessibility, and reduced IT overhead. Services providers are expanding their offerings beyond basic implementation to include strategic consulting, workflow optimization, and continuous improvement programs that help healthcare organizations maximize the value of their patient engagement investments. The component ecosystem continues to evolve in response to changing healthcare delivery models, with an increasing emphasis on solutions that support care delivery outside traditional clinical settings.

Web and cloud-based solutions collectively dominate the market with a 70.31% share in 2024, reflecting healthcare's decisive shift away from legacy on-premise systems. Cloud-based solutions specifically are experiencing explosive growth at a CAGR of 18.94% for 2025-2030, as healthcare organizations recognize the advantages in scalability, accessibility, and reduced IT burden. The economic case for cloud adoption is compelling, with cloud deployments being 77% cheaper than on-premises systems and offering significant reductions in maintenance costs. On-premise solutions retain relevance primarily in settings with specific security requirements or connectivity limitations, but their market share continues to decline as cloud security capabilities mature and connectivity infrastructure improves.

The transition to cloud-based delivery models is enabling new capabilities that were previously impractical, including real-time data analytics, seamless multi-device experiences, and rapid feature updates that keep pace with evolving healthcare needs. Healthcare organizations are increasingly adopting hybrid approaches that combine cloud and on-premise elements to balance security, compliance, and accessibility requirements. The cost structure of cloud solutions, typically following a 'per user per month' model, is proving particularly attractive for smaller healthcare organizations that lack the capital for large upfront investments. Security concerns that previously limited cloud adoption are being addressed through advanced encryption, multi-factor authentication, and compliance certifications, with many cloud providers now exceeding the security capabilities of traditional on-premise deployments. The flexibility of cloud-based solutions is proving especially valuable during healthcare disruptions, enabling rapid deployment of new engagement capabilities in response to changing patient needs and care delivery models.

The Patient Engagement Solution Market Report Segments the Industry Into by Component (Hardware, Software, Services), Delivery Mode (Web-Based and Cloud-Based, On-Premise), Application (Social and Behavioral Management, and More), End User (Providers, Payers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America maintains its dominant position in the Patient Engagement Solution Market with a 42.15% share in 2024, driven by advanced healthcare infrastructure, favorable reimbursement policies, and early adoption of digital health technologies. The region's leadership is reinforced by strong regulatory support for patient engagement initiatives, including Meaningful Use requirements and value-based care programs that incentivize provider investments in engagement technologies. A comprehensive survey by the Healthcare Information and Management Systems Society (HIMSS) indicates that 61% of U.S. healthcare organizations have prioritized patient experience and engagement initiatives in their strategic plans, with 72% planning to increase investments in digital patient engagement technologies by 2026. The integration of AI-powered engagement solutions is particularly advanced in this region, with applications ranging from automated appointment scheduling to personalized health recommendations and virtual health assistants. Canada and Mexico are following similar adoption trajectories, though at a somewhat slower pace due to differences in healthcare system structures and funding mechanisms.

Asia-Pacific represents the fastest-growing regional market with a projected CAGR of 17.77% for 2025-2030, fueled by rapidly expanding healthcare infrastructure, increasing smartphone penetration, and growing middle-class populations with higher healthcare expectations. China leads regional growth with substantial investments in digital health infrastructure and patient-centered care initiatives, while India is experiencing accelerated adoption driven by government digital health programs and a burgeoning telehealth sector. Japan's aging population is creating unique engagement challenges and opportunities, with solutions increasingly focused on remote monitoring and chronic disease management for elderly patients. Australia and South Korea are at the forefront of integrating advanced technologies like AI and IoT into patient engagement platforms, creating more personalized and proactive care experiences. The region's growth is further supported by increasing healthcare expenditure and a strong focus on improving healthcare accessibility in both urban and rural areas.

Europe holds a significant market share, with countries like Germany, the United Kingdom, and France leading adoption of patient engagement solutions. The region's strict data protection regulations, particularly GDPR, have shaped the development of engagement platforms with enhanced privacy features and transparent data governance practices. The Middle East and Africa region, while currently representing a smaller market share, is experiencing growing adoption particularly in Gulf Cooperation Council (GCC) countries where healthcare modernization initiatives are driving investments in patient engagement technologies. South America shows promising growth potential, with Brazil leading regional adoption as healthcare providers seek to address access challenges through digital engagement solutions. The global nature of the patient engagement market is increasingly evident, with solutions being adapted to address region-specific healthcare challenges while maintaining core functionality that transcends geographic boundaries.